Unlock Your Dream Ride: A Deep Dive into KFCU Car Loan Rates and How to Secure Your Best Deal

Unlock Your Dream Ride: A Deep Dive into KFCU Car Loan Rates and How to Secure Your Best Deal Carloan.Guidemechanic.com

Navigating the world of auto loans can feel like a complex journey, but securing the right financing is a crucial step toward owning your dream vehicle. For many, credit unions like KFCU offer a compelling alternative to traditional banks, often boasting competitive rates and a member-centric approach. But what exactly are KFCU car loan rates, what factors influence them, and how can you ensure you’re getting the absolute best deal?

As an expert blogger and professional SEO content writer, I’ve spent years analyzing financial products and helping consumers make informed decisions. In this super comprehensive guide, we’ll peel back the layers of KFCU car loan rates, providing you with unique insights and actionable strategies to confidently approach your next auto financing decision. Our goal is to make this a pillar content piece, easy to understand, and packed with real value, designed to empower you on your car buying journey.

Unlock Your Dream Ride: A Deep Dive into KFCU Car Loan Rates and How to Secure Your Best Deal

What is KFCU and Why Consider a Credit Union for Your Auto Loan?

Before we dive into the specifics of rates, let’s establish a foundational understanding of KFCU. While specific details may vary depending on the actual credit union named "KFCU" (as there can be multiple credit unions with similar acronyms or local variations), the general principles of a credit union remain consistent. Credit unions are not-for-profit financial cooperatives owned by their members. This fundamental structure sets them apart from commercial banks, which are typically for-profit entities accountable to shareholders.

This difference in ownership directly translates into how credit unions operate and the benefits they often pass on to their members. Unlike banks that aim to maximize profits, credit unions focus on providing competitive rates on loans, higher returns on savings, and lower fees. This member-first philosophy is a significant reason why many savvy consumers turn to credit unions for their auto financing needs.

Based on my experience, credit unions frequently offer car loan rates that are a full percentage point or more lower than those found at large national banks. This might not sound like much, but over the life of a 5 or 6-year car loan, even a half-percent difference can save you hundreds, if not thousands, of dollars. Moreover, the personalized service and community focus often lead to a more pleasant and supportive borrowing experience.

Unpacking KFCU Car Loan Rates: The Key Factors That Influence Your Offer

Understanding KFCU car loan rates isn’t just about looking at a published number; it’s about recognizing the intricate web of factors that determine the specific rate you, as an individual borrower, will be offered. Lenders, including credit unions, assess various elements to gauge your risk profile and set an interest rate that reflects that assessment. Let’s break down the most crucial influencers:

1. Your Credit Score: The Ultimate Indicator of Risk

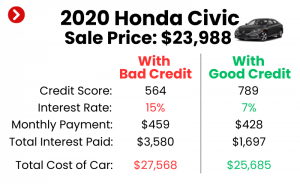

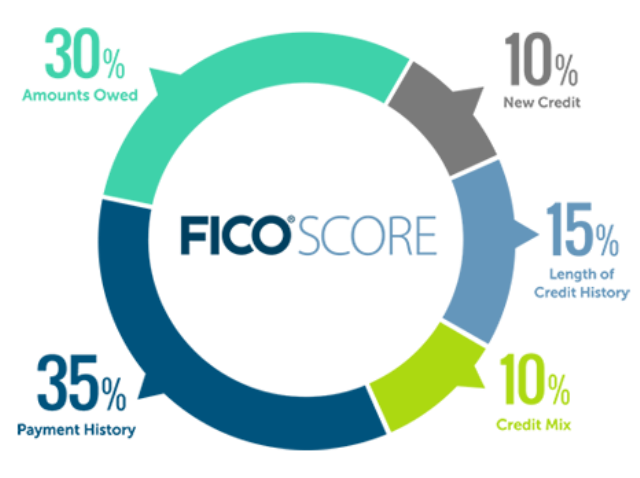

Without a doubt, your credit score is the single most impactful factor in determining your car loan interest rate. This three-digit number, primarily generated by FICO or VantageScore models, summarizes your creditworthiness based on your payment history, amounts owed, length of credit history, new credit, and credit mix. A higher score signifies a lower risk to the lender, resulting in more favorable rates.

For instance, borrowers with excellent credit (typically 780+) can expect to receive the lowest advertised rates. Those with good credit (670-739) will still get competitive offers, but perhaps slightly higher. If your score falls into the fair (580-669) or poor (below 580) categories, you’ll likely face significantly higher rates, as the lender perceives a greater risk of default. This is why consistently managing your credit is paramount for any major purchase.

Pro Tip: Before you even start shopping for a car or a loan, pull your credit report from all three major bureaus (Experian, Equifax, TransUnion) via AnnualCreditReport.com. Review it for accuracy and dispute any errors. Knowing your score upfront empowers you to negotiate and understand what rates you realistically qualify for.

2. The Loan Term: How Long You’re Willing to Pay

The loan term refers to the duration over which you agree to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72, or even 84 months). Generally, shorter loan terms come with lower interest rates. This is because a shorter term reduces the lender’s risk exposure over time. However, shorter terms also mean higher monthly payments.

Conversely, longer loan terms (e.g., 72 or 84 months) will typically have higher interest rates but offer lower monthly payments, making the car more "affordable" on a month-to-month basis. Common mistakes to avoid are focusing solely on the lowest monthly payment without considering the total cost of the loan. A longer term with a higher interest rate means you’ll pay significantly more in total interest over the life of the loan.

3. Your Down Payment: Showing Your Commitment

A substantial down payment can significantly influence your car loan rate. When you put more money down upfront, you reduce the amount you need to borrow, which in turn reduces the lender’s risk. Lenders see a larger down payment as a sign of financial stability and commitment, making them more inclined to offer you a lower interest rate.

Furthermore, a larger down payment helps prevent you from being "upside down" on your loan, a situation where you owe more than the car is worth. This provides an additional layer of security for the lender. Based on my experience, aiming for at least 10-20% of the vehicle’s purchase price as a down payment is a smart strategy to secure better rates and a stronger financial position.

4. Vehicle Type: New vs. Used and Age Matters

The type of vehicle you’re financing also plays a role in the interest rate. New cars typically qualify for lower interest rates than used cars. This is due to several factors: new cars have a higher resale value, are less likely to have immediate mechanical issues, and their value depreciation is more predictable in the short term.

Used cars, especially older models or those with high mileage, are considered higher risk due to potential mechanical problems and faster depreciation. As a result, lenders often charge higher interest rates on used car loans to compensate for this increased risk. The older the used car, generally the higher the rate.

5. Debt-to-Income (DTI) Ratio: Your Repayment Capacity

Your debt-to-income (DTI) ratio is a critical metric lenders use to assess your ability to manage monthly payments and repay new debt. It’s calculated by dividing your total monthly debt payments by your gross monthly income. A lower DTI ratio indicates that you have more disposable income available to cover your loan payments, making you a less risky borrower.

KFCU, like other lenders, will look for a DTI ratio that demonstrates you’re not overextending yourself financially. While specific thresholds vary, a DTI ratio below 36% is generally considered excellent, while anything above 43% might raise concerns and could lead to higher rates or even loan denial.

6. Market Conditions: The Broader Economic Landscape

Beyond your personal financial profile, broader economic factors and market conditions also influence car loan rates. The Federal Reserve’s target interest rate, inflation, and the overall economic outlook can affect the cost of borrowing for financial institutions. When the Fed raises rates, it generally leads to higher interest rates across the board, including for auto loans.

While you have no control over market conditions, being aware of them can help you decide the best time to apply for a loan. Sometimes, waiting a few months could result in a slightly better or worse rate depending on economic shifts.

7. KFCU Membership and Relationship: Loyalty Benefits

As a credit union, KFCU often rewards its members, especially those with an established relationship. If you’ve been a long-time member, have other accounts (savings, checking), or use other KFCU services, you might be eligible for loyalty discounts or slightly better rates. This is part of the member-first philosophy.

Building a strong relationship with your credit union can unlock various benefits over time, not just for car loans but for other financial products as well. It’s always worth inquiring about member-specific perks.

Types of KFCU Car Loans Available

KFCU typically offers a range of auto loan products designed to meet diverse member needs. Understanding these options can help you choose the best fit for your specific situation.

- New Car Loans: These are for financing brand-new vehicles directly from the dealership. They often come with the most attractive interest rates due to the lower risk associated with new cars.

- Used Car Loans: If you’re buying a pre-owned vehicle, KFCU provides used car loans. Rates for these are generally a bit higher than new car loans, and they may have restrictions based on the car’s age or mileage.

- Auto Loan Refinancing: Already have a car loan with another lender? KFCU might be able to help you refinance it. If your credit score has improved, market rates have dropped, or you want to change your loan term, refinancing can potentially lower your monthly payments or total interest paid. We have a detailed guide on this topic, "The Ultimate Guide to Car Loan Refinancing," which you might find helpful.

- Lease Buyout Loans: If your car lease is ending and you decide you want to purchase the vehicle, KFCU can offer a lease buyout loan. This converts the remaining value of the leased car into a traditional auto loan.

The KFCU Car Loan Application Process: A Step-by-Step Guide

Applying for a car loan with KFCU is generally a straightforward process, especially if you’re well-prepared. Here’s a typical step-by-step breakdown:

- Become a Member (If Not Already): Since KFCU is a credit union, you’ll need to meet their membership eligibility requirements. This often involves living, working, or worshipping in a specific geographical area, or being associated with a particular organization.

- Gather Your Documents: Before applying, have all necessary paperwork ready. This typically includes:

- Government-issued ID (driver’s license, passport).

- Proof of income (pay stubs, W-2s, tax returns for self-employed).

- Proof of residency (utility bill, lease agreement).

- Social Security Number.

- Vehicle information (if you’ve already chosen a car): VIN, make, model, year, mileage, purchase agreement.

- Apply for Pre-Approval: This is a crucial step I always recommend. You can apply online, over the phone, or in person at a KFCU branch. Pre-approval means KFCU reviews your financial information and tentatively approves you for a certain loan amount at a specific interest rate before you even pick out a car.

- Review the Offer: Once pre-approved, KFCU will provide you with a loan offer detailing the approved amount, interest rate, and potential terms. Carefully review all conditions.

- Shop for Your Car: With pre-approval in hand, you can shop for your car with confidence, knowing exactly how much you can spend and what your financing terms will be. This puts you in a stronger negotiating position at the dealership.

- Finalize the Loan: Once you’ve found your vehicle, you’ll finalize the paperwork with KFCU. This involves signing the loan agreement and providing any remaining necessary vehicle documentation. The funds are then disbursed to the seller.

Pro Tips for Securing the Best KFCU Car Loan Rates

Getting a car loan is a significant financial decision, and a little preparation can go a long way in securing the most favorable terms. Here are some pro tips from us to help you lock in the best possible KFCU car loan rates:

- Boost Your Credit Score: As discussed, your credit score is king. Before applying, dedicate time to improving it. Pay down credit card balances, ensure all bills are paid on time, and avoid opening new lines of credit. Even a 20-point increase can sometimes shift you into a better rate tier. If you want a deep dive into this, check out our article: "Understanding Your Credit Score: A Comprehensive Guide."

- Save for a Larger Down Payment: The more cash you put down, the less you need to borrow, and the lower your risk profile becomes for the lender. Aim for at least 10-20% of the vehicle’s value.

- Shop Around (Even within KFCU): While you might be loyal to KFCU, it’s always wise to compare their rates with other credit unions or even a few select banks. Sometimes, a competing offer can give you leverage. Also, ask KFCU if there are any special promotions or rates for certain vehicle types or terms.

- Consider a Shorter Loan Term: If your budget allows for higher monthly payments, opt for a shorter loan term. You’ll generally get a lower interest rate, pay less total interest over time, and own your car outright sooner.

- Get Pre-Approved: This cannot be stressed enough. Pre-approval separates the financing from the car purchase, allowing you to focus on getting the best deal on the vehicle itself. It also gives you a powerful negotiating tool at the dealership.

- Negotiate the Car Price First: Always negotiate the purchase price of the car before discussing financing options with a dealership. If you combine these two negotiations, you might lose sight of where you’re getting the best deal.

Common Mistakes to Avoid When Applying for a Car Loan

Even experienced car buyers can sometimes fall prey to common pitfalls. Being aware of these can save you money and stress.

- Applying to Too Many Lenders at Once: While shopping around is good, submitting multiple full applications within a short period can negatively impact your credit score. Each application typically results in a "hard inquiry," which can temporarily lower your score. Aim to submit all applications within a 14-45 day window, as FICO models often count these as a single inquiry for rate shopping.

- Not Checking Your Credit Report: As mentioned, reviewing your credit report for errors before applying is crucial. Incorrect information could lead to a lower score and a higher interest rate.

- Focusing Only on the Monthly Payment: Dealerships often try to "sell" you on a low monthly payment. However, this often means extending the loan term and paying significantly more in total interest. Always ask for the total cost of the loan, including all interest and fees.

- Ignoring Additional Fees: Be vigilant about any hidden fees or add-ons. Some lenders or dealerships might try to include unnecessary extras like extended warranties or GAP insurance without clearly explaining them. Understand every charge.

- Skipping Pre-Approval: Going into a dealership without pre-approval is like walking into a negotiation unarmed. You lose leverage and might be pressured into less favorable financing options offered by the dealer.

Beyond the Rate: Other Factors to Consider with KFCU

While securing a competitive interest rate is paramount, it’s not the only factor to consider when choosing a lender. KFCU, being a credit union, often excels in other areas that provide significant value.

- Customer Service and Support: Credit unions are renowned for their personalized, member-focused service. This can be invaluable if you have questions during the application process or need support throughout the life of your loan.

- Loan Flexibility: Ask about flexibility in payment options, early payoff penalties (most credit unions don’t have them), or options for deferring a payment in case of an unforeseen financial hardship.

- Additional Products and Services: KFCU might offer other beneficial services in conjunction with your auto loan, such as Guaranteed Asset Protection (GAP) insurance, extended warranties, or payment protection plans. Compare these offerings with third-party providers to ensure they are competitively priced.

- Ease of Payment: Confirm the various ways you can make your loan payments (online, mobile app, in-person, automatic deductions) to ensure convenience.

Real-World Value: Is a KFCU Car Loan Right for You?

Ultimately, the decision to choose KFCU for your car loan will depend on your individual circumstances and priorities. However, based on the inherent advantages of credit unions, a KFCU car loan often presents a compelling option for a wide range of borrowers.

If you value competitive rates, personalized service, and a member-first approach, and you meet their membership criteria, KFCU is definitely worth exploring. Their commitment to their members often translates into tangible savings and a more positive borrowing experience. By understanding the factors that influence rates, preparing thoroughly, and asking the right questions, you can leverage KFCU’s offerings to unlock your dream ride with confidence.

Remember, the goal isn’t just to get a car loan, but to secure the best car loan for your financial situation.

Conclusion: Drive Away with Confidence

Securing a car loan is a significant financial step, and understanding the nuances of KFCU car loan rates is your key to making an informed decision. By recognizing the power of your credit score, the impact of your down payment and loan term, and the advantages of credit unions, you are now equipped with the knowledge to navigate the application process like a pro.

Our comprehensive dive into KFCU’s offerings, combined with expert tips and warnings against common mistakes, aims to empower you to not just find a car, but to finance it intelligently. Take the time to prepare, compare, and engage proactively with KFCU. Your dream car, financed at the best possible rate, is well within reach. Don’t settle for less; drive away with confidence knowing you’ve made a smart financial choice.

Disclaimer: This article provides general information and is not financial advice. Specific KFCU car loan rates, terms, and conditions can vary and are subject to change. Always consult directly with KFCU or a qualified financial advisor to discuss your individual financial situation and obtain precise loan details.