Unlock Your Dream Ride: A Comprehensive Guide to Applying for a Car Loan with Bank of America

Unlock Your Dream Ride: A Comprehensive Guide to Applying for a Car Loan with Bank of America Carloan.Guidemechanic.com

Embarking on the journey to purchase a new vehicle is an exciting prospect. Whether it’s your first car, an upgrade, or an additional family vehicle, securing the right financing is a pivotal step. For many, Bank of America stands out as a reputable and reliable choice for auto loans, offering a blend of competitive rates, flexible terms, and convenient services.

This in-depth guide is designed to be your ultimate resource, meticulously detailing every aspect of how to apply for a car loan with Bank of America. We’ll delve into the nuances of their offerings, walk you through the application process step-by-step, and equip you with expert insights to enhance your chances of approval. Our goal is to provide you with actionable advice, ensuring a smooth and successful financing experience, and ultimately, getting you behind the wheel of your dream car.

Unlock Your Dream Ride: A Comprehensive Guide to Applying for a Car Loan with Bank of America

Why Choose Bank of America for Your Auto Financing?

When considering a financial institution for such a significant purchase, reputation and reliability are paramount. Bank of America, a global financial giant, brings a wealth of experience and resources to the auto loan market. They are a popular choice for many car buyers due to several compelling reasons.

First and foremost, Bank of America frequently offers competitive interest rates. Their extensive financial backing allows them to provide attractive terms that can lead to significant savings over the life of your loan. This is particularly true for applicants with strong credit profiles.

Beyond rates, the convenience factor is substantial. With a vast network of branches and a robust online platform, managing your application and subsequent loan is incredibly straightforward. Their digital tools simplify the process from pre-qualification to payment.

Furthermore, existing Bank of America customers often benefit from streamlined processes and potentially even preferential rates due to their established relationship. This can be a significant advantage, as the bank already has access to your financial history, potentially speeding up approval times. Their commitment to customer service also ensures you have support throughout your car buying journey.

Understanding Bank of America Car Loan Options

Bank of America understands that not all car buying situations are the same. They offer a diverse range of auto loan products designed to cater to various needs, whether you’re eyeing a brand-new model or a pre-owned gem. Recognizing these options is the first step in aligning your needs with their offerings.

For those seeking the thrill of a brand-new vehicle, Bank of America provides new car loans. These loans are typically for vehicles purchased directly from a dealership and often come with the most favorable rates and terms, reflecting the lower risk associated with new collateral. The bank usually has specific criteria regarding the age and mileage of what qualifies as a "new" car, so it’s always wise to confirm these details.

If a pre-owned vehicle aligns better with your budget or preferences, their used car loans are an excellent option. These loans are designed for vehicles that have had previous owners. While rates might be slightly higher than new car loans, they remain competitive. Bank of America will have specific requirements regarding the maximum age and mileage of the used vehicle they are willing to finance.

Moreover, if you already have a car loan with another lender and are looking to reduce your monthly payments or secure a lower interest rate, Bank of America offers auto loan refinancing. This option can be incredibly beneficial, potentially saving you thousands over the life of your loan. Refinancing involves taking out a new loan with Bank of America to pay off your existing car loan, and it’s a strategy often overlooked by car owners seeking financial relief.

The Pre-Approval Advantage: A Smart First Step

Based on my experience, one of the most powerful tools a car buyer can wield is a pre-approved auto loan. It transforms your position from a mere shopper to a confident, cash-equivalent buyer. Bank of America makes this process accessible, and I strongly recommend it as your initial move.

What exactly is pre-approval? It’s a preliminary commitment from Bank of America to lend you a specific amount of money for a car purchase, based on an initial review of your credit and financial information. This isn’t a final loan offer, but it provides a clear understanding of how much you can borrow and at what potential interest rate. It’s like having a spending limit before you even step foot in a dealership.

The benefits of securing a Bank of America pre-approval are manifold. Firstly, it sets a realistic budget for your car search, preventing you from falling in love with a vehicle outside your financial reach. You’ll know precisely what price range to focus on, streamlining your shopping process significantly.

Secondly, and perhaps most importantly, pre-approval empowers you with negotiation leverage. When you walk into a dealership with your own financing secured, you’re negotiating on price as a cash buyer. This means you can focus solely on getting the best deal on the car itself, rather than being swayed by the dealer’s financing options, which may not always be in your best interest.

To get pre-approved, you’ll typically provide some basic personal, income, and employment information. Bank of America will then perform a "soft" credit inquiry, which doesn’t impact your credit score. If approved, you’ll receive a pre-approval letter stating the maximum loan amount and estimated terms. This document is your golden ticket to a more confident car buying experience.

Step-by-Step Guide: How to Apply for a Car Loan with Bank of America

Applying for a car loan, especially with a major institution like Bank of America, can seem daunting. However, by breaking it down into manageable steps, the process becomes much clearer and less intimidating. Let’s walk through each stage to ensure you’re well-prepared.

Step 1: Gather Your Documents

Preparation is key to a smooth application process. Before you even begin filling out forms, compile all the necessary information and documents. This proactive step can significantly reduce delays and stress.

You will need personal identification, such as a valid driver’s license or state ID. Bank of America will also require your Social Security number to pull your credit report and verify your identity. Ensure all your personal details are accurate and up-to-date.

Financial information is crucial for assessing your ability to repay the loan. This includes proof of income, which could be recent pay stubs, W-2 forms, or tax returns if you’re self-employed. You might also need to provide bank account statements to demonstrate financial stability and liquidity.

Employment details are also vital. Be ready to provide your employer’s name, address, phone number, and your length of employment. Stability in employment is a significant factor in a lender’s decision. If you already have a specific vehicle in mind, you’ll also need its details, such as the make, model, year, and Vehicle Identification Number (VIN).

Step 2: Check Your Credit Score

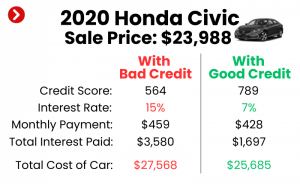

Your credit score is arguably the most critical factor in securing a favorable car loan with Bank of America. It directly influences whether your application is approved and what interest rate you’ll be offered. Taking the time to understand your credit health beforehand is a smart move.

A higher credit score signals lower risk to lenders, often translating to better loan terms and lower interest rates. Conversely, a lower score might lead to higher rates or even denial. You can obtain a free copy of your credit report from each of the three major credit bureaus (Equifax, Experian, and TransUnion) once a year. Review these reports meticulously for any errors that could negatively impact your score.

If your credit score isn’t where you’d like it to be, take steps to improve it before applying. Paying down existing debts, making all payments on time, and avoiding opening new lines of credit can all help boost your score. Even a few points can make a difference in your loan offer. explores how credit scores directly influence your borrowing costs.

Step 3: Choose Your Application Method

Bank of America provides several convenient ways to apply for a car loan, allowing you to choose the method that best suits your preferences and schedule. Each option offers a different level of interaction and convenience.

The most popular method for many is applying online. Bank of America’s website offers a user-friendly application portal where you can complete the entire process from the comfort of your home. This is often the quickest way to get a pre-approval or full loan application submitted, as it’s available 24/7.

Alternatively, you can choose to apply in-person at a Bank of America branch. This option is ideal if you prefer face-to-face interaction, have complex questions, or need assistance gathering documents. A loan officer can guide you through the application, explain terms, and provide personalized advice. This can be particularly helpful if you’re an existing customer.

Finally, you can also apply over the phone. This provides a middle ground, offering direct interaction with a representative without needing to visit a physical branch. You can call their dedicated auto loan department and complete the application with their assistance. Whichever method you choose, ensure you have all your gathered documents ready.

Step 4: Complete the Application

Once you’ve chosen your application method and gathered your documents, the next step is to accurately and thoroughly complete the application form. This is where all your preparation comes together.

Whether online, in-person, or over the phone, you’ll be asked to provide all the information you’ve prepared. This includes personal details, employment history, income information, and details about the vehicle you intend to purchase (if known). Be meticulous in filling out every field.

Accuracy is paramount. Any discrepancies or errors could delay the processing of your application or even lead to its denial. Double-check all numbers, dates, and spellings before submitting. If you’re unsure about a question, don’t hesitate to ask a Bank of America representative for clarification.

Step 5: Await a Decision

After submitting your completed application, the waiting game begins. Bank of America will review all the information you’ve provided, along with your credit report, to make a lending decision. The timeframe for a decision can vary.

Often, for online applications, you might receive an instant decision, especially for pre-approvals or if your financial profile is straightforward. For full applications or those requiring more detailed review, it might take a few business days. The bank will typically communicate their decision via email, phone, or mail.

There are three potential outcomes: approval, conditional approval, or denial. An approval means you’ve met all their criteria, and they’re ready to offer you a loan. Conditional approval might mean they need additional documents or clarification before making a final decision. A denial means they’ve decided not to extend credit at this time, and they are legally required to provide you with the reasons for their decision.

Key Factors Bank of America Considers for Approval

Based on my experience reviewing countless loan applications, Bank of America, like other major lenders, assesses several critical factors to determine your eligibility and the terms of your auto loan. Understanding these elements can help you present the strongest possible application.

Your credit score and history are, without a doubt, the most influential factors. A strong credit score (generally 670 and above) indicates a responsible borrower who pays debts on time. Bank of America will look for a consistent payment history, the absence of recent delinquencies, and a reasonable credit utilization ratio. A robust credit profile suggests you are less of a risk.

Another crucial metric is your debt-to-income (DTI) ratio. This ratio compares your total monthly debt payments to your gross monthly income. A lower DTI ratio (typically below 36-40%) shows that you have sufficient income left after paying your existing debts to comfortably afford new car payments. Lenders want to ensure you’re not overextending yourself financially.

Employment stability plays a significant role. Lenders prefer to see a consistent work history, ideally with the same employer for at least two years. This indicates a reliable income source, which directly impacts your ability to make regular loan payments. Frequent job changes or gaps in employment can raise red flags.

While not always mandatory, making a down payment can significantly strengthen your application. A substantial down payment reduces the amount you need to borrow, lowers your monthly payments, and shows the bank you have a financial stake in the vehicle. It also reduces the lender’s risk, as the loan-to-value (LTV) ratio becomes more favorable.

The vehicle details themselves are also considered. The make, model, year, and mileage of the car affect its value and, consequently, the risk associated with the loan collateral. Older vehicles or those with very high mileage might have stricter lending criteria.

Finally, your relationship with Bank of America can sometimes be a subtle advantage. Existing customers with a history of responsible banking (e.g., checking accounts, credit cards) might find the application process smoother, and in some cases, might even qualify for relationship-based discounts on interest rates.

Pro Tips from Us: Strengthening Your Application

To maximize your chances of approval and secure the best terms, here are some pro tips based on years of helping clients navigate auto financing:

- Boost Your Credit: If time allows, dedicate a few months to improving your credit score before applying. Pay down credit card balances, ensure all bills are paid on time, and avoid opening new credit accounts.

- Save for a Down Payment: Aim for at least 10-20% of the car’s purchase price as a down payment. This significantly reduces your loan amount and improves your LTV ratio, making you a more attractive borrower.

- Calculate Your DTI: Know your debt-to-income ratio beforehand. If it’s high, consider paying off some smaller debts before applying for the car loan.

- Be Honest and Thorough: Provide accurate information on your application. Incomplete or misleading information will only cause delays or lead to denial.

Common Mistakes to Avoid Are:

- Applying Everywhere: Don’t apply for multiple car loans simultaneously within a short period. Each "hard" credit inquiry can temporarily ding your credit score. Bunch your applications within a 14-day window to have them count as a single inquiry.

- Ignoring Your Credit Report: Failing to check your credit report for errors before applying can be a costly oversight. Dispute any inaccuracies immediately.

- Overestimating Your Budget: Don’t apply for a loan amount that strains your budget. Be realistic about what you can comfortably afford each month, considering insurance, fuel, and maintenance costs.

- Skipping Pre-Approval: Going to the dealership without pre-approval means you’re negotiating from a weaker position. Get pre-approved first to understand your financing power.

Navigating Interest Rates and Loan Terms

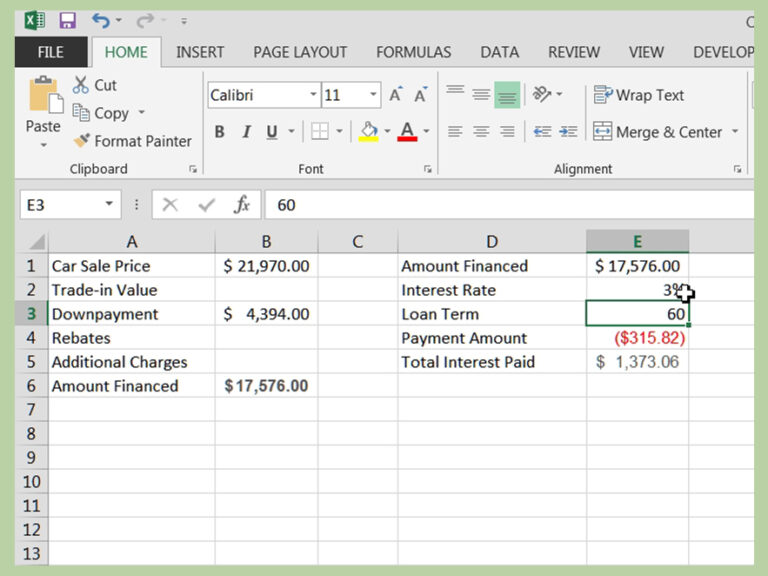

Understanding the intricacies of interest rates and loan terms is vital when you apply for a car loan with Bank of America. These elements directly impact your monthly payments and the total cost of your vehicle over time. A little knowledge here can save you a lot of money.

When you receive a loan offer, you’ll primarily look at the Annual Percentage Rate (APR). The APR is more comprehensive than just the interest rate because it includes not only the interest charged but also any other fees associated with the loan, expressed as a yearly percentage. This gives you a true picture of the annual cost of borrowing. A lower APR means lower overall borrowing costs.

You’ll also need to consider the loan term, which is the duration over which you agree to repay the loan. Common terms range from 36 to 72 months, and sometimes even longer. A shorter loan term typically means higher monthly payments but less interest paid over the life of the loan. Conversely, a longer loan term will result in lower monthly payments but a higher total interest cost. It’s a balance between affordability and long-term cost.

Bank of America generally offers fixed interest rates for their auto loans. This means your interest rate will remain the same for the entire duration of your loan, providing predictable monthly payments. This stability is a significant advantage, shielding you from potential rate increases in the future. offers a deeper dive into how these calculations work and how to find the best rate for your situation.

What if Your Application is Denied?

A car loan denial from Bank of America can be disappointing, but it’s not the end of your car buying journey. Based on my experience, it’s crucial to approach a denial constructively. Understanding the reason and taking corrective steps is key.

Firstly, if your application is denied, Bank of America is legally required to send you an Adverse Action Notice. This notice will explain the specific reasons for the denial. Common reasons include a low credit score, high debt-to-income ratio, insufficient income, or a short credit history. Read this notice carefully, as it provides valuable insight into areas you need to improve.

Once you understand the reason, you can take concrete steps. If it was due to a low credit score, focus on improving it. This involves checking your credit report for errors, paying down existing debts, and ensuring all future payments are made on time. If your debt-to-income ratio was too high, consider reducing existing debts or finding ways to increase your income before reapplying.

It’s also a good idea to speak directly with a Bank of America loan officer. They might be able to offer more personalized advice or suggest alternative solutions, such as applying with a co-signer who has stronger credit. Don’t reapply immediately without addressing the underlying issues; otherwise, you’re likely to face another denial.

After Approval: What Comes Next?

Congratulations! You’ve received approval for your Bank of America car loan. This is an exciting milestone, but there are still a few important steps to complete before you drive off in your new vehicle. Being prepared for these final stages ensures a smooth transition from approval to ownership.

The first step after approval is to meticulously review the loan offer. This includes checking the loan amount, interest rate (APR), loan term, and any associated fees. Make sure all these details match what you discussed and expected. If anything is unclear or seems incorrect, do not hesitate to ask for clarification from your Bank of America representative.

Once you are satisfied with the terms, you will proceed to signing the loan documents. This is a legally binding agreement, so take your time to read through all the paperwork. You’ll sign promissory notes, security agreements, and other disclosures. Ensure you receive copies of all signed documents for your records.

Finally, Bank of America will fund the loan. This means the approved loan amount is disbursed. Depending on whether you’re buying from a dealership or a private seller, the funds might be sent directly to the seller or made available to you. Your loan payments will typically begin a month after the funding date. Set up automatic payments to ensure you never miss a due date.

Pro Tips for a Smooth Car Loan Journey

Securing your Bank of America car loan is a major accomplishment, but the journey doesn’t end there. To truly optimize your car buying experience and ensure financial well-being, here are some pro tips from us, born from years of guiding consumers through this process.

First and foremost, shop around for cars after you’ve secured your pre-approval. This strategy puts you in a powerful position. You know exactly how much you can spend, and you can focus entirely on negotiating the best price for the vehicle itself, rather than being distracted by the dealer’s financing offers. Having your own financing ready gives you the upper hand.

Next, negotiate like a pro. Don’t be afraid to haggle on the car’s price. Research the market value of the vehicle you’re interested in using resources like Kelley Blue Book or Edmunds. Be firm but polite, and be prepared to walk away if the deal isn’t right. Remember, the dealership makes money on both the car and the financing, so separate these two aspects.

Finally, consider additional products carefully. Dealerships often offer extended warranties, GAP insurance, and other add-ons. While some of these might be valuable, many are overpriced or unnecessary. Do your research beforehand and decline anything you don’t genuinely need or that you can get cheaper elsewhere. Adding these to your loan significantly increases your total cost. provides more detailed strategies for dealership interactions.

Frequently Asked Questions (FAQs)

To further assist you in your car loan journey with Bank of America, here are answers to some common questions we encounter:

Can I apply for a car loan with a co-applicant?

Yes, Bank of America allows you to apply for a car loan with a co-applicant. This can be particularly beneficial if your credit score is not as strong as you’d like, or if you wish to combine incomes to qualify for a larger loan amount or better interest rate. The co-applicant’s credit history and income will also be considered.

What are the minimum credit score requirements for a Bank of America car loan?

While Bank of America does not publicly disclose a strict minimum credit score, generally, applicants with good to excellent credit (typically FICO scores of 670 or higher) have the best chances of approval and securing competitive rates. If your score is lower, consider building your credit or applying with a strong co-applicant.

How long does the Bank of America car loan application process take?

For online pre-approvals, you might receive a decision almost instantly. For a full loan application, it can range from a few minutes to a few business days, depending on the completeness of your application and the complexity of your financial profile. Providing all required documents upfront can significantly expedite the process.

Conclusion: Drive Towards Your Financial Goals with Confidence

Navigating the world of auto financing can be complex, but with the right information and a clear strategy, securing a car loan from a reputable institution like Bank of America becomes a manageable and even empowering process. This comprehensive guide has walked you through every critical step, from understanding your options and preparing your documents to the nuances of pre-approval and the final signing.

By leveraging the insights provided, you’re now well-equipped to approach your car loan application with confidence. Remember to prioritize your credit health, prepare meticulously, and utilize Bank of America’s resources effectively. Taking control of your financing journey ensures you not only get the car you desire but also do so on terms that align with your financial well-being.

Ready to take the next step towards owning your dream car? Explore Bank of America’s official auto loan offerings today and begin your application with the knowledge you’ve gained. Your ideal vehicle, backed by solid financing, awaits.