Unlock Your Dream Car: A Comprehensive Guide to the Scotiabank Car Loan Calculator

Unlock Your Dream Car: A Comprehensive Guide to the Scotiabank Car Loan Calculator Carloan.Guidemechanic.com

Buying a car is a significant life event for many, often marking a new chapter of independence, convenience, or family growth. However, the excitement of choosing the perfect vehicle can quickly turn into apprehension when faced with the complexities of financing. Understanding how much you can afford, what your monthly payments will look like, and the total cost of your loan is crucial for making a smart financial decision.

This is where powerful tools like the Scotiabank Car Loan Calculator come into play. Far more than just a simple arithmetic tool, it’s a strategic partner in your car-buying journey. In this in-depth guide, we’ll explore every facet of this essential calculator, helping you navigate the world of auto financing with confidence and clarity.

Unlock Your Dream Car: A Comprehensive Guide to the Scotiabank Car Loan Calculator

The Power of Planning: What is the Scotiabank Car Loan Calculator?

At its core, the Scotiabank Car Loan Calculator is an online tool designed to help prospective car buyers estimate their potential loan payments. It allows you to input various financial figures, such as the desired loan amount, interest rate, and repayment term, to instantly calculate your estimated monthly or bi-weekly payments. This immediate feedback empowers you to understand the financial implications of different borrowing scenarios.

Think of it as your personal financial simulator for car purchases. Before you even step foot in a dealership, this calculator can provide a realistic picture of your financial commitment. It helps transform abstract figures into concrete, manageable numbers, giving you a clear path forward.

Based on my experience in personal finance, neglecting to use such a tool is a common oversight. Many buyers focus solely on the car’s sticker price, forgetting the long-term impact of interest and loan terms. The calculator brings these vital elements into sharp focus, ensuring you consider the full financial picture.

Your Step-by-Step Guide: How to Effectively Use the Scotiabank Car Loan Calculator

Using the Scotiabank Car Loan Calculator is straightforward, but understanding each input field’s significance is key to maximizing its value. Let’s break down the typical components you’ll encounter:

1. The Loan Amount (Purchase Price – Down Payment – Trade-in)

This is the principal amount you intend to borrow. It’s not simply the sticker price of the car. Instead, it’s the vehicle’s purchase price minus any down payment you make and the value of any trade-in you offer. A higher loan amount will naturally result in higher monthly payments and a greater total interest paid over the life of the loan.

Pro Tip: Be realistic about the car’s price. Research average market values for the specific make and model you’re interested in. Don’t forget to factor in potential sales taxes and other applicable fees that might be rolled into the loan if not paid upfront.

2. The Interest Rate (APR – Annual Percentage Rate)

The interest rate is arguably the most critical factor influencing the total cost of your loan. It represents the cost of borrowing money, expressed as a percentage of the principal. Scotiabank, like other lenders, determines your interest rate based on several factors, primarily your credit score, current market rates, and the loan term.

Even a difference of one or two percentage points can significantly alter your total payments. A lower interest rate means less money paid back to the bank over time, making your loan more affordable. This is where pre-approval can be incredibly beneficial, as it gives you a concrete rate to plug into the calculator.

3. The Loan Term (Amortization Period)

The loan term, or amortization period, refers to the length of time you have to repay the loan, typically expressed in months (e.g., 60 months, 72 months, 84 months). This variable has a direct inverse relationship with your monthly payments: a longer term usually means lower monthly payments, but it also means you’ll pay more in total interest over the life of the loan.

Conversely, a shorter loan term results in higher monthly payments but significantly reduces the total interest paid. It’s a delicate balance between managing your monthly budget and minimizing the overall cost of borrowing. Based on my experience, many buyers gravitate towards longer terms for lower monthly payments without fully grasping the extra interest they’ll accrue.

4. The Down Payment

While not always a mandatory field, incorporating a down payment into your calculations is a wise move. A down payment is an upfront cash payment you make towards the purchase price of the car. It reduces the amount you need to borrow, thereby lowering your loan amount, subsequent monthly payments, and the total interest you’ll pay.

A substantial down payment also demonstrates financial stability to lenders, which can sometimes lead to more favorable interest rates. It immediately builds equity in your vehicle, protecting you against depreciation and potentially preventing you from being "upside down" on your loan (owing more than the car is worth).

The Variables That Drive Your Scotiabank Car Loan: A Deeper Dive

Beyond simply inputting numbers, understanding the underlying factors that influence these variables will give you a significant edge in securing favorable financing.

Understanding Loan Amount Dynamics

The true loan amount you need is derived from the vehicle’s negotiated price, less your down payment and any trade-in value. This figure is critical because it directly dictates the principal on which interest is calculated. Every dollar you reduce from the principal through a larger down payment or a good trade-in deal translates into substantial savings over the loan term.

Consider not just the car’s price, but also accessories, extended warranties, or protection packages that might be rolled into the loan. While these can be convenient, they also increase your borrowed amount and, consequently, your interest payments. Scrutinize these additions carefully to ensure they align with your budget and needs.

The Crucial Role of Your Interest Rate

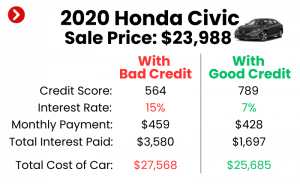

Your interest rate is profoundly impacted by your creditworthiness. Scotiabank, like any lender, assesses your credit score and history to determine your risk profile. A higher credit score signals a lower risk, often qualifying you for the most competitive rates. It’s always a good idea to check your credit score before applying for any loan.

Market conditions also play a part; general interest rates set by central banks can influence what lenders offer. Furthermore, the type of car (new vs. used) and the loan term itself can affect the rate. Sometimes, a shorter term might come with a slightly lower rate because the lender’s risk exposure is reduced.

Navigating the Loan Term Trade-off

Choosing the right loan term is a balancing act. A 60-month term versus an 84-month term for the same car can mean hundreds, if not thousands, of dollars in difference in total interest paid. While an 84-month term might make a luxury car seem affordable monthly, you could end up paying back 1.5 times the car’s value by the end of the loan.

Common mistakes to avoid are: blindly opting for the longest term just to achieve the lowest monthly payment. Always compare the total cost of the loan across different terms. The goal is to find the shortest term you can comfortably afford, minimizing the amount of interest you pay over time.

The Strategic Advantage of a Down Payment

A solid down payment is one of your most powerful financial tools when buying a car. It not only reduces your borrowing amount but also provides a buffer against rapid depreciation. Most new cars lose a significant portion of their value in the first few years. A strong down payment ensures you’re less likely to owe more than the car is worth if you need to sell it early.

Furthermore, lenders view a larger down payment as a sign of financial responsibility, which can sometimes translate into better loan terms. Aim for at least 10-20% of the car’s purchase price if possible. Even a smaller down payment is better than none.

The Undeniable Benefits of Using the Scotiabank Car Loan Calculator

Utilizing this calculator offers a multitude of advantages that go beyond simple arithmetic.

1. Empowered Budgeting and Financial Planning

The calculator gives you a clear, immediate picture of how a car loan will impact your monthly budget. By inputting different scenarios, you can determine what payment fits comfortably within your existing financial commitments. This foresight prevents financial strain and helps you maintain a healthy cash flow.

Based on my experience, many people overestimate what they can truly afford. The calculator provides a reality check, allowing you to align your car aspirations with your financial realities.

2. Strategic Scenario Comparison

Want to see the difference between a 60-month and a 72-month loan? Or how a larger down payment affects your monthly payment and total interest? The Scotiabank Car Loan Calculator allows for quick "what-if" analyses. This flexibility helps you explore various options and pinpoint the financing structure that best suits your goals.

You can compare how a slightly higher interest rate impacts your total cost versus a slightly longer loan term. This dynamic comparison is invaluable for informed decision-making.

3. Enhanced Negotiation Power

Knowing your precise budget and pre-approved interest rate before you talk to a dealership puts you in a much stronger negotiating position. You won’t be swayed by dealer financing offers that might not be as competitive as what you’ve already secured or calculated. You can confidently discuss pricing and loan terms, knowing your financial boundaries.

Pro tips from us: Always get a pre-approval from Scotiabank or another lender before stepping into the dealership. This provides a benchmark rate and empowers you to negotiate the car’s price separately from the financing.

4. Avoiding Financial Surprises

There’s nothing worse than signing on the dotted line only to realize your monthly payments are higher than anticipated or the total cost of the loan is overwhelming. The calculator helps you avoid these unwelcome surprises by giving you accurate estimates upfront. It fosters financial transparency and reduces post-purchase anxiety.

It’s about making an informed decision, not an emotional one. The calculator helps ground your excitement in financial prudence.

Beyond the Calculator: Comprehensive Considerations for Your Scotiabank Car Loan

While the calculator is an excellent tool, it’s only one piece of the car-buying puzzle. Here’s what else you should consider when planning your Scotiabank car loan:

Your Credit Score: The Unseen Force

Your credit score is paramount. A good to excellent credit score (typically 680+) will open doors to the best interest rates Scotiabank offers, significantly reducing the total cost of your loan. If your score isn’t where you want it to be, take steps to improve it before applying. Pay bills on time, reduce outstanding debt, and avoid opening too many new credit lines.

Understanding your credit report is also vital. You can obtain a free copy from Equifax or TransUnion annually. Review it for any errors that might be negatively impacting your score.

The Power of Pre-Approval

Getting pre-approved for a Scotiabank car loan before you shop provides a concrete loan amount and interest rate. This not only gives you peace of mind but also allows you to focus solely on negotiating the car’s price at the dealership. It separates the car-buying process from the loan-getting process, simplifying both.

A pre-approval from Scotiabank also gives you leverage. If a dealership offers financing, you’ll have a benchmark to compare it against, ensuring you get the best deal.

Insurance: A Non-Negotiable Cost

Car insurance is a mandatory expense that the loan calculator won’t include. Obtain quotes from several insurance providers before finalizing your car purchase. Insurance premiums can vary widely based on the car’s make and model, your driving history, age, and location. Don’t let insurance costs become an unexpected burden.

For example, a sports car will almost certainly cost more to insure than a family sedan. Factor this into your overall monthly budget.

Ongoing Maintenance and Fuel Costs

Beyond loan payments and insurance, remember the recurring costs of car ownership: fuel, routine maintenance (oil changes, tire rotations), and potential repairs. These expenses aren’t part of your loan, but they are crucial for your overall budget. Research typical maintenance costs for the vehicles you’re considering.

A reliable vehicle with good fuel efficiency will save you money in the long run. Don’t let the initial excitement overshadow these practical, ongoing expenses.

Maximizing Your Trade-in Value

If you have an existing vehicle, research its market value thoroughly before heading to the dealership. Websites like Kelley Blue Book or Canadian Black Book can provide estimated trade-in values. Knowing your car’s worth empowers you to negotiate a fair price and reduces the amount you need to borrow for your new vehicle.

Consider selling your old car privately if you want to maximize its value, as this often yields more than a dealership trade-in. However, selling privately requires more effort and time.

Pro Tips for Smart Car Financing with Scotiabank

Here are some expert recommendations to ensure you get the best possible Scotiabank car loan deal:

- Save for a Larger Down Payment: The more you put down upfront, the less you borrow, which means lower payments and less interest over time. It’s the simplest way to reduce your total cost of ownership.

- Know Your Credit Score: Before applying, check your credit report. A good score is your ticket to better rates. If it’s low, take steps to improve it first.

- Shop Around for Rates: While you might prefer Scotiabank, it’s wise to compare offers from other lenders. This ensures you’re getting the most competitive interest rate available to you.

- Don’t Stretch the Loan Term Too Long: Resist the temptation of ultra-long loan terms (e.g., 84 or 96 months). While they offer lower monthly payments, they significantly increase the total interest paid and keep you in debt longer.

- Focus on Total Cost, Not Just Monthly Payment: Always look at the grand total you’ll pay over the loan’s life, including interest. A low monthly payment can mask a very expensive overall loan.

- Read the Fine Print: Understand all terms and conditions of your loan agreement, including any prepayment penalties, late fees, and insurance requirements.

Common Mistakes to Avoid When Using a Car Loan Calculator (and Financing in General)

Based on my experience, many buyers fall into predictable traps. Being aware of these can save you a lot of money and stress:

- Ignoring Total Interest Paid: Focusing solely on the monthly payment without considering the total interest you’ll pay is a major blunder. The calculator shows you both; pay attention to the sum.

- Forgetting Other Costs: The calculator provides loan estimates, but it doesn’t account for insurance, maintenance, fuel, or registration fees. These can add hundreds of dollars to your monthly expenses.

- Underestimating Your Credit Score’s Impact: A poor credit score can drastically increase your interest rate, making your car significantly more expensive. Don’t assume you’ll get the advertised "best rates."

- Not Getting Pre-Approved: Without pre-approval, you’re negotiating blind at the dealership. This makes you vulnerable to less favorable financing offers.

- Being Emotional: Car buying is exciting, but don’t let emotions override financial common sense. Stick to your budget and what the calculator tells you is affordable.

Conclusion: Your Road to a Confident Car Purchase Starts Here

The journey to owning a new car is thrilling, but it demands careful financial planning. The Scotiabank Car Loan Calculator is an indispensable tool that simplifies this process, empowering you to make informed, intelligent decisions. By understanding its functions, the variables at play, and integrating it into a comprehensive financial strategy, you can confidently navigate the world of auto financing.

Don’t just dream about your next car; plan for it wisely. Utilize the Scotiabank Car Loan Calculator to explore your options, understand your financial commitments, and ultimately, drive away with the perfect vehicle that fits comfortably into your life and budget. Start calculating today, and pave your way to a smart, stress-free car purchase.

Internal Links:

- Understanding Your Credit Score: A Guide to Boosting Your Financial Health (Simulated link)

- Negotiating Like a Pro: Tips for Getting the Best Car Price (Simulated link)

External Link:

- For more information on car loan rights and responsibilities in Canada, visit the Financial Consumer Agency of Canada (FCAC) website: https://www.canada.ca/en/financial-consumer-agency/services/buying-car.html (This is a trusted external source for Canadian financial consumers).