Unlock Your Dream Mazda: The Ultimate Guide to Securing the Best Mazda Car Loan

Unlock Your Dream Mazda: The Ultimate Guide to Securing the Best Mazda Car Loan Carloan.Guidemechanic.com

The allure of a Mazda is undeniable. From the sleek lines of a Mazda3 to the spirited performance of a CX-5 or the iconic MX-5 Miata, these vehicles offer a driving experience that blends elegance, innovation, and pure joy. But before you can feel the zoom-zoom behind the wheel, there’s often one crucial step: securing a Mazda car loan.

Navigating the world of auto financing can seem daunting, filled with jargon and endless options. However, with the right knowledge and a strategic approach, securing a Mazda car loan can be a straightforward and even empowering process. This comprehensive guide will demystify Mazda financing, offering expert insights and practical advice to help you drive away in your dream car with confidence. We’ll delve deep into every aspect, ensuring you’re well-equipped to make informed decisions.

Unlock Your Dream Mazda: The Ultimate Guide to Securing the Best Mazda Car Loan

Understanding Mazda Financial Services (MFS): Your Primary Partner

When you’re considering a new or Certified Pre-Owned (CPO) Mazda, Mazda Financial Services (MFS) is often your first and most convenient stop for financing. MFS is the captive finance arm of Mazda, meaning it’s specifically designed to support Mazda sales by offering competitive financing solutions directly to customers. They understand Mazda vehicles better than anyone.

Financing directly through MFS offers several distinct advantages. They frequently run special promotional interest rates and lease offers that are exclusively available through authorized Mazda dealerships. These incentives can significantly reduce your overall cost of ownership or your monthly payments, making a new Mazda even more accessible. Based on my experience in the auto industry, these manufacturer-backed programs are often the most attractive deals available.

Beyond standard car loans, MFS also provides flexible leasing options, which can be an excellent choice for drivers who prefer to upgrade their vehicle every few years. They also handle vehicle protection plans and other services, ensuring a holistic approach to your ownership experience. This integrated approach means less paperwork and a more streamlined process at the dealership.

Types of Mazda Car Loans: New vs. Used

The type of Mazda car loan you pursue will largely depend on whether you’re buying a brand-new vehicle or a pre-owned one. Each category comes with its own set of considerations and financing characteristics. Understanding these differences is key to making the best financial decision.

New Mazda Loans: These loans are typically for vehicles fresh off the assembly line. They often come with the lowest interest rates, especially when manufacturers offer promotional APRs (Annual Percentage Rates) to entice buyers. Loan terms for new cars can range from 24 to 84 months, with longer terms offering lower monthly payments but potentially higher overall interest paid. New car loans are generally easier to qualify for due to the vehicle’s pristine condition and higher resale value.

Used Mazda Loans: Financing a used Mazda involves a slightly different landscape. While still very accessible, interest rates on used car loans can be a bit higher than new car loans. This is often because used vehicles, depending on their age and mileage, carry a higher perceived risk for lenders. Loan terms are also typically shorter, often capping at 60 or 72 months. When considering a used Mazda, be sure to factor in its age and condition, as these will influence both the loan terms and the vehicle’s long-term reliability.

Certified Pre-Owned (CPO) Mazda Loans: This category offers a fantastic middle ground. CPO Mazdas are used vehicles that have undergone a rigorous multi-point inspection and reconditioning process by Mazda-trained technicians. They often come with an extended factory warranty, providing peace of mind similar to a new car. Financing for CPO Mazdas tends to fall between new and standard used car loans in terms of interest rates and terms. Many CPO programs offer special financing rates through MFS, making them an incredibly attractive option. Pro tips from us: CPO programs reduce risk for both you and the lender, often leading to better Mazda financing terms.

The Application Process: Step-by-Step Guide to Getting Approved

Securing a Mazda car loan doesn’t have to be a mystery. By understanding the application process, you can approach it with confidence and increase your chances of approval. Being prepared is half the battle.

The process typically begins with either getting pre-approved or applying directly at the dealership. Getting pre-approved through your bank, credit union, or an online lender before you visit the dealership is a powerful strategy. It gives you a clear understanding of what interest rate you qualify for and your maximum loan amount. This knowledge empowers you to negotiate the car price as a cash buyer, separating the vehicle price negotiation from the financing discussion.

When you’re ready to apply, either pre-approval or at the dealership, lenders will require several key documents. You’ll need valid identification (driver’s license), proof of income (pay stubs, tax returns, employment verification), and proof of residence (utility bill, lease agreement). They’ll also ask for your Social Security number to pull your credit report. Providing these documents promptly and accurately will expedite the approval process.

Lenders look at several factors when evaluating your application for a Mazda car loan. Your credit score is paramount, but they also assess your debt-to-income ratio (DTI), which shows how much of your gross monthly income goes towards debt payments. A stable employment history and a reasonable down payment also significantly strengthen your application. Common mistakes to avoid are not having all your documents ready or providing inconsistent information.

Credit Score and Its Impact on Your Mazda Car Loan

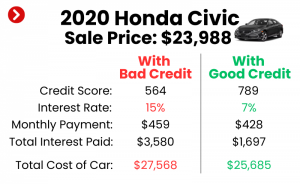

Your credit score is arguably the most influential factor in determining the interest rate and terms of your Mazda car loan. It’s a three-digit number that represents your creditworthiness, essentially telling lenders how risky it might be to lend you money. A higher score indicates a lower risk, translating to better loan offers.

Credit scores generally range from 300 to 850, with different tiers indicating various levels of credit quality. For example, scores above 720 are typically considered "excellent," 660-719 "good," 620-659 "fair," and below 620 "poor." Lenders use these ranges to categorize applicants and assign corresponding interest rates. Those with excellent credit will receive the most favorable rates on their Mazda financing, while those with lower scores will likely face higher rates to offset the increased risk.

Before you even think about applying for a Mazda car loan, it’s a pro tip from us to check your credit report and score. You can obtain a free copy of your credit report annually from each of the three major bureaus (Equifax, Experian, TransUnion) at AnnualCreditReport.com. Review it for any errors or discrepancies that could be negatively impacting your score. If you find errors, dispute them immediately.

If your credit score isn’t where you’d like it to be, there are strategies to improve it. Paying bills on time, reducing existing debt, and avoiding opening new lines of credit just before applying for a car loan can all help. Even a small increase in your score can lead to significant savings on interest over the life of your Mazda auto loan.

Down Payments and Trade-Ins: Paving the Way to Lower Payments

A substantial down payment and a valuable trade-in can dramatically improve the terms of your Mazda car loan. These elements directly reduce the amount of money you need to borrow, which in turn lowers your monthly payments and the total interest you’ll pay over the loan’s term. It’s a powerful financial lever.

The power of a down payment cannot be overstated. When you put money down upfront, you immediately reduce your principal loan amount. This means you’re borrowing less, which directly translates to lower monthly payments. Furthermore, a larger down payment often signals to lenders that you are a lower-risk borrower, potentially qualifying you for a better interest rate on your Mazda financing. Based on my experience, aiming for at least 10-20% of the vehicle’s price as a down payment is an excellent strategy.

If you have an existing vehicle, a trade-in can serve as an excellent form of down payment. The value of your trade-in is deducted from the purchase price of your new Mazda, reducing the amount you need to finance. To get the best value for your trade-in, do your research beforehand. Use online valuation tools like Kelley Blue Book or Edmunds to get an estimate of your car’s worth. Ensure your car is clean and well-maintained when you bring it to the dealership.

Calculating your equity in your current vehicle is crucial. If you owe less on your car than its market value, you have "positive equity," which acts like cash towards your new Mazda. If you owe more, you have "negative equity," which will need to be rolled into your new Mazda car loan, increasing your overall loan amount. It’s important to understand this before negotiating.

Interest Rates: What Drives Them and How to Get the Best Deal

The interest rate is arguably the most critical component of your Mazda car loan, as it dictates how much extra you’ll pay over the life of the loan. Understanding what influences these rates and how to negotiate them is vital for securing an affordable Mazda auto loan. A lower interest rate means more money in your pocket.

Several factors significantly influence the interest rate you’ll be offered. As discussed, your credit score is paramount; higher scores get lower rates. The loan term also plays a role; shorter terms generally have lower rates because the lender’s risk is reduced over a shorter period. Current market rates set by the Federal Reserve also impact auto loan rates across the board. The down payment amount and the age of the vehicle (new vs. used) also affect the risk assessment and, consequently, the rate.

When comparing Mazda car loan offers, you’ll encounter both fixed and variable interest rates. A fixed-rate loan means your interest rate remains constant throughout the entire loan term, providing predictable monthly payments. A variable-rate loan means your interest rate can fluctuate based on market conditions, potentially leading to changing monthly payments. Based on my experience, fixed-rate loans are generally preferred for peace of mind and budget stability.

Don’t be afraid to negotiate the interest rate, especially if you have excellent credit or multiple pre-approvals. Dealerships often have some flexibility, and showing them a lower rate you’ve been offered elsewhere can motivate them to match or even beat it. Pro tips from us: Even a small percentage point difference in your Mazda financing rate can save you hundreds, if not thousands, of dollars over the life of the loan. Always get multiple quotes before committing.

Loan Terms and Monthly Payments: Finding Your Sweet Spot

Choosing the right loan term for your Mazda car loan is a delicate balance between managing your monthly budget and minimizing the total interest paid. Loan terms are typically expressed in months, such as 24, 36, 48, 60, 72, or even 84 months. Each option has its own financial implications.

Shorter loan terms (e.g., 36 or 48 months) usually come with higher monthly payments but result in significantly less interest paid over the life of the loan. This means you own your Mazda outright much faster and save a substantial amount of money in the long run. If your budget allows for higher monthly payments, a shorter term is almost always the more financially savvy choice for your Mazda financing.

Longer loan terms (e.g., 72 or 84 months) offer lower monthly payments, making a new Mazda more affordable on a month-to-month basis. However, this convenience comes at a cost. You’ll pay more in total interest over the longer term, and you might face a period where your car’s value depreciates faster than you’re paying off the loan (known as being "upside down" or "underwater"). While lower payments can be tempting, it’s a common mistake to focus solely on the monthly payment without considering the total cost of the Mazda auto loan.

It’s crucial to budget effectively for your monthly Mazda payment. Don’t just consider the loan payment; remember to factor in insurance, fuel, maintenance, and any other associated costs of car ownership. Use online car loan calculators to experiment with different loan amounts, interest rates, and terms to find a monthly payment that comfortably fits within your budget without stretching you too thin.

Alternative Financing Options for Your Mazda

While Mazda Financial Services is a great starting point, it’s always wise to explore other financing avenues for your Mazda car loan. Comparing offers from various lenders can ensure you get the most competitive rates and terms. Diversifying your search can lead to significant savings.

Credit unions are member-owned financial institutions known for offering competitive auto loan rates, often lower than traditional banks. They prioritize their members and frequently have more flexible lending criteria. If you’re eligible to join a credit union (often based on residency, employer, or association), they can be an excellent source for Mazda financing.

Banks (both national and local) are another traditional source for auto loans. They offer a wide range of products and services, and if you have an existing relationship with a bank, they might offer you preferred rates. It’s worth checking with your current bank to see what they can offer before you commit to any other lender.

Online lenders have grown in popularity due to their convenience and competitive rates. Companies like Capital One Auto Finance, LightStream, or Carvana offer streamlined application processes that can often provide pre-approvals within minutes. They allow you to shop for your Mazda car loan from the comfort of your home, and their rates can sometimes undercut traditional institutions. However, always ensure the online lender is reputable and transparent with their terms.

Each option has its pros and cons. MFS offers convenience and specific Mazda incentives. Credit unions offer member benefits and often lower rates. Banks provide familiarity and established relationships. Online lenders offer speed and convenience. Pro tips from us: Apply to at least three different lenders (including MFS) to compare offers comprehensively before making a decision.

Securing a Mazda Car Loan with Less-Than-Perfect Credit

Having a less-than-perfect credit score doesn’t automatically close the door on owning a Mazda. While it might present more challenges, there are viable options for securing a Mazda car loan even with bad credit. It’s not impossible, but expectations need to be managed.

One of the most effective strategies for those with bad credit is to find a co-signer. A co-signer, typically a trusted friend or family member with good credit, agrees to be equally responsible for the loan. Their strong credit profile can help you qualify for a loan and potentially secure a much better interest rate than you would on your own. However, ensure both parties understand the full implications and responsibilities.

Another powerful tool is making a larger down payment. By putting more money down upfront, you reduce the amount the lender needs to finance, thereby decreasing their risk. This can significantly improve your chances of approval for a Mazda auto loan, even with a lower credit score. It also shows the lender your commitment to the purchase.

Some lenders specialize in what are known as subprime auto loans. These lenders are willing to take on higher-risk borrowers, but they typically charge significantly higher interest rates to compensate for that risk. While these loans make car ownership possible, it’s crucial to understand the high cost involved and ensure the payments are truly affordable. Based on my experience, these loans can be a stepping stone to rebuilding credit, but careful consideration is required.

Securing a Mazda car loan with bad credit can also be an opportunity to rebuild your credit. By consistently making on-time payments, you demonstrate financial responsibility, which will positively impact your credit score over time. This can pave the way for better financing options in the future, perhaps even allowing you to refinance your Mazda car loan at a lower rate down the line.

Refinancing Your Mazda Car Loan: When and Why It Makes Sense

Even after you’ve secured your initial Mazda car loan, the financial journey doesn’t necessarily end. Refinancing your Mazda auto loan can be a smart move in certain situations, potentially saving you money or improving your monthly cash flow. It’s about optimizing your existing loan for better terms.

There are several compelling reasons to consider refinancing your Mazda car loan. The most common is to lower your interest rate. If your credit score has significantly improved since you first took out the loan, or if market interest rates have dropped, you might qualify for a much better rate. Even a slight reduction can lead to substantial savings over the remaining term of your loan.

Another reason is to reduce your monthly payments. This can be achieved either by securing a lower interest rate or by extending your loan term. While extending the term will mean paying more in total interest, it can provide much-needed breathing room in your monthly budget if you’re facing financial constraints. Conversely, you might also want to refinance to a shorter loan term if your financial situation has improved, allowing you to pay off your Mazda faster and save on overall interest.

The refinancing process is similar to applying for an initial loan. You’ll compare offers from various lenders (banks, credit unions, online lenders), submit an application, and provide necessary documents. Once approved, the new lender pays off your old loan, and you begin making payments to the new lender under the new terms.

When is the right time to refinance? Consider it if your credit score has improved, if interest rates have fallen, if you want to change your loan term, or if you’re looking to remove a co-signer from the original loan. Pro tips from us: Always calculate the total savings over the life of the loan to ensure refinancing is truly beneficial after considering any potential fees.

Common Mistakes to Avoid When Getting a Mazda Car Loan

Navigating the car loan process can be complex, and it’s easy to fall into common traps that can cost you money and peace of mind. Based on years of advising car buyers, these are the pitfalls I see most often that you should absolutely avoid when securing your Mazda car loan.

- Not Comparing Offers: This is perhaps the biggest mistake. Relying solely on the financing offered by the dealership, without checking rates from banks, credit unions, or online lenders, means you could be leaving money on the table. Always shop around for your Mazda financing.

- Focusing Only on Monthly Payments: While your monthly budget is important, fixating solely on the lowest possible monthly payment can lead to longer loan terms and significantly higher total interest paid. Always ask for the total cost of the loan and compare APRs.

- Ignoring the Total Cost of the Loan: Beyond the monthly payment, understand the total amount you will pay over the life of the loan, including all interest and fees. A lower monthly payment over a longer term often means a higher overall cost.

- Not Checking Your Credit Report: As mentioned earlier, reviewing your credit report for errors and understanding your score beforehand is crucial. Not doing so can result in higher interest rates due to inaccurate information or a lack of preparation.

- Rolling Negative Equity into a New Loan: If you owe more on your trade-in than it’s worth, rolling that negative equity into your new Mazda car loan immediately puts you underwater on the new vehicle. It’s often better to pay off the negative equity separately if possible.

- Skipping the Down Payment: While zero-down loans exist, making a down payment significantly reduces your principal, lowers monthly payments, and reduces the total interest paid. It also creates immediate equity in your Mazda.

- Not Reading the Fine Print: Always read your loan agreement thoroughly before signing. Understand all terms, conditions, fees, and penalties for early payoff or late payments. If something is unclear, ask for clarification. Don’t be rushed.

By being aware of these common mistakes, you can approach the Mazda car loan process with greater confidence and secure a deal that truly benefits you.

Conclusion: Your Road to Mazda Ownership Starts Here

Securing a Mazda car loan doesn’t have to be a source of stress. By understanding the various financing options, preparing your application, knowing the impact of your credit score, and strategically using down payments and trade-ins, you can confidently navigate the process. This comprehensive guide has equipped you with the expert knowledge to make informed decisions, ensuring you get the best possible terms for your Mazda financing.

Remember, the goal is not just to get approved, but to secure a Mazda auto loan that aligns with your financial goals and budget. Take the time to compare offers, negotiate wisely, and avoid common pitfalls. With this knowledge in hand, you’re now ready to embark on your journey towards Mazda ownership. Go forth, secure your ideal Mazda car loan, and enjoy the exhilarating driving experience that awaits you!

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Always consult with a qualified financial advisor before making significant financial decisions.

Explore More:

- Understanding Your Credit Score Before Buying a Car (Internal Link)

- The Ultimate Guide to Car Trade-Ins (Internal Link)

- For official information on Mazda financing, visit the Mazda Financial Services website (External Link)