Unlock Your Dream Car: The Ultimate Guide to Using a Free Online Car Loan Calculator

Unlock Your Dream Car: The Ultimate Guide to Using a Free Online Car Loan Calculator Carloan.Guidemechanic.com

Buying a new or used car is an exciting milestone, often representing freedom, convenience, or a significant life upgrade. However, the thrill can quickly turn to stress when confronted with the complex world of car financing. From interest rates and loan terms to down payments and trade-in values, there are numerous variables that impact your monthly budget.

This is where a free online car loan calculator becomes your indispensable financial co-pilot. It’s more than just a tool; it’s a powerful ally that brings clarity and confidence to your car buying journey. As an expert blogger and professional SEO content writer, I’ve seen firsthand how understanding your financing options before you step into a dealership can save you thousands of dollars and countless headaches.

Unlock Your Dream Car: The Ultimate Guide to Using a Free Online Car Loan Calculator

In this super comprehensive guide, we’ll dive deep into everything you need to know about these calculators. We’ll explore their inner workings, uncover their hidden benefits, highlight advanced tips, and help you avoid common pitfalls. Our ultimate goal is to equip you with the knowledge to make informed decisions, ensuring your dream car doesn’t turn into a financial burden. Get ready to empower your car buying experience!

What is a Free Online Car Loan Calculator and Why Do You Absolutely Need One?

At its core, a free online car loan calculator is a digital tool designed to help prospective car buyers estimate their potential monthly car payments. It takes several key financial inputs and, using a sophisticated algorithm, quickly determines what your recurring obligation will be. Think of it as your personal financial crystal ball for auto loans.

The beauty of these calculators lies in their accessibility and simplicity. You don’t need to be a math whiz or a financial guru to use one. Most are intuitively designed with user-friendly interfaces, making complex calculations digestible for everyone. This accessibility is crucial for anyone navigating the often-opaque world of car financing.

Based on my experience, many car buyers make the mistake of focusing solely on the sticker price of a vehicle. They walk into a dealership, fall in love with a car, and then try to make the numbers work on the fly. This reactive approach often leads to rushed decisions, higher interest rates, and ultimately, buyer’s remorse. A car loan calculator flips this script, empowering you to be proactive.

By using a calculator early in your process, you shift from reacting to loan offers to predicting and planning for them. You gain a clear understanding of what you can realistically afford, not just what a lender might approve you for. This foresight is invaluable, transforming a potentially stressful negotiation into a confident, informed discussion.

Deconstructing the Calculator: Key Inputs You’ll Encounter

To get accurate estimates from any free online car loan calculator, you need to understand the fundamental pieces of information it requires. Each input plays a significant role in shaping your final monthly payment. Let’s break them down.

1. Vehicle Purchase Price / Loan Amount

This is arguably the most straightforward input: the selling price of the car you’re considering. However, it’s crucial to differentiate between the purchase price and the loan amount. The loan amount is the portion of the purchase price that you actually need to borrow after factoring in your down payment and any trade-in value.

If you’re just starting out, you might enter the sticker price. As you get closer to a deal, you’ll use the negotiated price. Always aim for the final agreed-upon price before taxes and fees for the most accurate calculation.

2. Down Payment

Your down payment is the initial amount of cash you pay upfront towards the car’s purchase. This reduces the total amount you need to finance. A larger down payment translates directly into a smaller loan amount, which in turn means lower monthly payments and less interest paid over the life of the loan.

Pro tips from us: While 10-20% is often recommended for new cars, any amount you can comfortably put down will help. Even a small down payment can make a noticeable difference in your overall financial burden and demonstrate your commitment to lenders.

3. Trade-In Value

If you’re trading in your current vehicle, its value acts similarly to a down payment. The agreed-upon trade-in amount will be deducted from the car’s purchase price, further reducing the loan amount you need to secure. It’s essentially another form of upfront payment.

It’s wise to get an independent appraisal of your trade-in value before visiting a dealership. This ensures you have a benchmark and aren’t undersold on your current vehicle, maximizing its contribution to your new car purchase.

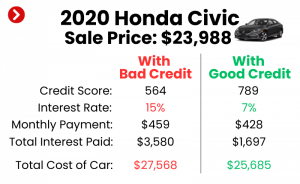

4. Interest Rate (APR – Annual Percentage Rate)

The interest rate, often expressed as an Annual Percentage Rate (APR), is the cost of borrowing money. It’s the percentage charged by the lender on the unpaid balance of your loan. A lower APR means you pay less in interest over time, significantly impacting the total cost of your car.

Your credit score is the primary determinant of the interest rate you’ll be offered. Individuals with excellent credit typically qualify for the lowest rates. If you don’t know your approximate APR, many calculators offer a range to choose from, or you can use an average rate for your credit tier as a starting point.

5. Loan Term (Months)

The loan term refers to the length of time you have to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72, or even 84 months). A longer loan term generally results in lower monthly payments, as you’re spreading the repayment over more installments.

However, a longer term also means you’ll pay more in total interest over the life of the loan. Conversely, a shorter term will have higher monthly payments but will save you money on interest and get you debt-free faster. Balancing these factors is a key decision point in your financing.

6. Sales Tax & Other Fees

Don’t forget sales tax, registration fees, title fees, and documentation fees. These can add a significant amount to the total cost of your vehicle and are often financed along with the car itself. While some basic calculators might not include these, more advanced ones will have fields for them.

Ignoring these additional costs is a common oversight that can lead to an inaccurate understanding of your true monthly payment. Always try to factor them in for a comprehensive financial picture.

How Does a Car Loan Calculator Actually Work? (The Math Made Simple)

The magic behind a free online car loan calculator lies in its ability to quickly perform an amortization calculation. Amortization is the process of paying off a debt over time through regular, equal payments. Each payment consists of both principal (the amount you borrowed) and interest.

In the early stages of a loan, a larger portion of your payment goes towards interest. As the loan matures, more of each payment is allocated to reducing the principal balance. The calculator uses a standard loan amortization formula to figure this out instantly.

What the calculator shows you is incredibly valuable. Primarily, it will display your estimated monthly payment. This is the single most important number for most buyers, as it directly impacts their monthly budget. Beyond that, many calculators also provide:

- Total Interest Paid: This figure reveals the actual cost of borrowing the money over the entire loan term. It helps you see how much extra you’re paying beyond the car’s price.

- Total Cost of the Car: This is the sum of the principal amount borrowed plus the total interest paid. It gives you the true, all-in cost of your vehicle over the loan’s lifetime.

- Amortization Schedule: Some advanced calculators will even generate a detailed schedule showing how much principal and interest you pay with each installment throughout the loan term. This transparency is incredibly empowering.

The real power of these calculators comes from their ability to run "what if" scenarios. You can instantly change the down payment, the interest rate, or the loan term and see how your monthly payment and total cost change. This iterative process allows you to fine-tune your financial plan before you even speak to a lender.

The Myriad Benefits of Using a Free Online Car Loan Calculator

Embracing a free online car loan calculator in your car buying process offers a wealth of advantages that extend far beyond simply knowing your monthly payment. These benefits contribute significantly to a smoother, more confident, and ultimately, more affordable purchase.

1. Budgeting Precision

Perhaps the most immediate benefit is the ability to budget with unparalleled precision. Before you even start test-driving, you can determine what monthly payment truly fits your financial capacity without straining your other obligations. This proactive budgeting prevents you from falling in love with a car you can’t realistically afford.

Knowing your payment limits empowers you to shop smarter, focusing only on vehicles within your pre-determined price range. This saves time and emotional energy, streamlining your entire search process.

2. Comparing Loan Offers Effectively

When you receive loan offers from different banks, credit unions, or the dealership itself, a calculator becomes your ultimate comparison tool. Instead of just looking at the APR, you can input each offer’s terms and see the direct impact on your monthly payment and total cost. This allows for a true apples-to-apples comparison.

Pro tips from us: Don’t just compare APRs; compare the total interest paid over the life of the loan for a comprehensive view of which offer is genuinely better for your wallet. A slightly higher APR on a shorter term might still be cheaper overall than a low APR on a very long term.

3. Understanding the True Cost of Ownership

Many buyers fixate on the purchase price, but the true cost of a car includes the interest paid over the loan term. A calculator illuminates this "hidden" cost, showing you exactly how much extra you’re paying to borrow the money. This transparency is vital for long-term financial planning.

By seeing the total cost, you can make more informed decisions about whether a particular vehicle is worth its overall expense. It helps you factor in depreciation, insurance, and maintenance costs more realistically, as you have a clear picture of the financing component.

4. Enhanced Negotiation Power

Walking into a dealership armed with your own payment calculations puts you in a position of strength. You know your budget, you understand how different variables affect payments, and you can quickly assess the fairness of any offer. This knowledge allows you to negotiate with confidence.

You can counter an offer not just on the car’s price, but also on the loan’s terms. For instance, if a dealer tries to stretch your loan term to lower the monthly payment, you can point out the increased total interest and suggest alternative adjustments.

5. Avoiding Financial Surprises

There’s nothing worse than signing on the dotted line only to realize your monthly payment is higher than anticipated, or that hidden fees have inflated the total cost. By running various scenarios with a calculator, you can anticipate these costs and ensure there are no unwelcome surprises.

This due diligence provides peace of mind, knowing that you’ve thoroughly vetted the financial implications of your purchase. It allows you to address any discrepancies before commitment, preventing future financial strain.

6. Saving Money in the Long Run

Ultimately, the biggest benefit is the potential to save a substantial amount of money. By understanding the impact of down payments, interest rates, and loan terms, you can strategize to minimize interest paid. A few percentage points off your APR or a slightly shorter term can translate into hundreds, if not thousands, of dollars saved over the life of the loan.

Using a calculator empowers you to optimize your loan structure, ensuring you get the best possible deal that aligns with your financial goals, rather than simply accepting the first offer presented.

Beyond the Basics: Advanced Tips for Maximizing Your Calculator’s Potential

While basic calculations are incredibly helpful, a free online car loan calculator can do much more than just estimate your monthly payment. With a little strategic thinking, you can leverage it for more sophisticated financial planning.

1. Considering Extra Payments

Many car loan calculators, especially those offered by financial institutions, allow you to factor in extra payments. This feature is invaluable if you plan to pay off your loan faster. By adding even a small additional amount to your monthly payment, you can significantly reduce the total interest paid and shorten your loan term.

Experiment with different extra payment amounts to see the long-term savings. For instance, paying an extra $50 a month might shave several months off a 60-month loan and save you hundreds in interest. This insight helps you build an aggressive repayment strategy.

2. The Impact of Credit Score on APR

While a calculator can’t directly improve your credit score, it can help you understand its financial impact. If you have an idea of your credit score (e.g., excellent, good, fair), you can research typical APR ranges for those scores. Inputting these different rates into the calculator will vividly show you how much more you’d pay with a lower score.

This visualization can be a powerful motivator to improve your credit before applying for a loan. For strategies on enhancing your credit profile, check out our detailed article: .

3. Factoring in Insurance and Maintenance

A truly holistic view of car ownership goes beyond just the loan payment. While a basic car loan calculator doesn’t have fields for insurance or maintenance, you can use its output as a starting point. Once you have your estimated monthly payment, add your projected insurance premiums and a realistic estimate for maintenance costs.

This combined figure gives you a much more accurate picture of the total monthly cost of ownership. This comprehensive number is crucial for ensuring the car truly fits within your overall budget, preventing financial strain from unexpected expenses.

4. When to Refinance Your Loan

Even after you’ve purchased a car, a free online car loan calculator remains a valuable tool. If interest rates drop, your credit score improves significantly, or your financial situation changes, you might consider refinancing your car loan. Use the calculator to compare your current loan terms with potential new ones.

Input your current loan balance, a new (lower) interest rate, and a desired new loan term to see if refinancing would result in lower monthly payments or significant interest savings. This proactive approach can save you money even years after your initial purchase.

Common Mistakes to Avoid When Using an Auto Loan Calculator

While a free online car loan calculator is a powerful tool, it’s only as effective as the information you feed it and your interpretation of its results. Common mistakes to avoid are often rooted in oversight or misunderstanding, and steering clear of them will ensure you get the most accurate and valuable insights.

1. Ignoring Additional Costs (Tax, Fees, Registration)

One of the most frequent errors is forgetting to factor in sales tax, registration fees, title fees, and dealership documentation fees. These can easily add hundreds, or even thousands, of dollars to the total amount you need to finance. If your calculator doesn’t have specific fields for these, manually add them to your "purchase price" input.

Failing to include these costs will result in an artificially low monthly payment estimate, leading to a financial surprise when you get the actual loan paperwork. Always aim for the most comprehensive cost picture.

2. Only Focusing on the Monthly Payment

While the monthly payment is important for budgeting, it shouldn’t be your only focus. A common sales tactic is to extend the loan term to lower the monthly payment, making the car seem more affordable. However, this often dramatically increases the total interest you pay over the loan’s lifetime.

Always look at the total interest paid and the total cost of the car alongside the monthly payment. A slightly higher monthly payment for a shorter term can save you a significant amount in the long run.

3. Not Trying Different Terms (Loan Lengths)

Sticking to just one loan term (e.g., 60 months) limits your understanding of your options. Experiment with various terms, such as 48, 60, 72, and even 84 months. This allows you to see the trade-offs between lower monthly payments (longer term) and lower total interest (shorter term).

Understanding these variations helps you find the sweet spot that balances affordability with financial efficiency, preventing you from committing to an unnecessarily long and expensive loan.

4. Assuming a Low APR

Unless you have excellent credit and have been pre-approved for a specific rate, don’t assume you’ll qualify for the lowest advertised APR. Input a realistic interest rate based on your credit score. If you’re unsure, use a slightly higher, more conservative rate for your initial calculations.

It’s better to overestimate your APR and be pleasantly surprised than to underestimate it and find your actual payments are much higher than expected. Always get pre-approved or research typical rates for your credit tier.

5. Not Using It Early Enough in the Process

Many buyers only turn to a calculator when they’re already at the dealership, trying to make sense of a loan offer. The true power of the calculator comes from using it before you start shopping. This allows you to set a realistic budget, understand what you can afford, and approach the car buying process from a position of knowledge.

Using the calculator early ensures you’re proactive, not reactive, which is a fundamental principle of smart financial decision-making.

Choosing the Right Free Online Car Loan Calculator for You

With so many options available, how do you pick the best free online car loan calculator? While most perform the basic function well, certain features can elevate your experience and provide deeper insights.

1. Features to Look For

- Comprehensive Inputs: Look for calculators that allow you to input not just the price, down payment, rate, and term, but also trade-in value, sales tax, and other fees. The more variables it can handle, the more accurate your estimate will be.

- Amortization Schedule: A calculator that generates an amortization schedule is a significant plus. This detailed breakdown shows you exactly how much principal and interest you’re paying with each installment, offering full transparency.

- Extra Payment Options: If you plan to pay off your loan early, a calculator that allows you to simulate extra payments can show you the substantial interest savings and how quickly you can become debt-free.

- "What If" Scenarios: The best calculators make it easy to quickly adjust inputs and see immediate changes in the outputs, facilitating quick comparisons and scenario planning.

2. Reputable Sources

Always use calculators from trusted financial institutions, consumer advocacy websites, or well-known automotive portals. These sources are more likely to use accurate formulas and provide reliable estimates. Examples include major banks, credit unions, sites like NerdWallet, Edmunds, or Kelley Blue Book.

Be wary of calculators on obscure websites that might be collecting your data or providing overly simplified, potentially misleading results. Prioritize credibility for financial tools.

3. Mobile-Friendliness and User Experience

In today’s mobile-first world, a good calculator should be easy to use on your smartphone or tablet. A clean, intuitive interface with clear labels and immediate results enhances the user experience. You want a tool that’s quick to navigate and understand, especially if you’re using it on the go or while comparing options at a dealership.

Integrating the Calculator into Your Car Buying Journey (A Step-by-Step Guide)

A free online car loan calculator isn’t a one-time tool; it’s a constant companion throughout your car buying process. Here’s how to effectively integrate it into each stage:

1. Pre-Shopping Phase: Set Your Budget

- Determine Affordability: Before you even look at cars, use the calculator to figure out what monthly payment you’re comfortable with. Start with a target payment and work backward to see what loan amount, term, and interest rate are required.

- Estimate Your Down Payment: Decide how much you can realistically put down. Run scenarios with different down payment amounts to see their impact.

- Get Pre-Approved: Seek pre-approval from a bank or credit union. This gives you a concrete interest rate and maximum loan amount to input into your calculator, making your estimates highly accurate.

- Factor in Trade-In: If you have a trade-in, get an estimate of its value and include it in your calculations.

2. During Shopping Phase: Compare and Refine

- Test Drive, Then Calculate: Once you find a car you like, get its firm selling price. Input this into your calculator along with your pre-approved APR, your planned down payment, and various loan terms.

- Compare Dealership Offers: If a dealership offers financing, input their proposed terms (price, APR, term) into your calculator. Compare their offer against your pre-approval and your own budget to ensure it aligns with your financial goals.

- Adjust on the Fly: Don’t be afraid to adjust variables in the calculator while at the dealership. See how a slightly different down payment or a shorter term changes the numbers. This empowers you in negotiations.

3. Before Signing: Verify Everything

- Final Review: Before signing any paperwork, take the final numbers from the loan agreement (exact loan amount, APR, term, and any fees) and plug them into your free online car loan calculator one last time.

- Check for Discrepancies: Ensure the calculator’s output for monthly payment and total cost matches what’s on the official loan documents. If there are significant differences, ask for clarification before you sign.

- Understand the Fine Print: Use the calculator’s insights to better understand the impact of every line item on your loan agreement.

For more detailed advice on navigating the car buying process, the Consumer Financial Protection Bureau (CFPB) offers excellent resources on understanding auto loans and making smart decisions.

Conclusion: Empower Your Car Buying Journey with a Free Online Car Loan Calculator

The journey to owning a new vehicle is a significant financial undertaking, but it doesn’t have to be overwhelming. By embracing the power of a free online car loan calculator, you transform from a passive recipient of loan offers into an empowered, informed consumer. This simple yet sophisticated tool demystifies the complexities of auto financing, putting you firmly in control.

Throughout this comprehensive guide, we’ve explored every facet of these invaluable calculators – from understanding their core inputs and mechanics to leveraging advanced features and avoiding common mistakes. We’ve highlighted how they offer budgeting precision, enhance your negotiation power, and ultimately, save you money by revealing the true cost of your car.

Remember, the goal is not just to find a car, but to secure one that comfortably fits into your financial life without causing undue stress. So, as you embark on your next car buying adventure, make sure your first stop is always a reputable free online car loan calculator. It’s the smartest step you can take towards driving away with confidence and financial peace of mind. Start calculating today, and drive smarter tomorrow!