Unlock Your Dream Ride: A Deep Dive into the 60 Month Car Loan Rates Calculator

Unlock Your Dream Ride: A Deep Dive into the 60 Month Car Loan Rates Calculator Carloan.Guidemechanic.com

The scent of a new car, the thrill of hitting the open road – buying a vehicle is an exciting milestone for many. However, the path to ownership often involves navigating the complex world of auto financing. For most, the dream ride isn’t paid for in cash; instead, it’s financed through a loan, and understanding the nuances of that loan is paramount.

Among the myriad of financing options, the 60-month (or 5-year) car loan has emerged as a popular choice. It strikes a balance, offering manageable monthly payments without stretching the loan term out excessively. But how do you ensure you’re getting the best deal? This is where a powerful tool, the 60 Month Car Loan Rates Calculator, comes into play.

Unlock Your Dream Ride: A Deep Dive into the 60 Month Car Loan Rates Calculator

As an expert blogger and someone deeply immersed in personal finance, I’ve seen firsthand how a well-utilized calculator can transform a potentially stressful car-buying experience into an empowered, informed decision. This comprehensive guide will not only demystify the 60-month car loan rates calculator but also equip you with the knowledge to leverage it for significant savings and financial peace of mind. We’ll explore its inner workings, the crucial factors influencing your rates, and pro tips to secure the best possible deal.

What Exactly is a 60 Month Car Loan Rates Calculator?

At its heart, a 60 Month Car Loan Rates Calculator is an online tool designed to estimate your potential monthly car payment and the total interest you’ll pay over a five-year loan term. It takes several key pieces of information you provide and, using a sophisticated financial formula, crunches the numbers instantly. This tool moves beyond simple guesswork, offering a concrete projection of your financial commitment.

The "60 months" part specifically refers to the loan term – the period over which you agree to repay the borrowed amount. A five-year term is a sweet spot for many borrowers. It often results in more affordable monthly payments compared to shorter terms, without extending so long that you risk prolonged negative equity or significantly higher total interest.

Based on my experience, many people get caught up in the excitement of car shopping and only think about the sticker price. They often overlook the true cost of borrowing. This calculator helps shift that focus, allowing you to understand the total financial picture before you even step foot in a dealership. It’s an essential first step in responsible car ownership.

The Core Components: What Inputs Do You Need?

To get the most accurate estimate from any 60 Month Car Loan Rates Calculator, you need to gather a few essential pieces of information. Think of these as the ingredients for your financial recipe. Each input plays a critical role in determining your final monthly payment and the overall cost of your loan.

-

The Total Loan Amount:

This isn’t simply the car’s sticker price. Instead, it’s the price of the vehicle minus any down payment you make and any trade-in value you’re applying. For example, if a car costs $30,000 and you put down $5,000, your loan amount is $25,000. This figure forms the principal that the interest will be calculated on. -

Your Estimated Interest Rate (APR):

This is perhaps the most crucial input. The Annual Percentage Rate (APR) represents the actual yearly cost of funds over the term of a loan, including any fees or additional costs associated with the transaction. A seemingly small difference in APR can translate into hundreds, or even thousands, of dollars saved or spent over a 60-month term. This rate is highly personal and depends on several factors we’ll explore shortly. -

The Loan Term (60 Months):

For this specific calculator, the term is fixed at 60 months. However, it’s important to understand why this duration is chosen. A 60-month term generally provides a good balance between manageable monthly payments and avoiding excessive total interest compared to longer terms like 72 or 84 months. -

Your Down Payment Amount:

This is the amount of cash you pay upfront towards the purchase price of the car. A larger down payment directly reduces the amount you need to borrow, which in turn lowers your monthly payments and, significantly, the total interest you’ll pay over the life of the loan. It’s one of the most effective ways to make a car more affordable. -

Trade-in Value (if applicable):

If you’re trading in your current vehicle, its value can also reduce the principal amount of your new car loan, similar to a down payment. Ensure you have a realistic estimate of your trade-in’s worth, which you can often get from online valuation tools or by visiting multiple dealerships.

Decoding Your Interest Rate: The Factors at Play

Your interest rate is the single biggest determinant of how much your 60-month car loan will truly cost you. It’s not a static number; rather, it’s a dynamic figure influenced by a combination of personal financial health and market conditions. Understanding these factors is key to securing the most favorable rate.

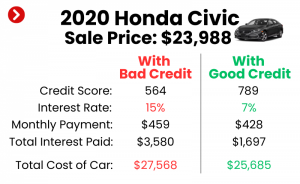

- Your Credit Score: This is, without a doubt, the most significant factor. Lenders use your credit score as a snapshot of your creditworthiness and your likelihood to repay the loan. Borrowers with excellent credit (typically 780+) can expect the lowest interest rates, while those with fair or poor credit will face higher rates to compensate lenders for the increased risk.

- Your Debt-to-Income Ratio (DTI): Lenders look at your DTI to assess your ability to handle additional debt. This ratio compares your total monthly debt payments to your gross monthly income. A lower DTI indicates you have more disposable income to cover new loan payments, making you a less risky borrower and potentially qualifying you for better rates.

- The Loan Term Itself: While we’re focusing on 60-month loans, it’s worth noting that shorter loan terms often come with slightly lower interest rates than longer terms. Lenders perceive less risk when their money is tied up for a shorter period. Conversely, stretching a loan to 72 or 84 months usually means a higher APR.

- New vs. Used Car: Generally, new car loans tend to have slightly lower interest rates than used car loans. Lenders consider new cars to be less risky because they hold their value better initially and have fewer unknown maintenance issues. Used cars, especially older models, are seen as higher risk.

- Current Market Conditions: The broader economic environment, particularly the federal interest rates set by the Federal Reserve, influences all lending rates. When the Fed raises rates, auto loan rates typically follow suit. Conversely, in a low-interest rate environment, you might find more attractive offers.

- The Lender You Choose: Not all lenders offer the same rates. Banks, credit unions, and dealership financing arms all have different criteria and rate structures. This is why shopping around is so critical. Credit unions, in particular, often provide competitive rates due to their member-focused structure.

How to Effectively Use the 60 Month Car Loan Rates Calculator

Using the calculator isn’t just about plugging in numbers; it’s about strategic planning. Based on my experience, the real power of this tool lies in its ability to help you understand your affordability and negotiate with confidence. Here’s a step-by-step guide to making the most of it:

- Gather Your Financial Data: Before you even open the calculator, have your estimated credit score, potential down payment amount, and any trade-in value ready. If you’re unsure about your credit score, many credit card companies or financial apps offer free access to it.

- Input the Variables: Enter the estimated loan amount (car price minus down payment/trade-in), your estimated APR, and ensure the loan term is set to 60 months. For the APR, start with an average rate for your credit tier, then adjust.

- Analyze the Results: The calculator will instantly display your estimated monthly payment and the total interest you’ll pay over the 60 months. Don’t just look at the monthly payment; the total interest figure is equally, if not more, important for understanding the true cost of borrowing.

- Experiment with Different Scenarios: This is where the magic happens.

- What if I increase my down payment by $1,000? See how much your monthly payment drops and how much interest you save.

- What if I can negotiate a slightly lower interest rate? Even a 0.25% reduction can lead to significant savings over five years.

- What if I consider a slightly less expensive car? This will show you the impact on both monthly payments and total interest.

- Pro Tip from Us: Use the calculator before you visit a dealership. Knowing your affordable monthly payment range and the total interest implications gives you immense power. You can walk in with a clear budget and avoid being swayed by high-pressure sales tactics that focus solely on low monthly payments without revealing the overall cost.

Beyond the Calculator: Smart Strategies for Lowering Your 60-Month Car Loan

While the calculator is an excellent starting point, your journey to an affordable car loan doesn’t end there. There are proactive steps you can take to significantly improve your loan terms and save money over the 60-month period.

- Boost Your Credit Score: This is foundational. Pay bills on time, reduce existing debt, and avoid opening new credit accounts right before applying for a car loan. Even a 20-point increase can sometimes move you into a better rate tier. For a deeper dive into improving your credit score, check out our guide on .

- Increase Your Down Payment: As mentioned, a larger down payment reduces the principal, leading to lower monthly payments and less total interest. Aim for at least 10-20% of the car’s purchase price, if possible. This also helps reduce the risk of becoming "upside down" on your loan (owing more than the car is worth).

- Shop Around for Rates (Get Pre-Approved!): This is one of the most crucial pieces of advice I can offer. Don’t just rely on the dealership’s financing. Apply for pre-approval with multiple banks and credit unions before you even start serious car shopping. Having a pre-approved offer in hand acts as a baseline and gives you negotiating leverage with the dealership.

- Consider a Shorter Term (if affordable): While this article focuses on 60 months, if your budget allows, a 48-month or even 36-month loan will almost always result in less total interest paid. Explore different loan terms and their impact in our article, ‘.

- Refinancing Your Loan: If you’ve improved your credit score since you first bought your car, or if interest rates have dropped, you might be able to refinance your existing 60-month loan at a lower rate. This can significantly reduce your monthly payments and/or the total interest you pay.

- Negotiate the Car Price: Remember, the lower the actual purchase price of the car, the less you’ll need to borrow. Always negotiate the vehicle’s price independently of the financing. A lower sticker price directly translates to a lower loan amount, which then impacts your monthly payments and total interest.

The Pitfalls: Common Mistakes to Avoid with 60-Month Loans

Even with a calculator, it’s easy to fall into common traps that can make your 60-month car loan more expensive or lead to financial stress. Being aware of these pitfalls can save you from costly mistakes.

- Overlooking Total Interest Paid: Many borrowers focus exclusively on the monthly payment. While crucial for budgeting, ignoring the total interest can lead you to accept higher rates over the 60 months, costing you thousands more in the long run. Always ask for the total cost of the loan.

- Stretching Your Budget Too Thin: Just because a calculator shows you can afford a certain monthly payment doesn’t mean you should. Leave room in your budget for other car-related expenses like insurance, maintenance, fuel, and unexpected repairs. A car is more than just a loan payment.

- Ignoring Additional Costs: Beyond the loan, remember to factor in sales tax, registration fees, and the ongoing cost of car insurance. These can add a substantial amount to your initial outlay and ongoing expenses, impacting your overall affordability.

- Not Getting Pre-Approved: Relying solely on dealership financing is a common mistake. Dealerships often mark up interest rates as a profit center. Getting pre-approved gives you a competing offer and empowers you to negotiate.

- Rolling Negative Equity into a New Loan: If you owe more on your current car than it’s worth, and you trade it in, the outstanding balance (negative equity) can be added to your new 60-month loan. This means you’re paying interest on a debt that has no asset backing it, immediately putting you "upside down" on your new car. Avoid this if at all possible.

- Focusing Solely on the Car, Not the Deal: It’s easy to get emotionally attached to a specific car. However, maintaining objectivity and focusing on the overall financial deal – including the car price, interest rate, and total cost – is crucial for making a sound decision.

When a 60-Month Loan is Right for You (and When it’s Not)

The 60-month loan term is popular for good reason, but it’s not a one-size-fits-all solution. Understanding its pros and cons in the context of your personal finances is vital.

When a 60-Month Loan is a Good Fit:

- You Need Manageable Monthly Payments: For many, a 60-month term offers a comfortable monthly payment that fits within their budget, especially for newer, more expensive vehicles.

- You Have a Good Interest Rate: If you qualify for a very low APR, the extended term means the total interest paid won’t be excessively high compared to shorter terms.

- You Plan to Keep the Car for a While: If you intend to own the vehicle beyond the 5-year loan term, the risk of negative equity is less concerning, as the car will likely be fully paid off before you consider selling or trading it.

- You Prefer Financial Flexibility: Lower monthly payments free up cash flow for other financial goals or emergencies.

When a 60-Month Loan Might Not Be Ideal:

- You Prioritize Minimal Total Interest: If your primary goal is to pay the least amount of interest possible, and you can afford higher monthly payments, a shorter loan term (e.g., 36 or 48 months) would be more advantageous.

- You Frequently Trade In Cars: If you typically upgrade your vehicle every 2-3 years, a 60-month loan significantly increases your risk of negative equity. You might owe more on the car than it’s worth when you’re ready to trade, creating a financial burden.

- Your Interest Rate is High: With a high APR, a 60-month term will accumulate a substantial amount of interest over time, making the car much more expensive in the long run. In such cases, a shorter term might be necessary, or reconsidering the purchase altogether.

- You Dislike Being in Debt: For individuals who prefer to be debt-free as quickly as possible, a 60-month commitment might feel too long.

Conclusion: Empowering Your Car-Buying Journey

The journey to owning a new car should be exciting, not intimidating. With the right tools and knowledge, you can navigate the financial landscape with confidence. The 60 Month Car Loan Rates Calculator is more than just a number-cruncher; it’s an empowerment tool that puts you in the driver’s seat of your financial decisions.

By understanding the inputs, the factors influencing your interest rate, and how to strategically use the calculator, you’re not just estimating payments – you’re building a solid financial plan. Remember to always look beyond the monthly payment to the total cost of the loan, shop around for the best rates, and take proactive steps to improve your financial standing.

Don’t let the excitement of a new car overshadow smart financial planning. Use the 60 Month Car Loan Rates Calculator as your guide, combine it with the expert tips provided here, and drive away with not just your dream car, but also a loan that makes financial sense for you. For current average interest rates based on credit score, a reliable source like can provide valuable insights to help you get started. Happy driving!