Unlock Your Car Loan: The Ultimate Guide to Amortization Tables & Smart Payoff Strategies

Unlock Your Car Loan: The Ultimate Guide to Amortization Tables & Smart Payoff Strategies Carloan.Guidemechanic.com

Buying a car is an exciting milestone for many, offering freedom and convenience. However, for most, it also involves taking on a car loan. While the monthly payment might seem straightforward, the inner workings of how your money is allocated between principal and interest often remain a mystery. This lack of clarity can leave many feeling disempowered and unsure about how to truly manage their debt.

This is where the Car Loan Amortization Table comes into play. It’s not just a fancy financial term; it’s your personal roadmap to understanding every single payment you make on your car loan. In this comprehensive guide, we’ll demystify the amortization table, explain why it’s an indispensable tool for every car owner, and show you how to leverage it to save money and pay off your car loan faster. Get ready to transform from a passive borrower into an active, informed financial manager.

Unlock Your Car Loan: The Ultimate Guide to Amortization Tables & Smart Payoff Strategies

What Exactly is a Car Loan Amortization Table?

At its core, a car loan amortization table is a detailed schedule of your loan payments, broken down over the entire life of the loan. Think of it as a step-by-step financial blueprint that shows you exactly how each of your monthly payments is applied. Instead of just seeing one lump sum leaving your bank account, this table meticulously separates the portion going towards the interest from the portion reducing your actual loan balance (the principal).

The word "amortization" itself means the process of paying off a debt with regular payments over time. Each payment you make systematically reduces your principal balance, with a calculated amount of interest applied based on the remaining balance. This table provides a clear, transparent view of this entire process, from your very first payment to your very last. It’s a powerful tool that transforms complex financial calculations into an easy-to-understand format.

Why Every Car Owner Needs to Understand Their Amortization Table

Understanding your car loan amortization table goes far beyond mere curiosity; it’s about financial empowerment and smart money management. Based on my experience in financial literacy, many borrowers only focus on the monthly payment amount, overlooking the significant impact of interest and the potential for savings.

1. Transparency and Clarity

The primary benefit is unparalleled transparency. Without an amortization table, your monthly payment feels like a black box. You know money goes out, but you don’t truly grasp where it’s going. The table illuminates this, showing you precisely how much of your hard-earned cash is paying the bank for the privilege of borrowing (interest) and how much is chipping away at the actual debt (principal). This clarity removes the guesswork and helps you see the true cost of your loan.

2. Strategic Financial Planning

Having a detailed payment schedule allows you to plan your finances more effectively. You can anticipate exactly how your loan balance will decrease over time and how your interest payments will reduce as you progress. This foresight is invaluable for budgeting, especially if you’re considering other major financial decisions, like buying a home or saving for retirement. It gives you a clear picture of your debt obligations for years to come.

3. The Power to Save Money on Interest

Perhaps the most compelling reason to understand your amortization table is the potential to save a significant amount of money on interest. By seeing how interest is calculated and how it dominates your early payments, you can develop strategies to reduce the overall interest paid. We’ll dive into these strategies later, but suffice it to say, knowing how the game is played allows you to win it. Pro tips from us include using this knowledge to make informed decisions that benefit your wallet, not just the lender’s.

4. Informed Decision-Making

An amortization table arms you with critical information for various financial decisions. Should you refinance? Is it worth making an extra payment this month? When is the best time to sell your car if you want to avoid being upside down on your loan? All these questions can be answered with confidence when you understand the trajectory of your loan payments and balances. It transforms abstract financial concepts into actionable insights.

Deconstructing the Amortization Table: Key Components Explained

To truly harness the power of a car loan amortization table, you need to understand each of its columns. Every piece of data tells a crucial part of your loan’s story. Let’s break down the essential components you’ll find in any standard amortization schedule.

1. Payment Number

This column simply lists the sequence of your payments, usually starting from 1 and going up to the total number of payments in your loan term. For example, a 60-month car loan would have payment numbers from 1 to 60. It helps you track where you are in your loan journey.

2. Beginning Balance

At the start of each payment period, this is the remaining amount of money you still owe on your loan before you make your current payment. For the very first payment, the beginning balance will be your original loan amount. For subsequent payments, it will be the ending balance from the previous period.

3. Monthly Payment

This is the fixed amount you pay each month. It remains constant throughout the life of the loan (assuming a fixed-rate loan and no extra payments). This single figure is what most people focus on, but as we’ll see, it’s just the tip of the iceberg.

4. Interest Paid

This is a critical column. It shows the portion of your monthly payment that goes towards paying the interest accrued on your loan’s beginning balance for that period. In the early stages of a car loan, a significant portion of your payment often goes towards interest. This is a crucial insight into how loans are structured.

5. Principal Paid

This column reveals the amount of your monthly payment that directly reduces your outstanding loan balance. Unlike the interest portion, which is essentially the cost of borrowing, the principal portion is what actually brings you closer to owning your car free and clear. As your loan progresses, this portion will gradually increase.

6. Ending Balance

After your monthly payment is applied (with both interest and principal portions accounted for), this is the new, reduced amount you still owe on your loan. This figure then becomes the "beginning balance" for the next payment period. Tracking this shows your progress towards debt freedom.

7. Cumulative Interest Paid (Optional but Useful)

Some tables include a cumulative interest column, which sums up all the interest you’ve paid up to that point. This can be a sobering but motivating figure, showing you the total cost of borrowing over time. Seeing this total grow can often inspire borrowers to pay off their loan faster.

8. Cumulative Principal Paid (Optional but Useful)

Similarly, a cumulative principal column tracks the total amount of principal you’ve paid down. This provides a positive reinforcement, showing you how much of the original loan amount you’ve successfully eliminated. It’s a clear indicator of your progress towards ownership.

Pro Tip: When you look at the "Interest Paid" and "Principal Paid" columns, you’ll immediately notice a pattern. In the initial payments, the "Interest Paid" amount is significantly higher than the "Principal Paid." As you progress through the loan term, this dynamic shifts, with the principal portion growing larger and the interest portion shrinking. Understanding this "front-loaded" interest structure is key to smart loan management.

How Interest Works: The Front-Loaded Nature of Car Loans

One of the most eye-opening revelations an amortization table provides is the understanding of how interest is calculated and applied. Car loans typically use what’s called "simple interest," meaning interest is calculated only on the outstanding principal balance. However, the allocation of your monthly payment between interest and principal creates a "front-loaded" effect that surprises many.

In the early months of your car loan, a disproportionately large percentage of your fixed monthly payment goes towards covering the interest. This is because your outstanding principal balance is at its highest, and therefore, the interest accrued on that large balance is also at its peak. As you make payments, your principal balance slowly decreases, and with it, the amount of interest charged each month also declines.

This means that for a significant portion of your loan’s early life, you’re primarily paying for the privilege of borrowing the money, with only a smaller portion actually reducing the core debt. It’s like climbing a hill where the steepest part is at the very beginning.

Based on my experience, this front-loaded interest structure is often misunderstood. Many borrowers assume that their payments consistently reduce their principal equally throughout the loan term. When they see their amortization table, they realize how much interest they’re paying upfront. This realization isn’t meant to be discouraging; rather, it’s a powerful motivator. It highlights why making even small extra principal payments, especially early in the loan, can have a dramatically positive impact on the total interest you pay and how quickly you become debt-free. It’s about working smarter, not just harder, to pay off your car loan.

Creating Your Own Car Loan Amortization Table

While the concept might seem complex, creating or accessing your own car loan amortization table is quite straightforward. You don’t need to be a math whiz to benefit from this powerful financial tool.

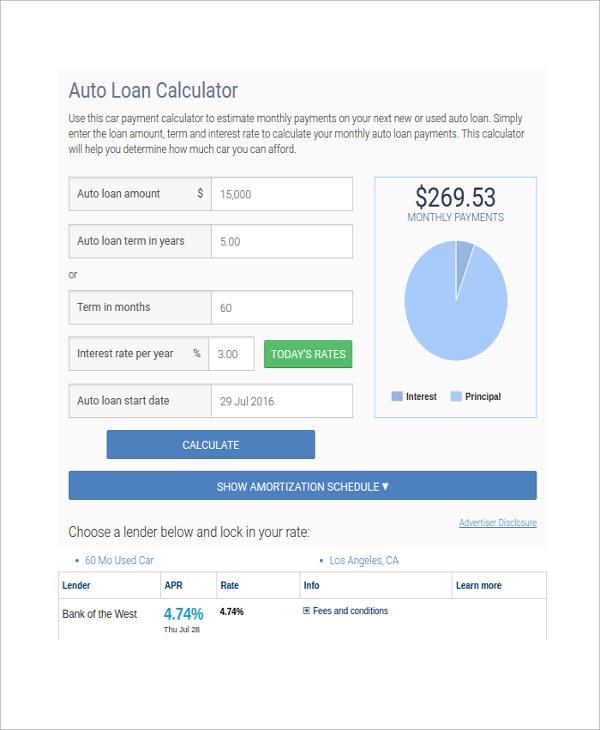

1. Online Amortization Calculators

This is by far the easiest and most common method. Numerous reputable financial websites offer free online car loan amortization calculators. All you need to input are a few key pieces of information:

- Original Loan Amount (Principal): How much you borrowed.

- Annual Interest Rate: The rate you’re paying (e.g., 5.99%).

- Loan Term: The duration of your loan in months (e.g., 60 months).

Once you enter these details, the calculator will instantly generate a full amortization schedule, often including all the columns we discussed earlier. This is a quick and effective way to get a clear picture of your loan.

2. Using Spreadsheet Software (Excel/Google Sheets)

For those who enjoy a bit more control and customization, creating an amortization table in a spreadsheet program like Microsoft Excel or Google Sheets is an excellent option. This allows you to:

- Input your own formulas: You can build a dynamic table that updates if you change the interest rate or payment amount.

- Track extra payments: You can easily add columns to show when you make extra principal payments and how they affect your remaining balance and interest paid.

- Visualize data: Spreadsheets allow you to create charts and graphs to visualize your loan progress.

While it requires a basic understanding of spreadsheet functions (like SUM, PMT, IF), there are countless free templates and tutorials available online that can guide you through the process step-by-step.

3. Request from Your Lender

Your loan servicer or bank should be able to provide you with an amortization schedule for your specific loan. Many lenders offer this as part of your loan documents or can generate one upon request. This ensures accuracy based on your exact loan terms.

Pro Tip: Whichever method you choose, ensure the information you input is accurate. Even a small discrepancy in the interest rate or loan amount can significantly alter the amortization schedule. Double-check your loan documents for precise figures.

Strategies to Save Money and Pay Off Your Car Loan Faster

Now that you understand the mechanics of your car loan through the amortization table, it’s time to put that knowledge into action. The power of the table lies in its ability to show you exactly how extra payments accelerate your debt payoff and reduce your total interest paid.

1. Making Extra Principal Payments

This is arguably the most effective strategy. Any amount you pay over your regular monthly payment, if designated specifically for principal, will directly reduce your loan balance. Because interest is calculated on the outstanding principal, reducing that balance sooner means less interest accrues in subsequent periods.

- How to do it: Contact your lender to ensure extra payments are applied directly to the principal, not just prepaying future interest.

- Impact: Even small, consistent extra payments can shave months off your loan term and save you hundreds, if not thousands, in interest. Use an amortization calculator to see the dramatic effect.

2. Bi-Weekly Payments

Instead of making one monthly payment, you make half of your payment every two weeks. Since there are 52 weeks in a year, this results in 26 half-payments, which equates to 13 full monthly payments annually instead of 12.

- How to do it: Set up automatic bi-weekly payments with your lender or manually make extra payments equivalent to one full monthly payment per year.

- Impact: This strategy effectively adds an extra payment each year, accelerating your payoff and reducing total interest.

3. Round-Up Payments

A simple psychological trick that works wonders. If your payment is, say, $317.50, round it up to $320 or even $325. That small extra amount goes directly to principal.

- How to do it: Adjust your automatic payments or manually add a few extra dollars each month.

- Impact: These seemingly insignificant amounts add up over time, providing a gentle push towards early payoff without feeling like a major financial sacrifice.

4. Lump Sum Payments

Did you receive a bonus, tax refund, or unexpected windfall? Consider using a portion of it to make a lump sum payment towards your car loan principal.

- How to do it: Ensure the payment is applied directly to the principal.

- Impact: A substantial lump sum can significantly reduce your principal, leading to immediate and considerable savings on future interest.

5. Refinancing Your Loan

If interest rates have dropped since you took out your original loan, or if your credit score has significantly improved, refinancing could be a smart move.

- How to do it: Shop around with different lenders for a new loan with a lower interest rate or a shorter term.

- Impact: A lower interest rate means less money paid overall, while a shorter term accelerates payoff (though it might increase your monthly payment). Always compare the total cost of the new loan, including any fees, with your remaining original loan.

Common mistakes to avoid are:

- Not specifying principal-only payments: Always confirm with your lender that any extra money you send is applied directly to the principal, not towards future interest. Otherwise, you might not see the accelerated payoff benefits.

- Ignoring prepayment penalties: While rare for car loans, always check your loan agreement for any fees associated with paying off your loan early.

- Refinancing without calculating total cost: A lower monthly payment might seem appealing, but if it extends your loan term significantly or includes high fees, you could end up paying more in the long run. Always do the math!

Real-World Applications of Your Amortization Table

The Car Loan Amortization Table isn’t just a theoretical exercise; it’s a practical tool with numerous real-world applications that can significantly impact your financial life.

1. Budgeting and Financial Planning

Knowing exactly how much of your payment goes to interest versus principal helps you budget more effectively. You can anticipate your declining interest payments and rising principal payments, allowing you to reallocate funds or plan for other savings goals. It provides a clear picture of your debt service obligations, which is crucial for overall financial health. For more tips on managing your budget, consider exploring our article on Smart Budgeting for Car Owners – .

2. Negotiating with Lenders (or Refinancing)

When you understand the total cost of interest over the life of a loan, you become a savvier negotiator. If you’re considering refinancing, your amortization table helps you evaluate new offers. You can compare the remaining interest on your current loan with the total interest of a new loan, ensuring any refinancing move truly benefits you. It moves you past just comparing monthly payments to understanding the true long-term financial impact.

3. Deciding When to Sell or Trade In Your Vehicle

One of the most common pitfalls for car owners is being "upside down" on their loan – owing more than the car is worth. Your amortization table shows your exact principal balance at any given point. This allows you to make an informed decision about when to sell or trade in your car to avoid negative equity. Knowing your equity position helps you maximize your return and avoid bringing debt from an old car into a new purchase.

4. Assessing the Impact of Extra Payments

As discussed, extra payments can dramatically alter your loan’s trajectory. With an amortization table, you can precisely calculate how many months you’ll shave off your loan and how much interest you’ll save by making an extra payment of a specific amount. This instant feedback is incredibly motivating and turns a theoretical goal into a concrete plan.

5. Building Financial Literacy and Confidence

Perhaps the most underrated application is the boost in your financial literacy and confidence. Understanding how interest works and how your payments are applied demystifies the world of loans. This knowledge empowers you to make better financial decisions, not just for your car loan, but for all future borrowing and saving endeavors. It’s an investment in your financial future.

Beyond the Numbers: The Psychological Benefits of Understanding Your Loan

While the financial benefits of understanding your car loan amortization table are substantial, there’s a powerful psychological advantage that often goes unmentioned. Managing debt can be a source of significant stress, but knowledge is truly power when it comes to personal finance.

1. Reduced Stress and Anxiety

Ignorance about debt can breed anxiety. When you don’t fully understand how your loan works, it feels like a heavy, uncontrollable burden. The amortization table pulls back the curtain, transforming that opaque burden into a clear, manageable path. Seeing the numbers, understanding the mechanics, and having a plan dramatically reduces financial stress. You move from a feeling of being trapped to a feeling of being in control.

2. Increased Control and Empowerment

Knowing exactly where your money is going and how your debt is decreasing instills a profound sense of control. You’re no longer passively making payments; you’re actively managing your debt. This empowerment extends beyond your car loan, fostering a more proactive and confident approach to all your financial decisions. You become the driver of your financial destiny, not just a passenger.

3. Motivation and Goal Achievement

Watching your principal balance shrink and your interest payments decline can be incredibly motivating. Each payment becomes a small victory, moving you closer to the tangible goal of car ownership. This visual progress, especially when coupled with strategies to accelerate payoff, can fuel your determination to reach debt freedom faster. It transforms a long-term obligation into a series of achievable milestones.

4. Foundation for Future Financial Success

Mastering your car loan is an excellent training ground for larger financial undertakings, like a mortgage. The principles of amortization, interest calculation, and strategic debt repayment are universal. By confidently navigating your car loan, you’re building a strong foundation of financial expertise that will serve you well throughout your life. For more insights on managing debt, you might find our article on Smart Strategies for Debt Reduction – helpful.

Conclusion: Drive Towards Financial Freedom

The Car Loan Amortization Table is far more than just a dry financial document; it’s an indispensable tool for every car owner. It illuminates the often-hidden dynamics of interest and principal, transforming your loan from a mystery into a clear, understandable journey. By embracing this powerful schedule, you gain unparalleled transparency, enabling you to plan strategically, make informed decisions, and ultimately save a significant amount of money.

Remember, understanding your loan isn’t just about the numbers; it’s about the confidence and control it gives you over your financial future. Whether you choose to use an online calculator, a spreadsheet, or request one from your lender, take the initiative to truly understand your car loan amortization table today. This knowledge empowers you to actively manage your debt, accelerate your payoff, and drive towards true financial freedom.

Start exploring your car loan’s amortization schedule now, and take the first step towards becoming a more informed and empowered car owner. For further reading on consumer finance and auto loans, we recommend visiting the Consumer Financial Protection Bureau (CFPB) website for trusted information and resources. Your financial well-being is in your hands – make every payment count!