Unlock Your Dream Ride: The Ultimate Guide to BECU Used Car Loans

Unlock Your Dream Ride: The Ultimate Guide to BECU Used Car Loans Carloan.Guidemechanic.com

The thrill of finding that perfect pre-owned vehicle is undeniable. It could be a classic sedan, a robust SUV for family adventures, or an economical compact car for daily commutes. Whatever your dream ride, securing the right financing is often the critical next step to turning that dream into a reality. This is where a trusted financial partner like BECU comes into play, offering tailored BECU Used Car Loans that can make your car buying journey smoother and more affordable.

Navigating the world of auto financing can feel overwhelming, with countless options and terms to decipher. However, understanding your choices, especially when considering a credit union like BECU, can significantly impact your financial well-being. This comprehensive guide will delve deep into everything you need to know about BECU’s offerings, helping you make an informed decision and drive away with confidence.

Unlock Your Dream Ride: The Ultimate Guide to BECU Used Car Loans

Why Choose BECU for Your Used Car Loan? The Credit Union Advantage

When it comes to financing a used car, you have many choices, from traditional banks to online lenders. However, credit unions like BECU (Boeing Employees’ Credit Union) often stand out for their member-focused approach and competitive offerings. Unlike banks, which are for-profit entities, credit unions are not-for-profit financial cooperatives owned by their members. This fundamental difference translates into tangible benefits for you.

Based on my experience, credit unions consistently prioritize their members’ financial health. This means they are often able to offer more favorable terms, including lower interest rates and fewer fees, because their primary goal isn’t maximizing shareholder profits. Instead, any surplus earnings are typically reinvested into the credit union to benefit members through better rates, lower fees, and improved services. This makes a BECU Used Car Loan an attractive option for many.

Beyond competitive rates, BECU is renowned for its exceptional member service. You’re not just an account number; you’re a valued member of a community. This often translates to personalized guidance throughout the loan application process, ensuring you understand every step and feel supported in your financial decisions. Their commitment to member satisfaction is a cornerstone of their operation.

Understanding BECU Used Car Loan Eligibility: Are You Ready?

Before you even start browsing vehicles, it’s crucial to understand the eligibility requirements for a BECU Used Car Loan. This foresight can save you time and potential disappointment. Eligibility typically boils down to a few key areas: BECU membership, your creditworthiness, and the specifics of the vehicle you intend to purchase.

BECU Membership: The Gateway to Benefits

The first and most critical step to securing any BECU product, including their used car loans, is to become a member. BECU is an open-charter credit union, which means their membership is quite broad. You generally qualify if you:

- Live, work, or worship in Washington State.

- Are a current or retired employee of Boeing or an affiliate company.

- Are a family member of an existing BECU member.

- Are a member of the Northwest Credit Union Foundation.

The process of joining is straightforward and usually involves opening a savings account with a minimal deposit. Pro tips from us: Confirm your eligibility directly on the BECU website or by contacting their member service before initiating any loan application. This ensures a smooth start to your financing journey.

Your Credit Profile: What BECU Looks For

Like any lender, BECU assesses your creditworthiness to determine your loan eligibility and interest rate. While BECU is known for being member-friendly, a good credit score is always beneficial. They typically look at:

- Credit Score: A higher score generally indicates a lower risk, leading to better rates. While BECU may approve loans for a range of scores, aiming for a FICO score of 670 or above is often ideal for securing the most competitive BECU auto loan rates.

- Credit History: Lenders review your payment history, the types of credit you’ve managed, and how long you’ve had credit. A history of timely payments and responsible credit use is highly favorable.

- Debt-to-Income (DTI) Ratio: This ratio compares your total monthly debt payments to your gross monthly income. A lower DTI ratio (typically below 36-40%) shows you have enough income to comfortably manage additional debt, such as a car loan.

Common mistakes to avoid are applying for multiple lines of credit shortly before a car loan application, which can temporarily lower your score, or not checking your credit report for errors beforehand.

Vehicle Requirements: What Kind of Used Car Qualifies?

BECU, like other lenders, has specific requirements for the used vehicles they will finance. These are in place to protect both the borrower and the lender. Generally, these include:

- Age and Mileage Limits: While specific limits can vary, most lenders prefer vehicles that are not excessively old or have extremely high mileage. For example, a car might need to be less than 10 years old with fewer than 125,000 miles.

- Vehicle Value: The loan amount is usually tied to the car’s market value, often determined by resources like Kelley Blue Book (KBB) or NADAguides. BECU will finance a percentage of this value, ensuring the loan doesn’t exceed the vehicle’s worth.

- Title Status: The vehicle must have a clean title, meaning no salvage, rebuilt, or branded titles. This ensures the car is safe and legally sound.

Always verify these specific requirements with BECU directly before falling in love with a particular car. This ensures that the vehicle you choose aligns with their financing criteria.

The BECU Used Car Loan Application Process: A Step-by-Step Guide

Securing used car financing with BECU is a streamlined process designed with the member in mind. Breaking it down into manageable steps can help demystify the journey and ensure you’re well-prepared.

Step 1: Become a BECU Member (If You Aren’t Already)

As discussed, membership is the foundation. If you’re not yet a BECU member, this is your very first step. You can typically apply for membership online, in person at a BECU branch, or by phone. You’ll need to provide personal identification, your Social Security Number, and make a small initial deposit into a savings account to activate your membership. This process is usually quick and straightforward.

Step 2: Get Pre-Approved for Your Loan

This is arguably the most crucial step in the car buying process. Getting BECU pre-approval for a used car loan offers significant advantages:

- Know Your Budget: Pre-approval gives you a clear understanding of how much you can borrow, allowing you to shop within your financial comfort zone.

- Bargaining Power: Walking into a dealership with a pre-approval letter from BECU is like having cash in hand. It demonstrates you’re a serious buyer and gives you leverage to negotiate a better price on the vehicle, rather than focusing solely on monthly payments.

- Faster Purchase: With financing already secured, you can expedite the purchase process once you find the right car.

To get pre-approved, you’ll typically provide BECU with personal information, income details, employment history, and authorize a credit check. They will then provide you with a conditional loan offer, including an interest rate and maximum loan amount, valid for a specific period (e.g., 30-60 days). Pro tips from us: Always get pre-approved before you start test driving cars. It shifts your focus from "can I afford this car?" to "is this the right car for me?"

Step 3: Find Your Perfect Car

With your BECU pre-approval in hand, you’re now empowered to shop confidently. Take your time to research vehicles that fit your needs, budget, and pre-approved loan amount. Consider factors like:

- Reliability Ratings: Look up reviews and reliability scores for different makes and models.

- Vehicle History Reports: Always get a CarFax or AutoCheck report to check for accidents, title issues, and service history.

- Professional Inspection: Even if you’re buying from a reputable dealer, it’s wise to have an independent mechanic inspect the car before purchase.

- Negotiation: Remember your pre-approval gives you leverage. Don’t be afraid to negotiate the car’s price.

Once you’ve found the ideal vehicle, ensure it meets BECU’s specific used car financing requirements regarding age, mileage, and value.

Step 4: Finalize Your Loan

After you’ve agreed on a price with the seller, it’s time to finalize your BECU loan application process. You’ll provide BECU with the final details of the vehicle, including the VIN, mileage, and purchase price. They will then prepare the final loan documents.

Required documents for closing typically include:

- Proof of income (pay stubs, tax returns).

- Proof of residence.

- Valid driver’s license.

- Vehicle purchase agreement or bill of sale.

- Vehicle title information.

You’ll review and sign the loan agreement, and BECU will disburse the funds directly to the seller or provide you with a check to complete the purchase. The entire process, especially with pre-approval, can be remarkably quick and efficient, often completed within a few business days.

Key Features and Benefits of BECU Used Car Loans

Choosing BECU for your used car loan comes with a host of features and benefits designed to provide value and peace of mind. These elements contribute to making their offerings highly competitive in the market.

Competitive Interest Rates

BECU is consistently recognized for offering some of the most competitive BECU auto loan rates. As a credit union, their non-profit structure allows them to pass savings directly to their members. The actual interest rate you receive will depend on several factors, including your credit score, the loan term, and the vehicle’s specifics. Generally, excellent credit will qualify you for the lowest advertised rates.

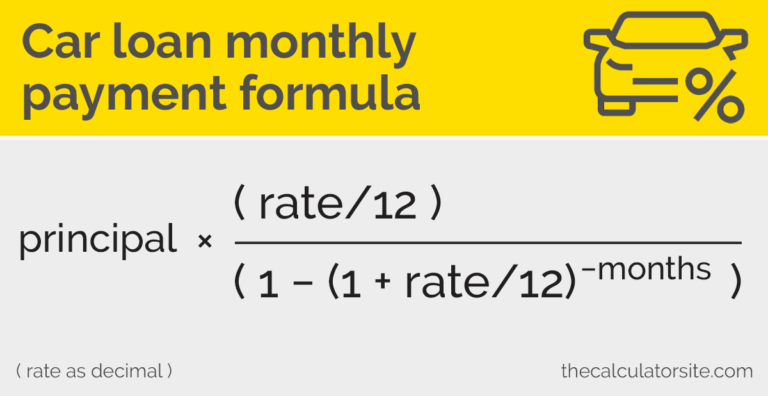

It’s important to remember that even a small difference in interest rates can lead to significant savings over the life of your loan. Using a BECU used car loan calculator on their website can help you estimate your potential monthly payments and total interest paid based on different rates and terms.

Flexible Repayment Terms

BECU understands that every borrower’s financial situation is unique. They offer a range of flexible repayment terms, typically from 12 months up to 84 months (7 years). This flexibility allows you to choose a term that best fits your budget and financial goals.

- Shorter Terms (e.g., 36-48 months): Lead to higher monthly payments but result in less interest paid over the life of the loan. You’ll own your car outright faster.

- Longer Terms (e.g., 60-84 months): Offer lower monthly payments, making the car more affordable on a month-to-month basis. However, you’ll pay more in total interest over the longer duration.

Carefully consider your budget and the total cost of the loan when selecting a term. Our pro tip is to choose the shortest term you can comfortably afford.

No Prepayment Penalties

One of the significant advantages of a BECU auto loan is the absence of prepayment penalties. This means you can pay off your loan early without incurring any additional fees. This flexibility is invaluable if you receive a bonus, a tax refund, or simply find yourself in a better financial position to accelerate your loan repayment. Paying off your loan early saves you money on interest and frees up your monthly budget.

Optional Loan Protection Products

BECU offers various optional products to protect your investment and financial well-being:

- Guaranteed Asset Protection (GAP) Insurance: If your car is totaled or stolen, your insurance payout might be less than what you still owe on the loan. GAP insurance covers this difference, preventing you from being upside down on your loan.

- Payment Protection: This can help cover your loan payments in the event of unforeseen life events like job loss, disability, or death. It provides a safety net during challenging times.

While these are optional, they offer valuable peace of mind and are worth considering, especially for newer or higher-value vehicles.

Auto-Pay Discounts

Many financial institutions, including BECU, offer small interest rate discounts if you set up automatic payments from your BECU checking or savings account. This not only saves you a bit of money but also ensures you never miss a payment, protecting your credit score. It’s a simple way to maximize the benefits of a BECU auto loan.

Refinancing Your Used Car Loan with BECU

Perhaps you already have a used car loan with another lender, but the interest rate isn’t as favorable as you’d like, or your financial situation has improved. This is where the option to refinance your used car loan with BECU becomes highly beneficial.

Many of our readers have successfully refinanced their existing auto loans, often resulting in significant savings. Refinancing essentially means taking out a new loan to pay off your current one. You might consider refinancing if:

- Interest Rates Have Dropped: If current BECU auto loan rates are lower than your existing rate.

- Your Credit Score Has Improved: A better credit score can qualify you for a lower rate now.

- You Want Lower Monthly Payments: By extending the loan term (though this might increase total interest).

- You Want to Reduce Total Interest Paid: By shortening the loan term (though this might increase monthly payments).

The process for refinancing a used car loan with BECU is similar to applying for a new loan. You’ll need to be a BECU member, apply for the refinance, and provide details about your current loan and vehicle. If approved, BECU will pay off your old loan, and you’ll begin making payments to BECU under your new, hopefully more favorable, terms. It’s a smart financial move worth exploring.

Pro Tips for a Smooth BECU Used Car Loan Experience

Navigating the used car loan process can be straightforward if you’re well-prepared. Here are some expert tips to ensure you have the best possible experience with your BECU Used Car Loan:

1. Boost Your Credit Score

Before applying, take steps to improve your credit score. Pay down existing debts, make all payments on time, and avoid opening new credit accounts. A higher score translates directly to better BECU auto loan rates.

2. Save for a Down Payment

While not always required, making a down payment on your used car can significantly reduce the amount you need to borrow. This lowers your monthly payments, reduces the total interest you’ll pay, and helps you build equity in the vehicle faster. A larger down payment can also make you a more attractive borrower to BECU.

3. Know Your Full Budget

Beyond the monthly loan payment, remember to factor in other costs of car ownership. These include insurance, registration fees, maintenance, fuel, and potential repairs. A comprehensive budget ensures you can comfortably afford your car without financial strain.

4. Read the Fine Print

Always take the time to thoroughly read and understand all the terms and conditions of your loan agreement before signing. Pay attention to the interest rate, loan term, any fees, and the total cost of the loan. Don’t hesitate to ask BECU representatives to clarify anything you don’t understand.

5. Ask Questions

BECU prides itself on its member service. If you have any questions at any point during the process, whether it’s about membership, eligibility, the application, or specific loan terms, reach out to them. Getting clear answers ensures you’re making informed decisions.

6. Consider Your Trade-In Value

If you’re trading in your old vehicle, research its market value beforehand using resources like Kelley Blue Book. This knowledge will help you negotiate a fair trade-in price and ensure you’re getting the best deal on your new-to-you car.

Common Mistakes to Avoid When Applying for a Used Car Loan

Even with the best intentions, certain pitfalls can derail your used car loan journey. Being aware of these common mistakes can help you steer clear of them:

- Not Checking Your Credit Report: Always review your credit report for inaccuracies before applying. Errors can negatively impact your score and affect your loan terms.

- Skipping Pre-Approval: As highlighted earlier, pre-approval is a powerful tool. Not getting it means you’re shopping blind and lose significant negotiation power.

- Focusing Only on Monthly Payments: While important, fixating solely on the monthly payment can lead to longer loan terms and ultimately, paying more in interest. Always consider the total cost of the loan.

- Ignoring Additional Costs: Forgetting to budget for insurance, registration, and potential maintenance can quickly lead to financial stress.

- Not Comparing Offers (Even from BECU): While BECU often offers excellent rates, it’s always wise to briefly compare at least one or two other offers to ensure you’re truly getting the best deal. However, be mindful of too many hard inquiries on your credit report.

By avoiding these common missteps, you can ensure a smoother, more financially sound used car purchase.

Your Road Ahead: Driving with BECU Confidence

Securing a used car loan doesn’t have to be a daunting task. With its member-centric approach, competitive BECU auto loan rates, flexible terms, and comprehensive support, BECU stands out as an excellent choice for financing your next pre-owned vehicle. By understanding the eligibility requirements, meticulously following the application steps, and leveraging the benefits offered, you can navigate the process with confidence and clarity.

Whether you’re looking to purchase your first car, upgrade to a family-friendly SUV, or simply find a reliable daily driver, a BECU Used Car Loan can provide the financial foundation you need. Remember to utilize resources like the BECU used car loan calculator and always ask questions. With BECU as your partner, you’re not just getting a loan; you’re gaining a trusted advisor committed to helping you achieve your automotive dreams. Start your journey today and drive away in the car you’ve always wanted.