Unlock Your Dream Ride: The Ultimate Guide to Getting a Pre-Approved Used Car Loan

Unlock Your Dream Ride: The Ultimate Guide to Getting a Pre-Approved Used Car Loan Carloan.Guidemechanic.com

Buying a used car can be an exciting journey, offering fantastic value and a wide array of choices. However, for many, the financing aspect often casts a shadow of uncertainty over the entire process. Walking into a dealership without a clear understanding of your financial standing can feel like navigating a maze blindfolded, leaving you vulnerable to high-pressure sales tactics and less-than-ideal loan terms.

This is where the power of a Pre-Approved Used Car Loan comes into play. It’s not just a convenience; it’s your strategic advantage, transforming you from a hopeful buyer into a confident negotiator. Imagine knowing exactly how much you can spend, what your interest rate will be, and what your monthly payments look like before you even set foot on a car lot. This isn’t just a dream; it’s a very achievable reality.

Unlock Your Dream Ride: The Ultimate Guide to Getting a Pre-Approved Used Car Loan

In this super comprehensive guide, we’ll deep dive into everything you need to know about securing a pre-approved used car loan. We’ll explore its profound benefits, walk you through the step-by-step application process, reveal expert tips, and highlight common pitfalls to avoid. Our ultimate goal is to empower you with the knowledge and confidence to secure the best possible financing, ensuring your used car purchase is smooth, transparent, and financially sound.

Let’s embark on this journey to transform your used car buying experience.

What Exactly is a Pre-Approved Used Car Loan? Your Financial Passport Explained

Before we delve into the ‘how-to,’ it’s crucial to understand precisely what a pre-approved used car loan entails. Many people confuse pre-qualification with pre-approval, but there’s a significant difference that can impact your car buying power.

A pre-approved used car loan is a conditional offer from a lender to provide you with a specific amount of money to purchase a used vehicle, at a particular interest rate, and for a set loan term. This offer is based on a thorough review of your credit history, income, and financial stability. Unlike a pre-qualification, which is typically a soft inquiry and a preliminary estimate, a pre-approval involves a hard credit inquiry and represents a more concrete commitment from the lender.

Think of it as receiving a financial passport before your trip. You know your travel budget, where you can go, and what you can afford, rather than just hoping you have enough money when you arrive. This clarity empowers you immensely in the car buying process. Based on my experience, securing pre-approval is one of the smartest financial moves any used car buyer can make.

The lender scrutinizes your financial health to determine your eligibility and the terms they’re willing to offer. They assess factors like your debt-to-income ratio, employment history, and of course, your credit score. If approved, you receive an official letter or document detailing the maximum loan amount, the interest rate, and the loan duration. This document is your proof of financing, ready to be presented at any dealership.

Why Pre-Approval is Your Secret Weapon in Used Car Buying: Unpacking the Benefits

Securing a pre-approved used car loan offers a multitude of advantages that can dramatically improve your car buying experience. It shifts the power dynamic from the seller to you, the buyer.

Here are the key benefits you stand to gain:

1. Crystal-Clear Budgetary Confidence

One of the biggest anxieties in car shopping is not knowing how much you can truly afford. A pre-approved loan eliminates this uncertainty entirely. You’ll know your maximum spending limit, your exact interest rate, and your estimated monthly payment before you even start browsing vehicles.

This clarity allows you to focus solely on finding a car that fits both your needs and your confirmed budget. It prevents the heartbreak of falling in love with a car only to discover it’s financially out of reach.

2. Enhanced Negotiation Power at the Dealership

Imagine walking onto a car lot with your financing already secured. You’re not just another customer hoping to get approved; you’re effectively a cash buyer in the eyes of the dealership. This significantly boosts your negotiation leverage.

When you have your own financing, the dealership knows they can’t make extra profit by marking up the interest rate. This allows you to negotiate solely on the vehicle’s price, potentially saving you thousands. Pro tips from us: always let them know you’re pre-approved early in the negotiation.

3. Significant Time Savings and a Streamlined Process

The traditional car buying process can be incredibly time-consuming, with hours spent haggling over prices and then waiting for financing approval. Pre-approval drastically cuts down this time. You’ve already completed the most tedious part of the financing process.

At the dealership, your focus shifts directly to finding the right car and finalizing the paperwork. This means less waiting around, less stress, and a much more efficient overall experience.

4. Reduced Stress and a More Enjoyable Experience

Car shopping should be exciting, not stressful. When you’re pre-approved, the pressure of getting approved for a loan is completely removed. You can relax and enjoy the process of test driving and comparing vehicles.

You’re no longer at the mercy of the dealership’s finance department or worried about being rejected. This peace of mind is invaluable and makes the entire car acquisition process much more pleasant.

5. Protection Against Dealership Upselling and Hidden Fees

Dealerships often make a significant portion of their profit from financing. Without pre-approval, you might be persuaded into higher interest rates, longer loan terms, or unnecessary add-ons to boost their bottom line.

Your pre-approval acts as a shield. You have a solid alternative if the dealership’s financing offer isn’t competitive. This empowers you to decline offers that don’t serve your best interests.

6. Access to Potentially Better Interest Rates and Terms

While dealerships can offer competitive rates, they are sometimes limited to a handful of lenders. By seeking pre-approval independently, you can shop around with multiple banks, credit unions, and online lenders. This broadens your options and increases your chances of securing the absolute best interest rate and most favorable terms available to you.

Based on my experience, independent shopping nearly always yields better rates for well-qualified buyers compared to solely relying on dealership financing.

The Step-by-Step Guide to Getting Pre-Approved for a Used Car Loan

Navigating the pre-approval process might seem daunting, but it’s straightforward when broken down into manageable steps. Follow this guide to confidently secure your financing.

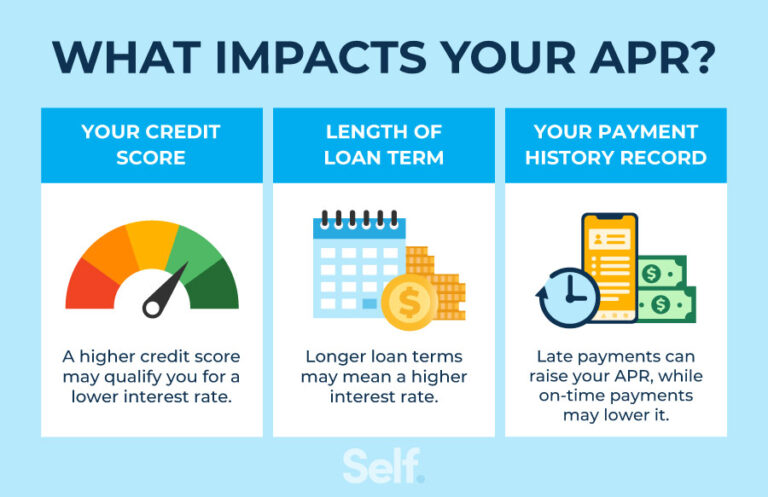

Step 1: Check Your Credit Score and Report

Your credit score is arguably the most critical factor lenders consider. It tells them how reliable you are as a borrower. Before applying, obtain your credit score and review your credit report for any errors.

Lenders typically look for scores in the good to excellent range (generally 670 and above) for the most favorable rates. A higher score signifies lower risk, leading to better loan terms. If your score is lower, consider taking steps to improve it before applying. For more detailed advice on boosting your credit, you might find our article on incredibly helpful.

Step 2: Gather All Necessary Documentation

Lenders require specific documents to verify your identity, income, and residence. Having these ready will significantly speed up your application process.

Common documents include:

- Proof of Identity: Government-issued ID (driver’s license, passport).

- Proof of Income: Recent pay stubs (usually 2-3 months), W-2 forms, tax returns (if self-employed), or bank statements.

- Proof of Residence: Utility bill, lease agreement, or mortgage statement.

- Social Security Number: For credit checks.

- Vehicle Information (if applicable): Though for pre-approval, you usually don’t need a specific car in mind yet.

Step 3: Research and Compare Lenders

Don’t just go with the first lender you find. Different financial institutions offer varying rates and terms based on their risk assessment and business models.

Consider the following types of lenders:

- Banks: Large national and regional banks often have competitive rates, especially for existing customers.

- Credit Unions: Known for member-focused services and often lower interest rates due to their non-profit structure.

- Online Lenders: Many reputable online platforms specialize in auto loans and can offer quick approvals and competitive rates.

- Dealerships (for comparison): While you’re getting pre-approved elsewhere, it’s still wise to see what the dealer offers as a point of comparison.

Apply with 2-3 lenders within a short window (typically 14-45 days, depending on the credit scoring model). This allows multiple hard inquiries for the same type of loan to be counted as a single inquiry, minimizing the impact on your credit score.

Step 4: Submit Your Application

Once you’ve chosen your preferred lenders, submit your pre-approval application. This can often be done online, over the phone, or in person at a branch.

You’ll need to provide personal information, financial details, and consent for a credit check. Be accurate and thorough; any discrepancies could delay your approval.

Step 5: Review the Offer Carefully

If approved, the lender will present you with a loan offer. This document is critical and outlines the terms of your potential loan.

Pay close attention to:

- Annual Percentage Rate (APR): This is the true cost of your loan, including interest and fees.

- Loan Term: The length of time you have to repay the loan (e.g., 36, 48, 60 months). Longer terms mean lower monthly payments but more interest paid overall.

- Maximum Loan Amount: The highest amount the lender is willing to finance.

- Monthly Payment Estimate: What your payments would likely be.

- Any Fees: Origination fees, processing fees, etc.

Ensure you understand every aspect of the offer before moving forward.

Step 6: Get Your Pre-Approval Letter

Upon accepting a pre-approval offer, the lender will issue an official pre-approval letter or certificate. This document is your golden ticket.

It confirms your approved loan amount, interest rate, and the validity period (usually 30-60 days). Keep this letter safe, as you’ll need to present it to the dealership when you find your perfect used car.

Navigating the Dealership with Your Pre-Approval in Hand

Having a pre-approval letter changes your entire dynamic at the dealership. You’re no longer solely dependent on their financing department.

Here’s how to use it effectively:

- Lead with Your Pre-Approval: When discussing pricing, inform the salesperson that you already have financing secured. This immediately sets a serious tone for negotiations on the car’s price.

- Focus on the Car Price: Your primary goal now is to negotiate the lowest possible selling price for the vehicle. Since your loan is separate, you can keep the discussions focused purely on the car itself.

- Compare Dealer Financing: Even with your pre-approval, it’s still a good idea to ask the dealership about their financing options. Sometimes, they might have special promotions or work with a lender who can beat your pre-approved rate. If they offer a better deal, you’re free to take it!

- Don’t Feel Pressured: Remember, your pre-approval gives you an exit strategy. If you don’t like the dealer’s financing or if you feel pressured, you always have your pre-approved loan to fall back on. You’re in control.

Common Mistakes to Avoid When Seeking a Pre-Approved Used Car Loan

Even with the best intentions, certain missteps can hinder your pre-approval process or lead to less favorable outcomes. Common mistakes to avoid are crucial for a smooth experience.

Here are some pitfalls to steer clear of:

- Not Checking Your Credit First: Going into the application process blind to your credit score is a major oversight. This can lead to applying for loans you won’t qualify for, or being surprised by high interest rates. Always review your credit report and score beforehand.

- Applying with Too Many Lenders Simultaneously (Incorrectly): While shopping around is good, submitting applications to dozens of lenders within a short period can potentially lower your credit score if not handled correctly. Stick to 2-3 reputable lenders within the credit inquiry window to minimize impact.

- Not Understanding the Terms of the Offer: It’s easy to get excited about an approval, but glossing over the APR, loan term, and any hidden fees can be costly. Always read the fine print and ask questions until you fully understand every detail.

- Ignoring Your Budget Beyond the Monthly Payment: A low monthly payment might seem attractive, but it could be tied to a very long loan term, meaning you pay significantly more interest over time. Factor in the total cost of the loan, not just the monthly figure.

- Getting Pre-Approved for Too Much: Just because you’re approved for a certain amount doesn’t mean you should spend it all. Over-borrowing can lead to financial strain and ‘buyer’s remorse.’ Stick to a budget that comfortably fits your overall financial situation.

- Not Bringing the Pre-Approval Letter: This seems obvious, but people forget! Your physical or digital pre-approval letter is your proof of financing. Without it, you might lose some negotiation leverage or face delays.

Beyond Pre-Approval: Smart Tips for Buying Your Used Car

While securing a pre-approved used car loan is a massive step, the journey isn’t over. A few more strategic moves can ensure you drive away with the perfect vehicle.

- Budget for the Total Cost of Ownership: Beyond the loan, remember to factor in insurance, registration, taxes, potential maintenance, and fuel costs. A lower monthly car payment means little if the car itself is a money pit.

- Get a Pre-Purchase Inspection (PPI): This is non-negotiable for used cars. Have an independent, trusted mechanic inspect the vehicle thoroughly before you buy it. They can uncover hidden issues that might save you from significant repair costs down the line. This small investment can save you thousands.

- Test Drive Thoroughly: Don’t just take it around the block. Drive the car on different types of roads, at various speeds, and pay attention to any unusual noises, vibrations, or handling issues. Ensure it feels comfortable and safe for your daily needs.

- Understand Vehicle History Reports: Services like CarFax or AutoCheck provide valuable insights into a car’s past, including accident history, previous owners, and service records. Always review these reports diligently. You can learn more about assessing used car value and history at a trusted resource like Edmunds.com (External Link: https://www.edmunds.com/car-buying/how-to-get-a-carfax-report.html – Note: This is an example, actual link may vary).

- Negotiate Wisely: Remember your pre-approval is your biggest bargaining chip. Be firm but polite, and don’t be afraid to walk away if you don’t feel the deal is fair. Patience is key in negotiations. For a deeper dive into negotiation tactics, check out our guide on

.

Conclusion: Drive Away with Confidence

Securing a Pre-Approved Used Car Loan is more than just a financial transaction; it’s an empowering step that puts you firmly in the driver’s seat of your used car buying journey. By taking the time to understand the process, prepare your finances, and shop for the best loan terms, you gain invaluable advantages. You’ll approach dealerships with confidence, armed with a clear budget and robust negotiation power.

No longer will you face the uncertainty and pressure that often accompanies car financing. Instead, you’ll enjoy a streamlined, transparent, and ultimately more satisfying experience. We hope this comprehensive guide has equipped you with all the knowledge you need to successfully navigate the world of used car financing.

Now, go forth, get pre-approved, and drive away in your dream used car with the peace of mind that comes from making a smart financial decision. Your perfect ride awaits!