Unlock Your Dream Ride: A Comprehensive Guide to Discovering Used Car Loans

Unlock Your Dream Ride: A Comprehensive Guide to Discovering Used Car Loans Carloan.Guidemechanic.com

Embarking on the journey to purchase a used car can be an exciting prospect. You’re looking for value, reliability, and a vehicle that fits your lifestyle without the hefty price tag of a brand-new model. However, for many, the path to ownership involves securing the right financing. This is where Discover Used Car Loans come into play, offering a gateway to making that pre-owned vehicle a reality.

Navigating the world of automotive financing can feel overwhelming, with countless terms, options, and lenders vying for your attention. But don’t fret! As an expert in vehicle financing, my mission is to demystify the process, providing you with a super comprehensive, in-depth guide designed to empower you with knowledge. We’ll explore everything from understanding loan types to securing the best rates, ensuring you drive away with confidence and a deal that truly benefits you.

Unlock Your Dream Ride: A Comprehensive Guide to Discovering Used Car Loans

This article is your ultimate resource, meticulously crafted to serve as pillar content for anyone seeking to discover used car loans. We’ll cover essential strategies, common pitfalls, and insider tips to help you secure financing that aligns with your financial goals. Get ready to transform confusion into clarity and drive towards a smarter car-buying experience.

Why a Used Car (and a Loan) Makes Smart Financial Sense

Choosing a used car is often a financially savvy decision, offering significant advantages over purchasing a new vehicle. While the allure of a brand-new car is undeniable, the practical benefits of a pre-owned model, especially when financed correctly, are hard to ignore.

The Undeniable Benefits of Opting for a Used Vehicle

One of the most compelling reasons to buy used is depreciation. New cars lose a substantial portion of their value the moment they’re driven off the lot. A used car has already absorbed this initial depreciation hit, meaning your investment retains more of its value over time. This makes a used vehicle a more stable asset from a financial perspective.

Furthermore, insurance costs are typically lower for used cars compared to new ones. Insurers base premiums partly on the vehicle’s value, so a less expensive used car usually translates to more affordable coverage. You might also find a wider variety of models and features available within your budget in the used car market, allowing you to get more car for your money.

The Role of Used Car Loans in Achieving Your Goals

While paying cash for a car is ideal, it’s not a realistic option for most people. This is where used car loans become an indispensable tool. They allow you to spread the cost of a significant purchase over several months or years, making car ownership accessible without depleting your savings or tying up all your liquid assets.

A well-structured used car loan can help you establish or improve your credit history, provided you make timely payments. It’s a strategic financial instrument that bridges the gap between your immediate funds and your desire for reliable transportation. Understanding how to discover used car loans that fit your specific situation is the first step towards a successful purchase.

Understanding the Used Car Loan Landscape

Before diving into applications, it’s crucial to grasp the fundamental concepts of used car financing. Knowing the terminology and the factors that influence your loan terms will put you in a stronger negotiating position and help you make informed decisions.

What Exactly Is a Used Car Loan?

At its core, a used car loan is a secured loan specifically designed to finance the purchase of a pre-owned vehicle. The car itself serves as collateral for the loan, meaning if you fail to make payments, the lender has the right to repossess the vehicle. This security often allows lenders to offer more favorable interest rates compared to unsecured personal loans.

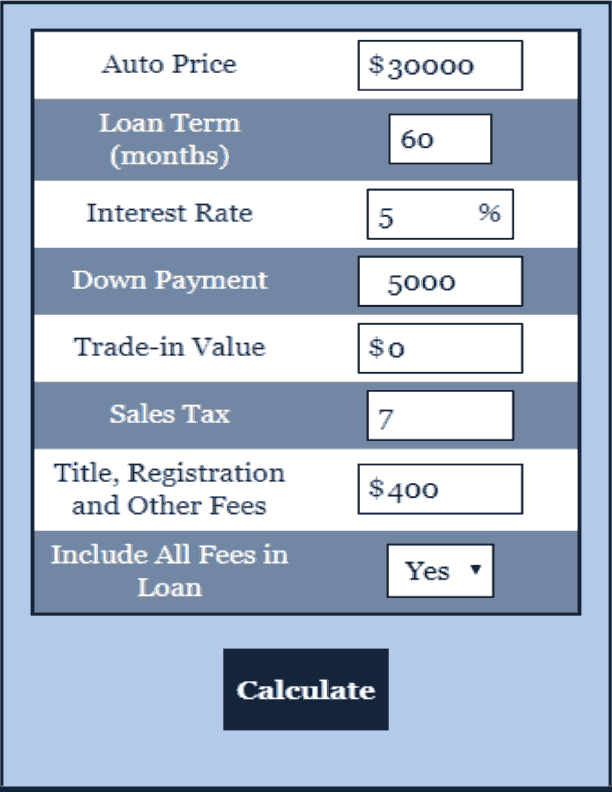

These loans cover the purchase price of the car, minus any down payment you make. They typically come with a fixed interest rate and a set repayment period, known as the loan term, which can range from 24 to 72 months, or sometimes even longer. The longer the term, the lower your monthly payments, but you’ll generally pay more in total interest over the life of the loan.

Key Factors Influencing Your Loan Offer

Several critical elements dictate the kind of used car loan you’ll qualify for and the terms you’ll receive. Understanding these factors is paramount.

- Credit Score: This is arguably the most important factor. A higher credit score (generally above 670) indicates to lenders that you are a responsible borrower, leading to lower interest rates and better terms. A lower score might still allow you to secure financing, but often at a higher rate.

- Debt-to-Income (DTI) Ratio: Lenders look at your DTI ratio to assess your ability to take on new debt. This is the percentage of your gross monthly income that goes towards debt payments. A lower DTI ratio (ideally below 36%) signals less financial risk.

- Loan Term: As mentioned, the length of your repayment period impacts both your monthly payment and the total interest paid. Longer terms mean lower monthly payments but more interest.

- Interest Rate (APR): The interest rate is the cost of borrowing money, expressed as a percentage of the loan amount. The Annual Percentage Rate (APR) includes both the interest rate and any additional fees, giving you a more accurate picture of the total cost of the loan.

Types of Lenders: Where to Discover Used Car Loans

When searching for used car loans, you’ll encounter various types of financial institutions, each with its own advantages.

- Banks: Traditional banks offer competitive rates, especially if you have a strong credit history and an existing relationship with them. They are a reliable option for many borrowers.

- Credit Unions: Often lauded for their customer-centric approach, credit unions are non-profit organizations that typically offer some of the most competitive interest rates. They may also be more flexible with borrowers who have less-than-perfect credit, especially if you’re a member.

- Online Lenders: The digital age has brought a surge of online lenders specializing in auto loans. They often boast quick approval processes and can be a great option for comparing rates from multiple lenders simultaneously. Based on my experience, online platforms can be incredibly efficient, providing pre-approvals in minutes.

- Dealership Financing: Many dealerships offer in-house financing or work with a network of lenders. While convenient, it’s crucial to compare their offers with those you’ve obtained independently. Sometimes, they might mark up interest rates to increase their profit.

The Pre-Approval Advantage: Your Secret Weapon

One of the most powerful tools in your car-buying arsenal is pre-approval for a used car loan. This step, often overlooked, can dramatically simplify your shopping experience and put you in a position of strength.

What is Pre-Approval for a Used Car Loan?

Pre-approval means a lender has reviewed your financial information (credit score, income, debt) and tentatively agreed to lend you a specific amount of money at a particular interest rate, before you’ve even picked out a car. It’s a conditional offer, typically valid for a certain period (e.g., 30-60 days).

It’s important to distinguish pre-approval from pre-qualification. Pre-qualification is usually a soft credit check that gives you an estimate of what you might qualify for, while pre-approval involves a hard credit inquiry and a more definite loan offer.

The Undeniable Benefits of Being Pre-Approved

Having a pre-approval letter in hand offers several significant advantages:

- Clear Budgeting: You’ll know exactly how much you can afford, allowing you to focus your car search on vehicles within your budget. This prevents you from falling in love with a car you can’t realistically finance.

- Stronger Negotiation Power: When you walk into a dealership with pre-approved financing, you become a cash buyer in the eyes of the salesperson. You can focus solely on negotiating the car’s price, rather than getting tangled up in financing discussions that might distract from the vehicle’s cost.

- Less Stressful Shopping: The financial aspect is often the most stressful part of buying a car. With pre-approval, that major hurdle is cleared, allowing you to enjoy the car-shopping experience more.

- Benchmark for Dealership Offers: Your pre-approval acts as a benchmark. If a dealership offers you a higher interest rate, you know you have a better alternative, giving you leverage to ask them to beat or match your pre-approved rate.

How to Get Pre-Approved for a Used Car Loan

The process for pre-approval is straightforward:

- Gather Your Documents: You’ll typically need proof of income (pay stubs, tax returns), proof of residence (utility bill), identification (driver’s license), and possibly your Social Security number.

- Contact Lenders: Reach out to banks, credit unions, and online lenders. It’s advisable to apply to 2-3 different institutions within a short timeframe (usually 14-45 days) to minimize the impact on your credit score, as multiple hard inquiries for the same type of loan are often grouped together.

- Review Offers: Compare the loan amounts, interest rates, APRs, and terms from each lender. Don’t just look at the monthly payment; consider the total cost of the loan.

Common mistakes to avoid are applying for pre-approval too early if you’re not ready to buy, as the offer might expire. Also, avoid only applying to one lender; comparison shopping is crucial to discover used car loans with the best rates.

Navigating the Application Process for Used Car Loans

Once you’ve identified a vehicle and are ready to finalize your financing, understanding the full application process is key. This stage moves beyond pre-approval to securing the actual loan for your chosen car.

Step-by-Step Guide to Securing Your Loan

- Choose Your Car: Select the specific used car you intend to buy. Its age, mileage, and make/model can all influence the lender’s decision and the interest rate.

- Provide Vehicle Information: Lenders will need details about the car, including its Vehicle Identification Number (VIN), mileage, and potentially a vehicle history report. This helps them assess the car’s value and risk.

- Submit Final Application: If you have pre-approval, this step often involves confirming the details of the vehicle with your pre-approved lender. If not, you’ll submit a full application, including all your financial and personal information.

- Await Approval and Finalize Terms: The lender will conduct a final review. Upon approval, you’ll receive the official loan documents outlining the interest rate, APR, loan term, and monthly payment.

- Sign and Drive: Carefully read all documents before signing. Once signed, the funds are disbursed, and you’re ready to take ownership of your used car.

Understanding Interest Rates and APR

It’s vital to differentiate between the interest rate and the Annual Percentage Rate (APR). The interest rate is simply the cost of borrowing money. The APR, however, is a more comprehensive measure of the loan’s cost, as it includes the interest rate plus any additional fees charged by the lender (e.g., origination fees, processing fees). Pro tips from us: Always compare APRs when evaluating loan offers, as it provides the most accurate reflection of the total borrowing cost.

Factors Impacting Your Approval and Rate

Beyond your credit score and DTI, other elements can influence your loan outcome:

- Loan-to-Value (LTV) Ratio: This compares the loan amount to the car’s market value. Lenders prefer a lower LTV, meaning you’re borrowing less relative to the car’s worth. A significant down payment helps reduce LTV.

- Age and Mileage of the Car: Older cars or those with very high mileage are often seen as riskier by lenders, potentially leading to higher interest rates or stricter loan terms. Some lenders have limits on the age or mileage they will finance.

- Employment Stability: Lenders prefer borrowers with a stable employment history, as it indicates a consistent income source for repayment.

Pro Tips for a Smooth Application Process

- Be Prepared: Have all required documents organized and ready. This speeds up the process significantly.

- Be Honest: Provide accurate information. Misrepresenting facts can lead to denial or even legal issues.

- Read the Fine Print: Don’t rush through the loan agreement. Understand every clause, especially regarding early payoff penalties or late payment fees.

- Negotiate: Don’t be afraid to negotiate the interest rate or terms, especially if you have multiple offers. Many lenders have some flexibility.

Special Considerations for Used Car Loans

Not all borrowers or vehicles fit neatly into standard loan categories. Understanding these special scenarios is crucial for a truly comprehensive approach to used car financing.

Bad Credit Used Car Loans: Strategies for Success

Having a low credit score doesn’t automatically disqualify you from getting a used car loan, but it does present unique challenges. Lenders view borrowers with poor credit as higher risk, leading to higher interest rates.

- Strategies for Securing a Loan:

- Increase Your Down Payment: A larger down payment reduces the loan amount and the lender’s risk, making you a more attractive borrower.

- Find a Co-Signer: A co-signer with good credit can significantly improve your chances of approval and help secure a better interest rate. Remember, they are equally responsible for the loan.

- Work with Subprime Lenders: These lenders specialize in working with borrowers who have lower credit scores, though their interest rates will be considerably higher.

- Improve Your Credit First: If possible, take some time to improve your credit score before applying. Pay down existing debts, dispute errors on your credit report, and make all payments on time. For a deeper dive into improving your credit score, check out our comprehensive guide on .

Private Party Used Car Loans: Navigating the Unique Challenges

Buying a used car from a private seller can often yield a better price than buying from a dealership. However, financing a private party purchase can be more complex.

- Challenges: Many traditional lenders are hesitant to finance private party sales due to increased risk and less oversight compared to dealership transactions. The car isn’t subject to the same inspections or warranties.

- How to Secure One:

- Specialized Lenders: Some banks and credit unions specifically offer private party auto loans. You’ll likely need to provide the lender with the vehicle’s title, a bill of sale, and proof of insurance.

- Collateral Requirements: The lender will typically require a clean title and a valuation of the car (e.g., through Kelley Blue Book or NADA guides) to ensure it’s worth the loan amount.

- Pre-Purchase Inspection: Always insist on a pre-purchase inspection by an independent mechanic. This protects you from hidden issues and reassures the lender about the car’s condition.

Older Used Car Loans: Age Restrictions and Higher Rates

While used car loans are available for a wide range of vehicles, financing for very old cars (e.g., over 10-12 years old) or those with extremely high mileage can be difficult.

- Why the Difficulty: Lenders perceive older vehicles as having a higher risk of mechanical failure and lower resale value, which impacts their collateral value.

- Potential Outcomes: If approved, you might face significantly higher interest rates and shorter loan terms to mitigate the lender’s risk. Some lenders have strict cut-offs for vehicle age and mileage.

The Importance of a Down Payment

Making a down payment on your used car loan is one of the smartest financial moves you can make.

- Why it’s Crucial:

- Reduces Loan Amount: Less money borrowed means lower monthly payments and less interest paid over the life of the loan.

- Builds Equity Faster: You start with equity in the car, protecting you from becoming "upside down" (owing more than the car is worth), especially due to depreciation.

- Improves Loan Terms: Lenders view a substantial down payment favorably, often leading to better interest rates.

- How Much is Ideal? While there’s no magic number, a down payment of 10-20% of the car’s purchase price is generally recommended for used cars. If possible, aim for more.

- Saving Strategies: Start saving early, set a specific goal, and consider automatic transfers to a dedicated savings account.

Beyond the Loan: Protecting Your Investment

Securing a used car loan is just one part of the equation. To truly make a smart purchase, you need to protect your investment and ensure the vehicle you’re financing is sound.

The Value of Vehicle History Reports

Before committing to any used car, obtaining a comprehensive vehicle history report is non-negotiable. Services like CarFax and AutoCheck provide invaluable insights.

- What They Reveal: These reports detail a car’s past, including accident history, salvage titles, odometer discrepancies, flood damage, recall information, service records, and the number of previous owners.

- Why It Matters: A clean history report gives you peace of mind, while a problematic one is a clear warning sign. It helps prevent you from financing a car with hidden issues that could lead to costly repairs down the line.

Don’t Skip the Pre-Purchase Inspection

Even with a clean history report, a professional pre-purchase inspection (PPI) by an independent mechanic is essential.

- What a PPI Does: An experienced mechanic will thoroughly examine the vehicle for mechanical issues, structural damage, fluid leaks, and any other problems that might not be visible to the untrained eye or listed in a history report.

- Why It’s Crucial: This independent assessment can uncover potential problems, give you leverage for negotiation, or even save you from buying a lemon. It’s a small investment that can prevent huge future expenses.

Extended Warranties and GAP Insurance: To Buy or Not to Buy?

These add-ons are often presented at the point of sale. Understanding their purpose is key to making an informed decision.

- Extended Warranties: These cover repairs after the manufacturer’s original warranty expires.

- Pros: Can provide peace of mind and protect against unexpected repair costs, especially for older or high-mileage vehicles.

- Cons: Can be expensive, and coverage might have limitations or exclusions. Always read the fine print. Consider the car’s reliability ratings and your risk tolerance.

- Guaranteed Asset Protection (GAP) Insurance: This covers the difference between what you owe on your used car loan and the car’s actual cash value if it’s totaled or stolen.

- Pros: Highly recommended, especially if you’ve made a small down payment or financed a car that depreciates quickly. It protects you from owing money on a car you no longer possess.

- Cons: It’s an additional cost, and some insurance policies might already offer similar coverage. Check with your auto insurance provider first.

Managing Your Used Car Loan & Future Options

Once you’ve secured your used car loan and are happily driving your pre-owned vehicle, your financial journey isn’t over. Effective loan management and awareness of future options are key to long-term financial health.

Making Timely Payments: The Foundation of Good Credit

This might seem obvious, but consistently making your loan payments on time is paramount.

- Impact on Credit: Every on-time payment helps build a positive credit history, which is crucial for future borrowing (mortgages, personal loans, etc.). Late payments, even by a few days, can negatively impact your credit score and incur fees.

- Avoid Penalties: Late payment fees can add up quickly, increasing the overall cost of your loan. Set up automatic payments or calendar reminders to ensure you never miss a due date.

Understanding Your Loan Statements

Your monthly loan statements aren’t just a bill; they’re a detailed breakdown of your loan’s progress.

- Key Information: Look for the principal balance remaining, the amount of interest paid, the amount applied to the principal, and any fees incurred.

- Tracking Progress: Regularly reviewing your statements helps you track your repayment progress and ensures accuracy. If anything looks incorrect, contact your lender immediately.

Refinancing a Used Car Loan: When and Why It Makes Sense

Refinancing means taking out a new loan to pay off your existing used car loan, often with better terms.

- When to Consider Refinancing:

- Improved Credit Score: If your credit score has significantly improved since you first took out the loan, you might qualify for a lower interest rate.

- Lower Interest Rates: If market interest rates have dropped, refinancing could save you money.

- Change in Financial Situation: If you need to lower your monthly payments, you might refinance for a longer term (though this means more interest overall). Conversely, if you want to pay off the loan faster, you could refinance to a shorter term.

- Benefits: A lower interest rate means less money paid over the life of the loan. Lower monthly payments can free up cash flow.

- Process: Similar to applying for a new loan, you’ll shop around with different lenders, provide financial details, and secure a new loan to pay off the old one.

Paying Off Your Loan Early: Pros and Cons

While it might sound appealing to eliminate debt quickly, paying off your used car loan early has both advantages and disadvantages.

- Pros:

- Save on Interest: The most significant benefit is reducing the total amount of interest you pay.

- Debt Freedom: You’ll free up cash flow that was going towards car payments and eliminate a monthly obligation.

- Improved DTI: A lower DTI ratio can improve your eligibility for other loans in the future.

- Cons:

- Opportunity Cost: The money you use to pay off the loan early could potentially be invested elsewhere for a higher return.

- Prepayment Penalties: Some loans have penalties for early repayment, though these are less common with auto loans than with other types of financing. Always check your loan agreement.

- Impact on Credit Mix: If this is your only installment loan, paying it off might slightly reduce your credit mix, though the impact is usually minor if you have other credit accounts.

Considering whether a new or used car is right for you? Read our detailed comparison: .

Your Journey to a Great Used Car Loan Starts Here

Navigating the landscape of used car loans doesn’t have to be a daunting task. By understanding the intricacies of financing, leveraging pre-approval, and making informed decisions throughout the process, you can secure a loan that aligns perfectly with your financial situation and car-buying aspirations. From deciphering interest rates to exploring options for bad credit, every piece of knowledge you gain empowers you to make a smarter choice.

Remember, the goal isn’t just to get a loan, but to discover used car loans that offer the most favorable terms, protect your investment, and ultimately lead to a positive ownership experience. Take the time to research, compare offers, and ask questions. Your due diligence will pay off, ensuring you drive away not just with a great car, but with a smart financial decision under your belt.

Ready to take the next step? Use the insights from this guide to confidently explore your financing options. Your dream used car is within reach, and with the right loan, it can become a reality. For more detailed information on consumer financial products, including auto loans, visit a trusted external source like the Consumer Financial Protection Bureau (CFPB) website. Happy driving!