Unlock Your Dream Car: The Ultimate Guide to Car Loan Preapproval (1500+ Words)

Unlock Your Dream Car: The Ultimate Guide to Car Loan Preapproval (1500+ Words) Carloan.Guidemechanic.com

Buying a new or used car is an exciting milestone, but the financing process can often feel like navigating a complex maze. Many car shoppers walk onto a dealership lot without a clear financial plan, leaving themselves vulnerable to higher interest rates and less favorable terms. This is where the power of car loan preapproval comes into play, transforming your car-buying journey from stressful to strategic.

Imagine stepping onto a car lot with your financing already secured, knowing exactly how much you can spend and what your monthly payments will look like. That’s the confidence preapproval offers. In this comprehensive guide, we’ll demystify auto loan preapproval, explain its immense benefits, walk you through the process, and equip you with the knowledge to secure the best possible deal. Our goal is to make you an informed, empowered car buyer.

Unlock Your Dream Car: The Ultimate Guide to Car Loan Preapproval (1500+ Words)

What Exactly Is Car Loan Preapproval? A Foundational Understanding

At its core, car loan preapproval is a conditional offer from a lender to lend you a specific amount of money at a particular interest rate for a car purchase. This offer is made before you’ve even chosen the vehicle itself. It’s essentially a preliminary green light from a financial institution, signaling that you meet their criteria for a loan.

Think of it as having a shopping budget and a guaranteed payment method in your pocket before you even enter the store. The lender assesses your financial health – including your credit score, income, and debt-to-income ratio – and determines the maximum loan amount they’re willing to offer you, along with the estimated interest rate and loan term. This isn’t a commitment to buy a specific car, but rather an approval for a certain financing package.

It’s crucial to distinguish preapproval from pre-qualification. Pre-qualification is a softer inquiry, often just a quick check of your basic financial information, providing an estimate without a deep dive into your credit. Preapproval, however, involves a more thorough review, including a hard credit inquiry, and results in a concrete offer that’s valid for a set period, typically 30 to 60 days. This distinction is vital for understanding the weight and reliability of the offer you receive.

Why Bother? The Unbeatable Advantages of Getting Preapproved for a Car Loan

Based on my experience, neglecting car loan preapproval is one of the most common mistakes car buyers make. The benefits extend far beyond just securing financing; they fundamentally shift the power dynamics in your favor at the dealership. Let’s delve into why this step is absolutely essential.

1. Crystal-Clear Budget Clarity

The most immediate advantage of get preapproved for a car loan is gaining a precise understanding of your budget. You’ll know exactly how much a lender is willing to lend you, which directly translates into the maximum price range for your potential car. This clarity prevents you from falling in love with a car you can’t realistically afford, saving you from potential disappointment and financial strain.

This firm budget allows you to focus your car search on vehicles that are truly within reach. You can filter out cars that exceed your preapproved limit, making your shopping more efficient and less overwhelming. It’s about making an informed decision, not an emotional one, when it comes to such a significant purchase.

2. Enhanced Negotiating Power

Walking into a dealership with a preapproved auto loan transforms you into a cash buyer in the eyes of the salesperson. You’re not relying on their in-house financing, which means they can’t use the financing terms as leverage against you. Your focus shifts entirely to the vehicle’s price, giving you significant leverage to negotiate.

Salespeople often try to "pack" additional products or higher interest rates into the deal when you’re financing through them. With preapproval, you can confidently say, "I already have my financing," and concentrate solely on getting the best price for the car itself. This separates the car price negotiation from the financing negotiation, simplifying the process and usually leading to a better overall deal.

3. Stress Reduction and Peace of Mind

Car buying can be notoriously stressful, filled with uncertainty and high-pressure sales tactics. Car financing preapproval eliminates a huge chunk of this anxiety. You’ve already handled the most challenging part – securing the money – before you even set foot on the lot.

Knowing your financial standing upfront allows you to enjoy the car-shopping experience. You can focus on features, test drives, and comparing models, rather than worrying if you’ll qualify or what interest rate you’ll be offered. This peace of mind is invaluable, making the entire process much more pleasant.

4. Time Savings at the Dealership

Dealership financing can be a lengthy process, often involving multiple trips to the finance manager’s office while they "shop" your credit to various lenders. This can add hours, sometimes even days, to your car purchase. With car loan preapproval, you significantly streamline this part of the process.

You arrive with your financing in hand, ready to complete the paperwork for the car purchase itself. This expedites the entire transaction, allowing you to drive away in your new vehicle much faster. Pro tips from us: Time is money, and preapproval saves you both.

5. Avoiding Dealership Financing Traps

Dealerships often mark up interest rates on loans they arrange, earning a commission on top of what the lender charges. This is a common practice known as "dealer reserve." When you get preapproved for a car loan elsewhere, you have a benchmark. You can compare the dealership’s offer against your preapproval and opt for the better deal.

This comparison is crucial. Sometimes, a dealership might genuinely beat your preapproval rate, especially if they have special manufacturer incentives. However, having your own preapproval empowers you to identify and avoid less favorable terms, ensuring you don’t overpay for your financing.

6. Potentially Better Interest Rates and Terms

Independent lenders (banks, credit unions, online lenders) often offer more competitive interest rates and flexible terms than what you might initially find at a dealership. They are directly competing for your business, which can drive rates down.

By shopping around for preapproval, you ensure you’re getting the best possible financing package available to you, given your credit profile. This could translate into hundreds, or even thousands, of dollars saved over the life of the loan.

The Journey to Preapproval: How Does It Work?

Understanding the process of how to get car loan preapproval is key to a smooth experience. It’s generally straightforward, but involves a few distinct steps.

Step 1: Gather Your Financial Information

Before you even apply, you’ll need to compile essential documents and details. Lenders want a clear picture of your financial stability. This typically includes personal identification, proof of income, employment history, and housing information. Having these ready will significantly speed up your application.

Step 2: Choose Your Lenders and Apply

Don’t just apply to one place! Based on my experience, shopping around is critical. You can apply to traditional banks, credit unions, and various online lenders. Each will have slightly different criteria and offers. Most applications can be completed online, often taking just a few minutes.

When you apply, lenders will perform a "hard inquiry" on your credit report. While multiple hard inquiries for the same type of loan within a short period (typically 14-45 days, depending on the credit scoring model) are usually grouped as a single inquiry to minimize impact, it’s still wise to apply only to lenders you are seriously considering.

Step 3: Review Your Preapproval Offers

Once your applications are processed, you’ll start receiving preapproval offers. These will clearly state the maximum loan amount, the interest rate, and the loan term (e.g., 60 or 72 months). Pay close attention to these details. Compare the annual percentage rate (APR), which includes fees, not just the interest rate.

Some offers might also include specific conditions, such as requiring a certain down payment. Read all the fine print carefully. This is your opportunity to pick the offer that best suits your financial situation and car-buying goals.

Step 4: Understand the Validity Period

Preapproval offers are not indefinite. They typically come with an expiration date, often 30 to 60 days from the date of approval. This gives you a window to find your car and finalize the loan. Be mindful of this timeframe; if it expires, you might need to reapply.

It’s important to start your car search soon after getting preapproved to make the most of your offer. The market, interest rates, and your credit profile can change, so acting within the validity period is advisable.

What You’ll Need: Documents and Information for Your Auto Loan Preapproval

To streamline your auto loan preapproval process, it’s best to have the following information and documents readily available. Lenders use these to assess your creditworthiness and ability to repay the loan.

- Personal Identification: Driver’s license, Social Security number, and contact information (phone, email, address).

- Income Verification: Recent pay stubs (typically 2-3 months), W-2 forms, tax returns (especially if self-employed), or bank statements showing direct deposits.

- Employment History: Details of your current employer, including contact information and how long you’ve been employed. Lenders prefer stable employment.

- Housing Information: Your current address, how long you’ve lived there, and whether you rent or own. If renting, your monthly rent payment. If owning, your mortgage payment.

- Debt Information: Details about existing debts, such as credit card balances, student loans, and other car loans. This helps lenders calculate your debt-to-income (DTI) ratio.

- Down Payment Details: If you plan to make a down payment, some lenders may ask for proof of funds.

- Vehicle Information (Optional but helpful): While not strictly required for preapproval, having a general idea of the type of car you want (e.g., SUV, sedan, new, used) can help lenders provide more accurate estimates, as loan terms can vary by vehicle.

Where to Get Preapproved: Exploring Your Options

One of the pro tips from us is to always shop around for your car loan preapproval. Different lenders cater to different types of borrowers and offer varying rates. Here are the primary sources you should consider:

1. Traditional Banks

Your existing bank is often a good starting point. They already have your financial history, which can sometimes lead to a smoother application process or preferential rates due to your established relationship. Major national banks and smaller regional banks all offer auto loans.

However, don’t assume your bank automatically offers the best deal. Always compare their offer with others.

2. Credit Unions

Credit unions are member-owned financial cooperatives known for often offering more competitive interest rates and personalized service compared to larger banks. Their non-profit status allows them to pass savings onto their members. If you’re eligible to join one (often based on residency, employer, or association), they are definitely worth considering for preapproval for car loan.

Their application processes are typically straightforward, and they often have a strong community focus.

3. Online Lenders

The digital age has brought forth a multitude of online lenders specializing in auto loans. Companies like Capital One Auto Finance, LightStream, and others offer convenient, often fast, online application processes. They can be excellent sources for competitive rates and a streamlined experience, especially for tech-savvy borrowers.

Common mistakes to avoid are: not checking their legitimacy. Always verify that an online lender is reputable and well-reviewed before sharing your personal financial information.

4. Manufacturer Financing (Dealerships)

While the primary goal of preapproval is to secure independent financing, it’s worth noting that car manufacturers often offer attractive financing incentives (like 0% APR for qualified buyers) through their captive finance companies (e.g., Toyota Financial Services, Ford Credit). These are typically offered at the dealership.

Having your preapproval in hand allows you to compare these special dealership offers against your independent preapproval. If the dealership can beat your rate, great! If not, you have a solid backup.

Key Factors Influencing Your Car Loan Preapproval

Lenders assess several critical factors when determining your eligibility and the terms of your preapproved auto loan. Understanding these can help you improve your chances of securing a favorable offer.

1. Credit Score

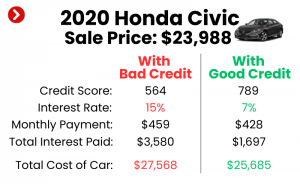

Your credit score is arguably the most significant factor. It’s a numerical representation of your creditworthiness, reflecting your history of managing debt. A higher credit score (generally 700+) indicates a lower risk to lenders and typically qualifies you for the best interest rates. Lower scores will result in higher rates or potentially a denial.

Lenders look at your payment history, amounts owed, length of credit history, new credit, and credit mix. A strong credit score demonstrates responsible financial behavior, which is highly valued.

2. Debt-to-Income (DTI) Ratio

Your DTI ratio compares your total monthly debt payments to your gross monthly income. Lenders use this to gauge your ability to take on additional debt. A lower DTI ratio (ideally below 36-43%) suggests you have sufficient disposable income to handle new car payments without strain.

If your DTI is high, lenders might view you as a higher risk, even with a good credit score. This is because a large portion of your income is already committed to other obligations.

3. Income Stability and Employment History

Lenders want assurance that you have a stable and reliable source of income to make your monthly payments. A steady job history, preferably with the same employer for several years, signals financial stability. Freelancers or those with inconsistent income may face more scrutiny and might need to provide more extensive documentation.

Proof of consistent income, such as pay stubs or tax returns, is essential to demonstrate your ability to meet financial commitments.

4. Down Payment Amount

While not always mandatory, making a substantial down payment can significantly improve your chances of car loan preapproval and secure a better interest rate. A larger down payment reduces the amount you need to borrow, thereby lowering the lender’s risk.

It also means you’ll have smaller monthly payments and pay less interest over the life of the loan. Pro tips from us: Aim for at least 10-20% of the car’s price if possible.

5. Loan Term

The loan term refers to the length of time you have to repay the loan (e.g., 36, 60, or 72 months). Shorter loan terms typically come with lower interest rates but higher monthly payments. Longer terms mean lower monthly payments but often higher overall interest paid. Lenders will assess your ability to manage the payments over the chosen term.

Common mistakes to avoid are: extending the loan term too much to reduce monthly payments, as this often leads to paying significantly more in interest over time.

Pro Tips for a Smooth and Successful Car Loan Preapproval

To maximize your chances of getting the best possible car financing preapproval, follow these expert recommendations:

- Check Your Credit Report: Before applying anywhere, obtain a free copy of your credit report from AnnualCreditReport.com. Review it for any errors and dispute them immediately. A clean report can significantly boost your score.

- Improve Your Credit Score: If your score isn’t ideal, take steps to improve it. Pay down existing debts, make all payments on time, and avoid opening new lines of credit just before applying for a car loan. Even a small increase can make a difference in your interest rate.

- Save for a Down Payment: As discussed, a larger down payment reduces your loan amount and risk for the lender, often leading to better terms.

- Shop Around Aggressively: Don’t settle for the first offer. Apply to multiple banks, credit unions, and online lenders within a concentrated period (e.g., 14-45 days) to minimize the impact on your credit score.

- Understand the Terms: Fully comprehend the interest rate (APR), loan term, and any fees associated with the preapproval offer. Don’t be afraid to ask questions.

- Based on my experience… a well-prepared borrower with multiple preapproval offers is in the strongest position to negotiate not only the car price but also the final financing terms.

After You’re Preapproved: What’s Next?

Congratulations, you’ve secured your car loan preapproval! Now, it’s time to leverage this powerful tool.

1. Stick to Your Budget

Your preapproval sets your maximum spending limit. It’s tempting to look at cars slightly above that, but resist the urge. Staying within your preapproved budget ensures your car payments remain affordable and prevents financial strain down the road. Remember, there are also insurance, maintenance, and fuel costs to consider.

2. Visit Dealerships with Confidence

Walk onto the lot knowing your financial boundaries. Inform the salesperson early in the process that you already have your financing secured. This immediately positions you as a serious buyer focused on the car’s price, not on struggling with financing.

3. Compare All Offers

While you have your preapproval, the dealership might still present their own financing options, sometimes touting special manufacturer rates. Always compare their offer directly against your preapproval. Look at the total interest paid, not just the monthly payment. Go with whichever offer provides the best overall value for you.

For more insights on securing the best deal, you might find our article on "" helpful.

Common Myths and Misconceptions About Car Loan Preapproval

There are several misunderstandings surrounding auto loan preapproval that can deter people from taking this beneficial step. Let’s debunk them:

- Myth 1: It significantly hurts your credit score. While a hard inquiry does temporarily lower your score by a few points, multiple inquiries for the same type of loan within a short window (typically 14-45 days) are often treated as a single inquiry by credit scoring models. The long-term benefits of securing a lower interest rate far outweigh this minor, temporary dip.

- Myth 2: You’re locked into the first preapproval offer. Absolutely not. Preapproval is a non-binding offer. You can apply to multiple lenders and choose the best one. You can even choose not to use your preapproval if a dealership offers a better deal.

- Myth 3: Preapproval guarantees a loan for any car. Preapproval is for a specific amount and often has conditions. If the car you choose is significantly more expensive than your preapproved amount, or if it’s an older model that doesn’t meet the lender’s criteria for used car loans, you might need to adjust your plans.

- Myth 4: It’s the same as pre-qualification. As discussed earlier, pre-qualification is a preliminary estimate, while preapproval is a more solid, conditional offer based on a detailed credit check.

Final Thoughts: Drive Away with Confidence

The journey to owning a new car should be exciting, not intimidating. By taking the proactive step of securing preapproval for a car loan, you equip yourself with invaluable financial clarity, negotiating power, and peace of mind. It’s a simple yet incredibly effective strategy that empowers you to make smarter financial decisions and ultimately drive away with a better deal.

Don’t let the financing process control you; take control of it. Invest a little time upfront to get preapproved for a car loan, and you’ll find the entire car-buying experience transformed. This intelligent approach will save you money, reduce stress, and ensure you’re making a confident, informed purchase.

Frequently Asked Questions (FAQs) About Car Loan Preapproval

Q1: How long does car loan preapproval last?

A1: Most car loan preapproval offers are valid for a specific period, typically 30 to 60 days. This gives you ample time to find your desired vehicle and finalize the purchase. Be sure to check the expiration date on your specific offer.

Q2: Does preapproval guarantee I will get a car loan?

A2: Car loan preapproval is a conditional offer. While it means you’ve met the lender’s initial criteria, the final loan is still contingent on a few factors. These include the vehicle meeting the lender’s requirements (e.g., age, mileage), the final purchase price aligning with your approved amount, and no significant changes occurring in your financial situation between preapproval and closing.

Q3: Can I get preapproved for a car loan with bad credit?

A3: It is possible to get preapproved for a car loan with less-than-perfect credit, but the terms might be less favorable. You might face higher interest rates, require a larger down payment, or need a co-signer. Some lenders specialize in bad credit auto loans. It’s still highly recommended to get preapproved to understand your options and avoid high-pressure sales at dealerships.

Q4: What’s the difference between pre-qualification and pre-approval?

A4: Pre-qualification is a preliminary assessment, often based on basic financial information, and usually involves a "soft" credit inquiry that doesn’t affect your score. It gives you an estimate. Pre-approval, on the other hand, involves a more thorough review, including a "hard" credit inquiry, and results in a conditional offer with specific terms (amount, rate) that is typically valid for a set period. Pre-approval carries more weight and is a firmer offer.

Q5: Should I get preapproved before I even start looking at cars?

A5: Yes, absolutely! Getting car financing preapproval before you start car shopping is the ideal approach. It provides you with a clear budget, empowers you with negotiating leverage, and saves you time and stress at the dealership. It transforms you into a cash buyer, focusing negotiations solely on the car’s price. For more on planning your car purchase, check out this external resource from the Consumer Financial Protection Bureau: https://www.consumerfinance.gov/consumer-tools/auto-loans/