Unlock Your Dream Ride: A Deep Dive into First Federal Car Loan Rates

Unlock Your Dream Ride: A Deep Dive into First Federal Car Loan Rates Carloan.Guidemechanic.com

Embarking on the journey to purchase a new or used vehicle is an exciting prospect. However, the excitement can quickly turn into apprehension when faced with the complexities of auto financing. Among the myriad of lending options available, First Federal Car Loan Rates often stand out as a highly attractive pathway for savvy consumers. But what exactly makes them so compelling, and how can you navigate the landscape to secure the best possible deal?

This comprehensive guide is meticulously crafted to demystify everything you need to know about securing a car loan through a First Federal credit union. We’ll explore the unique advantages, dissect the factors influencing your rate, and provide actionable strategies to ensure you drive away with confidence, knowing you’ve made an informed financial decision. Prepare to become an expert in auto financing through federal credit unions.

Unlock Your Dream Ride: A Deep Dive into First Federal Car Loan Rates

Understanding the Foundation: What Are Car Loan Rates and Why Do They Matter?

Before we delve into the specifics of First Federal options, it’s crucial to grasp the fundamental concept of car loan rates. Essentially, a car loan rate is the cost you pay to borrow money for your vehicle purchase, expressed as a percentage of the loan amount. This percentage directly impacts your monthly payment and, more importantly, the total amount of interest you’ll pay over the life of the loan.

The rate you secure can mean the difference of hundreds, even thousands, of dollars over several years. It’s not just about the monthly affordability; it’s about the overall financial burden. A lower interest rate means more of your payment goes towards the principal balance, helping you build equity in your vehicle faster and reducing your total expenditure.

Deconstructing the Loan Rate: APR vs. Interest Rate

When discussing car loan rates, you’ll often encounter two key terms: "interest rate" and "Annual Percentage Rate" (APR). While seemingly similar, there’s a critical distinction. The interest rate is solely the cost of borrowing the principal amount.

The APR, on the other hand, provides a more holistic view of the loan’s true cost. It includes the interest rate plus any additional fees associated with the loan, such as origination fees or processing charges. Always focus on the APR when comparing loan offers, as it gives you the most accurate picture of what you’ll actually pay.

The Federal Credit Union Difference: Why Look Beyond Traditional Banks?

When it comes to securing a car loan, many consumers automatically turn to large commercial banks or dealership financing. However, a significant number of people are missing out on potentially better deals by overlooking federal credit unions. These institutions operate under a fundamentally different model, which often translates into tangible benefits for their members.

Federal credit unions are non-profit financial cooperatives owned by their members, not shareholders. This member-centric approach means their primary goal isn’t to maximize profits, but rather to provide valuable financial services, including loans, at competitive rates. This core difference is a game-changer for borrowers.

The Undeniable Advantages of Choosing a Federal Credit Union

Based on my extensive experience in the financial sector, I’ve observed several consistent advantages that federal credit unions offer over traditional banking institutions. These benefits directly impact your borrowing experience and, ultimately, your wallet.

Firstly, and perhaps most significantly, federal credit unions typically offer lower interest rates on auto loans. Because they are not driven by profit motives, they can pass on savings to their members in the form of more favorable rates. This competitive edge is a primary reason why so many people seek out First Federal Car Loan Rates.

Secondly, the personalized customer service at federal credit unions is often unparalleled. You’re not just an account number; you’re a member-owner. This fosters a more supportive and understanding environment, especially when discussing complex financial products like car loans. They are often more willing to work with members to find flexible solutions.

Thirdly, federal credit unions often have more flexible lending criteria. While credit scores are always a factor, they may take a more holistic view of your financial situation, especially if you have an established relationship with them. This can be particularly beneficial for individuals with less-than-perfect credit histories.

Demystifying First Federal Car Loan Rates: What to Expect

When you approach a First Federal credit union for an auto loan, you can generally expect a transparent and member-focused process. Their rates are designed to be competitive, often benchmarked against the best available in the market, but with the added benefit of their non-profit structure.

You’ll find that First Federal Car Loan Rates are typically clearly advertised, often with tiered pricing based on credit score, loan term, and vehicle age (new vs. used). This transparency empowers you to understand what rate you might qualify for before even applying.

Membership Eligibility: The Gateway to Better Rates

To access the attractive rates and services of a federal credit union, you first need to become a member. Membership requirements vary by institution, but they generally revolve around a "field of membership." This could be based on:

- Location: Living, working, or worshipping in a specific geographic area.

- Employer: Working for a particular company or organization.

- Association: Being a member of a specific group, club, or association.

- Family Ties: Having a family member who is already a member.

Many federal credit unions also offer easy ways to join, such as by making a small donation to an affiliated charity or organization. Don’t let membership requirements deter you; a quick inquiry will often reveal a simple pathway to becoming a member and unlocking those advantageous First Federal Car Loan Rates.

The Application Process: Your Roadmap to Approval

Securing a car loan, whether from a federal credit union or another lender, involves a structured application process. Understanding each step can help you prepare effectively and increase your chances of approval for the best possible rate.

The process typically begins with gathering necessary documentation. This usually includes proof of identity (driver’s license, Social Security card), proof of income (pay stubs, tax returns), and proof of residence (utility bill). Having these documents organized beforehand streamlines the entire procedure.

Next, you’ll complete a loan application, which allows the credit union to assess your financial health. This assessment includes reviewing your credit report and score, your debt-to-income ratio, and your employment history. The more complete and accurate your information, the smoother the process.

Pro tips from us: Consider getting pre-approved for a loan before you even step foot in a dealership. Pre-approval gives you a clear understanding of your borrowing power and interest rate, transforming you into a cash buyer. This leverage can significantly improve your negotiation position on the vehicle price itself.

Key Factors That Shape Your First Federal Car Loan Rate

While federal credit unions are known for competitive rates, your individual rate will still be influenced by several critical factors. Understanding these elements is essential for strategizing how to secure the most favorable First Federal Car Loan Rates for your specific situation.

1. Your Credit Score: The Cornerstone of Lending

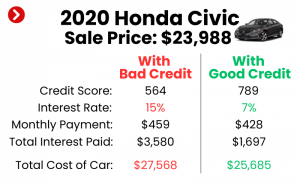

Your credit score is arguably the most significant factor lenders consider. It’s a numerical representation of your creditworthiness, reflecting your history of borrowing and repayment. A higher credit score signals lower risk to lenders, which typically translates to lower interest rates.

For instance, someone with an excellent credit score (typically 760+) will almost always qualify for the most attractive First Federal Car Loan Rates. Conversely, a lower score might result in a higher rate to compensate the lender for the perceived increased risk. If your score isn’t where you want it to be, focusing on improving it before applying can save you a substantial amount of money. For a deeper dive into improving your credit score, check out our comprehensive guide on .

2. The Loan Term: Balancing Monthly Payments and Total Cost

The loan term refers to the length of time you have to repay the loan, usually expressed in months (e.g., 36, 48, 60, 72, or even 84 months). While a longer loan term will result in lower monthly payments, it almost always means you’ll pay more in total interest over the life of the loan.

Common mistakes to avoid are extending the loan term simply to achieve a lower monthly payment without considering the long-term financial implications. A shorter loan term, while demanding higher monthly payments, can significantly reduce the total interest paid and help you pay off your vehicle faster. Federal credit unions offer a range of terms, allowing you to choose what best fits your budget and financial goals.

3. Your Down Payment: Reducing Risk and Rates

Making a substantial down payment on your vehicle is one of the most effective ways to lower your interest rate and improve your loan terms. A larger down payment reduces the amount you need to borrow, which in turn reduces the lender’s risk. This lower risk profile often translates into a more favorable First Federal Car Loan Rate.

Furthermore, a significant down payment can help prevent you from being "upside down" on your loan, a situation where you owe more than the car is worth. This provides a crucial buffer against depreciation and offers greater financial flexibility down the line.

4. Debt-to-Income Ratio (DTI): A Measure of Your Capacity

Your debt-to-income (DTI) ratio is a crucial metric lenders use to assess your ability to manage monthly payments. It’s calculated by dividing your total monthly debt payments by your gross monthly income. A lower DTI indicates that you have more disposable income available to comfortably handle new loan payments.

Federal credit unions, like other lenders, prefer borrowers with a lower DTI. A high DTI might signal that you are overextended financially, potentially leading to a higher interest rate or even loan denial. Proactively managing your existing debt before applying for a car loan can positively impact your DTI.

5. Vehicle Type and Age: New vs. Used Considerations

The type and age of the vehicle you intend to purchase also play a role in determining your interest rate. New cars typically qualify for slightly lower interest rates than used cars. This is because new cars generally have a predictable depreciation schedule and are considered less risky by lenders due to manufacturer warranties and lack of prior ownership issues.

Used cars, while often more affordable upfront, can come with slightly higher rates due to factors like their age, mileage, and potential for unforeseen mechanical issues. However, many federal credit unions offer very competitive First Federal Car Loan Rates for both new and used vehicles, making them an excellent option regardless of your preference.

Beyond the Rate: What Else to Look for in a First Federal Car Loan

While securing a low interest rate is paramount, it’s not the only aspect to consider when evaluating a car loan offer. A truly comprehensive assessment involves looking at the entire loan package.

- Fees and Charges: Always inquire about any potential fees, such as origination fees, application fees, or documentation fees. Federal credit unions are generally known for transparent fee structures, often with fewer hidden costs than some other lenders.

- Prepayment Penalties: Ideally, you want a loan that allows you to pay it off early without incurring any penalties. This flexibility can save you significant interest if you find yourself in a position to pay off the loan ahead of schedule. Most federal credit unions do not impose prepayment penalties.

- Customer Service and Flexibility: Consider the overall experience. How responsive and helpful is the loan officer? Do they offer flexible payment options or grace periods in case of unforeseen circumstances? The member-centric philosophy of federal credit unions often shines in these areas.

- Insurance Requirements: Lenders typically require you to carry comprehensive and collision insurance on your financed vehicle. Ensure you understand these requirements and factor the insurance cost into your overall budget.

Proactive Strategies to Secure the Best First Federal Car Loan Rates

Armed with this knowledge, you can now take proactive steps to position yourself for the most favorable First Federal Car Loan Rates. It’s about being prepared and strategic.

- Build and Maintain Excellent Credit: This cannot be emphasized enough. Pay all your bills on time, keep your credit utilization low, and regularly review your credit report for errors. A strong credit profile is your golden ticket to the lowest rates.

- Save for a Substantial Down Payment: Aim for at least 10-20% of the vehicle’s purchase price. Not only does this reduce your loan amount and interest, but it also provides immediate equity in your car.

- Shop Around (Even Within Federal Credit Unions): Don’t assume the first federal credit union you inquire with offers the absolute best rate. While they are generally competitive, rates can still vary. Apply for pre-approval at 2-3 different federal credit unions to compare offers and ensure you’re getting the most competitive First Federal Car Loan Rates.

- Consider a Co-signer (If Necessary): If your credit score is less than ideal, a co-signer with excellent credit can significantly improve your chances of approval and help you secure a lower rate. Ensure both parties understand the responsibilities involved.

- Explore Refinancing Options: If you already have a car loan with a higher interest rate, especially from a traditional bank or dealership, consider refinancing with a federal credit union. Many offer very attractive refinancing rates. We’ve covered the ins and outs in our article: .

Budgeting for Your Car Loan: A Holistic Approach

Securing a great First Federal Car Loan Rate is only one part of smart car ownership. It’s crucial to budget for the total cost of owning a vehicle, not just the monthly loan payment.

Think beyond the loan:

- Insurance: Premiums can vary wildly based on your vehicle, location, age, and driving record.

- Fuel: Factor in your daily commute and weekend trips.

- Maintenance: Regular oil changes, tire rotations, and unexpected repairs are inevitable.

- Registration and Taxes: Annual fees and initial sales tax can add up.

A common guideline is the "20/4/10 rule": make a 20% down payment, finance the car for no more than four years, and keep your total monthly car expenses (payment, insurance, maintenance) under 10% of your gross income. While this is a guideline, it serves as an excellent starting point for responsible financial planning. For more general guidance on smart financial decisions, the Consumer Financial Protection Bureau offers excellent resources: https://www.consumerfinance.gov/

Common Misconceptions About Car Loans (and First Federal CUs)

Let’s debunk a few myths that often lead people astray in their car buying journey:

- Myth 1: Dealership financing is always the easiest and best option. While convenient, dealership financing often includes markups on interest rates. They might present it as a "one-stop shop," but comparing offers from federal credit unions beforehand often reveals better deals.

- Myth 2: You need perfect credit to get a good rate from a federal credit union. While excellent credit yields the best rates, federal credit unions are often more willing to work with members with average or even slightly below-average credit, especially if you have a relationship with them. Their member-centric approach can lead to more flexible solutions.

- Myth 3: All federal credit unions offer the exact same rates. While generally competitive, rates can vary slightly between different federal credit unions based on their financial health, specific promotions, and internal policies. Always compare offers.

Conclusion: Drive Away with Confidence

Navigating the world of car loans can feel overwhelming, but by understanding the unique advantages and processes associated with First Federal Car Loan Rates, you empower yourself to make a truly informed decision. Federal credit unions offer a compelling alternative to traditional lenders, providing competitive rates, personalized service, and a member-focused approach that can save you significant money over the life of your loan.

By taking the time to improve your credit, save for a down payment, and shop around for the best terms, you’re not just buying a car; you’re making a smart financial investment. So, before you sign on the dotted line, remember the power of the federal credit union. Start your journey today by exploring the First Federal Car Loan Rates available in your community. Your dream car, financed intelligently, awaits.