Unlock Your Dream Ride: The Ultimate Guide to PSBank Car Loan Approval in the Philippines

Unlock Your Dream Ride: The Ultimate Guide to PSBank Car Loan Approval in the Philippines Carloan.Guidemechanic.com

The dream of owning a car in the Philippines is a powerful one. It represents freedom, convenience, and a significant step towards a better quality of life for many. Whether it’s for daily commutes, family outings, or starting a new business venture, a personal vehicle can transform your daily experience. But how do you turn that dream into a tangible reality without draining your savings overnight? This is where a reliable auto loan comes into play, and PSBank, a trusted name in Philippine banking, offers some of the most accessible and competitive options available.

Navigating the world of car loans can feel overwhelming, especially with the myriad of requirements, terms, and processes involved. That’s why we’ve crafted this super comprehensive guide. Here, we will demystify everything you need to know about securing a PSBank Car Loan, from understanding their offerings and eligibility criteria to mastering the application process and getting that coveted approval. Our goal is to equip you with the knowledge and confidence to drive away in your new (or new-to-you) car with ease.

Unlock Your Dream Ride: The Ultimate Guide to PSBank Car Loan Approval in the Philippines

Why Choose PSBank for Your Auto Loan Journey?

When it comes to vehicle financing in the Philippines, you have several choices. So, why should PSBank be at the top of your list? Based on my experience in the financial industry, PSBank has consistently proven itself as a strong contender due to its customer-centric approach and straightforward processes. They understand the aspirations of the Filipino consumer and tailor their services to meet those needs effectively.

PSBank, or the Philippine Savings Bank, is a key player in the country’s banking sector, known for its focus on consumer and small business loans. This specialization means they have refined their auto loan offerings to be both competitive and accessible. Their long-standing reputation for reliability and stability provides a crucial layer of trust, which is paramount when making a significant financial commitment like a car loan.

One of their standout features is their streamlined application process. They strive to make the journey as hassle-free as possible, which is a huge relief for busy individuals. Furthermore, PSBank offers various loan terms and competitive interest rates, making car ownership more attainable for a wider range of Filipinos. They truly aim to make your car ownership dream a reality.

Understanding PSBank Car Loan Options: New vs. Used Vehicles

PSBank caters to different car ownership needs by offering distinct car loan products. Whether you’re eyeing a brand-new vehicle fresh from the showroom or a pre-owned gem, PSBank has a financing solution for you. Understanding these options is the first step in choosing the right path.

New Car Loan

For those who crave that "new car smell" and the latest features, PSBank’s New Car Loan is the perfect fit. This loan product is designed to finance the purchase of brand-new vehicles directly from accredited dealerships. You get to enjoy the full manufacturer’s warranty and the peace of mind that comes with being the first owner.

The new car loan typically offers longer repayment terms, which can translate to lower monthly amortizations. This makes it easier to manage your budget while enjoying your new ride. PSBank works with a wide network of reputable car dealers, simplifying the purchasing process for you.

Used Car Loan (Pre-Owned Vehicle Financing)

If budget is a primary concern, or if you’ve found a fantastic deal on a pre-owned vehicle, PSBank’s Used Car Loan is an excellent alternative. This option allows you to finance the purchase of second-hand cars, often at a more affordable price point than new ones. It’s a smart way to get a quality vehicle without the depreciation hit of a brand-new model.

PSBank accepts used vehicles that meet specific criteria, usually regarding age and condition. While interest rates might be slightly different from new car loans, the overall cost of ownership can be significantly lower. This makes the used car loan a popular choice for many Filipinos seeking practical and economical vehicle solutions. It’s crucial to ensure the pre-owned vehicle is in good condition and has a clear ownership history.

Eligibility Requirements: Are You Ready for a PSBank Car Loan?

Before you even start gathering documents, it’s essential to understand if you meet PSBank’s fundamental eligibility criteria. This step saves time and helps you prepare adequately. Based on our experience, many applicants overlook these basic requirements, leading to unnecessary delays or even rejection.

Here are the key qualifications you’ll generally need to meet:

- Age: Applicants must be at least 21 years old and not more than 65 years old upon loan maturity. This ensures that borrowers are of legal age to enter into contracts and have a reasonable period of earning capacity to repay the loan.

- Citizenship/Residency: You must be a Filipino citizen or a foreign national residing in the Philippines for at least two (2) years. This ensures a stable presence and easier verification processes for the bank.

- Income: A stable and sufficient source of income is paramount. PSBank requires applicants to have a minimum gross monthly income, which can vary depending on the loan amount and current policies. This income must be verifiable through employment certificates, payslips, or business permits and financial statements for self-employed individuals. Your income needs to demonstrate your capacity to comfortably handle the monthly amortizations.

- Employment Status:

- Employed Individuals: Must be regularly employed for at least two (2) years with a reputable company.

- Self-Employed Individuals: Must have a profitable business operating for at least three (3) years.

- OFWs (Overseas Filipino Workers): Must have a stable job contract with at least two (2) years remaining or have a consistent track record of remittances.

- Credit History: A good credit standing is crucial. PSBank will check your credit report for any past due accounts, defaults, or negative records. A clean credit history signals to the bank that you are a responsible borrower. For more on improving your financial standing, you might find our article on Understanding Your Credit Score: A Key to Loan Approval helpful.

Common mistakes to avoid are: underestimating the income requirement or having a shaky employment history. Banks look for stability, so ensure your work history is consistent. Also, any unpaid loans or credit card bills can severely impact your eligibility.

Documents Checklist: What You’ll Need for Your PSBank Car Loan Application

Gathering the correct documents is often the most tedious part of the loan application process, but it’s also one of the most critical. Incomplete or incorrect documentation is a leading cause of delays. Pro tips from us: organize everything neatly and make sure all copies are clear and legible.

Here’s a detailed breakdown of the documents PSBank will typically require, categorized for your convenience:

I. Personal Information Documents

- Completely Filled-out PSBank Auto Loan Application Form: This is your initial declaration of intent and personal details. Fill it out accurately and completely.

- Two (2) Valid Government-Issued IDs: Examples include a Driver’s License, Passport, SSS ID, UMID, Postal ID, or PRC ID. These IDs must be unexpired and contain your photo and signature.

- Proof of Billing: A recent utility bill (electricity, water, phone, internet) under your name, or a barangay certificate. This verifies your residential address. If the bill is not under your name, an affidavit of residency may be required.

- Marriage Contract (if applicable): For married applicants, this document is necessary to confirm marital status.

II. Income Documents (Based on Employment Status)

A. For Employed Individuals:

- Certificate of Employment and Compensation (COEC): This should be original, issued within the last three (3) months, and state your position, length of service, and gross monthly income.

- Latest Income Tax Return (ITR) with W2 Form (Form 2316): This provides an official record of your declared income and taxes paid.

- Latest Three (3) Months Payslips: These further verify your consistent income over a recent period.

B. For Self-Employed Individuals:

- Business Registration Documents: DTI or SEC registration, Mayor’s Permit/Business Permit. These prove the legitimacy of your business.

- Latest Two (2) Years Audited Financial Statements (AFS): This provides a comprehensive overview of your business’s financial health and profitability.

- Latest Two (2) Years Income Tax Return (ITR) with Financial Statements: Similar to AFS, but specifically for tax purposes.

- Bank Statements: Latest six (6) months bank statements for your personal and/or business accounts. This shows consistent cash flow.

- List of Trade References/Suppliers/Clients: This helps the bank verify the active operation of your business.

C. For Overseas Filipino Workers (OFWs):

- Copy of Employment Contract or Certificate of Employment: Should clearly state your position, salary, and contract duration.

- Latest Six (6) Months Proof of Remittances: Bank statements or official receipts from remittance centers. This demonstrates a consistent income stream.

- Special Power of Attorney (SPA): If someone else will represent you in the Philippines for the loan processing.

III. Collateral Documents (Vehicle Information)

- Proforma Invoice or Quotation from Car Dealer: For new cars, this details the vehicle specifications and price.

- Copy of OR/CR (Official Receipt / Certificate of Registration): For used cars, this proves ownership and registration.

- Picture of the Vehicle (for used cars): Helps the bank assess the condition of the car.

Pro tips from us: Always make photocopies of all documents for your records before submitting them. Double-check that all information is consistent across all submitted papers. Any discrepancies can raise red flags and cause delays.

The PSBank Car Loan Application Process: Your Step-by-Step Journey

Applying for a car loan doesn’t have to be a mystery. PSBank aims for a straightforward process, and understanding each step will help you navigate it with confidence. Based on my experience, knowing what to expect at each stage significantly reduces anxiety.

Here’s a typical walkthrough of the PSBank Car Loan application:

- Inquiry and Pre-qualification: Your journey begins by inquiring about PSBank’s car loan products. You can do this by visiting a PSBank branch, checking their official website, or contacting their customer service. At this stage, you can get an estimate of your potential loan amount and monthly amortization using a PSBank car loan calculator, usually available online or with a bank representative. This also helps you assess your eligibility based on the basic requirements.

- Application Form Submission: Once you’ve decided to proceed, you’ll need to fill out the PSBank Auto Loan Application Form. Be meticulous and ensure all information is accurate and complete.

- Document Submission: Gather all the required documents as per the checklist provided earlier. Submit these along with your application form to a PSBank branch or through an accredited dealer. Make sure all copies are clear and all originals are available for verification if needed.

- Credit Investigation and Evaluation: This is a crucial phase where PSBank assesses your creditworthiness. They will review your submitted documents, verify your income and employment, and conduct a credit check with credit bureaus. This step determines your capacity to repay the loan and your historical financial responsibility. They might also conduct a personal interview or call your employer.

- Vehicle Appraisal (for Used Cars): If you’re applying for a used car loan, PSBank will arrange for an appraisal of the vehicle to determine its fair market value and ensure it meets their quality standards.

- Loan Approval and Notification: If your application passes the credit investigation and evaluation, PSBank will notify you of your loan approval. This notification will include the approved loan amount, interest rate, and repayment terms.

- Loan Documentation and Signing: Upon approval, you will proceed to sign the loan documents, including the Promissory Note and Disclosure Statement. Ensure you read and understand all terms and conditions before signing. Don’t hesitate to ask questions if anything is unclear.

- Chattel Mortgage Registration: A chattel mortgage will be registered on your vehicle in favor of PSBank. This means the bank holds the title to your car until the loan is fully paid.

- Disbursement and Vehicle Release: Once all documents are signed, the chattel mortgage is registered, and the required down payment (if any) is made, PSBank will disburse the loan proceeds directly to the car dealer. You can then pick up your new car!

The entire process, from application to disbursement, can typically take anywhere from 5 to 10 working days, assuming all documents are complete and there are no complications. Pro tips from us: Be responsive to calls or requests for additional information from the bank to avoid delays.

Demystifying PSBank Car Loan Interest Rates and Fees

Understanding the costs involved beyond the principal loan amount is vital for responsible car ownership. PSBank, like any financial institution, charges interest and various fees. Knowing what to expect helps you budget effectively.

Interest Rates

PSBank car loan interest rates are competitive and generally depend on several factors:

- Loan Term: Shorter loan terms (e.g., 3 years) often have slightly lower interest rates than longer terms (e.g., 5 years), though monthly payments will be higher.

- Loan Amount: The total amount borrowed can sometimes influence the rate.

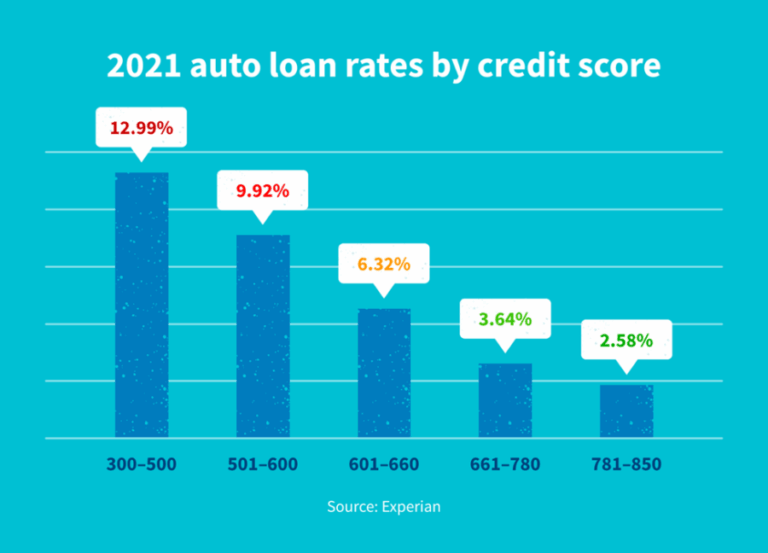

- Applicant’s Credit Standing: Borrowers with excellent credit scores and stable financial profiles often qualify for the best rates.

- Market Conditions: Prevailing economic conditions and the Bangko Sentral ng Pilipinas (BSP) policy rates can also affect interest rates. You can always refer to the BSP website for general economic indicators and financial literacy resources.

Pro tips from us: Don’t just focus on the lowest advertised rate. Ask for the Effective Interest Rate (EIR), which includes all charges and gives you a truer picture of the loan’s annual cost. Use the PSBank car loan calculator to compare different scenarios and see how varying interest rates impact your monthly amortization.

Other Fees and Charges

Beyond the interest, you’ll encounter several other fees:

- Processing Fee: A one-time fee charged by the bank for processing your loan application.

- Documentary Stamp Tax (DST): A government tax imposed on loan documents, usually a percentage of the loan amount.

- Chattel Mortgage Fee: The cost associated with registering the chattel mortgage on your vehicle.

- Insurance Premium: Comprehensive car insurance is typically required by the bank for the duration of the loan. This can be paid annually or bundled into your monthly amortization.

- Notarial Fees: For notarization of loan documents.

- Late Payment Charges: Penalties if you fail to pay your monthly amortization on time.

Common mistakes to avoid are: not factoring these additional costs into your budget. They can significantly increase your overall outlay. Always ask for a detailed breakdown of all fees before signing any agreements.

Tips for a Smooth PSBank Car Loan Approval

Securing a PSBank Car Loan approval isn’t just about meeting the minimum requirements; it’s about presenting yourself as a highly reliable borrower. Here are pro tips from us to significantly boost your chances of approval:

- Maintain an Excellent Credit Score: Your credit history is a report card of your financial behavior. Pay all your existing debts (credit cards, other loans) on time and in full. Avoid opening too many new credit lines before applying for a car loan. A strong credit score signals trustworthiness to the bank.

- Provide Strong and Verifiable Income Proof: The clearer and more consistent your income documents are, the better. If you’re employed, ensure your COEC and payslips are up-to-date. For self-employed individuals, well-maintained financial records and bank statements are crucial.

- Keep Your Debt-to-Income Ratio Low: This ratio compares your total monthly debt payments to your gross monthly income. Banks prefer a lower ratio, indicating you have sufficient disposable income to handle new loan payments. Pay down existing debts before applying for a car loan.

- Complete and Accurate Documentation: As emphasized earlier, incomplete or erroneous documents are a major roadblock. Double-check everything before submission. PSBank values thoroughness.

- Choose the Right Car and Loan Term: Don’t over-borrow. Select a car that genuinely fits your budget and lifestyle, and a loan term that results in comfortable monthly payments. While longer terms mean lower monthly payments, they also mean more interest paid over time. Finding the right balance is key.

- Have a Sufficient Down Payment: While PSBank may offer low down payment options, making a larger down payment reduces your loan amount, leading to lower monthly amortizations and potentially better interest rates. It also shows your financial commitment.

- Be Transparent and Honest: Provide accurate information on your application form. Any misrepresentation can lead to immediate rejection or even legal repercussions.

- Be Prepared for Interviews/Verifications: PSBank may call your employer, references, or even visit your residence/business. Be prepared to provide consistent information.

What to do if denied: Don’t despair. Ask PSBank for the reason for denial. It could be due to incomplete documents, insufficient income, or a poor credit score. Address these issues, improve your financial standing, and reapply in a few months. For guidance on financial planning, you might find our article on Budgeting for Your First Car: Beyond the Monthly Payment useful.

Common Mistakes to Avoid When Applying for a PSBank Car Loan

Even with the best intentions, applicants can sometimes make errors that hinder their approval chances. Being aware of these common pitfalls can help you avoid them.

- Submitting Incomplete or Incorrect Documents: This is arguably the most frequent mistake. A missing payslip, an expired ID, or an inconsistent address can bring your application to a grinding halt. Always double-check your checklist.

- Over-borrowing or Choosing an Unaffordable Car: It’s tempting to go for the fanciest car, but if the monthly payments stretch your budget too thin, PSBank will likely deny the loan. Banks assess your capacity to pay, not just your desire.

- Ignoring Your Credit History: Many applicants fail to check their credit standing before applying. Any negative marks, such as missed payments or defaulted loans, will significantly impact your eligibility. Address these issues proactively.

- Not Comparing Loan Options: While this guide focuses on PSBank, it’s always wise to compare offers from different banks. However, don’t apply to too many banks simultaneously, as multiple inquiries can negatively affect your credit score.

- Lack of Transparency: Providing false information, even minor details, can be grounds for immediate rejection. Banks conduct thorough verifications, and inconsistencies will be flagged.

- Neglecting the Down Payment: While not always mandatory, a minimal or no down payment can signal higher risk to the bank, potentially leading to higher interest rates or even denial. A solid down payment shows your commitment.

By being mindful of these common errors, you can significantly streamline your application process and increase your likelihood of approval.

After Approval: What Happens Next?

Congratulations, your PSBank Car Loan has been approved! But the journey doesn’t end there. There are a few more steps before you can truly drive off into the sunset.

- Signing the Final Documents: You’ll need to visit a PSBank branch to sign the official loan documents. These include the Promissory Note, Disclosure Statement, and Deed of Chattel Mortgage. Take your time to review everything carefully before affixing your signature.

- Payment of Down Payment and Other Fees: If you have a down payment, this will be settled at the dealership or as per bank instructions. Other initial fees like processing fees or chattel mortgage fees might also be collected at this stage or deducted from the loan proceeds.

- Vehicle Release and Insurance: Once all documents are signed, the chattel mortgage is registered, and payments are settled, the loan proceeds are released to the dealer. The dealer will then prepare your car for release. Remember, comprehensive car insurance is usually a requirement for the entire loan term, and it’s wise to have it arranged before you drive off.

- Understanding Your Payment Schedule: You’ll receive a clear payment schedule detailing your monthly amortization due dates. Set up reminders or consider enrolling in auto-debit arrangements from your PSBank account to ensure timely payments. Maintaining good payment habits is crucial for your credit standing and relationship with the bank.

Is a PSBank Car Loan Right for You? Weighing the Pros and Cons

Deciding on a car loan is a major financial decision. Here’s a quick summary to help you weigh if a PSBank Car Loan aligns with your needs:

Pros:

- Trusted Institution: PSBank’s strong reputation provides peace of mind.

- Competitive Rates & Flexible Terms: Offers various options to suit different budgets.

- Streamlined Process: Designed for efficiency and ease of application.

- Wide Network: Partnership with numerous car dealers.

- Both New & Used Car Options: Caters to diverse vehicle preferences.

- Accessible Customer Service: Support available for inquiries and assistance.

Cons:

- Strict Eligibility: Like all banks, PSBank has stringent requirements for income, credit score, and employment.

- Documentation Intensive: Requires a comprehensive set of documents, which can be time-consuming to gather.

- Additional Fees: Beyond interest, various fees add to the total cost of the loan.

- Chattel Mortgage: The vehicle is legally owned by the bank until the loan is fully paid.

Ultimately, if you meet the eligibility criteria, have a stable income, and are committed to responsible repayment, a PSBank Car Loan can be an excellent and reliable pathway to owning your dream car.

Frequently Asked Questions (FAQs) about PSBank Car Loan

Q1: How long does PSBank Car Loan approval take?

A1: Typically, the approval process takes 5 to 10 working days, provided all submitted documents are complete and verifiable.

Q2: Can I apply for a PSBank Car Loan if I have a low credit score?

A2: While PSBank prefers a good credit score, they evaluate applications holistically. However, a low score might lead to a higher interest rate or require a larger down payment. It’s best to improve your score before applying.

Q3: What is the maximum loan term for a PSBank Car Loan?

A3: PSBank usually offers loan terms of up to 5 years (60 months) for both new and used cars, depending on the vehicle’s age for pre-owned units.

Q4: Do I need a down payment for a PSBank Car Loan?

A4: While PSBank may offer low down payment options (e.g., 15-20% of the car’s price), making a larger down payment is always recommended as it reduces your loan amount and monthly amortization.

Q5: Can I pay off my PSBank Car Loan early?

A5: Yes, generally you can pay off your loan early. However, check your loan agreement for any pre-termination fees or charges that might apply.

Conclusion: Your Road to Car Ownership Starts Here

Owning a car is more than just a convenience; it’s an investment in your lifestyle, your family, and your future. With PSBank Car Loan, that investment becomes a tangible reality, made accessible through their competitive offerings and streamlined processes. We hope this extensive guide has illuminated every corner of the PSBank Car Loan journey, empowering you with the knowledge needed to confidently pursue your dream vehicle.

From understanding the different loan types and meticulous document preparation to navigating the application steps and securing that coveted approval, every detail matters. Remember, a well-prepared and informed applicant is often a successful applicant. So, take these insights, gather your documents, and start your application today. Your dream car is waiting, and PSBank is ready to help you drive it home.