Unlock Your Dream Car: A Deep Dive into the NCSECU Car Loan Calculator

Unlock Your Dream Car: A Deep Dive into the NCSECU Car Loan Calculator Carloan.Guidemechanic.com

Buying a car is a significant financial decision, often ranking as one of the largest purchases many individuals make after a home. It’s an exciting prospect, but the financial implications can quickly become overwhelming without the right tools and understanding. This is where the NCSECU Car Loan Calculator becomes an invaluable asset, transforming a complex process into a clear, manageable journey.

As an expert blogger and professional SEO content writer, I’ve seen countless individuals navigate the choppy waters of car financing. Based on my experience, leveraging a reliable car loan calculator like NCSECU’s is not just a convenience; it’s a strategic necessity. This comprehensive guide will peel back the layers of car financing, showing you exactly how to use the NCSECU Car Loan Calculator to your advantage, understand its results, and make truly informed decisions that align with your financial goals.

Unlock Your Dream Car: A Deep Dive into the NCSECU Car Loan Calculator

What is the NCSECU Car Loan Calculator and Why is it Essential?

At its core, the NCSECU Car Loan Calculator is a digital tool designed to estimate your potential car loan payments. It allows you to input various financial figures related to a car purchase and instantly receive an estimated monthly payment. This isn’t just a simple math exercise; it’s a window into your financial future.

Many people dive into car shopping without a clear understanding of what they can truly afford. This often leads to sticker shock, disappointment, or worse, committing to a loan that strains their budget. The NCSECU calculator empowers you to avoid these pitfalls by providing realistic payment scenarios before you even set foot on a dealership lot. It helps you grasp the intricate relationship between the loan amount, interest rate, and repayment term.

Think of it as your personal financial compass in the world of auto loans. It helps you budget effectively, compare different vehicle options, and confidently negotiate prices knowing your financial boundaries. This proactive approach not only saves you money in the long run but also reduces stress during the car buying process.

Key Inputs for the NCSECU Car Loan Calculator

To get the most accurate results from the NCSECU Car Loan Calculator, you need to understand the critical pieces of information it requires. Each input plays a vital role in shaping your estimated monthly payment and the overall cost of your auto loan. Let’s break them down in detail.

1. Loan Amount (or Vehicle Price)

This is the starting point for any car loan calculation. It refers to the total amount you need to borrow after any down payment and trade-in value have been applied. If you’re just starting, you might input the anticipated purchase price of the vehicle.

It’s crucial to remember that the loan amount isn’t just the car’s sticker price. It includes the vehicle’s cost, potentially some dealer fees, and sales tax, minus any contributions you make upfront. Accurately estimating this figure is the first step towards a realistic calculation.

2. Interest Rate (APR)

The interest rate, often expressed as an Annual Percentage Rate (APR), is arguably the most impactful variable. This is the cost you pay to borrow the money, calculated as a percentage of the principal loan amount. A higher interest rate means a higher monthly payment and a greater total cost over the life of the loan.

NCSECU, like other lenders, determines your interest rate based on several factors, including your credit score, the loan term, and the age of the vehicle. Based on my experience, securing a competitive interest rate is paramount. Even a small difference can save you hundreds, if not thousands, of dollars over the loan’s duration.

3. Loan Term (Repayment Period)

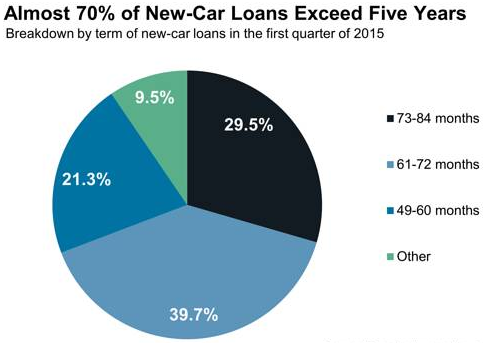

The loan term refers to the length of time you have to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72, or even 84 months). This input has a direct and significant impact on your monthly payment.

A longer loan term will result in lower monthly payments, which might seem appealing initially. However, it also means you’ll pay more interest over the life of the loan. Conversely, a shorter loan term will lead to higher monthly payments but significantly less interest paid overall. Balancing affordability with the total cost is a key consideration here.

4. Down Payment

A down payment is the initial amount of money you pay towards the purchase of the car, reducing the total amount you need to borrow. This is a powerful tool for financial savvy car buyers.

A substantial down payment offers several benefits: it lowers your monthly payments, reduces the total interest you’ll pay, and decreases your loan-to-value (LTV) ratio, which can sometimes qualify you for a better interest rate. Pro tips from us: always aim for the largest down payment you can comfortably afford without depleting your emergency savings.

5. Trade-in Value (if applicable)

If you’re trading in your current vehicle, its value can act much like a down payment, reducing the principal amount you need to finance. The calculator will factor this directly into the loan amount.

It’s wise to get an independent appraisal of your trade-in value before heading to the dealership. This ensures you have a strong negotiating position and can input a realistic figure into the calculator. This simple step can prevent you from undervaluing your existing asset.

6. Sales Tax, Fees, and Other Costs

While some calculators might not explicitly ask for these, it’s crucial to factor them into your overall budget. Sales tax varies by state and can add a significant amount to the total purchase price. There might also be documentation fees, registration fees, and other charges.

Common mistakes to avoid are focusing solely on the vehicle’s price and forgetting these additional expenses. They can quickly inflate your required loan amount or reduce the actual cash you have available for a down payment. Always research the specific taxes and fees applicable in your area.

How to Effectively Use the NCSECU Car Loan Calculator: A Step-by-Step Guide

Using the NCSECU Car Loan Calculator is straightforward, but maximizing its potential requires a strategic approach. Here’s how you can use it to gain clarity and control over your car financing journey.

Step 1: Gather Your Information

Before you even open the calculator, have your key figures ready. This includes your estimated desired loan amount (or vehicle price), your potential down payment, and any trade-in value. If you’ve already been pre-approved by NCSECU, you’ll have a specific interest rate to input. If not, you might start with an estimated rate based on typical rates for your credit score range.

Having these numbers at hand ensures a smooth and efficient calculation process. Don’t guess; aim for accuracy.

Step 2: Input the Core Data

Navigate to the NCSECU Car Loan Calculator on their official website (or a similar reputable tool). You will typically find fields for:

- Loan Amount/Vehicle Price: Enter the total cost of the car you’re considering.

- Interest Rate (APR): Input the rate you anticipate or have been pre-approved for.

- Loan Term (Months): Select the desired repayment period.

- Down Payment: Enter the amount you plan to put down.

- Trade-in Value: If applicable, input your vehicle’s trade-in worth.

These fields are designed to be intuitive and user-friendly, allowing for quick data entry.

Step 3: Experiment with Different Scenarios

This is where the real power of the calculator comes into play. Don’t just run one calculation. Experiment!

- Vary the Loan Term: See how a 60-month loan compares to a 72-month loan in terms of monthly payment and total interest. You’ll likely notice a significant difference.

- Adjust the Down Payment: Increase your hypothetical down payment to understand its impact on your monthly obligation.

- Consider Different Interest Rates: If you’re not pre-approved, try a range of interest rates (e.g., 4.5%, 5.0%, 5.5%) to see how your payments change based on your potential creditworthiness.

By running multiple scenarios, you gain a holistic understanding of how each variable influences your financial commitment. This is crucial for making an informed decision.

Step 4: Understand and Analyze Your Results

Once you hit "calculate," the tool will instantly display your estimated monthly payment. But don’t stop there. Look for additional details like the total interest paid over the loan term and the total cost of the car (principal + interest).

Pro tips from us: Pay close attention to the total interest paid. While a low monthly payment might seem attractive, a long loan term can dramatically increase the overall cost of the vehicle due to accumulated interest. This broader perspective is key to long-term financial health.

Step 5: Refine Your Car Search

With a clear understanding of your affordable monthly payment range and total loan costs, you can now refine your car search. This might mean adjusting your target vehicle price, saving more for a down payment, or exploring different loan terms. The calculator empowers you to set realistic expectations and make data-driven decisions.

Understanding Your Results: What the Calculator Tells You

The numbers generated by the NCSECU Car Loan Calculator are more than just figures; they are insights into your financial capacity and the true cost of your desired vehicle. Interpreting these results correctly is crucial for sound decision-making.

Estimated Monthly Payment

This is typically the most prominent result and the one most car buyers focus on. It tells you exactly how much money you’ll need to set aside each month to cover your car loan. This number is vital for budgeting.

However, based on my experience, it’s a common mistake to focus only on this figure. While affordability is key, a low monthly payment achieved through an excessively long loan term can hide significant long-term costs. Always consider this in conjunction with the total interest paid.

Total Interest Paid

This figure reveals the entire amount of money you will pay purely as interest over the life of the loan. It’s the "cost of borrowing." This number is often eye-opening, as it highlights how much extra you pay beyond the vehicle’s initial price.

Understanding this allows you to compare different loan scenarios effectively. A loan with a slightly higher monthly payment but a much lower total interest paid might be the more financially prudent choice in the long run.

Total Cost of the Car

This is the ultimate figure you need to grasp. It combines the principal loan amount (the car’s price minus down payment/trade-in) with the total interest paid. This represents the true, all-inclusive cost of owning the car through financing.

When comparing vehicles or loan options, always look at the total cost. This provides the clearest picture of your investment and helps you make a decision that aligns with your overall financial strategy.

Affordability vs. Desirability: Making Informed Decisions

The calculator helps you bridge the gap between what you want and what you can realistically afford. If your desired car pushes your estimated monthly payment beyond your comfort zone, the calculator provides concrete data to adjust your expectations. This might mean choosing a less expensive model, increasing your down payment, or opting for a shorter loan term if your budget allows.

This tool transforms abstract desires into concrete financial realities, leading to more sustainable and less stressful car ownership.

Beyond the Calculator: NCSECU Car Loan Application Process

While the NCSECU Car Loan Calculator is an excellent planning tool, it’s just one part of the journey. Once you have a clear financial picture, the next step is to engage with NCSECU for an actual loan.

Membership Requirements

NCSECU is a credit union, which means you need to be a member to access their services, including auto loans. Membership eligibility typically revolves around living, working, or attending school in North Carolina, or being a relative of an existing member.

Pro tips from us: If you’re not yet a member, explore their eligibility requirements early in your process. Joining a credit union often comes with benefits like lower interest rates and personalized service, making it a worthwhile step. You can find detailed membership information on their official website.

Pre-Approval: Why It’s a Smart Move

Based on my experience, seeking pre-approval is one of the smartest moves you can make. Pre-approval from NCSECU means they have reviewed your creditworthiness and agreed to lend you a specific amount at a particular interest rate, usually for a set period.

This offers several advantages:

- Budget Clarity: You know exactly how much you can spend, empowering you during negotiations.

- Negotiating Power: You become a cash buyer in the eyes of the dealership, often leading to better deals.

- Speed: It streamlines the purchase process at the dealership.

- Confidence: You shop with peace of mind, knowing your financing is secured.

Required Documents

When you apply for an NCSECU auto loan, whether for pre-approval or a direct application, you’ll need to provide certain documents. These typically include:

- Proof of identity (driver’s license, state ID).

- Proof of income (pay stubs, tax returns).

- Proof of residence (utility bill, lease agreement).

- Vehicle information (if you’ve already chosen a car).

Having these documents organized and ready can significantly expedite your application process.

Application Steps

The NCSECU auto loan application process is typically straightforward:

- Initiate Application: You can usually apply online, by phone, or in person at an NCSECU branch.

- Provide Information: Fill out the application form with personal, financial, and employment details.

- Credit Check: NCSECU will perform a credit check to assess your creditworthiness.

- Review Offer: If approved, you’ll receive an offer outlining the loan amount, interest rate, and terms.

- Finalize Loan: Once you accept the offer and provide any necessary documentation, the loan can be finalized.

Maximizing Your NCSECU Car Loan Benefits

Securing a car loan is more than just getting approved; it’s about optimizing the terms to benefit your financial health. NCSECU offers several avenues to help members maximize their car loan advantages.

Improving Your Credit Score Before Applying

Your credit score is a primary determinant of your interest rate. A higher score typically translates to a lower APR, saving you thousands over the loan’s life. Before you even think about applying, take steps to improve your credit.

This includes paying bills on time, reducing existing debt, and checking your credit report for errors. Even a few points increase can make a tangible difference in your loan offer. For more tips on improving your credit score, check out our guide on "Boosting Your Credit for Better Loan Rates."

Saving for a Larger Down Payment

As discussed, a larger down payment reduces the amount you need to borrow, thus lowering your monthly payments and the total interest paid. It also signals financial stability to lenders, potentially leading to better terms.

If you’re not in a rush, consider delaying your car purchase for a few months to save up a more substantial down payment. This disciplined approach often pays dividends in the long run.

Choosing the Right Loan Term

While a longer loan term offers lower monthly payments, it costs more in interest. Conversely, a shorter term saves interest but comes with higher monthly payments. The "right" term balances these two factors based on your budget and financial goals.

Pro tips from us: Always try to choose the shortest loan term you can comfortably afford. This minimizes the total cost of ownership and helps you pay off debt faster.

Considering NCSECU’s Additional Services

NCSECU often provides additional services that can be beneficial for car owners. These might include:

- GAP Insurance: Covers the difference between what you owe on your loan and your car’s actual cash value if it’s totaled or stolen.

- Extended Warranties: Offer protection beyond the manufacturer’s warranty.

- Payment Protection: Can help cover payments in case of unforeseen circumstances like disability or involuntary unemployment.

Evaluate these options carefully. While they add to the overall cost, they can provide valuable peace of mind and financial protection.

Refinancing Options

If you already have a car loan with another lender, or if your credit score has significantly improved since you first financed your vehicle, NCSECU might offer refinancing options. Refinancing can potentially lower your interest rate, reduce your monthly payments, or shorten your loan term, saving you money.

It’s always a good idea to periodically review your existing loan terms and compare them with current market rates.

Common Mistakes to Avoid When Using a Car Loan Calculator

Even with a powerful tool like the NCSECU Car Loan Calculator, mistakes can happen. Avoiding these common pitfalls ensures you get the most accurate and useful information.

1. Ignoring Additional Costs (Tax, Fees, Insurance)

A common oversight is to calculate only the principal loan amount without factoring in sales tax, registration fees, documentation fees, and the cost of car insurance. These can add thousands of dollars to your overall vehicle expense.

Always consider these "hidden" costs. They can significantly impact your true monthly financial commitment and the total amount you need to borrow or pay upfront.

2. Focusing Only on the Monthly Payment

While crucial, fixating solely on the lowest possible monthly payment can be a trap. As discussed, this often leads to longer loan terms and substantially more interest paid over the life of the loan.

Look at the bigger picture: the total cost of the car, including all interest. A slightly higher monthly payment for a shorter term might be far more cost-effective in the long run.

3. Underestimating Interest Rates

If you haven’t been pre-approved, it’s easy to be overly optimistic about the interest rate you’ll qualify for. Using an unrealistically low interest rate in the calculator will give you a misleadingly low monthly payment.

Pro tips from us: If unsure, use a slightly higher, more conservative estimate for the interest rate, especially if your credit isn’t stellar. This helps you prepare for a worst-case scenario and avoid disappointment.

4. Not Accounting for Future Budget Changes

Your current budget might allow for a certain monthly payment, but consider how your finances might change. Are you planning a career change, having a baby, or facing other significant life events that could impact your income or expenses?

Factor in potential future changes to ensure your car payment remains sustainable. The calculator provides a snapshot, but your financial plan should look ahead.

5. Not Getting Pre-Approved

As highlighted earlier, skipping pre-approval means you’re shopping without knowing your precise financing terms. This puts you at a disadvantage during negotiations and can lead to less favorable loan offers at the dealership.

Always secure pre-approval from NCSECU or another trusted lender before you start serious car shopping. It’s a game-changer.

Real-World Scenarios and Case Studies (Illustrative Examples)

Let’s illustrate the power of the NCSECU Car Loan Calculator with a couple of hypothetical scenarios. These examples demonstrate how different inputs lead to varying outcomes and help you make better decisions.

Scenario 1: New Car Dreamer with Good Credit

- Vehicle Price: $30,000

- Down Payment: $5,000

- Trade-in: $0

- Desired Loan Term: 60 months

- Estimated Interest Rate (Good Credit): 4.0% APR

Using the calculator, the results might show:

- Loan Amount: $25,000

- Estimated Monthly Payment: Approximately $460.40

- Total Interest Paid: Approximately $2,624.00

- Total Cost of Car (excluding down payment): $27,624.00

Analysis: This individual has a manageable monthly payment and pays a reasonable amount of interest over five years. The down payment significantly reduced the principal, making the loan more affordable.

Scenario 2: Used Car Buyer with Average Credit

- Vehicle Price: $18,000

- Down Payment: $2,000

- Trade-in: $1,000

- Desired Loan Term: 72 months

- Estimated Interest Rate (Average Credit): 7.5% APR

Using the calculator, the results might show:

- Loan Amount: $15,000

- Estimated Monthly Payment: Approximately $255.45

- Total Interest Paid: Approximately $3,392.40

- Total Cost of Car (excluding down payment/trade-in): $18,392.40

Analysis: While the monthly payment is lower due to the longer term, the higher interest rate and extended repayment period result in a higher total interest paid compared to Scenario 1, even though the initial loan amount was significantly less. This highlights the impact of interest rates and loan terms. The calculator would immediately show this buyer the true long-term cost of their financing choice.

These scenarios underscore how the calculator allows you to compare different options and understand the financial implications of each choice.

Why NCSECU Stands Out for Car Loans

Beyond providing a robust car loan calculator, NCSECU offers several distinct advantages that make it a compelling choice for auto financing. As a credit union, its operational philosophy differs significantly from traditional banks.

Member-Focused Approach

Unlike banks that primarily serve shareholders, credit unions like NCSECU are member-owned. This structure means their profits are often returned to members in the form of lower loan rates, higher savings rates, and fewer fees. Based on my experience, this translates to a more personalized and supportive lending environment.

NCSECU’s focus is on helping its members achieve their financial goals, not just maximizing profits.

Competitive Rates

Due to their not-for-profit status and member-centric approach, NCSECU often provides highly competitive auto loan rates. These rates can frequently be lower than those offered by larger commercial banks, potentially saving you a substantial amount of money over the life of your loan.

Always compare NCSECU’s rates with other lenders to see the potential savings.

Personalized Service

When you’re a member of NCSECU, you’re not just an account number. You often receive more personalized attention and guidance from loan officers. This can be particularly beneficial if you have unique financial circumstances or need detailed explanations of your loan options.

This human touch can make a significant difference in navigating what can otherwise be a complex financial process.

Community Involvement

NCSECU is deeply rooted in the North Carolina community. Their operations and services are often tailored to the needs of local residents, and they frequently engage in community outreach and support initiatives. This local focus can provide an added sense of trust and reliability.

For more information on NCSECU’s car loan offerings and to use their official calculator, visit the NCSECU Auto Loans page. (Note: This link is illustrative and assumes the official NCSECU auto loans page. Always verify the actual URL).

Pro Tips from an Expert Blogger for a Smooth Car Buying Journey

The journey to your new car doesn’t end with understanding the calculator. Here are some final professional tips to ensure your entire car buying experience is as smooth and stress-free as possible.

- Research Thoroughly: Don’t just research the car; research the market. Understand average prices, common issues for specific models, and dealership reputations.

- Negotiate Wisely: Remember, everything is negotiable, from the car’s price to the trade-in value and even financing terms (though your pre-approval sets a good baseline). Be prepared to walk away if the deal isn’t right.

- Get Multiple Quotes: Don’t limit yourself to one lender or one dealership. Get pre-approved by NCSECU, but also check rates from other credit unions or banks. Compare vehicle prices from several dealerships.

- Read the Fine Print: Before signing any documents, carefully read and understand all terms and conditions of your loan and purchase agreement. If something is unclear, ask for clarification. Don’t be rushed.

- Consider Total Cost of Ownership: Beyond the loan payment, factor in insurance, maintenance, fuel, and potential depreciation when choosing a vehicle. A "cheap" car to buy might be expensive to own.

- Don’t Forget About Trade-In Value: Thinking about trade-ins? Read our article ‘Maximizing Your Trade-In Value: What You Need to Know’ to ensure you get the best deal for your current vehicle.

Conclusion

The NCSECU Car Loan Calculator is far more than just a simple tool; it’s an indispensable guide that empowers you to take control of your car financing journey. By providing a clear, instant estimation of your monthly payments and total costs, it transforms guesswork into informed decision-making.

From understanding the impact of interest rates and loan terms to planning for down payments and avoiding common financial mistakes, this calculator lays the groundwork for a financially sound car purchase. Based on my experience, leveraging such a tool is the cornerstone of responsible budgeting and smart consumer choices.

So, as you embark on the exciting quest for your next vehicle, make sure the NCSECU Car Loan Calculator is your first stop. Arm yourself with knowledge, clarity, and confidence. Start calculating, start planning, and drive off in your dream car without any financial regrets. Happy car hunting!