Unlock Your Dream Car: A Deep Dive into the NFCU Car Loan Calculator and Smart Auto Financing

Unlock Your Dream Car: A Deep Dive into the NFCU Car Loan Calculator and Smart Auto Financing Carloan.Guidemechanic.com

The thrill of a new car is undeniable. Whether it’s the latest model with cutting-edge technology or a reliable used vehicle that perfectly fits your needs, the journey to ownership is exciting. However, the path to driving away in your dream car often involves navigating the complexities of auto financing. This is where a powerful tool like the NFCU Car Loan Calculator becomes indispensable.

Many aspiring car owners dive into dealerships without a clear financial picture. This can lead to stress, overspending, and ultimately, buyer’s remorse. Understanding your budget and potential loan payments before you even start shopping is not just smart; it’s essential. This comprehensive guide will walk you through everything you need to know about the NFCU Car Loan Calculator, how to use it effectively, and strategies for securing the best auto loan possible. Get ready to drive away with confidence, armed with knowledge and a clear financial plan.

Unlock Your Dream Car: A Deep Dive into the NFCU Car Loan Calculator and Smart Auto Financing

Why the NFCU Car Loan Calculator is Your Best Friend on the Road to Ownership

Purchasing a vehicle is one of the most significant financial decisions many individuals make, second only to buying a home. The monthly payment, interest rates, and loan terms can all dramatically impact your long-term financial health. This is precisely why a robust tool like a car loan calculator is not just helpful, but crucial.

The NFCU Car Loan Calculator stands out as a powerful resource for several reasons. It provides immediate estimates of your potential monthly car payments, allowing you to quickly understand affordability. This initial insight empowers you to set realistic expectations for your car search.

Based on my experience, many buyers jump into car shopping without a clear financial picture. They fall in love with a vehicle only to discover its payments are outside their comfort zone. Using the NFCU calculator proactively helps you avoid this common pitfall. It shifts the focus from "What car do I want?" to "What car can I comfortably afford?"

Moreover, the calculator serves as an excellent planning tool. It allows you to experiment with different scenarios, such as varying down payments or loan terms. This flexibility helps you sculpt a loan structure that aligns perfectly with your personal budget and financial goals, ensuring a smoother and more confident car buying journey.

Deconstructing the NFCU Car Loan Calculator: Inputs and Outputs Explained

To effectively use the NFCU Car Loan Calculator, you need to understand the key pieces of information it requires and what the results mean. Each input plays a critical role in determining your estimated monthly payment and the total cost of your loan. Let’s break down these components.

Essential Inputs for Accurate Estimates

-

Vehicle Price / Loan Amount:

- This is the total purchase price of the car you’re considering. For a new car, this is often the sticker price (MSRP) or a negotiated price. For a used car, it’s the agreed-upon selling price.

- If you already know how much you want to borrow, you can enter that specific loan amount. Remember, the loan amount is typically the vehicle price minus any down payment and trade-in value.

-

Down Payment:

- A down payment is the amount of cash you pay upfront for the vehicle. It directly reduces the amount you need to borrow.

- A larger down payment generally means a smaller loan, lower monthly payments, and less interest paid over the life of the loan. Pro tips from us: Aim for at least 10-20% of the vehicle’s price if possible.

-

Trade-in Value:

- If you plan to trade in your current vehicle, its value can be applied towards the purchase of your new car. This acts similarly to a down payment, reducing the amount you need to finance.

- Be realistic with your trade-in estimate. Use online valuation tools like Kelley Blue Book or Edmunds to get a fair market value before visiting a dealership.

-

Interest Rate (APR):

- The Annual Percentage Rate (APR) is the cost of borrowing money, expressed as a yearly percentage. This is arguably the most impactful factor on your total loan cost.

- NFCU offers competitive rates to its members, often based on creditworthiness. While using the calculator, you might start with an estimated rate (e.g., current NFCU advertised rates for excellent credit) and then adjust it as you get closer to pre-approval.

-

Loan Term (Months):

- This is the duration over which you will repay the loan, typically expressed in months (e.g., 36, 48, 60, 72, or even 84 months).

- A longer loan term results in lower monthly payments but means you’ll pay more interest over the life of the loan. Conversely, a shorter term has higher monthly payments but saves you money on interest.

Understanding the Calculator’s Outputs

Once you’ve entered your inputs, the NFCU Car Loan Calculator will quickly generate key financial insights:

- Estimated Monthly Payment: This is the most immediate and often the most-watched output. It tells you how much you can expect to pay each month towards your loan. This helps you gauge if the payment fits comfortably within your budget.

- Total Interest Paid: This figure reveals the total amount of interest you will pay over the entire loan term. It’s a critical number for understanding the true cost of borrowing. This output clearly illustrates the financial impact of different interest rates and loan terms.

- Total Cost of Loan: This is the sum of the loan amount plus the total interest paid. It represents the overall expense of financing your vehicle. Don’t just focus on the monthly payment; this total cost gives you the complete financial picture.

By understanding these inputs and outputs, you can manipulate the variables to find a payment structure that aligns with your financial goals. It’s an iterative process that empowers you with knowledge.

Beyond the Calculator: Key Factors Influencing Your NFCU Car Loan

While the NFCU Car Loan Calculator provides excellent estimates, several underlying factors will determine the actual terms of your approved loan. Understanding these elements is crucial for securing the most favorable financing.

The Power of Your Credit Score

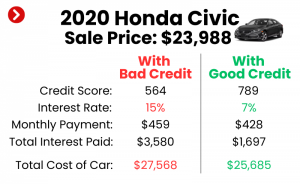

Your credit score is arguably the most significant factor influencing the interest rate you’ll be offered. Lenders, including NFCU, use this three-digit number to assess your creditworthiness and the likelihood of you repaying the loan. A higher credit score signals a lower risk to the lender.

Individuals with excellent credit scores (typically 720+) often qualify for the lowest advertised interest rates. Conversely, a lower credit score might result in a higher APR, increasing your monthly payments and the total cost of the loan. Pro tips from us: Check your credit score and report well in advance of applying. Dispute any errors promptly.

Your Debt-to-Income Ratio (DTI)

Lenders also look at your debt-to-income ratio (DTI). This is a percentage that compares your total monthly debt payments to your gross monthly income. A low DTI indicates that you have a good handle on your existing debts and are less likely to struggle with new payments.

NFCU, like other lenders, wants to ensure you can comfortably afford the new car payment. A high DTI might signal that you are already overextended, potentially leading to less favorable loan terms or even denial. Based on my experience, keeping your DTI below 36% for new credit is often advisable.

The Impact of Loan Term

The loan term, or how long you take to repay the loan, significantly affects both your monthly payment and the total interest paid. Longer terms (e.g., 72 or 84 months) result in lower monthly payments, which can seem attractive. However, this convenience comes at a cost.

With a longer term, you’ll pay more in total interest because the money is borrowed for a longer period. Furthermore, you risk owing more on the car than it’s worth (being "upside down") as depreciation often outpaces equity building in extended loan terms. Shorter terms (e.g., 36 or 48 months) mean higher monthly payments but substantially reduce the total interest paid and build equity faster.

The Advantage of a Strong Down Payment

A larger down payment is one of the best strategies to improve your loan terms. It directly reduces the amount you need to borrow, which in turn lowers your monthly payments and the total interest paid. It also shows the lender you are serious about your commitment and have financial discipline.

Common mistakes to avoid are underestimating the power of a solid down payment. Even a few extra hundred dollars can make a noticeable difference. It also provides an immediate buffer against depreciation, reducing the risk of being upside down on your loan.

Vehicle Type and Age

The type and age of the vehicle can also influence loan terms. New cars generally qualify for lower interest rates compared to used cars, as they are considered less of a risk. Lenders view newer vehicles as more reliable and less likely to require expensive repairs that could impact your ability to pay.

For used cars, older models or those with high mileage might have higher interest rates or shorter maximum loan terms. This is because their resale value depreciates faster, and they present a higher risk of mechanical issues. NFCU considers these factors when structuring your loan.

The Benefits of NFCU Membership

Being a Navy Federal Credit Union member comes with distinct advantages for auto loans. Credit unions are member-owned, often allowing them to offer more competitive interest rates and personalized service compared to traditional banks. Membership eligibility typically includes active duty military, veterans, Department of Defense civilians, and their families.

NFCU’s commitment to its members means you’re likely to find favorable terms, excellent customer service, and a variety of resources designed to help you make informed financial decisions. Their loan officers understand the unique needs of military families, adding another layer of trust and support.

Strategic Ways to Use the NFCU Car Loan Calculator for Smarter Decisions

The NFCU Car Loan Calculator isn’t just for getting a single estimate; it’s a dynamic tool for strategic planning. Leveraging its capabilities effectively can lead to significant savings and greater peace of mind.

Scenario Planning for Optimal Budgeting

One of the most powerful uses of the calculator is scenario planning. Don’t just input one set of numbers and stop. Instead, run multiple scenarios to see how different variables impact your payments and total cost.

- Vary Down Payment: What if you save an extra $1,000 for a down payment? How much does that reduce your monthly payment or total interest?

- Adjust Loan Term: Compare a 60-month loan to a 72-month loan. Is the lower monthly payment of the longer term worth the extra interest paid?

- Estimate Interest Rates: If your credit score improves, how much could you save with a slightly lower APR?

By exploring these "what if" scenarios, you gain a comprehensive understanding of your financial options. This helps you make an informed decision that balances affordability with the overall cost of the loan.

The Power of Pre-Approval

Using the calculator before seeking pre-approval from NFCU is a game-changer. Pre-approval means NFCU has reviewed your credit and financial situation and has conditionally approved you for a specific loan amount at a certain interest rate.

Knowing your pre-approved loan amount and estimated interest rate allows you to use the calculator with highly accurate figures. This provides a very realistic monthly payment estimate. You walk into the dealership not wondering what you can afford, but knowing precisely what your financing looks like.

Negotiation Leverage at the Dealership

Armed with your pre-approval and a clear understanding of your budget from the NFCU Car Loan Calculator, you gain significant negotiation leverage. Dealers often try to focus on the monthly payment, but you’ll be prepared to discuss the total vehicle price and the loan terms separately.

You can confidently say, "My pre-approval from Navy Federal is for X amount at Y interest rate." This removes the mystery of financing from the sales process. It allows you to negotiate the car’s price as a separate transaction, often leading to a better deal overall.

Evaluating Refinancing Options

The utility of the NFCU Car Loan Calculator extends beyond the initial purchase. If you already have a car loan with another lender, or if your credit score has significantly improved since your initial purchase, you might consider refinancing.

You can use the calculator to compare your current loan’s remaining balance, interest rate, and term against potential new terms from NFCU. Input the new potential interest rate and term to see how much you could save on your monthly payment or total interest. This helps you determine if refinancing is a financially sound move.

Common Mistakes to Avoid When Using Any Car Loan Calculator (and NFCU’s)

Even with a powerful tool like the NFCU Car Loan Calculator, it’s possible to make errors that lead to inaccurate estimates or poor financial decisions. Being aware of these common pitfalls can help you avoid them.

Focusing Solely on the Monthly Payment

This is perhaps the biggest mistake car buyers make. A lower monthly payment can seem appealing, but it often comes at the cost of a longer loan term and significantly more interest paid over time.

Based on my years of observing car buyers, one of the biggest pitfalls is payment shopping. While the monthly payment is important for your budget, always look at the total interest paid and the total cost of the loan. A slight increase in your monthly payment for a shorter term can save you thousands in the long run.

Ignoring Additional Costs of Ownership

The calculator estimates your loan payment, but a car comes with many other expenses that are often overlooked. These include:

- Car Insurance: Premiums vary widely based on the vehicle, your driving record, and location.

- Fuel Costs: Consider your commute and the car’s fuel efficiency.

- Maintenance and Repairs: All cars need servicing, and older vehicles might require more extensive repairs.

- Registration and Licensing Fees: Annual costs that vary by state.

Failing to factor these into your overall car budget can lead to financial strain, even if your loan payment is affordable. Pro tips from us: Create a separate "car ownership budget" that includes these items.

Not Factoring in Current Interest Rates

While the calculator allows you to input an estimated interest rate, using an outdated or generic rate can skew your results. Interest rates fluctuate based on market conditions, the economy, and your personal credit profile.

Always try to use the most current rates available from NFCU, especially if you have an idea of your credit tier. Getting a pre-approval will give you the most accurate rate to input into the calculator for a realistic estimate.

Overestimating Trade-in Value or Underestimating a Down Payment

It’s natural to want to get the most for your trade-in or believe you can save more for a down payment. However, being overly optimistic in these areas will lead to an estimated monthly payment that is lower than reality.

Use reputable online valuation tools for your trade-in, and be conservative with your down payment estimates if you’re still saving. It’s always better to be pleasantly surprised by a lower actual payment than to be shocked by a higher one.

Forgetting About Pre-Approval

Some buyers use the calculator, get an estimate, and then head straight to the dealership without getting pre-approved. While the calculator is a fantastic planning tool, pre-approval provides concrete loan terms based on your actual financial situation.

Pre-approval from NFCU gives you a firm offer and empowers you with real numbers. This allows you to confirm your calculator’s estimates and enter negotiations with the dealer as a cash buyer, knowing your financing is already secured.

Making the Most of Your NFCU Auto Loan Experience

Beyond using the calculator, leveraging the full range of NFCU’s services can significantly enhance your car buying journey. They are committed to providing value to their members.

The NFCU Pre-Approval Process: Your Head Start

Applying for pre-approval with NFCU is a straightforward process that offers immense benefits. It involves a credit check and an assessment of your financial health, after which they’ll provide you with a specific loan amount and interest rate you qualify for.

This process gives you significant buying power. It means you can shop for a car knowing exactly how much you can spend and what your financing terms will be. This removes much of the stress from the dealership experience.

Leveraging NFCU Resources and Expertise

NFCU offers more than just a calculator; they provide a wealth of financial education and resources. Their website often features articles, guides, and tools to help members make informed decisions about auto loans, budgeting, and overall financial wellness.

Don’t hesitate to reach out to their loan specialists if you have questions. They are there to guide you through the process and help you understand your options. Their expertise can be invaluable, especially for first-time car buyers.

Embracing Your Membership Benefits

As a Navy Federal Credit Union member, you’re part of an organization dedicated to serving its community. This often translates into highly competitive interest rates, flexible loan terms, and a member-first approach to customer service. These benefits are designed to save you money and provide a superior banking experience.

For a deeper dive into improving your credit score before applying for a loan, check out our comprehensive guide on Building a Strong Credit Score for Auto Loans. Understanding how your credit works is fundamental to securing the best rates.

Considering the long-term financial implications of car ownership? Read our article on Understanding the Total Cost of Car Ownership Beyond the Monthly Payment to ensure you’re fully prepared for all expenses.

For the most current rates, specific membership details, and to access the actual calculator, always refer to the official Navy Federal Credit Union website. Their site provides the definitive information you need to make your decisions: Navy Federal Credit Union Official Website.

Drive Away with Confidence: Your NFCU Car Loan Journey

Purchasing a car is a significant milestone, and with the right tools and knowledge, it can be a truly rewarding experience. The NFCU Car Loan Calculator is far more than just a simple online form; it’s a powerful financial planning instrument. It empowers you to explore scenarios, understand the true cost of borrowing, and ultimately, make an informed decision that aligns with your financial well-being.

By proactively using this calculator, understanding the factors that influence your loan, and avoiding common mistakes, you’re not just buying a car; you’re investing wisely in your financial future. Navy Federal Credit Union stands as a trusted partner in this journey, offering competitive rates and dedicated support to its members.

So, take control of your car buying process. Start by playing with the NFCU Car Loan Calculator today. Experiment with different inputs, understand the outputs, and build a financial plan that puts you in the driver’s seat of your dream car with complete confidence. Happy driving!