Unlock Your Car’s Value: A Comprehensive Guide to Using Your Car as Collateral for a Personal Loan

Unlock Your Car’s Value: A Comprehensive Guide to Using Your Car as Collateral for a Personal Loan Carloan.Guidemechanic.com

Life throws unexpected curveballs, and sometimes, you need quick access to funds. Whether it’s an emergency repair, medical bill, or an urgent financial gap, finding the right solution can be challenging, especially if your credit history isn’t perfect. This is where using your car as collateral for a personal loan enters the picture, offering a potential lifeline for many.

But what exactly does this mean? And more importantly, is it the right choice for you? As an expert in personal finance and lending options, I’ve seen firsthand how these loans can provide necessary relief, but also how they can lead to difficulties if not fully understood. This in-depth guide will demystify the process, explore the benefits and risks, and equip you with the knowledge to make an informed decision. We’ll cover everything from eligibility to repayment, ensuring you have a complete understanding of how to use your car as collateral for a personal loan responsibly.

Unlock Your Car’s Value: A Comprehensive Guide to Using Your Car as Collateral for a Personal Loan

What Exactly Does "Using Your Car as Collateral" Mean?

At its core, "collateral" is an asset that a borrower offers to a lender to secure a loan. It acts as a form of guarantee. If the borrower defaults on the loan, the lender has the right to seize the collateral to recover their losses. This arrangement reduces the risk for the lender, often making it easier for borrowers to qualify for a loan or secure more favorable terms.

When you use your car as collateral for a personal loan, you are essentially pledging your vehicle’s value against the money you borrow. The car serves as security for the loan, much like a house secures a mortgage. This type of lending is often referred to as an "auto equity loan" or, more commonly, a "car title loan."

The key distinction here is that the loan is "secured." Unlike an unsecured personal loan, which relies solely on your creditworthiness, a secured loan leverages a tangible asset. This security is precisely what makes car collateral loans accessible to individuals who might struggle to get approved for traditional loans, perhaps due to a lower credit score or limited credit history.

How Does a Car Collateral Loan Work?

Understanding the mechanics of a car collateral loan is crucial before you commit. The process generally begins with you, the borrower, approaching a lender who specializes in these types of secured loans. You present your vehicle as the asset that will secure the loan.

The lender will then assess the value of your car. This appraisal usually involves looking at factors like the make, model, year, mileage, and overall condition of the vehicle. Based on this valuation, and your ability to repay, the lender will determine the maximum loan amount they are willing to offer. Typically, you can borrow a percentage of your car’s wholesale value, not its retail price.

Once approved, you’ll receive the loan funds, and in exchange, you temporarily transfer your car’s title to the lender. It’s important to note that while the lender holds the title, you usually get to keep and drive your car throughout the loan term. This is a significant advantage for many borrowers, as it allows them to maintain their daily routines without disruption.

Repayment terms are then established, including the interest rate, fees, and the loan duration. These loans often have shorter repayment periods compared to traditional personal loans, sometimes ranging from a few weeks to several months. The interest rates can vary widely, often being higher than unsecured personal loans due to the perceived risk, despite the collateral.

Based on my experience, many people misunderstand that while they keep their car, the title is the crucial piece of collateral. Failing to repay the loan means the lender can repossess your vehicle, as they legally hold the title. This is the most significant risk associated with these types of loans, and it’s a consequence that must be taken very seriously.

The Benefits: Why Consider a Car Collateral Loan?

Despite the inherent risks, there are several compelling reasons why individuals turn to car collateral loans. For many, they represent a vital financial tool during challenging times. Understanding these advantages can help you determine if this option aligns with your current needs.

One of the primary benefits is quick access to funds. Unlike traditional bank loans that can take days or even weeks to process, car collateral loans often offer same-day or next-day funding. This speed is invaluable when facing an urgent financial crisis that simply cannot wait. If you need cash fast, this avenue can be significantly more efficient.

Another major advantage is their bad credit friendliness. Lenders for car collateral loans are typically more focused on the value of your vehicle and your ability to repay than on your credit score. This makes them an accessible option for individuals with poor credit, no credit history, or those who have been turned down by conventional lenders. Your car’s equity acts as a more powerful persuader than your credit report.

While interest rates can be high compared to prime loans, they can sometimes be lower than other high-risk options like payday loans. Because the loan is secured by your vehicle, the lender faces less risk, which can translate to slightly better rates than completely unsecured short-term loans designed for those with very poor credit. This isn’t always the case, but it’s a possibility worth exploring.

Crucially, you keep driving your car. This means your daily life and responsibilities, such as commuting to work, picking up children, or running errands, remain uninterrupted. This ability to retain possession and use of your vehicle makes the loan far more practical than selling your car outright.

Pro Tip: A car collateral loan can be a suitable option if you have a clear, urgent financial need, a fully paid-off car, and a solid plan to repay the loan within the agreed-upon terms. It’s a short-term solution for short-term problems, not a long-term debt strategy.

The Risks and Downsides: What You Absolutely Need to Know

While the benefits can be appealing, it’s imperative to confront the substantial risks associated with using your car as collateral for a personal loan. Overlooking these potential pitfalls can lead to severe financial consequences. Responsible borrowing means being fully aware of the worst-case scenarios.

The most significant and dire risk is repossession. If you fail to make your loan payments as agreed, the lender has the legal right to repossess your vehicle. This means you could lose your primary mode of transportation, which can severely impact your ability to work, care for family, and manage daily life. Losing your car can quickly spiral into further financial distress.

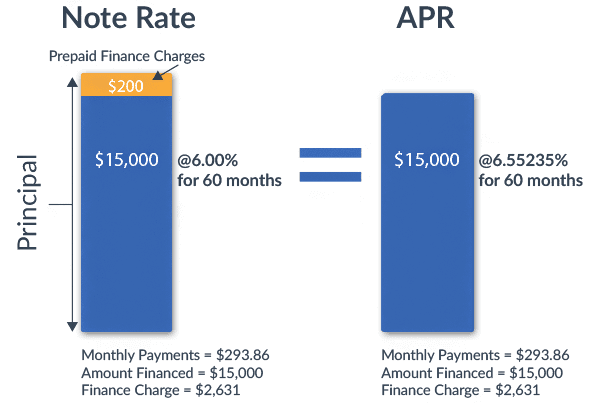

These loans often come with high interest rates. While they might be lower than some extreme alternatives, car title loans are notorious for their high Annual Percentage Rates (APRs), which can sometimes reach triple digits. These rates can make the total cost of borrowing incredibly expensive, potentially trapping borrowers in a cycle of debt if not managed carefully.

Beyond interest, be wary of fees and hidden charges. Lenders may impose various fees, including processing fees, lien fees, late payment fees, and even repossession fees if you default. These additional costs can significantly inflate the total amount you owe, making repayment even more challenging than anticipated. Always ask for a full breakdown of all costs.

There’s a real danger of a debt spiral potential. Because of the high costs and short repayment terms, many borrowers find themselves unable to repay the full amount by the due date. This often leads to "rolling over" the loan, meaning you pay only the interest and fees, and the principal balance is extended for another term. Each rollover adds more fees and interest, causing the debt to grow exponentially and making it incredibly difficult to escape.

While the immediate impact on your credit score might be less than traditional loans, defaulting on a car collateral loan can still harm your credit. If your car is repossessed and sold, the lender may report the delinquency to credit bureaus. Furthermore, if the sale of your car doesn’t cover the full loan amount, you might still owe the difference, and this could also be sent to collections, negatively affecting your credit.

Common mistake to avoid: Underestimating the repayment burden. Many borrowers focus solely on the initial loan amount and overlook the compound effect of high interest and fees, especially if they anticipate needing to roll over the loan. Always calculate the total cost of the loan before signing.

Are You Eligible? Key Requirements for Car Collateral Loans

Before you even consider applying, it’s essential to understand the typical eligibility criteria for car collateral loans. Meeting these requirements is the first step toward potential approval. While specifics can vary slightly between lenders, a common set of conditions generally applies.

Firstly, and most importantly, you must be the owner of the car with a clear title. This means the vehicle must be fully paid off, and you must hold the lien-free title in your name. If you still have an outstanding loan on your car, you typically won’t be able to use it as collateral, as the current lender already holds a lien.

Secondly, the car’s value and equity are paramount. Lenders will appraise your vehicle to determine its market value. The loan amount you qualify for will be a percentage of this value. Generally, older, higher-mileage, or damaged vehicles will yield lower loan offers, or might not be accepted at all. The car must have sufficient equity to secure the desired loan amount.

Lenders will also require proof of income. Even though your car secures the loan, lenders need assurance that you have a reliable source of income to make the scheduled payments. This could be from employment, self-employment, disability benefits, or other verifiable sources. They want to see that you can realistically repay the debt without defaulting.

You must also meet basic demographic requirements, including being of legal age (usually 18 or 21, depending on your state) and a resident of the state where you’re applying. Some lenders might also require a valid driver’s license.

Vehicle insurance is another common requirement. Lenders typically insist that your car is fully insured, protecting both your asset and their collateral in case of an accident or theft. This safeguards their investment should something happen to the vehicle while it’s pledged.

Finally, most lenders will require a vehicle inspection. This allows them to physically verify the car’s condition, mileage, and features, ensuring their appraisal is accurate. This step confirms that the vehicle truly matches the information you provided and holds the value necessary to secure the loan.

The Application Process: A Step-by-Step Walkthrough

Navigating the application process for a car collateral loan can seem daunting, but breaking it down into manageable steps makes it much clearer. Knowing what to expect can streamline your experience and increase your chances of approval.

Step 1: Research Lenders. Start by identifying reputable lenders who offer car collateral loans in your area or online. Look for those with positive reviews, clear terms, and proper licensing. Avoid lenders with a history of complaints or predatory practices. This initial research is critical for your financial safety.

Step 2: Gather Documents. Before you apply, compile all necessary paperwork. This typically includes your clear car title, a valid government-issued ID, proof of income (pay stubs, bank statements), proof of residency (utility bill), and proof of vehicle insurance. Having these ready will significantly speed up the process.

Step 3: Vehicle Appraisal. The lender will need to assess your car’s value. This often involves a physical inspection of your vehicle at their location or sometimes a mobile appraisal. They will check the make, model, year, mileage, and overall condition to determine how much they can lend you.

Step 4: Submit Application. With your documents and vehicle appraisal complete, you’ll fill out a loan application. This will ask for personal details, financial information, and specifics about your vehicle. Be honest and accurate with all information provided.

Step 5: Loan Offer & Agreement Review. If approved, the lender will present you with a loan offer detailing the principal amount, interest rate, repayment schedule, fees, and all terms and conditions. This is the most crucial step where you must meticulously read and understand every single clause in the loan agreement. Pay close attention to the APR, total repayment amount, and any penalties for late payments or default.

Step 6: Funding. Once you agree to the terms and sign the loan agreement, the lender will transfer the funds to you. This can often happen on the same day, either through a direct deposit to your bank account, a check, or sometimes even cash. At this point, you will usually hand over your car’s title to the lender, who will hold it until the loan is fully repaid.

Pro Tip: Never rush through the loan agreement. Ask questions about anything you don’t understand. A reputable lender will be happy to clarify all terms. If they pressure you to sign quickly or refuse to explain details, walk away.

Choosing the Right Lender: What to Look For

Selecting the right lender for a car collateral loan is as important as understanding the loan itself. The wrong choice can lead to significant financial hardship, while a responsible lender can make a challenging situation manageable. Here’s what to prioritize when making your decision.

First and foremost, assess the lender’s reputation and reviews. Search online for customer testimonials, check with consumer protection agencies, and read reviews on independent financial platforms. A lender with a history of transparent dealings and positive customer experiences is generally a safer bet. Avoid those with numerous complaints about hidden fees or aggressive collection tactics.

Transparency in terms is non-negotiable. A trustworthy lender will clearly outline all aspects of the loan: the principal amount, the Annual Percentage Rate (APR), all associated fees (processing, late payment, etc.), and the total cost of the loan. They should provide a written agreement that you can review thoroughly before signing. If a lender is vague about costs or pressures you to sign quickly, consider it a major red flag.

Good customer service is also a strong indicator of a reliable lender. Do they answer your questions patiently and clearly? Are they accessible if you need to discuss your loan? A lender who treats you with respect and provides clear communication can be invaluable, especially if you encounter repayment difficulties.

Look for flexibility in repayment options. While these loans often have strict terms, some lenders might offer slightly more flexible repayment schedules or options for extensions if you communicate problems early. Understanding these possibilities upfront can provide peace of mind.

Finally, ensure the lender is properly licensed and regulated in your state. Licensing ensures they operate within legal boundaries and are subject to oversight. You can usually verify a lender’s license through your state’s financial regulatory authority website. Operating with an unlicensed lender puts you at significant risk.

Alternatives to Car Collateral Loans

Before you commit to using your car as collateral, it’s wise to explore other financial options. While car collateral loans can be a lifeline, their high costs and risks mean they should often be a last resort. Knowing your alternatives can help you make a more informed and potentially less costly decision.

One common alternative is a traditional personal loan (unsecured). If your credit score is decent, you might qualify for an unsecured personal loan from a bank or credit union. These loans typically have much lower interest rates and longer repayment terms, making them more affordable. The downside is stricter credit requirements and a longer approval process.

Credit cards can also be an option for smaller, short-term needs, especially if you have an existing card with available credit. While credit card interest rates can be high, they are often lower than car title loans, and you avoid putting your car at risk. However, using credit cards for emergencies should always be done with a clear repayment plan.

Consider borrowing from family or friends. While this can sometimes strain relationships, it’s often the cheapest form of borrowing, usually with no interest. If possible, formalize the agreement in writing to avoid misunderstandings.

Debt consolidation might be an option if your need for funds is to manage existing debts. A debt consolidation loan, or even working with a credit counseling agency, can help you manage multiple debts into a single, more affordable payment, without putting your car at risk.

Exploring community resources or charities can provide assistance for specific needs like utility bills, rent, or food. Many non-profit organizations offer grants or low-interest loans for individuals facing temporary financial hardship. These resources are designed to help without adding to your debt burden.

Finally, consider selling assets you no longer need. This could include electronics, jewelry, or other valuables. While it requires parting with possessions, it provides immediate cash without incurring debt or putting your car at risk.

Based on my experience, before jumping into a car collateral loan, always explore these alternatives thoroughly. The long-term financial health benefits of avoiding high-interest, secured debt are significant.

Managing Your Car Collateral Loan Responsibly

Once you’ve secured a car collateral loan, the next crucial step is responsible management. This means having a clear strategy to repay the loan and avoid the pitfalls that can lead to repossession or a cycle of debt. Proactive management is key to successfully navigating this financial commitment.

The first and most important step is budgeting for repayments. Integrate your loan payments into your monthly budget immediately. Understand exactly how much is due and when, and ensure you have sufficient funds set aside for each payment. Missing even one payment can trigger late fees and accelerate the path to default.

Thoroughly understand your loan terms. Re-read your loan agreement and be clear on the interest rate, any fees, the full repayment schedule, and especially the consequences of late or missed payments. Know your rights and obligations as a borrower. This knowledge empowers you to stay on track and anticipate any potential issues.

If you foresee difficulties in making a payment, communicate with your lender immediately. Many lenders are willing to work with you if you reach out before a payment is due. They might offer a payment extension, a modified plan, or other options. Ignoring the problem only makes it worse and can lead to aggressive collection actions.

Avoid rollovers at all costs. As discussed, rolling over a loan means paying only the interest and fees, extending the principal balance, and incurring new charges. This is a primary driver of the debt spiral. Make every effort to repay the principal and interest in full by the original due date.

If your loan agreement allows, consider paying off the loan early. Some lenders do not charge prepayment penalties, which means you can save a significant amount on interest by settling the debt ahead of schedule. Always check your agreement for specific terms regarding early repayment.

For strategies on managing your personal finances effectively, read our guide on . It offers practical advice that can complement your efforts to repay your car collateral loan.

Frequently Asked Questions (FAQs)

Here are some common questions people ask about using their car as collateral for a personal loan, along with clear, concise answers.

Can I get a loan if my car isn’t fully paid off?

Typically, no. Most car collateral loan lenders require you to have a clear, lien-free title in your name. This means your car must be fully paid off. If you still owe money on your vehicle, the current lender holds the title, making it unavailable as collateral for a new loan.

How much can I borrow using my car as collateral?

The amount you can borrow depends primarily on the wholesale value of your car and your ability to repay. Lenders usually offer a percentage of your car’s value, often ranging from 25% to 50%, sometimes up to 75%. Factors like your car’s make, model, year, mileage, and condition all influence the final loan amount.

How fast can I get the money?

One of the main advantages of car collateral loans is their speed. Many lenders can process applications and disburse funds on the same day, sometimes within a few hours, provided you have all the necessary documents and your vehicle passes inspection.

What happens if I can’t repay the loan?

If you are unable to repay the loan according to the agreed-upon terms, the lender has the legal right to repossess your car. They will then sell the vehicle to recover the outstanding loan amount. In some cases, if the sale of the car does not cover the full debt, you might still owe the remaining balance.

Does taking out a car collateral loan affect my credit score?

Initially, applying for the loan might result in a hard inquiry on your credit report, which could slightly lower your score for a short period. However, many car collateral lenders do not report your payment activity (positive or negative) to the major credit bureaus. This means making on-time payments might not help build your credit. Conversely, defaulting on the loan and having your car repossessed could eventually negatively impact your credit if the lender reports the delinquency or sends the debt to collections.

Conclusion: Making an Empowered Decision

Using your car as collateral for a personal loan can be a viable option for quick access to funds, especially if traditional lending avenues are closed to you. It offers the distinct advantage of speed and accessibility, allowing you to address urgent financial needs without losing the use of your vehicle. However, this convenience comes with significant risks, primarily the potential for high interest rates and, most critically, the risk of repossession if you fail to meet your repayment obligations.

As an expert blogger and professional SEO content writer, my goal has been to provide you with a super comprehensive, in-depth, and honest assessment of this financial product. The decision to use your car as collateral for a personal loan should never be taken lightly. It requires careful consideration of your financial situation, a thorough understanding of the loan terms, and a solid plan for repayment. Always prioritize responsible borrowing and exhaust all other, less risky alternatives before committing to a car collateral loan.

By arming yourself with knowledge, understanding both the benefits and the substantial risks, and meticulously choosing a reputable lender, you can make an empowered decision that serves your best interests. Remember, financial stability is built on informed choices and proactive management. For official consumer protection information and further guidance on financial decisions, visit the .