Unlock Your Car’s Value: The Ultimate Guide to Getting a Loan Using Your Vehicle

Unlock Your Car’s Value: The Ultimate Guide to Getting a Loan Using Your Vehicle Carloan.Guidemechanic.com

Life is full of unexpected twists and turns. A sudden medical emergency, an urgent home repair, or an unforeseen bill can quickly drain your savings and leave you scrambling for solutions. In these moments of financial need, many people wonder about their options, especially when traditional bank loans seem out of reach due to credit history or lengthy approval processes. This is where the concept of using your car as collateral for a loan comes into play – a practical, often quicker alternative that can provide the immediate cash you need.

But what exactly does it mean to get a loan using your car? Is it a viable solution for everyone? What are the risks, and how do you navigate the process safely and responsibly? As an expert blogger and SEO content writer with years of experience in personal finance, I’ve delved deep into this topic to bring you a super comprehensive guide. Our mission here is to demystify how to get a loan using your car, providing you with unique, in-depth insights to help you make an informed decision. This isn’t just a list of facts; it’s a roadmap crafted to offer real value, ensure readability, and empower you with the knowledge to potentially unlock your vehicle’s hidden financial potential.

Unlock Your Car’s Value: The Ultimate Guide to Getting a Loan Using Your Vehicle

Understanding Loans Using Your Car: What You Need to Know

When you’re facing a financial crunch, your vehicle might represent more than just transportation; it could be a valuable asset capable of securing much-needed funds. Loans that use your car as collateral typically fall into two main categories: car title loans and auto equity loans. While both leverage your vehicle’s value, they have distinct characteristics worth understanding.

What is a Car Title Loan or Auto Equity Loan?

At its core, a car title loan involves using the clear title of your vehicle as collateral for a short-term loan. This means you transfer the title temporarily to the lender, but crucially, you usually retain possession and continue driving your car. The loan amount is typically a percentage of your vehicle’s wholesale value, and these loans are often designed for quick, emergency cash needs. They are usually repaid in a single lump sum or a few installments over a short period, often 15 to 30 days.

Auto equity loans, on the other hand, are generally larger, longer-term loans. They are based on the equity you have in your car – the difference between your car’s market value and what you still owe on it. If you own your car outright, your equity is 100% of its value. If you’re still making payments, you might still have enough equity to qualify. These loans often come with more structured repayment schedules over several months or even years, resembling traditional personal loans but secured by your vehicle.

The primary benefit of both types of loans is that they are secured. Because the loan is backed by a tangible asset (your car), lenders perceive less risk. This often translates into more accessible financing for individuals who might not qualify for unsecured loans due to a less-than-perfect credit history. It’s a way for your asset to speak for your creditworthiness.

When is This Type of Loan Suitable?

A loan using your car can be a suitable option in very specific circumstances, primarily when you need emergency cash quickly and have exhausted other, less costly alternatives. Based on my experience, people often turn to these loans for:

- Urgent Medical Bills: Unexpected health crises can lead to significant out-of-pocket expenses that require immediate payment.

- Essential Home or Vehicle Repairs: A broken furnace in winter or a car breakdown can be critical and can’t wait.

- Avoiding Eviction or Utility Shut-off: These loans can provide a temporary bridge to prevent losing essential services or housing.

- Bridging a Temporary Cash Flow Gap: If you know you’ll receive funds soon (e.g., a large bonus or tax refund) but need cash now, a short-term title loan might help.

It’s particularly relevant for individuals who might have a bad credit history, making it challenging to secure traditional personal loans from banks or credit unions. Because the loan is secured by your vehicle, your credit score often plays a secondary role, if any, in the approval process. The emphasis shifts to your car’s value and your ability to repay the loan from your income.

Common Misconceptions and Risks Associated with Car-Secured Loans

While these loans can offer a lifeline, it’s crucial to approach them with a clear understanding of the potential pitfalls. One of the most significant risks is the high interest rates associated with car title loans, in particular. Annual Percentage Rates (APRs) can be extremely high, sometimes in the triple digits, making them much more expensive than traditional bank loans. Auto equity loans generally have lower APRs than title loans but can still be higher than unsecured personal loans for prime borrowers.

The biggest risk, however, is the risk of repossession. If you fail to repay the loan according to the agreed-upon terms, the lender has the legal right to repossess your vehicle. This can lead to a complete loss of your transportation, which could, in turn, affect your ability to get to work and earn income, trapping you in a cycle of debt. Common mistakes to avoid include not fully understanding the repayment terms, underestimating the total cost of the loan, and borrowing more than you can realistically afford to pay back. Always consider your ability to repay the loan without jeopardizing your financial stability.

Are You Eligible? Key Requirements for Securing Your Loan

Before you even begin the application process, it’s vital to assess your eligibility. Lenders have specific criteria they look for, focusing on both your vehicle and your personal financial situation. Understanding these requirements upfront can save you time and increase your chances of approval.

Vehicle Requirements: What Your Car Needs

The cornerstone of any loan using your car is, naturally, the car itself. Lenders will primarily evaluate its value and your ownership status.

- Clear This is non-negotiable for most car title loans. A clear title means you own your vehicle outright, and there are no existing liens from previous loans or creditors. For auto equity loans, you might still be making payments, but the lender will assess the equity you’ve built up. If you have an existing loan, you’ll need sufficient equity for the new loan to cover the old one, or for the new lender to take a secondary lien.

- Vehicle Value and Appraisal: Lenders will need to determine how much your car is worth. This usually involves an appraisal, which considers the make, model, year, mileage, and overall condition of your vehicle. Newer cars with lower mileage and in excellent condition will typically qualify for higher loan amounts. The loan amount offered will be a percentage (often 25-50%) of this appraised value.

- Age and Condition: While there isn’t a strict age limit for all vehicles, very old cars or those in poor mechanical condition may not qualify, or might only secure a very small loan. Lenders prefer vehicles that are easily resalable in case of repossession.

Personal Requirements: Proving Your Ability to Repay

Beyond your vehicle, lenders need assurance that you can and will repay the loan. This involves a few personal and financial criteria.

- Proof of Identity and Residency: You’ll need a valid government-issued photo ID (like a driver’s license) to confirm your identity. Proof of residency, such as a utility bill or bank statement with your address, is also typically required. You must also be of legal age to enter into a contract in your state, usually 18 years old.

- Steady Income: This is critical. Lenders want to see that you have a consistent source of income that demonstrates your ability to make regular payments. This doesn’t always mean a traditional W-2 job; it could include social security benefits, disability payments, self-employment income, or even unemployment benefits, depending on the lender and state regulations.

- Proof of Insurance: Some lenders may require you to have comprehensive and collision insurance on your vehicle to protect their collateral. This is a standard practice for secured loans to mitigate risk.

The Role of Your Credit Score (or lack thereof)

One of the reasons many individuals explore loans using your car is that they can be more accessible to those with less-than-perfect credit. For many car title loans, your credit score is often not the primary factor in the approval process. Because the loan is secured by your vehicle’s title, the lender’s risk is mitigated by the collateral.

However, it’s not entirely irrelevant. For auto equity loans, especially those with longer terms and larger amounts, lenders might still perform a soft credit check to get an idea of your financial behavior. Even if your score is low, demonstrating a stable income stream and a clear ability to repay significantly boosts your chances. Pro tip from us: While a low credit score might not disqualify you, a history of consistent income shows responsibility, which lenders value highly. Don’t assume bad credit means no chance; focus on proving your repayment capacity.

The Step-by-Step Process to Get Your Car Loan

Navigating the application process for a loan using your car can seem daunting, but by breaking it down into manageable steps, you can approach it with confidence and clarity. Based on my experience, a structured approach significantly increases your chances of a smooth transaction.

Step 1: Research and Choose a Reputable Lender

This initial step is perhaps the most crucial. The market for car-secured loans can be diverse, with various lenders offering different terms, rates, and customer service levels.

- Online vs. Brick-and-Mortar: You can apply for these loans both online and in person. Online lenders offer convenience and often quicker processing, while local lenders might provide a more personalized experience.

- Importance of Licensed Lenders: Always ensure the lender is licensed and regulated in your state. This protects you from predatory practices and ensures they adhere to consumer protection laws. Check for their licensing information on their website or inquire directly.

- Reviews and Transparency: Read customer reviews and look for lenders with a reputation for transparency regarding fees, interest rates, and repayment terms. Avoid any lender that pressures you or seems unwilling to clearly explain all aspects of the loan agreement. Based on my experience, thorough research here saves a lot of headaches later and can protect you from falling into a debt trap.

Step 2: Gather Your Documents

Once you’ve identified a few potential lenders, the next step is to prepare your paperwork. Having everything ready expedites the application process significantly.

- Vehicle The original, clear title to your vehicle is paramount.

- Government-Issued ID: A valid driver’s license or state ID.

- Proof of Income: Recent pay stubs, bank statements, tax returns, or benefit statements.

- Proof of Residency: A utility bill, lease agreement, or bank statement.

- Proof of Insurance: Your vehicle’s insurance card or policy declaration page.

- References (Optional): Some lenders may ask for personal or professional references.

Step 3: Vehicle Appraisal

The lender needs to assess your car’s market value to determine the loan amount they can offer. This process varies slightly depending on the lender.

- Online Estimate: Many online lenders start with an initial estimate based on your car’s make, model, year, and mileage, often using tools like Kelley Blue Book or NADA Guides.

- Physical Inspection: Most lenders will require a brief physical inspection of your vehicle. This allows them to verify its condition, mileage, and ensure it matches the details on the title. The inspection is usually quick, often taking less than 15-30 minutes, and can sometimes be done at your home, at the lender’s office, or even virtually through photos and video. What affects value includes the overall condition, any modifications, and any existing damage.

Step 4: Application Submission

With your documents gathered and vehicle appraised, you’re ready to submit your application.

- Filling Out Forms Accurately: Whether online or in person, take your time to fill out all application forms completely and accurately. Any discrepancies could cause delays or even rejection.

- Disclosure of Information: Be honest about your financial situation and your ability to repay. Providing false information can lead to severe consequences. The lender will use the information you provide, along with the vehicle appraisal, to formulate a loan offer.

Step 5: Reviewing the Loan Offer

This is a critical stage where you need to exercise diligence. Do not rush this step.

- Key Terms to Scrutinize:

- Principal Loan Amount: How much cash you will receive.

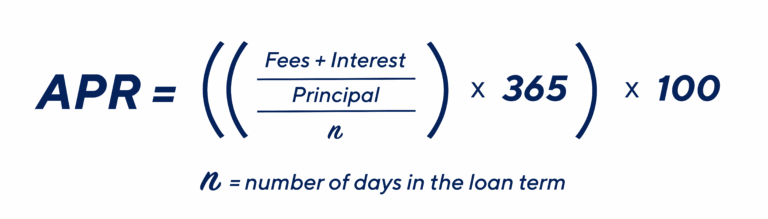

- Interest Rate (APR): The true annual cost of borrowing, including all fees. Compare APRs from different lenders.

- Fees: Look for origination fees, processing fees, late payment fees, and any prepayment penalties.

- Repayment Schedule: Understand the frequency and amount of your payments (weekly, bi-weekly, monthly) and the total number of payments.

- Total Cost of the Loan: Calculate how much you will pay back in total, including principal and interest.

- Default Consequences: Clearly understand what happens if you cannot make payments, including the process for repossession.

- Pro tip from us: Always read the fine print! If anything is unclear, ask the lender for clarification until you fully understand every clause in the agreement. Don’t be afraid to walk away if the terms seem predatory or if you feel uncomfortable.

Step 6: Receiving Funds

Once you’ve reviewed and signed the loan agreement, the funds will be disbursed.

- Quick Funding: One of the advantages of these loans is their speed. Funds can often be disbursed on the same day or within 24 hours of approval.

- Disbursement Methods: Lenders typically offer various methods for receiving your funds, including direct deposit to your bank account, a check, or sometimes even cash in hand. Discuss your preferred method with the lender. This rapid access to cash is often why people consider a loan using your car for urgent financial needs.

Responsible Borrowing and Repayment Strategies

Securing a loan using your car is just the first step; managing it responsibly is paramount to avoiding financial difficulties. Without a solid plan, a temporary solution can quickly become a long-term problem.

Understanding Interest Rates and Fees

As mentioned earlier, loans secured by your car, especially car title loans, often come with higher interest rates than traditional bank loans.

- Annual Percentage Rate (APR): Always focus on the APR, as it reflects the true annual cost of your loan, including interest and certain fees. A high APR can quickly inflate the total amount you owe, making even a small loan very expensive over time.

- Hidden Fees: Be vigilant about any additional fees that might not be immediately obvious. These can include application fees, document fees, lien fees, or late payment charges. Always ask for a full breakdown of all costs associated with the loan. Understanding these numbers is crucial for calculating the true expense of your vehicle collateral loan.

Crafting a Repayment Plan

A detailed and realistic repayment plan is your best defense against default and repossession.

- Budgeting: Before you even apply, create a strict budget that accounts for your loan payments. Identify where you can cut unnecessary expenses to free up funds specifically for repayment. This proactive approach helps ensure you don’t overextend yourself.

- Setting Aside Funds: Once approved, treat your loan payments as a priority. Consider setting up automatic payments if your lender offers them, or dedicate a specific portion of your income each pay period to cover the loan.

- Avoid Late Payments: Late payment fees can add up quickly, increasing your overall debt. More critically, consistent late payments can signal to the lender that you’re struggling, potentially leading to default proceedings.

What Happens if You Can’t Repay?

Despite your best intentions, unforeseen circumstances can sometimes make repayment difficult. Knowing the potential consequences and your options is vital.

- Communication with Lender: If you anticipate missing a payment, immediately contact your lender. Some lenders may be willing to work with you, offering a payment extension or a modified payment plan. Open communication is always better than ignoring the problem.

- Refinancing Options: In some cases, lenders might offer to refinance your loan, potentially extending the term but often at an additional cost. While this might lower your monthly payment, it could increase the total interest paid over the life of the loan.

- Repossession: This is the most severe consequence. If you default on your loan, the lender has the legal right to repossess your vehicle. They can then sell it to recover their money. This not only means losing your car but can also negatively impact your credit score and potentially leave you owing a deficiency balance if the car sells for less than the outstanding loan amount. Understanding the financial consequences of default is essential for responsible borrowing.

Common Mistakes to Avoid

Based on my professional experience, there are several common pitfalls borrowers often fall into when securing loans using their car:

- Not Comparing Lenders: Settling for the first offer without shopping around means you might miss out on better rates and terms.

- Borrowing More Than Needed: Only borrow the exact amount you require. Taking out more money than necessary means you’ll pay more in interest.

- Ignoring Repayment Capacity: Don’t just look at the monthly payment; consider if you can comfortably afford it without sacrificing other essential expenses. Overstretching your budget is a recipe for disaster.

- Not Reading the Fine Print: As emphasized before, every clause in the loan agreement is important. Don’t sign anything you don’t fully understand.

- Using the Loan for Non-Essentials: These loans are best reserved for genuine emergencies, not discretionary spending. Using them for vacations or luxury items can lead to regret and financial strain.

Exploring Alternatives to Car-Secured Loans

While a loan using your car can be a lifeline in a crisis, it’s always wise to explore all available options before committing to a high-interest, secured loan. Sometimes, alternatives might be more suitable or less costly depending on your specific situation.

- Personal Loans: If you have decent credit, an unsecured personal loan from a bank or credit union typically offers much lower interest rates and more flexible repayment terms. If you’re exploring other options, our comprehensive guide on might be helpful to weigh your choices.

- Credit Union Loans: Credit unions are member-owned and often offer more favorable rates and terms than traditional banks, especially for members with less-than-perfect credit. They also tend to be more understanding and flexible.

- Secured Credit Cards: For building credit, a secured credit card can be a safer option. You deposit money into an account, and that becomes your credit limit. It helps build a positive credit history without the immediate risk of losing an asset.

- Asking Friends or Family: While it can be uncomfortable, borrowing from trusted friends or family, with clear repayment terms, can be a zero-interest or low-interest alternative.

- Debt Consolidation: If your need for cash is to manage existing debt, exploring debt consolidation loans or credit counseling services might be a better long-term strategy. Explore strategies in our article, .

- Negotiating with Creditors: Sometimes, the best solution is to directly negotiate with the party you owe money to. Many companies are willing to work out a payment plan or offer temporary hardship relief rather than risk non-payment.

For further reliable information on consumer financial products and your rights, consider visiting the Consumer Financial Protection Bureau (CFPB) website (https://www.consumerfinance.gov/). This external resource provides unbiased guidance and tools to help you make informed financial decisions.

Conclusion: Making an Informed Decision About Your Vehicle Collateral Loan

Getting a loan using your car can provide immediate financial relief during unexpected emergencies. It offers a unique pathway for individuals, particularly those with challenging credit histories, to access much-needed funds by leveraging the value of their vehicle. However, it’s a financial tool that demands respect, careful consideration, and a thorough understanding of its implications.

The journey from needing cash to successfully securing and repaying an auto-secured loan involves several critical steps: from understanding the different types of loans and assessing your eligibility, to meticulously researching lenders, gathering documents, undergoing vehicle appraisal, and, most importantly, scrutinizing the loan offer. Each stage is crucial in ensuring you make a decision that aligns with your financial well-being.

Remember, the goal is not just to get the loan, but to repay it responsibly and avoid the significant risks, particularly the potential loss of your vehicle. By prioritizing responsible borrowing, crafting a realistic repayment plan, and being fully aware of the interest rates, fees, and potential consequences of default, you can navigate this option effectively. Always weigh the benefits against the risks, explore all available alternatives, and never hesitate to seek clarification on any aspect of the loan agreement. Your car is a valuable asset; use its financial potential wisely and with foresight to secure your future, not jeopardize it.