Unlock Your Dream Ride: The Ultimate Guide to DCCU Car Loans and How to Drive Away Happy

Unlock Your Dream Ride: The Ultimate Guide to DCCU Car Loans and How to Drive Away Happy Carloan.Guidemechanic.com

Are you dreaming of a new car, a reliable used vehicle, or perhaps looking to lower your current auto loan payments? Navigating the world of car financing can feel overwhelming, but what if there was a local, member-focused institution ready to guide you every step of the way? Enter DuPage Credit Union (DCCU) and their highly competitive car loan offerings.

In this comprehensive guide, we’ll dive deep into everything you need to know about securing a DCCU car loan. From understanding the unique benefits of a credit union to walking you through the application process and sharing expert tips, our goal is to empower you with the knowledge to make the best financial decision for your next vehicle purchase. Get ready to discover how DCCU can help you drive away happy, with a loan that fits your budget and your life.

Unlock Your Dream Ride: The Ultimate Guide to DCCU Car Loans and How to Drive Away Happy

Understanding DCCU: More Than Just a Bank

Before we explore the specifics of their auto loans, it’s crucial to understand what makes DuPage Credit Union, or any credit union for that matter, fundamentally different from a traditional bank. This distinction isn’t just semantics; it directly impacts the benefits you receive as a borrower.

Credit unions are not-for-profit financial cooperatives owned by their members. Unlike banks, which are typically publicly traded companies focused on generating profits for shareholders, credit unions channel their earnings back to their members through lower loan rates, higher savings rates, and reduced fees. This member-centric philosophy is at the core of their operations.

DuPage Credit Union, specifically, has a long-standing commitment to serving its community in the DuPage County area and beyond. Their mission revolves around helping members achieve financial success, and this ethos extends powerfully to their car loan products. When you choose DCCU, you’re not just a customer; you’re a part-owner, and that relationship often translates into a more personalized and advantageous borrowing experience.

Why Consider a DCCU Car Loan? The Unbeatable Advantages

When it comes to financing a vehicle, you have many options. So, why should DuPage Credit Union be high on your list? Based on my experience in the financial landscape, DCCU car loans offer several distinct advantages that can significantly benefit borrowers.

1. Competitive Interest Rates

One of the most compelling reasons to choose a credit union like DCCU for your car loan is the potential for lower interest rates. Because they are not-for-profit, credit unions can often pass on savings to their members in the form of more attractive Annual Percentage Rates (APRs) compared to traditional banks. This can translate into substantial savings over the life of your loan. A lower interest rate means more of your monthly payment goes towards the principal of your car, reducing the total cost of ownership.

2. Flexible Loan Terms Designed for You

DCCU understands that every borrower’s financial situation is unique. They typically offer a wide range of loan terms, allowing you to choose a repayment schedule that aligns with your budget and financial goals. Whether you prefer a shorter term to pay off your loan faster and save on interest, or a longer term to keep your monthly payments more manageable, DCCU aims to provide options. This flexibility is key to responsible borrowing and ensuring your car payment isn’t a strain.

3. Personalized Member Service

This is where the credit union difference truly shines. Unlike the often-impersonal experience at larger banks, DCCU prides itself on providing individualized attention. Their loan officers take the time to understand your specific needs, answer your questions, and guide you through the process with clarity and empathy. This personalized approach can be invaluable, especially if you have unique circumstances or are a first-time car buyer.

4. The Power of Pre-Approval

Getting pre-approved for a car loan with DCCU is a game-changer in the car buying process. Pre-approval gives you a clear understanding of how much you can afford before you even step foot in a dealership. This financial clarity empowers you to negotiate with confidence, knowing your budget and secured financing. Dealers often take pre-approved buyers more seriously, potentially leading to a smoother purchasing experience and better deals.

5. Local Community Focus and Support

As a community-focused institution, DCCU is deeply invested in the financial well-being of its members and the local economy. By choosing a DCCU car loan, you’re not just getting great rates and service; you’re also supporting an organization that actively contributes to the local community. This reciprocal relationship often fosters a sense of trust and loyalty that you might not find elsewhere.

Types of DCCU Car Loans: Tailored to Your Needs

DuPage Credit Union offers a variety of auto loan products designed to meet different member needs, whether you’re buying new, used, or looking to refinance your existing loan. Understanding these options is the first step towards choosing the right fit.

1. New Car Loans

If you’re eyeing a brand-new vehicle fresh off the lot, DCCU offers competitive loans specifically for new cars. These loans typically come with the most favorable interest rates and longest terms, reflecting the lower risk associated with financing a new asset. They understand the excitement of a new purchase and aim to make the financing part as smooth as possible.

When applying for a new car loan, you’ll generally need the vehicle’s make, model, year, and VIN (Vehicle Identification Number) once you’ve made your selection. DCCU’s pre-approval process is particularly beneficial here, allowing you to shop for your new car with financing already in hand.

2. Used Car Loans

Purchasing a used car can be a smart financial move, and DCCU provides excellent options for pre-owned vehicles. While used car loan rates might be slightly higher than new car rates, and terms can be a bit shorter due to the vehicle’s age and depreciation, DCCU strives to keep them competitive. They often have specific guidelines regarding the maximum age or mileage of a used car they will finance, so it’s wise to inquire about these specifics beforehand.

Pro tips from us: When considering a used car, always have it inspected by an independent mechanic. This extra step can save you from unforeseen repair costs down the road, and ensures the vehicle is a sound investment for your DCCU loan.

3. Auto Loan Refinancing

Perhaps you already have a car loan but are looking for a better deal. DCCU’s auto loan refinancing option could be your solution. Refinancing involves taking out a new loan, often with a lower interest rate or different terms, to pay off your existing car loan. This can lead to lower monthly payments, significant savings on interest over time, or a shorter repayment period.

Common reasons to refinance with DCCU include:

- Lowering your interest rate: If your credit score has improved since you first took out your loan, or if market rates have dropped.

- Reducing your monthly payment: By extending your loan term (though this might increase total interest paid).

- Shortening your loan term: To pay off your car faster and save on interest (this might increase your monthly payment).

4. Lease Buyout Loans

For those currently leasing a vehicle, DCCU may also offer lease buyout loans. At the end of a lease term, you often have the option to purchase the car for a predetermined residual value. A lease buyout loan from DCCU can provide the financing needed to exercise this option, allowing you to own the vehicle you’ve been driving. This can be a great choice if you love your leased car and want to avoid depreciation hit on a new car.

The DCCU Car Loan Application Process: A Step-by-Step Guide

Applying for a DCCU car loan is a straightforward process, especially when you know what to expect. Following these steps will help ensure a smooth and efficient experience, getting you closer to driving your new or used vehicle.

Step 1: Become a Member (If You Aren’t Already)

Since DCCU is a credit union, you’ll need to be a member to access their financial products, including car loans. Membership eligibility typically revolves around a common bond, such as living, working, or worshipping in specific geographic areas (like DuPage County), or being related to an existing member.

Check DCCU’s website or contact them directly to confirm your eligibility. Becoming a member usually involves opening a savings account with a small initial deposit, which then grants you access to all their services.

Step 2: Gather Your Essential Documents

Preparation is key to a swift application process. Before you apply, have the following documents and information readily available:

- Proof of Identity: Government-issued ID (driver’s license, state ID, passport).

- Proof of Income: Recent pay stubs (last 2-3), W-2s, or tax returns (if self-employed). This helps DCCU assess your ability to repay the loan.

- Proof of Residence: Utility bill, lease agreement, or mortgage statement.

- Social Security Number: For credit history verification.

- Vehicle Information (if already selected): Make, model, year, VIN, mileage (for used cars), and selling price.

- Trade-in Information (if applicable): Details about your current vehicle if you plan to trade it in.

Common mistakes to avoid are not gathering all necessary documents beforehand, which can lead to delays in your application. Having everything organized will streamline the process.

Step 3: Get Pre-Approved – Your Secret Weapon

We cannot stress enough the importance of pre-approval. This step is crucial for gaining leverage at the dealership and understanding your budget.

What is Pre-Approval? It’s a conditional commitment from DCCU stating that they are willing to lend you a certain amount of money, at a specific interest rate, based on your creditworthiness and financial situation. It’s not a final loan, but it gives you a powerful estimate.

How to Apply for Pre-Approval: You can typically apply for pre-approval online through the DCCU website, by phone, or by visiting a branch in person. The application will ask for your personal financial information, employment details, and how much you wish to borrow. DCCU will then perform a credit check.

Benefits of Pre-Approval:

- Clear Budget: You know exactly how much car you can afford.

- Bargaining Power: You walk into the dealership as a cash buyer, not dependent on their financing. This can often lead to a better vehicle price.

- Faster Purchase: Once you find the car, the final loan process is much quicker.

Step 4: Submit Your Full Application

Once you’ve been pre-approved or are ready to apply for a specific vehicle, you’ll complete the full loan application. This will include all the details of the car you intend to purchase. Whether you apply online, over the phone, or in person, ensure all information is accurate and complete.

Step 5: Loan Review and Approval

After submitting your application, DCCU’s loan officers will review all your information, including your credit history, income, and the details of the vehicle. They may contact you for additional documentation or clarification.

The timeframe for approval can vary, but credit unions are often known for their efficient processing. For pre-approved members, this step is usually very quick.

Step 6: Closing the Deal and Funding

Once your loan is approved, you’ll receive a loan agreement outlining all the terms, including the interest rate, monthly payment, and total loan amount. Read this document carefully.

After you sign the agreement, DCCU will disburse the funds directly to the dealership or, in the case of refinancing, to your previous lender. Congratulations, you’re ready to drive away in your new car!

Understanding Key Factors Affecting Your DCCU Car Loan

Several critical factors influence the terms and approval of your DCCU car loan. Being aware of these elements can help you prepare and potentially secure the best possible deal.

1. Your Credit Score

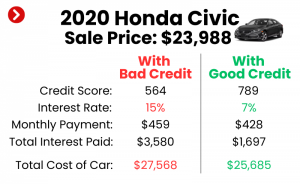

Your credit score is arguably the most significant factor lenders consider. It’s a numerical representation of your creditworthiness, based on your payment history, amounts owed, length of credit history, new credit, and credit mix. A higher credit score (generally above 700) indicates a lower risk to lenders and typically qualifies you for the lowest interest rates.

If your credit score isn’t where you’d like it to be, taking steps to improve it before applying can save you thousands of dollars over the life of the loan. This might include paying down existing debts, making all payments on time, and avoiding new credit applications.

2. Debt-to-Income (DTI) Ratio

Your Debt-to-Income (DTI) ratio is the percentage of your gross monthly income that goes towards paying your monthly debt payments. Lenders use this to assess your ability to take on new debt. A lower DTI ratio (typically below 36-43%) indicates you have more disposable income to cover your car loan payments.

DCCU will look at your DTI to ensure the new car loan won’t overextend your finances, helping to prevent financial strain for their members.

3. Loan Term (Repayment Period)

The loan term is the length of time you have to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72, 84 months).

- Shorter Terms: Result in higher monthly payments but lower total interest paid over the life of the loan. You pay off the car faster.

- Longer Terms: Result in lower monthly payments but higher total interest paid. The car takes longer to pay off, and you might owe more than the car is worth for a longer period (being "upside down" on your loan).

Choosing the right term is a balance between affordability and minimizing interest costs.

4. Down Payment

Making a down payment means paying a portion of the car’s purchase price upfront. This reduces the amount you need to borrow, which in turn lowers your monthly payments and the total interest you’ll pay.

Benefits of a Down Payment:

- Lower Loan Amount: Reduces your overall debt.

- Better Interest Rates: Lenders see you as less of a risk.

- Reduced Negative Equity: Helps prevent you from owing more than the car is worth, especially in the early years of the loan.

- Lower Monthly Payments: Frees up cash flow.

While a down payment isn’t always required, even a small one can significantly improve your loan terms.

5. Vehicle Age and Mileage (for Used Cars)

For used car loans, the age and mileage of the vehicle can affect the loan terms. Older cars or those with very high mileage are generally considered higher risk due to potential maintenance issues and faster depreciation. This can lead to slightly higher interest rates or shorter maximum loan terms. DCCU will have specific guidelines on what types of used vehicles they can finance.

6. Interest Rates (APR)

The Annual Percentage Rate (APR) is the total cost of borrowing money, expressed as a yearly percentage. It includes the interest rate plus any fees associated with the loan. A lower APR means your loan is cheaper.

DCCU’s competitive APRs are a major draw. Your specific APR will depend on your credit score, DTI ratio, the loan term, and the vehicle itself. Always compare the APR, not just the quoted interest rate, when evaluating loan offers.

Making the Most of Your DCCU Car Loan: Pro Tips and Smart Strategies

Securing a DCCU car loan is a fantastic start, but there are always ways to optimize your borrowing experience and maximize your savings. Here are some pro tips from us to help you get the most out of your auto loan.

1. Don’t Just Settle – Compare and Negotiate

Even with DCCU’s competitive rates, it’s always wise to compare their offer with one or two other reputable lenders. This due diligence ensures you’re getting the best possible deal. However, remember the added value of DCCU’s personalized service and member benefits. Once you have a pre-approval from DCCU, use it as leverage when negotiating the car’s price at the dealership. You’re empowered to focus on the vehicle price, knowing your financing is secured.

2. Understand All the Details: Beyond the Monthly Payment

Pro tips from us: Always read the fine print of your loan agreement. Don’t just focus on the monthly payment. Understand the total amount you’ll pay over the loan term, any potential fees, and prepayment penalties (though DCCU typically avoids these). Ensure you’re comfortable with all aspects of the agreement before signing.

3. Consider Automatic Payments

Setting up automatic payments from your checking account is a smart move. It ensures you never miss a payment, which protects your credit score and helps you avoid late fees. Many lenders, including credit unions, might even offer a slight interest rate discount for setting up autopay. It’s a convenient way to stay on track financially.

4. Pay More When You Can (If No Prepayment Penalties)

If your DCCU loan doesn’t have prepayment penalties (which is common for credit unions), consider paying a little extra each month or making an additional payment whenever you have extra funds. Even small extra payments can significantly reduce the principal balance, leading to less interest paid over the life of the loan and a faster payoff. Clearly specify that any extra payments should go directly towards the principal.

5. Review Your Loan Regularly – Is Refinancing an Option?

Life changes, and so do financial markets. Keep an eye on interest rates. If your credit score has significantly improved since you took out your DCCU loan, or if general interest rates have dropped, it might be worth exploring refinancing options again, even with DCCU itself. They might be able to offer you an even better rate, further reducing your costs.

6. Factor in Related Costs: Insurance and Warranties

Remember that a car loan is just one part of vehicle ownership. Don’t forget to budget for car insurance, which is legally required and often a condition of your loan. Also consider extended warranties, especially for used vehicles, but evaluate their value carefully. DCCU can sometimes offer competitive rates on related insurance products or connect you with trusted providers.

FAQs About DCCU Car Loans

Here are answers to some frequently asked questions about DuPage Credit Union car loans, providing quick insights for common queries.

Q1: Can I apply for a DCCU car loan online?

A1: Yes, DCCU typically offers a convenient online application process for both pre-approval and full loan applications. You can usually apply from the comfort of your home.

Q2: What credit score do I need for a DCCU car loan?

A2: While DCCU works with members across a range of credit scores, a higher score will generally qualify you for the best rates. They assess each application individually, considering various factors beyond just the score.

Q3: How long does it take to get approved for a DCCU car loan?

A3: Approval times can vary, but pre-approvals can often be processed quickly, sometimes within hours or one business day. Full loan approval once you have a specific vehicle is also generally efficient for DCCU members.

Q4: Can I refinance a car loan from another bank or credit union with DCCU?

A4: Absolutely. DCCU offers auto loan refinancing services, which can be a great way to potentially lower your interest rate, reduce your monthly payments, or adjust your loan terms.

Q5: Do I need to be a DCCU member before applying for a car loan?

A5: Yes, you must be a member of DuPage Credit Union to access their car loan products. However, becoming a member is usually a simple process, often initiated when you apply for your loan.

Drive Away with Confidence: Your DCCU Car Loan Journey

Securing a car loan is a significant financial decision, and choosing the right lender can make all the difference. DuPage Credit Union stands out as an exceptional option, offering not just competitive rates and flexible terms, but also a deeply personalized, member-focused service that you might not find elsewhere. Their commitment to their community and their members’ financial well-being translates into a car loan experience designed to empower you.

By understanding the types of loans available, preparing for the application process, and leveraging the power of pre-approval, you can navigate your car buying journey with confidence. Remember the value of a strong credit score, a manageable debt-to-income ratio, and the wisdom of making a down payment. With DCCU, you’re not just getting a loan; you’re gaining a financial partner dedicated to helping you achieve your automotive dreams.

Ready to take the next step towards your dream car? Explore DuPage Credit Union’s car loan options today and discover how easy and rewarding the process can be. Your ideal ride awaits!