Unlock Your Dream Ride: The Ultimate Guide on How To Be Pre Approved For A Car Loan

Unlock Your Dream Ride: The Ultimate Guide on How To Be Pre Approved For A Car Loan Carloan.Guidemechanic.com

Buying a car is an exciting milestone, whether it’s your very first vehicle or an upgrade. However, for many, the joy of choosing a new set of wheels can quickly be overshadowed by the complexities and uncertainties of financing. Walking into a dealership without a clear financial plan can leave you feeling vulnerable, confused, and potentially paying more than you should.

But what if you could flip the script? What if you could approach car shopping with the confidence of a cash buyer, knowing exactly how much you can spend and at what interest rate? This isn’t a fantasy; it’s the power of car loan pre-approval.

Unlock Your Dream Ride: The Ultimate Guide on How To Be Pre Approved For A Car Loan

In this comprehensive guide, we’ll demystify the process of how to be pre approved for a car loan. We’ll cover everything from understanding your credit to finding the best lenders, ensuring you’re well-equipped to secure favorable terms and drive away in your dream car with peace of mind. Get ready to transform your car buying experience from stressful to seamless!

What Exactly Is Car Loan Pre-Approval?

Let’s start with the basics. Car loan pre-approval is essentially a preliminary commitment from a lender to provide you with a specific amount of money for a car purchase, at a particular interest rate, and for a set loan term. This isn’t just a casual estimate; it’s a conditional offer based on a thorough review of your financial standing.

Think of it as having a "golden ticket" in your pocket before you even step foot on a dealership lot. The lender evaluates your credit history, income, and debt obligations to determine your creditworthiness. If approved, they provide you with a pre-approval letter outlining the maximum loan amount, the estimated interest rate (APR), and the duration of the loan.

It’s crucial to distinguish pre-approval from pre-qualification. Pre-qualification is often a soft credit check that gives you an idea of what you might qualify for, without a firm commitment from the lender. Pre-approval, on the other hand, involves a hard credit inquiry and results in a concrete offer, albeit one that is still conditional on the final vehicle and full documentation. Understanding this distinction is the first step in mastering how to be pre approved for a car loan effectively.

Why Pre-Approval Is Your Secret Weapon for Car Buying Success

Based on my experience advising countless car buyers, securing a car loan pre-approval is not just a good idea—it’s a game-changer. It transforms you from a hopeful shopper into an empowered buyer. Here’s why it’s your ultimate secret weapon:

1. Establishes a Clear Budget and Prevents Overspending

One of the biggest benefits of pre-approval is that it clearly defines your spending limit. You’ll know exactly how much a lender is willing to finance for you. This clarity helps you focus your car search on vehicles that genuinely fit your financial capabilities, preventing the common trap of falling in love with a car you can’t truly afford.

This definite budget acts as a financial guardrail, ensuring you don’t get swayed by high-pressure sales tactics. It keeps your car buying journey realistic and financially responsible from the outset.

2. Enhances Your Negotiating Power at the Dealership

Walking into a dealership with a pre-approval letter in hand immediately gives you leverage. You’re essentially telling the dealer, "I already have my financing secured, so let’s talk about the car’s price." This shifts the focus from your creditworthiness to the vehicle itself.

Dealers make money on both the car sale and the financing. When you arrive pre-approved, you’ve removed their ability to profit significantly from the loan. This often motivates them to offer a better price on the car to close the deal.

3. Saves Valuable Time at the Dealership

The financing process at a dealership can be notoriously long and arduous. Filling out applications, waiting for credit checks, and sifting through various loan offers can easily take hours. With pre-approval, you’ve completed much of this legwork beforehand.

You can walk in, choose your car, and often complete the purchase much faster. This means less time spent in a waiting room and more time enjoying your new vehicle.

4. Offers Transparency and Reduces Financial Surprises

Pre-approval provides a clear understanding of your interest rate and loan terms before you’re even at the dealership. This transparency allows you to compare different offers from various lenders side-by-side. You won’t be caught off guard by unexpected high interest rates or unfavorable terms.

Pro tips from us: Always scrutinize the Annual Percentage Rate (APR) and the total cost of the loan, not just the monthly payment. This ensures you’re getting the best possible deal.

5. Separates the Car Price from the Loan Terms

When you finance through a dealership, it’s easy for them to muddy the waters by bundling the car price and loan terms together. This makes it difficult to tell if you’re getting a good deal on the car or on the financing.

With pre-approval, you’ve already locked in your financing. This allows you to negotiate the car’s price as if you were a cash buyer, isolating that negotiation. Once you’ve agreed on a price, you can then decide whether to use your pre-approved loan or see if the dealership can beat your rate.

The Essential Steps to Prepare for Car Loan Pre-Approval

Mastering how to be pre approved for a car loan requires preparation. It’s not just about filling out a form; it’s about presenting yourself as a low-risk borrower. Here are the crucial steps you need to take:

Step 1: Know Your Credit Score Inside Out

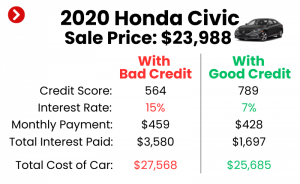

Your credit score is arguably the most critical factor lenders consider when evaluating a loan application. It’s a numerical representation of your creditworthiness, reflecting your history of borrowing and repaying debt. A higher score typically translates to lower interest rates and better loan terms.

Lenders primarily use FICO scores and VantageScores. These scores range from 300 to 850, with scores in the "good" (670-739), "very good" (740-799), or "excellent" (800+) ranges being most favorable. Understanding where you stand is the first order of business.

You are entitled to a free credit report from each of the three major credit bureaus (Experian, Equifax, and TransUnion) once every 12 months. You can access these reports at www.annualcreditreport.com. Reviewing your reports allows you to identify any errors that might be dragging your score down.

Step 2: Improve Your Credit Score (If Needed)

If your credit score isn’t where you want it to be, taking steps to improve it before applying for pre-approval can save you thousands over the life of the loan. Even a small bump in your score can significantly impact the interest rate offered.

- Pay Bills On Time, Every Time: Payment history is the largest factor influencing your credit score. Set up automatic payments or reminders to ensure you never miss a due date.

- Reduce Existing Debt: Your credit utilization ratio (how much credit you’re using compared to your total available credit) is another key factor. Aim to keep this ratio below 30%, ideally even lower. Paying down credit card balances can quickly improve this.

- Avoid New Credit Applications: Each new credit application results in a hard inquiry, which can temporarily ding your score. Try to avoid opening new credit accounts in the months leading up to your car loan application.

- Dispute Errors: If you find inaccuracies on your credit report, dispute them immediately with the credit bureau. These errors could be negatively impacting your score.

Common mistakes to avoid are closing old credit cards, even if they have a zero balance. An older credit account with a good payment history contributes positively to your credit age and available credit, which helps your utilization ratio.

Step 3: Determine Your Budget and Down Payment

While pre-approval gives you a maximum loan amount, it’s crucial to set your own comfortable budget. This budget should encompass more than just the monthly car payment. Remember to factor in insurance, fuel costs, maintenance, and potential registration fees.

Pro tips from us: Create a realistic budget that considers all these ongoing expenses. A car can become a financial burden if you only focus on the monthly payment.

A significant down payment can dramatically improve your chances of approval and secure a better interest rate. A larger down payment reduces the amount you need to borrow, making you a less risky borrower in the eyes of lenders. It also reduces your monthly payments and the total interest paid over the life of the loan. Aim for at least 10-20% of the car’s price, if possible.

Lenders also look at your debt-to-income (DTI) ratio. This is the percentage of your gross monthly income that goes towards paying your monthly debt payments. A lower DTI ratio (typically below 36-43%) indicates you have sufficient income to manage additional debt.

Step 4: Gather Necessary Documentation

Lenders require specific documents to verify your identity, income, and residence. Having these ready will streamline the pre-approval process and prevent delays. From years of advising, I’ve seen applications delayed simply because applicants weren’t prepared with the necessary paperwork.

Here’s a checklist of common documents you’ll need:

- Proof of Identity: Government-issued photo ID (driver’s license, passport) and Social Security Number.

- Proof of Income: Recent pay stubs (typically 2-3 months), W-2s, or tax returns (if self-employed).

- Proof of Residence: Utility bills (electricity, water), lease agreement, or mortgage statement.

- Bank Statements: Recent statements to show financial stability and cash flow.

- Existing Debt Information: Details on other loans or credit lines you hold.

Having everything organized in advance demonstrates your preparedness and seriousness as a borrower.

Step 5: Research Lenders and Compare Offers

Don’t just go with the first lender you find. Different lenders have different criteria and offer varying rates. Shopping around is a crucial step in how to be pre approved for a car loan at the best possible terms.

- Banks: Large national banks and smaller local banks are common sources for auto loans. If you have an existing relationship with a bank, they might offer you a preferential rate.

- Credit Unions: Often known for offering competitive interest rates and personalized service, credit unions are an excellent option to explore. Membership is usually required but is often easy to obtain.

- Online Lenders: A growing number of online-only lenders specialize in auto loans. They often provide quick decisions and can be very competitive.

- Dealership Financing: While you’re getting pre-approved elsewhere, dealerships also offer financing. It’s wise to consider their offer as a comparison, but always have your independent pre-approval as a benchmark.

Apply to a few different lenders within a short window (typically 14-45 days, depending on the credit scoring model). Multiple inquiries for the same type of loan within this period will usually be treated as a single hard inquiry on your credit report, minimizing the impact on your score. For a deeper dive into choosing the right lender, check out our guide on .

The Pre-Approval Application Process: What to Expect

Once you’ve prepared, the application process itself is fairly straightforward. Most lenders offer online applications, making it convenient to apply from home. You’ll fill out a form with your personal information, employment details, income, and existing debt.

The lender will then conduct a "hard inquiry" on your credit report. This is a detailed look at your credit history and is a necessary step for pre-approval. A hard inquiry can temporarily lower your credit score by a few points, but the impact is usually minor and short-lived, especially if you’re rate shopping within the recommended timeframe.

The timeline for approval can vary. Online lenders often provide instant decisions, while banks and credit unions might take a few hours to a few business days. Once approved, you’ll receive a pre-approval letter or certificate, either digitally or via mail.

What Happens After You Get Pre-Approved?

Congratulations! You’ve successfully navigated how to be pre approved for a car loan. Now, you’re ready to shop with confidence. Your pre-approval letter will detail the maximum loan amount, your approved interest rate, and the loan term. It will also specify an expiration date, so be mindful of the timeframe.

When you head to the dealership, you’re in the driver’s seat. You know your budget, and you have your financing secured. This allows you to focus purely on negotiating the best possible price for the car itself. Don’t feel pressured to reveal your pre-approval amount immediately. Use it as your backup plan.

Pro tips from us: Negotiate the car price first, as if you were paying cash. Once you’ve settled on a price, then you can present your pre-approval letter. You can even ask the dealership to see if they can beat your pre-approved interest rate. Sometimes, they can, especially if they have incentives from their own lending partners.

Common Mistakes to Avoid During the Pre-Approval Process

Even with the best intentions, it’s easy to make missteps. Being aware of these common mistakes can save you time, money, and frustration.

- Applying with Too Many Lenders Over a Long Period: While rate shopping within a short window is good, spreading your applications out over several months can lead to multiple hard inquiries that negatively impact your score. Group your applications within a 14-45 day period.

- Not Knowing Your Credit Score: Going into the process blind leaves you unprepared for potential rejections or high-interest offers. Always check your credit score and report beforehand.

- Ignoring Your Budget Beyond the Monthly Payment: As discussed, only focusing on the monthly payment can lead to an unaffordable car once insurance, fuel, and maintenance are factored in.

- Making Major Financial Changes After Pre-Approval: Avoid opening new credit lines, closing existing accounts, or taking on new debt between pre-approval and purchasing the car. Lenders may re-verify your financial situation, and significant changes could jeopardize your final loan approval.

- Falling for Dealer Financing Tricks Without Comparing: While some dealer financing can be competitive, always compare it against your independent pre-approval. Don’t let a dealership rush you into a higher-rate loan.

Frequently Asked Questions (FAQs) About Car Loan Pre-Approval

To further clarify how to be pre approved for a car loan, here are answers to some common questions:

How long does car loan pre-approval last?

Typically, car loan pre-approval is valid for 30 to 60 days. This gives you a reasonable window to find your car and finalize the purchase. Always check the expiration date on your pre-approval letter.

Does pre-approval guarantee I’ll get the loan?

No, pre-approval is a conditional offer. It means you’re approved based on the information you provided and your credit history. The final approval is contingent on verifying all your documentation, the specific vehicle you choose (it must meet the lender’s criteria, usually age and mileage limits), and no significant changes in your financial situation.

Can I get pre-approved for a used car?

Absolutely! Lenders pre-approve loans for both new and used vehicles. However, interest rates for used cars can sometimes be slightly higher, and there might be restrictions on the age or mileage of the used vehicle a lender will finance.

What if I have bad credit? Can I still get pre-approved?

It can be more challenging to get pre-approved with bad credit, and you may face higher interest rates. However, it’s not impossible. Some lenders specialize in bad credit auto loans. Focus on improving your credit score as much as possible, consider a larger down payment, or explore co-signers to increase your chances. For a comprehensive guide on improving your credit, see .

Is car loan pre-approval worth the effort?

Unequivocally, yes! The effort involved in getting pre-approved pays dividends in peace of mind, negotiating power, and potentially thousands of dollars saved over the life of your loan. It transforms the often-stressful car buying process into a more confident and controlled experience.

Drive Away with Confidence

Understanding how to be pre approved for a car loan is more than just a financial strategy; it’s an empowerment tool. It puts you in control of your car buying journey, giving you the clarity and confidence needed to make smart decisions. By taking the time to prepare, understand your credit, research lenders, and compare offers, you position yourself for success.

Don’t let the financing process intimidate you. Embrace the power of pre-approval, and you’ll not only secure a great deal but also enjoy the thrill of driving off in your new car, knowing you made a financially sound choice. Start your pre-approval journey today and unlock the door to your dream ride!