Unlock the Secrets of 0 APR Car Loan Deals: Your Ultimate Guide to Zero-Interest Auto Financing

Unlock the Secrets of 0 APR Car Loan Deals: Your Ultimate Guide to Zero-Interest Auto Financing Carloan.Guidemechanic.com

The phrase "0 APR car loan deals" instantly sparks interest for anyone in the market for a new vehicle. Imagine driving away in a brand-new car without paying a single cent in interest over the life of your loan. It sounds like a dream come true, a financial superpower that saves you thousands.

But is it truly as simple and straightforward as it appears? As an expert in automotive financing, I can tell you that while these zero-interest offers are undeniably attractive, they come with a specific set of circumstances, requirements, and sometimes, subtle trade-offs that every smart buyer needs to understand. This comprehensive guide will demystify 0 APR car loans, helping you navigate the fine print, maximize your chances of approval, and ultimately make the most informed decision for your next car purchase.

Unlock the Secrets of 0 APR Car Loan Deals: Your Ultimate Guide to Zero-Interest Auto Financing

We’ll dive deep into what these deals entail, who truly qualifies, and the crucial factors you need to consider before signing on the dotted line. Our goal is to equip you with the knowledge to approach these alluring offers with confidence and clarity, ensuring you truly benefit from what zero-interest auto financing has to offer.

The Allure of 0 APR Car Loan Deals – Too Good to Be True?

The concept of a 0% Annual Percentage Rate (APR) on a car loan is incredibly enticing. It fundamentally means that you will only pay back the principal amount you borrowed for the vehicle, with no additional cost for the privilege of borrowing that money. This direct saving on interest can translate into significant financial relief, making monthly payments more manageable or allowing you to pay off the car faster.

From a buyer’s perspective, the benefits are clear and immediate. You get to keep more of your hard-earned money in your pocket instead of funneling it towards interest charges. This can free up funds for other essential expenses, allow for a larger down payment on a future purchase, or simply improve your overall financial liquidity.

So, how do dealerships and manufacturers afford to offer such seemingly generous terms? These 0 APR car loan deals are primarily marketing tools and incentives. Automakers often subsidize the interest for specific models or during certain times of the year to clear out inventory, boost sales of slower-moving vehicles, or attract new customers to their brand. The dealer might also absorb some of the cost, viewing it as an investment in moving a car off the lot and securing a sale.

Understanding this underlying mechanism is crucial. It’s not simply a handout; it’s a strategic business decision designed to stimulate sales and move inventory. This insight will help you identify when and why these special auto financing offers become available.

Unveiling the Eligibility for Zero-Interest Car Loans

While the promise of zero-interest car loans is universal, the reality of qualification is highly selective. Lenders and manufacturers offering 0 APR deals are taking on a higher risk by foregoing interest revenue, so they seek out only the most creditworthy applicants. Meeting these stringent criteria is the first and most critical step towards securing such a deal.

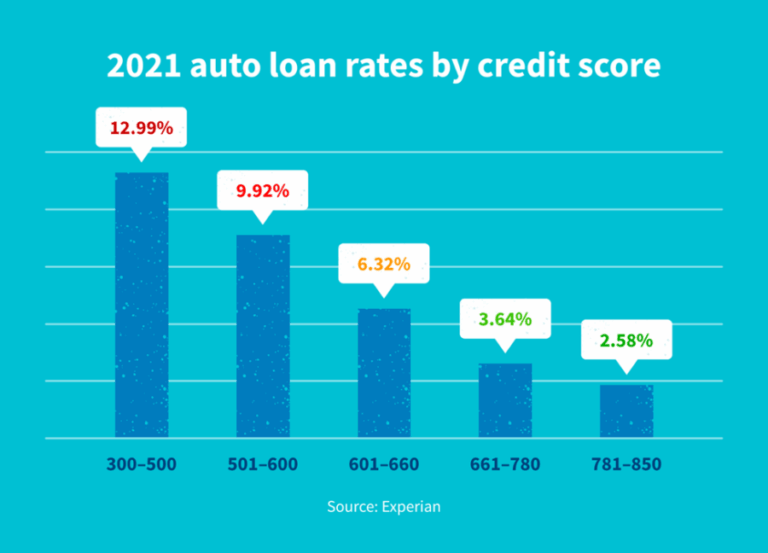

1. The Paramount Factor: Your Credit Score

An excellent credit score is almost always a non-negotiable requirement for 0 APR car loan deals. Typically, this means a FICO score in the upper 700s, often 740 or higher, extending into the 800s. Lenders view a high credit score as a strong indicator of financial responsibility and a very low risk of default. It tells them you have a proven track record of managing debt responsibly and making payments on time.

Based on my experience, lenders are very strict when it comes to these top-tier offers. If your score is even slightly below their threshold, you might be offered a low APR, but rarely 0%. It’s essential to check your credit score well in advance and address any inaccuracies or areas for improvement.

2. Loan Term Limitations

Zero-interest car loans are frequently offered for shorter loan terms, often 36 or 48 months, though sometimes 60 months. Longer terms, such as 72 or 84 months, are rarely eligible for 0 APR. This is because the longer the loan term, the higher the risk for the lender, and the more interest they forego.

A shorter term means higher monthly payments, which again, only highly qualified borrowers with stable incomes can comfortably manage. This structure reduces the lender’s exposure to market fluctuations and ensures a quicker return of their principal.

3. Vehicle Eligibility: New Cars and Specific Models

You’ll almost exclusively find 0 APR car loan deals on new vehicles, not used ones. These offers are primarily manufacturer incentives designed to push sales of their latest models or to clear out the previous year’s inventory. Within the new car lineup, the deals are often limited to specific models, trim levels, or even colors that the dealer or manufacturer wants to move quickly.

Don’t expect to find a 0 APR offer on every single car on the lot. Flexibility in your choice of vehicle can significantly increase your chances of finding an eligible deal.

4. Down Payment Considerations

While not always explicitly required for a 0 APR deal, making a substantial down payment can strengthen your application. A larger down payment reduces the total amount you need to borrow, which in turn reduces the lender’s risk. It also shows your commitment to the purchase and your financial capability.

Even if you qualify for 0 APR with no down payment, putting money down can lead to lower monthly payments, making the loan even more comfortable to manage. It’s always a smart financial move if you have the cash available.

5. Stable Income and Low Debt-to-Income Ratio

Lenders will also scrutinize your income stability and your existing debt obligations. They want to ensure that your monthly income is sufficient to comfortably cover the higher monthly payments associated with a shorter 0 APR loan term, in addition to your other financial commitments. A low debt-to-income (DTI) ratio demonstrates that you aren’t overleveraged and have ample capacity to take on new debt. This provides additional assurance to the lender that you are a reliable borrower.

Decoding the Deal: What to Look Out For with 0 APR Auto Financing

The siren song of "0 APR" can sometimes overshadow crucial details. While the absence of interest is a massive advantage, it’s vital to understand that these deals aren’t always a universally perfect fit for every buyer. There are several aspects you need to scrutinize to ensure you’re getting the best overall value.

1. Higher Purchase Price vs. Cash Rebates

One of the most common trade-offs with 0 APR car loan deals is the forfeiture of other incentives, particularly cash rebates. Manufacturers often offer buyers a choice: either a low (or zero) interest rate or a significant cash rebate. The cash rebate reduces the vehicle’s purchase price directly, which means you borrow less money overall.

Pro tips from us: Always compare both options. Calculate how much you would save with the cash rebate (and a standard interest loan) versus the 0 APR loan. Sometimes, taking the rebate and securing a competitive low APR loan from an external lender can result in greater overall savings, especially if you can get a good rate.

2. Limited Vehicle Choice and Inventory

As mentioned, 0 APR offers are typically tied to specific models, trim levels, or even colors that the dealer or manufacturer wants to sell. This means you might not be able to get your absolute first choice of vehicle, or you might have to compromise on certain features. If your heart is set on a particular, high-demand model or a very specific configuration, it might not be available with a 0 APR deal.

Be prepared to be flexible with your car selection if zero-interest auto financing is your top priority. The "perfect" car might not align with the "perfect" financing.

3. Shorter Loan Terms and Higher Monthly Payments

While shorter loan terms are great for paying off debt quickly, they also result in significantly higher monthly payments. For instance, a $30,000 loan over 36 months will have much higher payments than the same loan over 60 or 72 months, even with 0 APR. You need to be absolutely certain your budget can comfortably handle these elevated payments.

Common mistakes to avoid are focusing solely on the "0 APR" and neglecting the monthly payment amount. Overextending yourself can lead to financial strain down the road.

4. Impact on Trade-in Value

Dealers are businesses, and they need to make a profit. If they’re offering you a fantastic 0 APR deal, they might try to recoup some of their margin elsewhere, potentially by offering a lower trade-in value for your old car. It’s crucial to research the market value of your trade-in independently before you even step foot in the dealership.

Be prepared to negotiate your trade-in separately from the new car purchase and the financing. Don’t let one great offer blind you to a poor deal in another area.

5. Hidden Fees and Documentation Costs

Even with a 0 APR loan, you’ll still encounter standard fees associated with buying a car. These can include documentation fees, registration fees, sales tax, and sometimes additional dealer add-ons. These fees are separate from the loan interest and will still apply.

Always ask for a complete breakdown of all costs before finalizing the deal. A transparent dealer will be happy to provide this.

6. Penalties for Late Payments

Read the fine print very carefully regarding late payments. Many 0 APR car loan deals come with a clause stating that if you miss a payment or are late, the promotional 0 APR will be revoked. Your interest rate could then revert to a much higher, standard rate for the remainder of the loan term, which can be a significant financial blow.

Ensure you have a reliable system for making on-time payments, perhaps even setting up automatic deductions, to avoid this costly pitfall.

Navigating the Application Process for Your Dream 0 APR Car

Securing a 0 APR car loan deal requires more than just good credit; it demands preparation, strategic thinking, and a willingness to negotiate. Approaching the process with a clear plan will significantly improve your chances.

1. Preparation is Key: Credit Check and Budgeting

Before you even start looking at cars, pull your credit reports from all three major bureaus (Equifax, Experian, TransUnion). Review them for any errors and understand your current credit score. If your score isn’t in the excellent range, focus on improving it before applying. For more tips on improving your credit score, check out our guide on .

Simultaneously, establish a firm budget. Determine how much you can realistically afford for a monthly car payment, considering the shorter terms often associated with 0 APR. Don’t forget to factor in insurance, fuel, and maintenance costs.

2. Pre-approval vs. Dealer Financing

While 0 APR deals are typically offered through the dealership’s financing (often backed by the manufacturer’s captive finance company), it’s always wise to get pre-approved for a standard loan from your bank or credit union before visiting the dealership. This pre-approval gives you a baseline interest rate and loan amount, providing a powerful negotiation tool.

If the dealer’s 0 APR offer isn’t truly the best option (e.g., if it means sacrificing a large cash rebate), you’ll have an alternative financing offer ready to go. It also helps you separate the car price negotiation from the financing negotiation.

3. Negotiation Tactics: Price First, Then Financing

When you’re at the dealership, try to negotiate the car’s purchase price before discussing financing options. This prevents the dealer from shifting costs around between the car price and the interest rate. Once you agree on a firm price for the vehicle, then you can introduce the financing discussion and inquire about 0 APR car loan deals.

This strategy ensures you’re getting the best possible price on the car itself, regardless of the financing terms.

4. Required Documentation

Be prepared to provide standard documentation for any car loan application, even 0 APR auto financing. This typically includes:

- Proof of identity (driver’s license, passport)

- Proof of income (recent pay stubs, tax returns if self-employed)

- Proof of residence (utility bill, lease agreement)

- Social Security Number (for credit check)

- Trade-in title/registration (if applicable)

Having all these documents ready will streamline the application process and demonstrate your readiness to complete the purchase.

Beyond 0 APR: Exploring Alternative Car Loan Deals

While 0 APR car loan deals are highly desirable, they are not always the best fit for everyone, nor are they always available for the specific vehicle you desire. Understanding alternative financing options is crucial for making a well-rounded decision.

1. Cash Rebates vs. 0 APR: A Deeper Dive

This is a critical comparison. Let’s consider an example:

- Option A: 0 APR for 36 months. Car price: $30,000. Total paid: $30,000. Monthly payment: $833.33.

- Option B: $2,000 cash rebate + 3.9% APR for 36 months. Car price: $28,000.

- Loan amount: $28,000.

- At 3.9% APR over 36 months, total interest would be approximately $1,690.

- Total paid: $28,000 + $1,690 = $29,690.

- Monthly payment: approximately $824.72.

In this scenario, taking the cash rebate and a low APR loan actually saves you more money overall ($310) and results in slightly lower monthly payments. This is why a direct comparison is absolutely essential.

2. Low APR Loans: Still Excellent Alternatives

If you don’t qualify for 0 APR or if the 0 APR deal comes with too many compromises, a low APR loan (e.g., 1.9% to 3.9%) is still a fantastic option, especially with excellent credit. These rates are significantly better than average market rates and can still save you a considerable amount of money over the life of the loan. Many credit unions, in particular, are known for offering very competitive auto loan rates.

3. Used Car Loans: A Different Landscape

0 APR car loan deals are virtually non-existent for used vehicles. Used car financing typically carries higher interest rates due to the perceived higher risk (older vehicles, more mileage, potential for unknown issues). However, you can still find competitive rates for used cars, especially if you have strong credit. Focus on getting the best available rate for a used car, rather than holding out for 0 APR.

4. Leasing: A Different Approach to New Cars

Leasing is another popular option for new cars, offering lower monthly payments compared to buying, and the opportunity to drive a new car every few years. However, leasing means you don’t own the car, and there are mileage restrictions and potential end-of-lease fees. It’s a different financial product altogether and should be considered if your priority is always having the latest model without the commitment of ownership.

For a deeper understanding of current automotive market trends and their impact on financing, you can refer to reputable sources like J.D. Power’s consumer insights.

Maximizing Your Chances: Expert Strategies for Securing Those Elusive 0 APR Car Loan Deals

While 0 APR car loan deals are selective, there are concrete steps you can take to significantly increase your likelihood of approval. As someone who has spent years helping clients navigate auto financing, I’ve seen these strategies pay off time and time again.

1. Credit Score Optimization: Aim for the Top Tier

The single most impactful action you can take is to optimize your credit score. If your score is not in the "excellent" range (generally 740+ FICO), dedicate time to improving it.

- Pay all bills on time, every time: Payment history is the biggest factor.

- Reduce outstanding debt: Especially on credit cards, aim for utilization below 30% of your credit limit.

- Avoid new credit applications: Each application can temporarily ding your score.

- Review your credit report for errors: Dispute any inaccuracies immediately.

2. Research and Timing: When Are These Deals Most Common?

0 APR offers are strategic. They often appear during specific times:

- End of the month/quarter/year: Dealers and manufacturers are trying to hit sales targets.

- Model year changeovers: To clear out outgoing models.

- Slow sales periods: When foot traffic is down, incentives go up.

- Specific models: When a particular car isn’t selling as quickly as desired.

Do your homework. Check manufacturer websites, dealership promotions, and automotive news sites to identify when and where these zero-interest auto financing deals are being advertised.

3. Be Prepared to Walk Away: Your Ultimate Leverage

This is perhaps the most powerful negotiation tactic. If a dealer senses you’re desperate or unwilling to leave, they have less incentive to offer their best deal. If you’ve done your research, know your budget, and have alternative financing options (like a pre-approval from your bank), you can confidently walk away if the 0 APR deal isn’t working for you, or if other aspects of the deal are unfavorable.

The ability to say "no" or "I need to think about it" gives you significant leverage and encourages the dealer to sweeten the offer.

4. Understand Your Budget: Don’t Overcommit

While 0 APR eliminates interest, the higher monthly payments on shorter terms can still strain your budget. Don’t let the allure of "free money" tempt you into buying a car you can’t truly afford. A car loan, even at 0 APR, is still a significant financial commitment.

Create a realistic budget that includes all car-related expenses, not just the monthly payment. This ensures long-term financial comfort.

5. Separate the Deal:

Negotiate the car price, then your trade-in value, and then the financing. If you’re considering a trade-in, our article on can provide valuable insights. Do these as distinct transactions as much as possible. This makes it harder for the dealer to manipulate numbers to their advantage and ensures you’re getting the best possible outcome on each component of the purchase.

Conclusion

0 APR car loan deals are undoubtedly one of the most attractive financing options available in the automotive market. They offer genuine savings by eliminating interest, which can amount to thousands of dollars over the life of a loan. However, as we’ve explored, these offers are not a universal solution and come with specific eligibility requirements and potential trade-offs.

To truly benefit from zero-interest auto financing, you need to be an informed, prepared, and strategic buyer. This means cultivating an excellent credit score, thoroughly understanding the terms and conditions, meticulously comparing all available incentives (like cash rebates), and being ready to negotiate every aspect of the deal.

By following the insights and expert strategies outlined in this comprehensive guide, you can confidently approach the car buying process. Remember, the ultimate goal is not just to secure a 0 APR deal, but to ensure you’re making a smart, financially sound decision that puts you in the driver’s seat of a car you love, on terms that truly benefit your wallet. Happy car hunting, and may your next auto financing experience be as smooth as possible!