Unlock Your Dream Ride: The Ultimate Guide to Car Loan APR, Credit Score, and Smart Calculators

Unlock Your Dream Ride: The Ultimate Guide to Car Loan APR, Credit Score, and Smart Calculators Carloan.Guidemechanic.com

The excitement of getting a new car is undeniable. Imagine cruising down the open road, the wind in your hair, in a vehicle that perfectly suits your needs and desires. But before you hit the gas on your automotive dreams, there’s a crucial pit stop you need to make: understanding the financial mechanics of a car loan. This is where the powerful trio of Car Loan APR, Credit Score, and Smart Calculators comes into play.

Navigating the world of auto financing can feel like a complex maze, filled with jargon and numbers. Many prospective buyers focus solely on the monthly payment, overlooking critical factors that determine the true cost of their loan. This comprehensive guide is designed to empower you with the knowledge and tools you need to secure the best possible deal, saving you thousands of dollars over the life of your loan. We’ll dive deep into each element, ensuring you approach your next car purchase with confidence and clarity.

Unlock Your Dream Ride: The Ultimate Guide to Car Loan APR, Credit Score, and Smart Calculators

Demystifying the Car Loan APR: Your True Cost of Borrowing

When you’re shopping for a car loan, you’ll hear the term "APR" frequently. But what exactly does it mean, and why is it so important? APR stands for Annual Percentage Rate, and it represents the true yearly cost of borrowing money. It’s far more than just the interest rate.

The interest rate is simply the cost of borrowing the principal amount. However, the APR encompasses the interest rate plus any additional fees associated with the loan, such as administrative fees, origination fees, or closing costs. By bundling these charges into a single percentage, the APR provides a standardized way to compare different loan offers. This holistic view is crucial for understanding the total financial commitment.

Based on my experience, many first-time car buyers make the mistake of comparing only the stated interest rate. They might see two offers with similar interest rates but vastly different APRs. Always look at the APR when comparing loan products, as it gives you the most accurate picture of what you’ll actually pay each year for the privilege of borrowing. A lower APR directly translates to less money paid out of your pocket over the loan term.

Factors Influencing Your Car Loan APR

Several key factors determine the APR you’ll be offered for a car loan. Understanding these can help you strategize for a better rate.

-

Your Credit Score: This is arguably the most significant factor. Lenders use your credit score to assess your creditworthiness and the likelihood of you repaying the loan. A higher credit score signals lower risk, leading to a lower APR. We’ll explore this in much greater detail shortly.

-

Loan Term: The length of time you have to repay the loan also impacts the APR. Shorter loan terms typically come with lower APRs because the lender’s risk is reduced over a shorter period. While a longer term might offer a lower monthly payment, it often results in a higher overall interest paid and sometimes a slightly higher APR.

-

Down Payment Amount: Making a substantial down payment reduces the amount you need to borrow, which in turn reduces the lender’s risk. This can often translate into a more favorable APR. A larger down payment also builds immediate equity in your vehicle.

-

Vehicle Type (New vs. Used): New cars often qualify for lower APRs compared to used cars. Lenders perceive used cars as carrying more risk due to potential maintenance issues and faster depreciation. Dealerships may also offer special promotional rates for new vehicles.

-

Lender Type: Different lenders have different risk appetites and fee structures. Banks, credit unions, and online lenders each offer varying rates. Credit unions, for example, are known for often providing competitive APRs to their members due to their non-profit cooperative structure.

-

Market Conditions: Broader economic factors, such as the prime interest rate set by central banks, can influence car loan APRs across the board. When interest rates are generally low, car loan APRs tend to follow suit.

The Indispensable Role of Your Credit Score

Your credit score is a three-digit number that holds immense power in the world of lending. For a car loan, it acts as your financial report card, summarizing your credit history and predicting your ability to manage debt responsibly. Understanding this score is not just important; it’s essential for unlocking favorable loan terms.

What Exactly is a Credit Score?

A credit score is a numerical representation of your creditworthiness. The most widely used scoring models are FICO (Fair Isaac Corporation) and VantageScore. Both models analyze your credit report to generate a score, typically ranging from 300 to 850. A higher score indicates a lower risk to lenders.

Lenders use these scores to quickly assess how likely you are to repay your loan on time. A strong score means you’re considered a reliable borrower, which gives lenders the confidence to offer you lower interest rates and better terms. Conversely, a lower score signals higher risk, leading to higher APRs or even loan denial.

How Your Credit Score is Calculated

While the exact algorithms are proprietary, both FICO and VantageScore consider similar categories when calculating your score:

- Payment History (35% of FICO Score): This is the most crucial factor. Paying bills on time, every time, positively impacts your score. Late payments, defaults, bankruptcies, or collections will severely damage it.

- Amounts Owed / Credit Utilization (30%): This refers to the amount of credit you’re using compared to your total available credit. Keeping your credit card balances low (ideally below 30% of your limit) demonstrates responsible credit management.

- Length of Credit History (15%): A longer history of responsible credit use is generally better. It shows lenders a sustained pattern of good behavior.

- New Credit (10%): Applying for multiple new credit accounts in a short period can be seen as risky behavior and may temporarily lower your score. Each "hard inquiry" on your report can cause a slight dip.

- Credit Mix (10%): Having a healthy mix of different types of credit (e.g., credit cards, installment loans like mortgages or student loans) can be beneficial, as it shows you can manage various credit products.

Impact of Credit Score on Car Loan APR

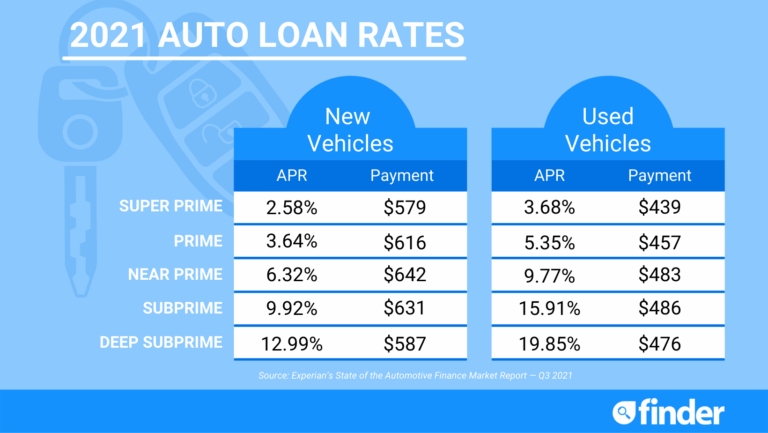

The link between your credit score and your car loan APR is direct and significant. Here’s a general breakdown of how different credit score ranges might influence the rates you’re offered:

- Excellent Credit (780-850): Borrowers in this range are considered prime candidates. They typically qualify for the lowest available APRs, often the best promotional rates.

- Good Credit (670-779): These borrowers are also viewed favorably. They can expect competitive APRs, though perhaps not the absolute lowest.

- Fair Credit (580-669): This range is often considered "subprime." Borrowers here will likely face higher APRs due to the increased perceived risk. Loan terms might also be less flexible.

- Poor Credit (300-579): Securing a car loan with poor credit is challenging and will almost certainly come with very high APRs, sometimes exceeding 20% or even higher. Lenders might also require a larger down payment or a co-signer.

Pro tips from us: Before you even step foot in a dealership or apply for any loan, pull your credit report from all three major bureaus (Equifax, Experian, TransUnion) via AnnualCreditReport.com. Review them thoroughly for any errors. Disputing inaccuracies can quickly boost your score. Knowing your score beforehand empowers you to negotiate effectively and target lenders who cater to your credit tier.

Improving Your Credit Score Before Applying

If your credit score isn’t where you want it to be, taking steps to improve it before applying for a car loan can save you a substantial amount of money.

- Pay All Bills On Time: This is paramount. Set up reminders or automatic payments to ensure you never miss a due date.

- Reduce Credit Card Balances: Lowering your credit utilization ratio is one of the fastest ways to positively impact your score.

- Avoid New Credit Applications: Limit new credit inquiries in the months leading up to your car loan application.

- Keep Old Accounts Open: Don’t close old, paid-off credit card accounts, as they contribute to your length of credit history and available credit.

- Become an Authorized User: If a trusted family member has excellent credit, becoming an authorized user on their credit card (used responsibly) can sometimes help.

Common mistakes to avoid are applying for multiple lines of credit or closing old accounts immediately before seeking a car loan. These actions can negatively impact your score right when you need it most. Patience and consistent good habits are your best allies in credit improvement.

The Power of the Car Loan APR Calculator

Now that you understand APR and your credit score, it’s time to introduce your most powerful tool in the car buying journey: the Car Loan APR Calculator. This simple yet incredibly effective instrument transforms complex financial calculations into clear, actionable insights. It’s your personal financial analyst, available at your fingertips.

What is a Car Loan APR Calculator?

A car loan APR calculator is an online tool that helps you estimate your potential monthly car payments and the total cost of a loan. You input a few key pieces of information:

- Loan Amount: The total amount of money you wish to borrow.

- APR (Annual Percentage Rate): The estimated interest rate you expect to receive based on your credit score and market conditions.

- Loan Term: The number of months or years you plan to take to repay the loan.

With these inputs, the calculator instantly provides an estimated monthly payment. Many advanced calculators will also show you the total interest you’ll pay over the life of the loan and the total cost of the vehicle, including principal and interest.

Why You MUST Use It

Using a car loan APR calculator is not just a suggestion; it’s a non-negotiable step for any smart car buyer.

- Accurate Budgeting: It allows you to determine a realistic monthly payment that fits comfortably within your budget, preventing you from overextending yourself.

- Effective Offer Comparison: You can input different APRs from various lenders to directly compare which offer provides the best value. This is critical for apples-to-apples comparisons.

- Negotiating Power: Armed with payment estimates, you can walk into a dealership or bank with confidence. You’ll know what a fair payment looks like and won’t be easily swayed by unfavorable terms.

- Understanding Long-Term Costs: The calculator reveals the total interest paid over the loan term, highlighting how longer terms, even with lower monthly payments, can drastically increase the overall cost.

- Avoiding Surprises: There’s nothing worse than signing a loan and later realizing the monthly payments are higher than you anticipated. The calculator helps eliminate these unwelcome surprises.

Based on my experience working with countless car buyers, this calculator is your secret weapon. It shifts the power dynamic, allowing you to make informed decisions rather than relying solely on a salesperson’s figures. It gives you control over your financial future.

How to Use It Effectively

Maximizing the benefits of a car loan APR calculator is straightforward:

- Gather Your Information: Have an estimate of the car’s price, your desired down payment (which helps determine the loan amount), and your estimated APR based on your credit score research.

- Input Values: Enter the loan amount, your expected APR, and various loan terms (e.g., 36, 48, 60, 72 months) into the calculator.

- Experiment with Scenarios: Don’t just run one calculation. Try different APRs (high and low ends of what you might qualify for), different loan terms, and even varying down payment amounts. See how each change impacts your monthly payment and total interest.

- Use It Before You Shop: The most effective time to use the calculator is before you even visit a dealership. This way, you establish your financial boundaries and know what you can genuinely afford.

- Re-evaluate with Real Offers: Once you receive actual loan offers, plug those specific APRs and terms into the calculator to verify the monthly payment and total cost.

Remember, the goal is to find the sweet spot where your monthly payment is manageable, and the total interest paid is minimized. This strategic use of the calculator empowers you to achieve both.

Navigating the Car Loan Application Process

Once you’ve done your homework on APR, understood your credit score, and practiced with the calculator, it’s time to engage with lenders. The application process can vary, but being prepared will make it smoother and more successful.

Pre-Approval vs. Dealership Finance

One of the most critical decisions you’ll make is whether to get pre-approved for a loan before visiting the dealership or to rely on their financing options.

- Pre-Approval Advantages: Getting pre-approved from a bank, credit union, or online lender before you shop is highly recommended. It provides you with a concrete loan offer, including a specific APR and loan amount. This knowledge gives you significant negotiating power at the dealership. You essentially walk in as a cash buyer, knowing your financing is already secured.

- Dealership Finance: Dealerships often work with multiple lenders and can sometimes offer competitive rates, especially through manufacturer incentives. However, it’s always best to have a pre-approval in hand as a benchmark. This allows you to compare their offer against your pre-approved rate and choose the better option. Never let the dealership be your only source of financing.

Documents You’ll Need

Lenders require specific documentation to process your loan application. Having these ready will expedite the process:

- Proof of Income: Pay stubs (recent 2-3 months), W-2 forms, or tax returns (if self-employed).

- Identification: Driver’s license or other government-issued ID.

- Proof of Residence: Utility bill, lease agreement, or mortgage statement.

- Bank Statements: Sometimes required to verify funds or spending habits.

- Social Security Number: For credit checks.

Understanding the Loan Offer

When you receive a loan offer, take your time to review every detail.

- Read the Fine Print: Don’t just glance at the monthly payment. Scrutinize the APR, the total loan amount, the loan term, and any associated fees.

- Look for Hidden Costs: Be wary of add-ons that inflate the loan amount, such as extended warranties or gap insurance, unless you’ve specifically requested and understood them.

- Don’t Rush: Never feel pressured to sign immediately. If you have questions, ask them. If you need time to think, take it. A reputable lender or dealership will respect your need for due diligence.

Common mistakes to avoid include feeling pressured into signing without fully understanding the terms or failing to compare your pre-approved rate against any dealership offers. Always prioritize clarity and your financial well-being.

Strategies for Securing the Best Car Loan APR

Achieving the lowest possible APR on your car loan requires a proactive and strategic approach. It’s about presenting yourself as the most attractive borrower possible and diligently shopping around.

-

Boost Your Credit Score: As repeatedly emphasized, this is your most potent weapon. The higher your score, the lower your perceived risk, and the better your APR. Commit to improving your credit well in advance of your car purchase.

-

Make a Larger Down Payment: Putting more money down reduces the loan amount, which in turn reduces the lender’s risk and can lead to a lower APR. It also means you’ll pay less interest overall and gain equity faster.

-

Choose a Shorter Loan Term (If Affordable): While longer terms offer lower monthly payments, they often come with a slightly higher APR and significantly more interest paid over time. If your budget allows, opt for the shortest loan term you can comfortably manage.

-

Shop Around for Lenders: Never settle for the first loan offer you receive. Contact multiple lenders—banks, credit unions, and online lenders—to compare their APRs and terms. This competitive shopping can reveal significant differences.

- External Link Pro Tip: For more insights on choosing the right lender and understanding loan types, consider resources from the Consumer Financial Protection Bureau (CFPB), a trusted external source for consumer finance education: Consumer Financial Protection Bureau – Auto Loans.

-

Consider a Co-signer (If Credit is Weak): If your credit score is less than ideal, having a co-signer with excellent credit can significantly improve your chances of approval and help you secure a lower APR. Be aware that the co-signer is equally responsible for the loan.

-

Negotiate!: Don’t be afraid to negotiate not just the price of the car, but also the terms of the loan. If you have multiple offers, leverage them. Tell one lender about a better rate you received elsewhere and ask if they can beat or match it.

Pro tips from us: Don’t just accept the first offer. Always get at least three competing quotes for your car loan. This competitive environment often results in lenders offering their best rates to win your business. Remember, every percentage point shaved off your APR can save you hundreds, if not thousands, of dollars over the loan’s lifetime.

Beyond the Calculator: Long-Term Considerations

Securing a great car loan is a significant achievement, but smart financial planning for your vehicle extends beyond the initial purchase. Thinking long-term can save you money and headaches down the road.

Refinancing Your Car Loan

Life changes, and so do financial circumstances. Refinancing your car loan means taking out a new loan to pay off your existing one, ideally with better terms.

- When It Makes Sense: Consider refinancing if your credit score has significantly improved since you took out the original loan, if market interest rates have dropped, or if you initially accepted a high-APR loan due to poor credit. You might also refinance to adjust your monthly payment or loan term.

- How It Works: You apply for a new loan with a different lender (or sometimes the same one). If approved, the new loan pays off the old one, and you begin making payments to the new lender under the new terms. Use a car loan calculator to see how much you could save by refinancing.

The True Cost of Car Ownership

While the monthly loan payment is a major expense, it’s just one piece of the car ownership puzzle. Many people overlook other significant costs.

- Insurance: Car insurance premiums can be substantial and vary widely based on your vehicle, driving history, and location. Get insurance quotes before finalizing your car purchase.

- Maintenance and Repairs: All cars require regular maintenance (oil changes, tire rotations) and will eventually need repairs. Factor these into your budget.

- Fuel: Consider the car’s fuel efficiency and your typical driving habits.

- Registration and Taxes: Annual registration fees and property taxes (in some states) are ongoing costs.

- Depreciation: While not an out-of-pocket expense, depreciation is the loss in value of your car over time. It’s an important consideration, especially if you plan to sell or trade in the vehicle.

Based on my experience, many people overlook these ongoing costs, leading to budget strain down the line. Create a comprehensive budget that includes all aspects of car ownership, not just your loan payment. For more detailed advice on managing these expenses, you might find our guide on "Budgeting for Car Ownership: Beyond the Monthly Payment" insightful.

Conclusion: Drive Smart, Drive Confidently

Congratulations! You’ve navigated the intricate world of car loan APR, credit scores, and the indispensable power of the car loan APR calculator. This journey through financial literacy isn’t just about numbers; it’s about empowering you to make informed decisions that impact your financial well-being for years to come.

Remember, your credit score is your financial passport, influencing the APR you’ll be offered. The APR itself is the true cost of your loan, encompassing both interest and fees. And the car loan APR calculator is your unwavering ally, helping you budget accurately, compare offers effectively, and understand the long-term implications of your choices.

By taking the time to understand these concepts, improve your credit, and strategically use the tools available, you are setting yourself up for success. You’re not just buying a car; you’re investing in smart financial practices. So, go forth, armed with knowledge and confidence, and drive off into the sunset knowing you’ve secured the best possible deal for your dream ride.