Unlock Your Dream Ride: A Deep Dive into Justice Federal Credit Union Car Loan Rates

Unlock Your Dream Ride: A Deep Dive into Justice Federal Credit Union Car Loan Rates Carloan.Guidemechanic.com

Securing the right financing for your next vehicle is often as crucial as choosing the car itself. In a world brimming with lending options, credit unions like Justice Federal Credit Union (JFCU) frequently stand out for their member-centric approach and competitive rates. For federal employees, retirees, and their families, understanding Justice Federal Credit Union car loan rates isn’t just about finding a good deal; it’s about leveraging a trusted institution dedicated to financial well-being.

This comprehensive guide will unravel everything you need to know about JFCU car loans. We’ll explore their unique advantages, dissect the factors influencing your rate, walk you through the application process, and provide expert tips to ensure you secure the best possible financing for your new or used vehicle. Our ultimate goal is to equip you with the knowledge to make an informed decision, driving away with confidence and a loan that truly fits your budget.

Unlock Your Dream Ride: A Deep Dive into Justice Federal Credit Union Car Loan Rates

Understanding Justice Federal Credit Union: Your Trusted Partner in Auto Financing

Before we delve into the specifics of car loan rates, it’s essential to understand who Justice Federal Credit Union is and why they are a significant player in the auto financing landscape. JFCU is a not-for-profit financial cooperative, meaning it’s owned by its members, not external shareholders. This fundamental difference shapes its entire operational philosophy, prioritizing member benefits over profit margins.

JFCU primarily serves employees and retirees of the Department of Justice, Department of Homeland Security, and related agencies, along with their families. This specific community focus allows them to tailor services and products, including car loans, to the unique needs of their membership. Being a member means you’re part owner, and that often translates to better rates, lower fees, and a more personalized banking experience compared to traditional banks.

Diving Deep into Justice Federal Credit Union Car Loan Rates: What to Expect

When it comes to car loans, JFCU consistently aims to offer highly competitive rates, often lower than those found at large commercial banks. This isn’t just a marketing claim; it’s a direct benefit of their credit union structure. Instead of distributing profits to shareholders, credit unions reinvest them back into the organization through better rates on loans and higher yields on savings.

However, it’s important to remember that the specific Justice Federal Credit Union car loan rate you receive will depend on several individual factors. These aren’t arbitrary figures but carefully calculated assessments of risk and your financial profile. Understanding these variables upfront can significantly impact your final interest rate and, consequently, your monthly payment and total cost of the loan.

Types of Auto Loans Offered by JFCU

Justice Federal Credit Union provides a range of auto loan options designed to meet diverse member needs. Whether you’re eyeing a brand-new model or a reliable pre-owned vehicle, they likely have a financing solution for you. Understanding these options is the first step towards choosing the right loan.

New Car Loans

For those seeking the latest models straight from the dealership, JFCU offers competitive new car loans. These loans typically come with the lowest interest rates due to the vehicle’s higher value and lower depreciation risk for the lender. Loan terms can vary, often extending up to 84 months, allowing for flexible payment options.

When considering a new car loan, JFCU looks at factors like the vehicle’s MSRP, your creditworthiness, and the loan term. They aim to make the process smooth, often working directly with dealerships or providing pre-approval so you can shop with confidence. This helps you negotiate from a position of strength, knowing your financing is already secured.

Used Car Loans

Purchasing a used car can be a smart financial move, and JFCU supports this with tailored used car loan options. While rates for used cars might be slightly higher than for new cars, JFCU still strives to keep them very competitive. The age and mileage of the vehicle often play a role in determining the specific rate and maximum loan term available.

JFCU understands that used vehicles come in all shapes and conditions. They typically finance vehicles up to a certain age, often 7-10 years old, and with specific mileage limits. It’s always best to confirm these criteria directly with JFCU before you start your used car search.

Auto Loan Refinancing

Perhaps you already have a car loan but are looking for a better deal. JFCU’s auto loan refinancing option could be a game-changer. Refinancing allows you to replace your current car loan with a new one, ideally at a lower interest rate, with a different term, or both. This can significantly reduce your monthly payments or the total interest paid over the life of the loan.

Common reasons to refinance include an improved credit score since you first took out the loan, lower market interest rates, or a desire to change your loan term to better suit your current financial situation. Based on my experience, many individuals overlook the potential savings from refinancing. A quick call to JFCU can determine if you’re eligible for a better rate and how much you could save.

The Application Process for a JFCU Car Loan: A Step-by-Step Guide

Navigating the loan application process can sometimes feel overwhelming, but JFCU aims to make it as straightforward as possible for its members. Understanding each step can help you prepare and ensure a smooth experience.

Step 1: Membership Eligibility and Application

First and foremost, you must be a member of Justice Federal Credit Union to apply for a loan. If you’re not yet a member, you’ll need to join, which typically involves opening a savings account with a small deposit. Membership is usually open to employees and retirees of specific federal agencies and their family members.

Step 2: Getting Pre-Approved

Based on my experience, getting pre-approved is one of the smartest moves you can make before stepping foot in a dealership. Pre-approval from JFCU provides you with a clear understanding of how much you can borrow and at what interest rate, before you even choose a car. This empowers you to negotiate confidently, focusing on the car’s price rather than being swayed by dealership financing offers.

To get pre-approved, you’ll typically provide information about your income, employment history, and financial obligations. JFCU will perform a credit check to assess your creditworthiness.

Step 3: Submitting Your Full Application

Once you’ve found your dream car, you’ll finalize your loan application. This involves providing specific details about the vehicle, such as its VIN, make, model, and mileage. You might also need to provide additional documentation to verify your income or identity.

JFCU offers several convenient ways to apply: online through their secure portal, over the phone with a loan officer, or in person at one of their branches. Choose the method that best suits your comfort and schedule.

Step 4: Loan Approval and Funding

After submitting all necessary information, JFCU will review your application. If approved, they will provide you with the final loan terms, including your interest rate, monthly payment, and total loan amount. Funds can then be disbursed directly to the dealership or, in the case of refinancing, used to pay off your existing loan. The entire process is designed for efficiency, getting you behind the wheel faster.

Key Factors That Influence Your Justice Federal Credit Union Car Loan Rate

Understanding what goes into determining your car loan rate is crucial for securing the best possible deal. JFCU, like any lender, assesses various factors to determine the risk associated with lending you money. The lower the perceived risk, the lower your interest rate will likely be.

Credit Score

Your credit score is arguably the most significant factor influencing your Justice Federal Credit Union car loan rate. This three-digit number, primarily FICO or VantageScore, reflects your creditworthiness based on your payment history, amounts owed, length of credit history, new credit, and credit mix. A higher score (generally above 700) indicates a lower risk to lenders and typically qualifies you for the most favorable rates.

Individuals with excellent credit scores demonstrate a consistent history of responsible borrowing and repayment. Conversely, lower credit scores often result in higher interest rates, as lenders compensate for the increased risk of default. It’s always a good idea to check your credit score and report before applying for any loan.

Loan Term (Length of Loan)

The loan term, or the length of time you have to repay the loan, also plays a critical role. Shorter loan terms, such as 36 or 48 months, generally come with lower interest rates because the lender’s money is tied up for a shorter period. While monthly payments will be higher, the total interest paid over the life of the loan will be significantly less.

Longer loan terms, such as 72 or 84 months, result in lower monthly payments, making the car more "affordable" on a month-to-month basis. However, you’ll pay more in total interest over the life of the loan, and the interest rate itself might be slightly higher due to the extended risk for the lender. Pro tips from us: Balance affordability with the total cost; don’t just focus on the lowest monthly payment.

Down Payment Amount

Making a substantial down payment on your vehicle can significantly improve your car loan rate. A larger down payment reduces the amount you need to borrow, thereby lowering the lender’s risk. It also demonstrates your financial commitment to the purchase.

When you put down a significant sum, you immediately gain equity in the vehicle, which can be advantageous if you ever need to sell it or if its value depreciates quickly. Lenders view this positively, often rewarding borrowers with better rates for their reduced exposure.

Debt-to-Income (DTI) Ratio

Your debt-to-income (DTI) ratio is another key metric JFCU will consider. This ratio compares your total monthly debt payments to your gross monthly income. A lower DTI ratio indicates that you have more disposable income available to comfortably manage your new car loan payments, signaling less risk to the lender.

Lenders prefer a DTI ratio that is generally below 43%, though this can vary. A high DTI suggests you might be overextended financially, potentially making it harder to secure the most competitive Justice Federal Credit Union car loan rates.

Vehicle Specifics (New vs. Used, Age, Mileage)

The characteristics of the vehicle itself also influence the loan rate. New cars generally command lower interest rates than used cars because they hold their value better initially and present less risk of mechanical issues. For used cars, factors like the vehicle’s age, mileage, and overall condition will be taken into account.

Older vehicles or those with very high mileage are considered higher risk due to potential maintenance issues and faster depreciation, which can lead to slightly higher interest rates. JFCU will assess the vehicle’s market value to ensure the loan amount is appropriate.

Comparing JFCU Rates with Other Lenders

While Justice Federal Credit Union offers competitive rates, it’s always wise to compare their offerings with other lenders. This due diligence ensures you’re getting the absolute best deal available.

Credit unions, in general, often beat out large commercial banks on auto loan rates due to their non-profit structure. Banks are typically profit-driven, which can translate to higher interest rates for borrowers. Dealership financing can be convenient, but their rates might be inflated to include commissions or other fees, even if they advertise "special" rates.

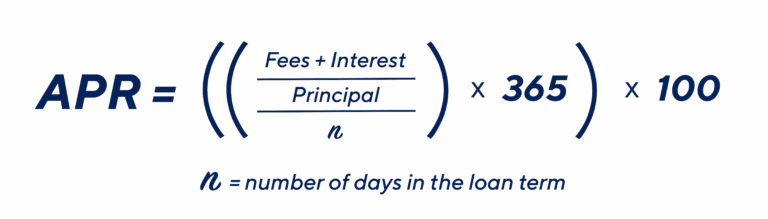

When comparing, always look at the Annual Percentage Rate (APR), which includes the interest rate plus any fees, giving you a truer picture of the total cost of borrowing. Don’t be afraid to get quotes from multiple sources – your local bank, other credit unions, and JFCU – before making a decision. For a broader perspective on current national auto loan trends, you might consult a trusted financial resource like the Consumer Financial Protection Bureau (CFPB) or Bankrate, which often publish aggregated rate data.

Common Mistakes to Avoid When Applying for a Car Loan

Applying for a car loan can be straightforward, but there are several common pitfalls that can cost you money or even lead to rejection. Being aware of these can save you a lot of headache and expense.

One of the most common mistakes to avoid is not checking your credit score and report before applying. Many people assume their credit is fine, only to discover errors or unexpected issues that negatively impact their rate. Always review your report for accuracy and address any discrepancies.

Another frequent error is focusing solely on the monthly payment. While a low monthly payment is appealing, it often means a longer loan term and significantly more interest paid over time. Always consider the total cost of the loan, not just the monthly outlay.

Not getting pre-approved before shopping for a car is also a significant misstep. Without pre-approval, you lose your negotiating power at the dealership and might be swayed into less favorable financing options. Pre-approval arms you with a clear budget and a competitive rate.

Finally, ignoring additional fees and charges can add unexpected costs. Always read the fine print and ask about any origination fees, application fees, or prepayment penalties. JFCU is known for transparency, but it’s always good practice to ask.

Maximizing Your Chances for the Best Justice Federal Credit Union Car Loan Rates

Securing the most favorable Justice Federal Credit Union car loan rates requires strategic planning and preparation. By proactively addressing key financial areas, you can significantly enhance your borrowing power.

First, make it a priority to improve your credit score. This is paramount. Pay all your bills on time, reduce existing debt, and avoid opening too many new credit accounts close to your loan application. A higher credit score directly translates to lower interest rates.

Second, save for a larger down payment. As discussed, a substantial down payment reduces the loan amount and the lender’s risk, often leading to better rates. Even an extra few hundred or thousand dollars can make a difference.

Third, consider a shorter loan term if your budget allows. While monthly payments will be higher, the total interest paid will be much lower, and you’ll typically qualify for a better rate. Evaluate your budget carefully to find a comfortable balance.

Fourth, if your credit history is limited or your score isn’t ideal, consider a co-signer with excellent credit. A co-signer shares responsibility for the loan and can help you qualify for a better rate, though they also bear the risk.

Lastly, if you’re not already a member, become a JFCU member early. Building a relationship with the credit union can sometimes open doors to better deals and personalized service. Explore all the benefits of membership beyond just car loans. For more tips on managing your finances and improving your credit, you might want to check out our blog post on Smart Money Habits for Federal Employees.

Beyond the Rate: Other Benefits of JFCU Auto Loans

While competitive Justice Federal Credit Union car loan rates are a primary draw, the advantages of choosing JFCU extend far beyond just the numbers. These additional benefits contribute to a more positive and supportive borrowing experience.

One significant benefit is the personalized service you receive as a member. Unlike large banks where you might be just another customer, JFCU prides itself on building relationships. Loan officers often take the time to understand your individual financial situation and offer tailored advice. This personal touch can be invaluable, especially if you have unique circumstances.

JFCU also often provides financial education resources to its members. They are invested in your overall financial well-being, not just securing a loan. This can include workshops, online tools, or one-on-one counseling that helps you manage your budget, improve your credit, and plan for future financial goals.

Finally, choosing a credit union like JFCU means you’re supporting an institution with a strong community focus. As a member-owned cooperative, JFCU is dedicated to serving its specific community, often participating in local initiatives and prioritizing member needs over external shareholder demands. This ethos translates into a more ethical and member-friendly lending environment.

Frequently Asked Questions about Justice Federal Credit Union Car Loans

-

Who is eligible for a Justice Federal Credit Union car loan?

Eligibility generally extends to employees and retirees of the Department of Justice, Department of Homeland Security, and related agencies, as well as their immediate family members. You must become a JFCU member to apply. -

What is the minimum credit score required for a JFCU car loan?

While JFCU does not publicly state a minimum score, generally, a higher credit score will qualify you for better rates. They consider your entire financial profile, not just one number. -

Can I get pre-approved for a car loan with JFCU?

Yes, JFCU strongly encourages pre-approval. It allows you to know your borrowing power and interest rate before you shop for a vehicle, giving you an advantage at the dealership. -

Does JFCU offer financing for both new and used cars?

Absolutely. JFCU provides competitive loan options for both new and used vehicles, with rates and terms varying based on the vehicle’s age, mileage, and your creditworthiness. -

What documents do I need to apply for a JFCU car loan?

Typically, you’ll need proof of income (pay stubs, tax returns), proof of identity (driver’s license), and details about the vehicle if you’ve already chosen one. For pre-approval, income and personal identification are usually sufficient. -

Can I refinance my current car loan with Justice Federal Credit Union?

Yes, JFCU offers auto loan refinancing, which can be a great way to lower your interest rate, reduce your monthly payments, or shorten your loan term. This is especially beneficial if your credit score has improved since your original loan. -

Are there any application fees for JFCU car loans?

JFCU is known for transparency, but it’s always best to inquire directly about any potential fees during the application process. Credit unions typically have fewer fees than traditional banks.

Your Journey to a Better Car Loan Starts Here

Navigating the world of auto financing doesn’t have to be a complex or intimidating process. By choosing a trusted institution like Justice Federal Credit Union, you’re not just getting a loan; you’re gaining a financial partner dedicated to your success. Their commitment to competitive Justice Federal Credit Union car loan rates, combined with personalized service and a member-first philosophy, makes them an excellent choice for federal employees and their families.

We’ve explored the nuances of their loan offerings, dissected the factors influencing your rate, and armed you with strategies to secure the best possible deal. Remember, preparation is key: check your credit, understand your budget, and consider pre-approval. With this knowledge, you’re well-equipped to make an informed decision, driving off with confidence in your new vehicle and your financial future. Don’t hesitate to reach out to Justice Federal Credit Union directly to discuss your specific needs and start your journey towards a better car loan today.