Unlock Your Dream Car: The Ultimate Guide to Using a Personal Loan for Your Next Vehicle Purchase

Unlock Your Dream Car: The Ultimate Guide to Using a Personal Loan for Your Next Vehicle Purchase Carloan.Guidemechanic.com

Buying a car is a significant milestone for many, offering unparalleled freedom and convenience. However, the path to vehicle ownership often involves navigating complex financing options. While traditional auto loans are the go-to for most, a personal loan for a car purchase is an increasingly popular and flexible alternative that many overlook. It’s a versatile tool that can open doors to owning the exact vehicle you desire, whether it’s a brand-new sedan or a cherished classic from a private seller.

This comprehensive guide will delve deep into everything you need to know about using a personal loan to buy a car. We’ll explore its unique advantages, potential drawbacks, the application process, and crucial financial considerations. Our goal is to equip you with the knowledge to make an informed decision, ensuring you drive away with confidence and a financing plan that perfectly suits your needs. By the end of this article, you’ll understand why a personal loan might just be the smart choice for your next car.

Unlock Your Dream Car: The Ultimate Guide to Using a Personal Loan for Your Next Vehicle Purchase

Understanding Personal Loans in the Context of Car Purchases

Before diving into the specifics of buying a car with a personal loan, it’s essential to grasp what a personal loan truly is and how it differs from other financing methods. A personal loan is a type of unsecured loan, meaning it doesn’t require any collateral like a house or a car to secure the borrowed funds. This is a crucial distinction that impacts everything from interest rates to the application process.

Lenders provide personal loans based primarily on your creditworthiness and your ability to repay the debt. Once approved, the funds are typically deposited directly into your bank account, giving you the freedom to use them for almost any purpose. This flexibility is one of the main reasons why personal loans are becoming a go-to option for those looking to purchase a vehicle outside of traditional dealership financing.

How Does a Personal Loan Differ from a Traditional Car Loan?

The differences between a personal loan and a traditional auto loan are fundamental and understanding them is key to making the right financial decision. A traditional car loan, whether from a dealership or a bank, is a secured loan. This means the car itself acts as collateral for the loan. If you fail to make payments, the lender has the right to repossess the vehicle.

With a personal loan for car financing, the situation is entirely different. Since it’s generally unsecured, the car is not used as collateral. This means that you own the car outright from day one, without the lender holding the title. This distinction offers a unique set of benefits and considerations, which we will explore in detail.

The Distinct Advantages of Using a Personal Loan for Your Car Purchase

Opting for a personal loan to purchase your vehicle comes with several compelling benefits that might make it a more suitable choice for your specific situation. These advantages often center around flexibility, ownership, and simplicity.

1. Unparalleled Flexibility in Car Choice and Seller

One of the most significant advantages of using a personal loan is the freedom it provides regarding your car choice. Traditional auto loans often have restrictions on the age, mileage, or type of vehicle they will finance, especially for used cars. Dealerships might also push you towards specific models or financing plans.

With a personal loan, the funds are yours to use as cash. This means you can buy a car from any seller – a private individual, an independent dealer, or even an auction – without being tied to specific lender requirements about the vehicle itself. Based on my experience, this flexibility can be a game-changer, allowing you to secure that rare classic car or a well-maintained used vehicle that wouldn’t qualify for conventional auto financing.

2. Immediate Ownership of Your Vehicle

When you use a personal loan, you essentially purchase the car with cash. This means you gain full ownership of the vehicle from the moment the transaction is complete. The lender has no claim on the car itself, and the title is immediately in your name.

This offers peace of mind and simplifies any future actions, such as selling the car or making modifications, without needing lender approval. In contrast, with a traditional auto loan, the lender holds the title until the loan is fully repaid, giving them a lien on the vehicle.

3. Potentially Competitive Interest Rates (Especially for Good Credit)

For individuals with excellent credit scores, a personal loan can sometimes offer competitive or even lower interest rates compared to certain traditional auto loans, particularly those offered by dealerships. While auto loans are typically secured and therefore often have lower rates, an unsecured personal loan for someone with a pristine credit history can sometimes rival or beat specific car loan offers, especially if those offers come with various fees or strict terms.

Pro tips from us: Always compare the Annual Percentage Rate (APR) for both types of loans, as it includes all fees and provides the true cost of borrowing. Don’t just look at the advertised interest rate.

4. Simpler and Quicker Application Process

Applying for a personal loan can often be a more streamlined and faster process than applying for a traditional car loan. Since there’s no vehicle appraisal or title transfer process involved from the lender’s side, the paperwork is usually less extensive. Many online lenders offer quick pre-approvals and can disburse funds within a day or two after final approval.

This speed and simplicity can be incredibly beneficial, especially if you need to secure financing quickly to capitalize on a good deal from a private seller. You avoid the lengthy back-and-forth often associated with car dealerships and their financing departments.

5. No Collateral Required (for Unsecured Loans)

As mentioned, most personal loans are unsecured, meaning you don’t have to put up any asset as collateral. This significantly reduces your risk. If unforeseen circumstances make it difficult to repay the loan, your car cannot be repossessed by the personal loan lender.

While default still carries severe consequences for your credit score and financial standing, the immediate threat of losing your vehicle is removed. This can offer a layer of security that a traditional secured auto loan simply cannot provide.

Potential Disadvantages and Critical Considerations

While personal loans offer attractive benefits, they also come with certain drawbacks and considerations that are crucial to understand. It’s important to weigh these against the advantages to determine if this financing option is right for you.

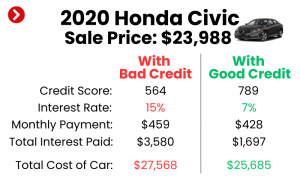

1. Potentially Higher Interest Rates (Especially for Average/Poor Credit)

For many borrowers, particularly those with average or lower credit scores, personal loan interest rates can be significantly higher than those for traditional secured auto loans. Since there’s no collateral backing the loan, lenders perceive a higher risk, which they mitigate by charging higher interest.

Common mistakes to avoid are focusing solely on the monthly payment without considering the total interest paid over the life of the loan. A higher interest rate means a more expensive loan overall, even if the monthly payments seem manageable.

2. Impact on Your Credit Score

Applying for a personal loan involves a hard inquiry on your credit report, which can temporarily lower your credit score by a few points. Furthermore, if you take on a large personal loan, it will increase your overall debt burden, potentially impacting your debt-to-income ratio.

This higher debt-to-income ratio could make it harder to qualify for other loans or lines of credit in the future. Responsible repayment is crucial, as late payments or defaults will severely damage your credit history.

3. Loan Amount Limits

Personal loans often have maximum borrowing limits that might not be sufficient for very expensive vehicles. While some lenders offer personal loans up to $100,000, many have lower caps, especially for first-time borrowers or those with less-than-perfect credit.

If you’re eyeing a luxury car or a high-performance vehicle, a personal loan might not cover the full purchase price, requiring you to make a substantial down payment from other sources.

4. No Car as Collateral Means Higher Lender Risk

From the lender’s perspective, the absence of collateral means a higher risk. This is why interest rates can be higher for personal loans compared to secured loans. Lenders have less recourse if a borrower defaults, making them more selective about who they approve and at what rates.

This inherent risk for the lender translates into stricter eligibility criteria and potentially less favorable terms for the borrower, especially if your financial profile isn’t exceptionally strong.

Eligibility Criteria for a Personal Loan for Car Financing

Lenders assess several factors when evaluating your application for a personal loan. Understanding these criteria beforehand can help you prepare and improve your chances of approval.

1. Your Credit Score: The Most Crucial Factor

Your credit score is arguably the single most important factor lenders consider. A higher credit score (generally 670 and above for FICO) indicates a lower risk to lenders, making you eligible for better interest rates and higher loan amounts. Lenders use your score to gauge your history of responsible borrowing and repayment.

For those with lower credit scores, approval might still be possible, but expect higher interest rates and potentially stricter terms. Based on my experience, a score below 600 often makes it challenging to secure favorable personal loan terms without a co-signer. For a deeper dive into improving your credit score, check out our guide on .

2. Stable Income and Employment History

Lenders need assurance that you have a consistent and sufficient income to comfortably make your monthly loan payments. They will typically ask for proof of income, such as pay stubs, W-2 forms, or tax returns. A stable employment history, usually at least one to two years with the same employer, further demonstrates reliability.

Freelancers or self-employed individuals might need to provide more extensive documentation, such as bank statements or profit and loss statements, to prove their income stability.

3. Debt-to-Income (DTI) Ratio

Your debt-to-income (DTI) ratio is another critical metric. It compares your total monthly debt payments to your gross monthly income. Lenders prefer a lower DTI ratio, typically below 36%, as it indicates you aren’t overextended with existing debts and can handle additional payments.

A high DTI ratio signals to lenders that you might struggle to manage another loan, even if your income is substantial. From a lender’s perspective, these factors paint a clear picture of your repayment capacity and overall financial health.

4. Age and Residency Requirements

Basic eligibility requirements include being at least 18 years old (19 or 21 in some states) and a U.S. citizen or permanent resident. Lenders will also require a valid government-issued ID and a Social Security number.

These foundational criteria ensure you are legally able to enter into a loan agreement and can be properly identified.

The Personal Loan Application Process for Buying a Car

Applying for a personal loan to purchase a car involves several straightforward steps. Being prepared and understanding each stage can make the process smoother and faster.

Step 1: Assess Your Needs and Budget

Before you even look at loans, determine how much you need to borrow and, more importantly, what you can truly afford. Factor in not just the car’s purchase price but also potential taxes, registration fees, and insurance.

Use an online loan calculator to estimate monthly payments at various interest rates and loan terms. To master your budget, read our comprehensive guide on .

Step 2: Check Your Credit Score and Report

Knowing your credit score is vital. Obtain a free copy of your credit report from AnnualCreditReport.com to check for any errors and understand your current credit standing. This will give you an idea of the interest rates you might qualify for.

If your score is lower than desired, consider taking steps to improve it before applying, as even a small increase can lead to better loan terms.

Step 3: Research and Compare Lenders

Don’t jump at the first offer. Research various lenders, including traditional banks, credit unions, and online lenders. Each type of lender has its own strengths: banks for established relationships, credit unions for potentially lower rates and personalized service, and online lenders for speed and convenience.

Compare interest rates (APR), loan terms, fees (like origination or prepayment penalties), and customer reviews. Pro tips from us: Many lenders offer a "soft inquiry" pre-qualification process that won’t harm your credit score, allowing you to compare offers.

Step 4: Gather Required Documents

Once you’ve chosen a few potential lenders, gather all necessary documents. This typically includes:

- Proof of identity (driver’s license, passport)

- Proof of address (utility bill, lease agreement)

- Proof of income (pay stubs, W-2s, tax returns, bank statements)

- Social Security number

- Bank account information for fund disbursement

Having these ready will significantly speed up the application process.

Step 5: Submit Your Application

Complete the loan application, either online or in person. Be thorough and accurate with all information. This is where the hard credit inquiry will occur, which is a necessary step for formal approval.

Many online applications can be completed in minutes, with a decision often provided within the same day.

Step 6: Review Loan Offers and Terms

If approved, you’ll receive a loan offer outlining the principal amount, interest rate (APR), repayment term, and monthly payment. Carefully read all the fine print, including any fees or penalties.

Ensure you understand the total cost of the loan and that the monthly payments fit comfortably within your budget.

Step 7: Accept Funds and Purchase Your Car

Once you accept the loan terms, the funds will typically be disbursed directly into your bank account within a few business days. With the cash in hand, you can then proceed to purchase your desired car, just as if you were paying with your own savings.

Remember, once the funds are yours, the responsibility of timely repayment begins.

Navigating Interest Rates and Fees

Understanding the true cost of your personal loan goes beyond just the interest rate. Several other factors contribute to the overall expense.

Annual Percentage Rate (APR)

The APR is the most important number to look at when comparing loan offers. It represents the true annual cost of borrowing, including the interest rate and any additional fees, such as origination fees. This provides a more comprehensive picture than just the nominal interest rate.

A good external resource for understanding APR and other loan terms is the Consumer Financial Protection Bureau (CFPB) website, which offers clear explanations and consumer guides on financial products. External Link: https://www.consumerfinance.gov/consumer-tools/auto-loans/

Origination Fees

Some lenders charge an origination fee, which is a one-time charge for processing your loan. This fee is typically a percentage of the total loan amount and can be deducted from your loan proceeds or added to your loan balance.

Always factor this into your calculations, as it reduces the actual amount of cash you receive or increases your total repayment.

Prepayment Penalties

While less common with personal loans than with some other loan types, some lenders may impose a prepayment penalty if you pay off your loan early. This fee compensates the lender for the interest they would have earned.

If you anticipate paying off your loan ahead of schedule, ensure your chosen lender does not have such a penalty.

Understanding Loan Terms

The loan term, or repayment period, significantly impacts your monthly payment and the total interest paid. Shorter terms mean higher monthly payments but less interest paid over time. Longer terms result in lower monthly payments but more interest over the life of the loan.

Choose a term that balances affordability with the overall cost of the loan.

Special Scenarios & Considerations

Beyond the standard application, certain situations might lead you to consider specific types of personal loans or alternative strategies.

Personal Loan for a Car with Bad Credit

Securing a personal loan for a car with bad credit is challenging but not impossible. Lenders offering loans to borrowers with poor credit typically charge significantly higher interest rates to offset the increased risk. The loan amounts might also be smaller.

Based on my observation, lenders offering bad credit personal loans often focus more on income stability and your ability to demonstrate consistent repayment from other sources. You might also consider applying with a co-signer who has good credit, which can improve your chances of approval and secure a better interest rate.

Secured Personal Loans

While most personal loans are unsecured, some lenders offer secured personal loans. In this scenario, you would use another asset you own, such as a savings account or a certificate of deposit (CD), as collateral.

This can be an option if you have poor credit but possess other assets, as it typically results in lower interest rates than an unsecured loan for the same credit profile. However, it means putting another asset at risk.

Refinancing Your Personal Loan

If your credit score improves significantly after taking out a personal loan, or if interest rates drop, you might be able to refinance your personal loan. Refinancing involves taking out a new loan, usually with a lower interest rate, to pay off your existing loan.

This can reduce your monthly payments or the total interest paid over the life of the loan. However, be aware of any prepayment penalties on your original loan and any origination fees on the new loan.

Financial Planning Before Taking the Plunge

A personal loan can be an excellent tool for buying a car, but it’s crucial to integrate it into a sound financial plan. A car purchase involves more than just the loan payment.

Budgeting for All Car-Related Expenses

Your monthly budget for a car needs to extend far beyond the loan payment. Factor in:

- Car Insurance: This can be a significant monthly cost, varying widely based on your car, driving history, and location.

- Fuel Costs: Estimate your weekly or monthly fuel expenses based on your commute and driving habits.

- Maintenance and Repairs: Set aside a contingency fund for routine maintenance (oil changes, tire rotations) and unexpected repairs.

- Registration and Licensing Fees: Annual or biannual costs associated with vehicle ownership.

Neglecting these additional costs is a common mistake that can quickly lead to financial strain.

Building an Emergency Fund

Before committing to a personal loan, ensure you have a robust emergency fund. This fund, typically three to six months’ worth of living expenses, acts as a financial safety net.

If you face an unexpected job loss, medical emergency, or significant car repair, your emergency fund can prevent you from defaulting on your loan payments, protecting your credit score.

Considering the Total Cost of Ownership

Don’t just look at the purchase price or monthly loan payment. Consider the total cost of ownership over the expected lifespan of the vehicle. This includes depreciation, insurance, fuel, maintenance, and the total interest paid on your loan.

A seemingly cheaper car with high maintenance costs or poor fuel efficiency might end up being more expensive in the long run.

Conclusion: Your Road to Informed Car Ownership

Using a personal loan to purchase a car offers a unique blend of flexibility, immediate ownership, and potentially competitive rates for those with strong credit. It empowers you to buy the exact vehicle you want, from any seller, without the typical restrictions of traditional auto financing. However, it’s a decision that requires careful consideration of higher potential interest rates, the impact on your credit, and the overall financial commitment.

By understanding the distinct advantages and disadvantages, diligently checking your eligibility, meticulously navigating the application process, and planning for all associated costs, you can harness the power of a personal loan to make your dream car a reality. Remember, the ultimate goal is not just to buy a car, but to do so responsibly, ensuring your financial well-being remains intact. Make an informed choice, and enjoy the open road ahead!