Unlock Your Dream Ride: The Ultimate Guide to NFCU Used Car Loans

Unlock Your Dream Ride: The Ultimate Guide to NFCU Used Car Loans Carloan.Guidemechanic.com

The open road calls, and for many, a reliable used car is the perfect answer. It offers significant savings compared to a new vehicle while still providing the freedom and functionality you need. But navigating the world of used car financing can feel like a complex maze. This is where a trusted partner like Navy Federal Credit Union (NFCU) steps in, offering tailored solutions for its members.

For military personnel, veterans, and their families, NFCU isn’t just a bank; it’s a financial ally. When it comes to securing a used car loan, they stand out with competitive rates, flexible terms, and a member-first approach that can truly make a difference. This comprehensive guide will deep dive into everything you need to know about securing an NFCU used car loan, empowering you to drive away with confidence and a smart financial decision.

Unlock Your Dream Ride: The Ultimate Guide to NFCU Used Car Loans

Why Choose NFCU for Your Used Car Loan?

Deciding where to finance your used car is a crucial step, and NFCU presents a compelling case for its members. Their unique structure as a credit union means they operate differently from traditional banks, often translating into better deals and a more personalized experience.

Firstly, NFCU’s core mission is to serve its members, not external shareholders. This fundamental difference means that profits are often reinvested into the credit union, allowing them to offer more favorable rates and terms on loans, including those for used cars. It’s a financial philosophy centered around mutual benefit, which directly impacts your bottom line.

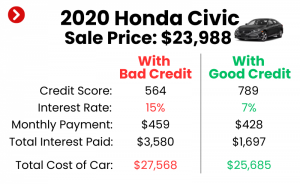

Secondly, based on my experience, credit unions like NFCU often provide significantly more competitive interest rates compared to many commercial banks. This isn’t just a small difference; even a fraction of a percentage point can save you hundreds, if not thousands, of dollars over the life of your loan. Their commitment to offering affordable financing makes a real impact on your monthly payments and overall loan cost.

Finally, the level of customer service at NFCU is consistently highly rated. They understand the unique financial situations of military families and strive to make the loan process as smooth and straightforward as possible. From application to closing, you can expect clear communication and support, which is invaluable when making a significant purchase like a vehicle.

Understanding NFCU Used Car Loan Eligibility

Before you even start browsing vehicles, it’s essential to understand the eligibility requirements for an NFCU used car loan. This preparation will streamline your application process and increase your chances of approval.

The primary requirement, of course, is NFCU membership. Eligibility extends to all branches of the armed forces (Army, Marine Corps, Navy, Air Force, Coast Guard, Space Force), Department of Defense civilian employees, and their immediate family members. If you’re not yet a member, joining is a straightforward process that can open doors to a host of financial benefits, including their competitive auto loans.

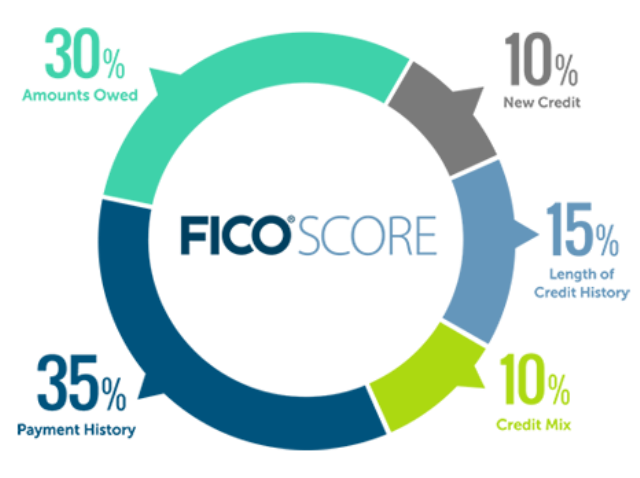

Beyond membership, your credit score plays a significant role in determining your loan eligibility and the interest rate you’ll receive. While NFCU doesn’t publish a minimum credit score, a higher score generally indicates lower risk to lenders, leading to better rates. Aiming for a good to excellent credit score (typically 670 and above) is always advisable for the most favorable terms.

NFCU will also assess your overall financial health, looking at factors like your income and debt-to-income (DTI) ratio. They want to ensure you have a stable income to comfortably afford the monthly payments, and that your existing debt obligations aren’t too high in relation to your earnings. A lower DTI ratio signals a healthier financial position.

Lastly, the vehicle itself must meet certain criteria for an NFCU used car loan. While they finance a wide range of used vehicles, there are usually restrictions on age and mileage. For example, vehicles typically need to be no more than a certain number of years old (e.g., 8-10 years) and have mileage below a specific threshold. The vehicle’s value, often determined by resources like Kelley Blue Book (KBB) or NADAguides, will also be a factor in how much NFCU is willing to lend.

Pro tip from us: Before applying, pull your credit report from all three major bureaus (Equifax, Experian, TransUnion) to check for any errors and get a clear picture of your credit standing. Addressing inaccuracies beforehand can significantly improve your loan prospects.

The NFCU Used Car Loan Application Process: Step-by-Step

Navigating the application process for an NFCU used car loan can be surprisingly straightforward, especially if you approach it strategically. Following these steps will help ensure a smooth and successful experience.

Step 1: Get Pre-approved (Crucial!)

This is perhaps the single most important step in the entire used car buying journey. Getting pre-approved for an NFCU used car loan means NFCU has already reviewed your finances and determined how much they are willing to lend you, along with an estimated interest rate. It’s like having cash in your pocket before you even step foot on a dealership lot.

The benefits of pre-approval are immense. Firstly, it sets a clear budget, preventing you from falling in love with a car you can’t truly afford. Secondly, it gives you incredible negotiating power with sellers, as you’re effectively a cash buyer. You can focus on the vehicle’s price, not on the financing terms the dealer might try to push. Thirdly, it speeds up the actual purchase process significantly, allowing you to drive off the lot sooner.

To apply for pre-approval, you’ll typically need to provide personal information, employment details, income verification, and a summary of your existing debts. You can apply online, over the phone, or in person at an NFCU branch. The process is generally quick, and you’ll usually receive a decision within a day or two.

Step 2: Finding Your Dream Car

With your NFCU pre-approval in hand, you’re now in a powerful position to shop for your used car. This is where the fun begins! Start by researching different makes and models that fit your needs and budget. Consider factors like reliability, fuel efficiency, safety ratings, and insurance costs.

You can search for vehicles through various channels:

- Dealerships: Both new car dealerships with used car inventories and dedicated used car lots.

- Private Sellers: Often found through online marketplaces or local classifieds, private sales can sometimes offer lower prices but require more due diligence.

- NFCU’s Car Buying Service: We’ll discuss this more later, but it’s a fantastic resource for members.

Once you’ve identified a potential vehicle, always arrange for a pre-purchase inspection by an independent, trusted mechanic. This small investment can save you from costly repairs down the road. Also, obtain a vehicle history report (like CarFax or AutoCheck) to check for accidents, flood damage, or title issues.

Step 3: Finalizing Your Loan

Once you’ve found the perfect used car and agreed on a price with the seller, the final steps for your NFCU used car loan are relatively simple. You’ll provide NFCU with the vehicle’s details, including the VIN, mileage, and purchase price. If you purchased from a dealership, they often handle much of the paperwork directly with NFCU. For private sales, you’ll work more closely with NFCU to ensure all documentation, such as the title transfer, is correctly handled.

NFCU will then review the vehicle information against their lending criteria and your pre-approval terms. Assuming everything aligns, they will finalize the loan, and the funds will be disbursed to the seller. You’ll then sign the final loan documents, outlining your exact interest rate, monthly payment, and loan term.

Common mistakes to avoid are: Not getting pre-approved, as this can lead to emotional purchases or less favorable financing terms offered by dealerships. Another common pitfall is skipping the independent vehicle inspection, which can leave you vulnerable to unexpected repair costs shortly after purchase.

NFCU Used Car Loan Rates and Terms

Understanding the nuances of interest rates and loan terms is crucial for securing the most affordable NFCU used car loan. These factors directly impact your monthly payments and the total amount you’ll pay over the life of the loan.

Several key factors influence the interest rate you’ll receive on your NFCU used car loan. Your credit score is paramount; a higher score generally translates to a lower Annual Percentage Rate (APR). The loan term also plays a role; shorter terms (e.g., 36 or 48 months) often come with slightly lower rates than longer terms (e.g., 72 or 84 months), though they result in higher monthly payments. The age and mileage of the used vehicle can also affect the rate, as older, higher-mileage cars may be seen as a slightly higher risk.

It’s important to differentiate between the interest rate and the APR. The interest rate is simply the cost of borrowing the principal amount. The APR, however, includes the interest rate plus any additional fees associated with the loan, giving you a more comprehensive picture of the true annual cost of borrowing. Always compare APRs when evaluating loan offers, as it provides a more accurate apples-to-apples comparison.

NFCU offers flexible loan terms, typically ranging from 12 to 84 months for used vehicles. While a longer loan term means lower monthly payments, it also means you’ll pay more in interest over time. Conversely, a shorter term leads to higher monthly payments but significantly less interest paid overall. It’s about finding the right balance that fits your budget and financial goals.

Pro tip from us: Look out for any special offers or discounts NFCU might have, such as rate reductions for setting up automatic payments from an NFCU checking account, or for using their Car Buying Service. These small reductions can add up to meaningful savings.

Beyond the Loan: Maximizing Your NFCU Benefits

NFCU’s commitment to its members extends far beyond simply approving your used car loan. They offer a suite of services and protections designed to enhance your car buying experience and safeguard your investment. Leveraging these additional benefits can provide peace of mind and further financial advantages.

One of the most valuable resources for members is the NFCU Car Buying Service. Powered by TrueCar, this service allows you to research vehicles, compare prices, and connect with certified dealers who offer pre-negotiated, upfront pricing. Based on my experience, this can save you a significant amount of time and stress by taking the guesswork out of price negotiations. It’s a fantastic way to ensure you’re getting a fair deal without the typical back-and-forth at the dealership.

NFCU also offers various loan protection options to shield you from unexpected financial burdens. Guaranteed Asset Protection (GAP) insurance is particularly relevant for used car loans. If your car is totaled or stolen, GAP coverage pays the difference between what your insurance company pays out and the remaining balance on your loan, preventing you from being upside down on your loan. They also offer Payment Protection, which can help cover your loan payments in the event of unforeseen circumstances like disability, involuntary unemployment, or death, providing a crucial safety net for your family.

Furthermore, if you already have an existing used car loan with another lender, NFCU provides excellent refinancing options. If your credit score has improved since you first took out your loan, or if interest rates have dropped, refinancing with NFCU could potentially lower your interest rate, reduce your monthly payments, or shorten your loan term. This is a smart financial move that can save you a considerable amount of money over time and is definitely worth exploring.

Finally, NFCU is dedicated to the financial well-being of its members. They offer a wealth of financial education resources, from articles and calculators to workshops and one-on-one counseling. These resources can help you manage your budget, understand your credit, and make informed financial decisions beyond your car loan.

Pro Tips for a Smooth NFCU Used Car Loan Experience

Securing an NFCU used car loan can be a smooth and rewarding process, especially when you come prepared. Here are some pro tips, drawn from years of experience in the auto finance world, to ensure you get the best possible outcome.

Firstly, improve your credit score before applying. This is perhaps the most impactful step you can take. Paying down existing debts, disputing inaccuracies on your credit report, and avoiding new credit applications in the months leading up to your loan application can significantly boost your score. A higher score directly translates to lower interest rates and better loan terms from NFCU. (For more detailed strategies, check out our article on How to Boost Your Credit Score for Auto Loans).

Secondly, save for a down payment. While NFCU may offer 100% financing for qualified buyers, making a down payment, even a small one, is always a smart move. It reduces the amount you need to borrow, lowers your monthly payments, and decreases the total interest paid over the life of the loan. A down payment also creates immediate equity in your vehicle, protecting you from being upside down on the loan.

Thirdly, research thoroughly – both the vehicle and the seller. Don’t rush into a purchase. Invest time in understanding the specific make and model you’re interested in, including common issues and maintenance costs. For private sellers, meet in a public place and bring a friend. For dealerships, read reviews and check their reputation before committing.

Fourthly, understand the total cost of ownership. Beyond the monthly loan payment, factor in insurance, fuel, maintenance, and potential repair costs. A car might seem affordable upfront, but these ongoing expenses can quickly add up. Budgeting for these elements gives you a realistic picture of your financial commitment.

Finally, always read the fine print. Whether it’s the pre-approval offer or the final loan agreement, take the time to understand every clause. Ask questions if anything is unclear. This diligence ensures there are no surprises down the road and that you’re fully comfortable with the terms of your NFCU used car loan. For general guidance on understanding loan terms, you can refer to reputable sources like the Consumer Financial Protection Bureau (CFPB) website (www.consumerfinance.gov).

Drive Away with Confidence: Your NFCU Used Car Loan Journey

Embarking on the journey to purchase a used car is an exciting prospect, and with Navy Federal Credit Union by your side, it can also be a financially savvy one. By understanding the ins and outs of NFCU used car loans, from eligibility and application processes to competitive rates and valuable member benefits, you are well-equipped to make an informed decision.

NFCU’s commitment to its members, coupled with their competitive financing options and excellent customer service, truly sets them apart. They offer more than just a loan; they provide a pathway to affordable vehicle ownership, backed by a credit union that understands and values your service.

Armed with this comprehensive knowledge, you’re ready to navigate the used car market with confidence. Take the first step today – explore your NFCU membership benefits, get pre-approved, and drive away in the used car of your dreams, knowing you’ve made a smart and secure financial choice. Your open road awaits!