Unlock Your Dream Ride: The Ultimate Guide to SDCCU Car Loans

Unlock Your Dream Ride: The Ultimate Guide to SDCCU Car Loans Carloan.Guidemechanic.com

Buying a car is more than just a transaction; it’s a significant life event that opens doors to new possibilities, freedom, and convenience. Whether you’re eyeing a sleek new sedan, a reliable used SUV, or simply looking to lower your current auto loan payments, securing the right financing is paramount. In the vibrant Southern California landscape, particularly in San Diego, one name frequently comes up as a trusted financial partner: San Diego County Credit Union (SDCCU).

As an expert blogger and SEO content writer with years of experience navigating the complexities of auto financing, I’ve seen firsthand how crucial it is to understand your options. This comprehensive guide will delve deep into everything you need to know about SDCCU Car Loans, helping you make an informed decision that drives you toward financial success. We’ll explore their offerings, application process, tips for securing the best rates, and common pitfalls to avoid.

Unlock Your Dream Ride: The Ultimate Guide to SDCCU Car Loans

What Makes SDCCU Car Loans a Smart Choice?

Choosing a financial institution for your auto loan is a decision that impacts your budget for years to come. SDCCU, as a member-owned credit union, operates differently from traditional banks, often translating into distinct advantages for its members.

Competitive Rates That Save You Money

One of the primary reasons many individuals gravitate towards credit unions like SDCCU for their car loans is the promise of competitive interest rates. Because credit unions are not-for-profit organizations, their earnings are often reinvested into providing better rates and services to their members.

Based on my experience, even a slight difference in interest rates can lead to substantial savings over the life of a car loan. SDCCU strives to offer rates that are often lower than those found at many big banks or dealership financing options, putting more money back into your pocket each month. This focus on member benefit is a cornerstone of the credit union philosophy.

Flexible Terms Tailored to Your Needs

Every borrower’s financial situation is unique, and a one-size-fits-all approach rarely works when it comes to financing. SDCCU understands this, offering a range of flexible loan terms designed to fit various budgets and preferences.

Whether you prefer a shorter term to pay off your loan faster and save on interest, or a longer term to reduce your monthly payments, SDCCU provides options. From 36-month loans to 84-month terms, they aim to match your loan structure to your personal financial goals. This flexibility is crucial for managing your budget effectively.

Personalized Service: The Credit Union Advantage

When you’re a member of SDCCU, you’re not just a customer; you’re a co-owner. This ownership model fosters a culture of personalized service and genuine care that can be hard to find elsewhere.

Pro tips from us: Don’t underestimate the value of a financial institution that genuinely listens to your needs and provides tailored advice. SDCCU’s loan officers are often focused on building relationships and helping you understand all aspects of your SDCCU auto loan, rather than simply pushing a product. This personal touch can make the entire car buying process much less stressful.

Community Focus and Local Presence

SDCCU is deeply rooted in the San Diego community, serving residents throughout Southern California. This local focus means they understand the regional market and the specific needs of their members.

Their commitment extends beyond financial products to community involvement and education. When you choose an SDCCU Car Loan, you’re supporting an institution that actively contributes to the local economy and well-being. This sense of community can provide an added layer of trust and reliability.

Navigating the Landscape of SDCCU Car Loans: Your Options

SDCCU offers a variety of car loan products designed to cater to different stages of vehicle ownership. Understanding these options is the first step toward finding the perfect fit for you.

New Car Loans: Driving Off the Lot with Confidence

If you’re looking to purchase a brand-new vehicle, SDCCU’s new car loans are specifically structured to help you finance your latest acquisition. These loans typically come with competitive rates, reflecting the lower risk associated with new vehicles.

When considering a new car loan, SDCCU can help you finance up to 100% of the vehicle’s purchase price, including taxes and license fees for qualified borrowers. This comprehensive financing can make the dream of a new car a reality without a hefty upfront cash outlay.

Used Car Loans: Quality and Value for Pre-Owned Vehicles

Buying a used car can be a smart financial move, offering excellent value and often lower insurance costs. SDCCU provides robust used car loan options, ensuring you can finance your pre-owned vehicle with favorable terms.

These loans are available for vehicles that meet specific age and mileage criteria, typically up to a certain number of years old and within a mileage limit. SDCCU assesses the vehicle’s value to ensure you’re getting a fair deal and financing it appropriately. could be helpful here.

Auto Loan Refinancing: Lower Your Payments, Save More

Perhaps you already have a car loan but are looking for a way to reduce your monthly payments or secure a lower interest rate. SDCCU’s auto loan refinancing program is an excellent solution.

Refinancing involves taking out a new loan to pay off your existing one, ideally with better terms. This can significantly reduce your overall interest paid or free up cash flow in your monthly budget. Many members find substantial savings by refinancing their high-interest auto loans with SDCCU.

Lease Buyout Loans: Owning Your Leased Vehicle

At the end of a car lease, you often have the option to purchase the vehicle. If you’ve fallen in love with your leased car and want to make it truly yours, SDCCU offers lease buyout loans.

These loans help you finance the residual value of the vehicle, as specified in your lease agreement. It’s a convenient way to transition from leasing to ownership, allowing you to avoid penalties for excess mileage or wear and tear, and continue driving a car you already know and trust.

The SDCCU Car Loan Application Process: A Step-by-Step Guide

Securing an SDCCU Car Loan doesn’t have to be daunting. By understanding the process and preparing adequately, you can ensure a smooth and efficient experience.

Step 1: Get Pre-Approved – Your Power Play at the Dealership

One of the most powerful moves you can make before stepping onto a car lot is to get pre-approved for an SDCCU auto loan. Pre-approval means SDCCU has conditionally agreed to lend you a certain amount of money at a specific interest rate, based on your creditworthiness.

Why is this crucial? Based on my experience, having a pre-approval letter in hand transforms you from a mere shopper into a cash buyer. It gives you significant leverage in negotiations with the dealership, as you already have your financing secured. You can focus on negotiating the car’s price, knowing your loan terms are already set.

Step 2: Gather Your Essential Documents

Before applying, ensure you have all necessary documentation ready. This proactive step can significantly speed up the application process.

Typically, you’ll need:

- Proof of Income: Pay stubs, tax returns, or employment verification.

- Identification: Driver’s license or state-issued ID.

- Social Security Number: For credit checks.

- Residence Information: Proof of address, like a utility bill.

- Vehicle Information (if already chosen): VIN, make, model, mileage.

Having these documents organized prevents delays and shows the loan officer you are prepared.

Step 3: Choose Your Application Method

SDCCU offers convenient ways to apply for your car loan, catering to your preference and schedule.

You can apply:

- Online: The quickest and most convenient method, accessible 24/7 from anywhere.

- In-Branch: Visit any SDCCU branch to speak directly with a loan officer. This is ideal if you prefer face-to-face interaction or have complex questions.

- By Phone: Speak with a loan representative over the phone to complete your application.

Each method is designed to provide a seamless experience, allowing you to choose what works best for you.

Step 4: What Happens After You Apply?

Once your application is submitted, SDCCU will review your financial information, including your credit history, income, and debt-to-income ratio. They will then provide you with a decision.

If approved, you’ll receive details about your loan amount, interest rate, and terms. You’ll then proceed to finalize the paperwork and, if applicable, work with the dealership to complete your purchase. The goal is to make this transition as smooth as possible.

Understanding SDCCU Car Loan Rates and Terms

Demystifying interest rates and loan terms is vital for making sound financial decisions. Here’s what you need to know about SDCCU’s approach.

Factors Affecting Your Interest Rate

Several key factors play a role in determining the interest rate you’ll receive on your SDCCU auto loan:

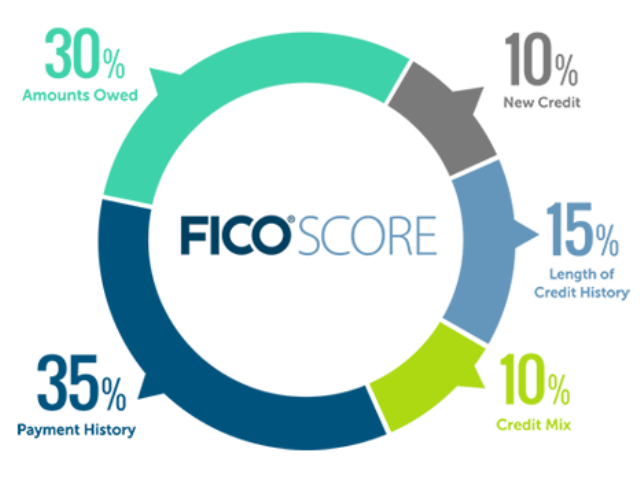

- Credit Score: This is perhaps the most significant factor. A higher credit score indicates lower risk to lenders, often resulting in lower interest rates.

- Loan Term: Shorter loan terms typically come with lower interest rates because the lender is exposed to risk for a shorter period.

- Down Payment: A larger down payment reduces the loan amount and the lender’s risk, which can lead to a better rate.

- Vehicle Type: New cars often qualify for slightly lower rates than used cars due to depreciation differences and perceived reliability.

Understanding these factors allows you to proactively work on improving aspects that could lead to a better rate.

APR vs. Interest Rate: Know the Difference

It’s important to differentiate between the interest rate and the Annual Percentage Rate (APR).

- Interest Rate: This is the cost of borrowing money, expressed as a percentage of the principal.

- APR: This is the total cost of the loan, including the interest rate and any additional fees (like origination fees, if applicable). The APR provides a more accurate picture of the overall cost of borrowing.

Always focus on the APR when comparing loan offers, as it gives you the complete financial picture.

Choosing the Right Loan Term for Your Budget

Selecting the appropriate loan term is a balancing act between monthly payments and the total interest paid over time.

- Shorter Terms (e.g., 36-48 months): Result in higher monthly payments but significantly lower total interest paid. You own the car outright faster.

- Longer Terms (e.g., 60-84 months): Offer lower monthly payments, making the car more affordable in the short term. However, you’ll pay more interest over the loan’s life and build equity slower.

Pro tips from us: Carefully assess your budget and future financial goals. While lower monthly payments are appealing, don’t extend the term so long that you end up "upside down" on your loan (owing more than the car is worth) for an extended period.

Pro Tips for Securing the Best SDCCU Car Loan

Maximizing your chances of getting a favorable SDCCU Car Loan involves a bit of preparation and strategic thinking.

Boost Your Credit Score Before Applying

Your credit score is your financial report card. Before you even think about applying, take steps to improve it. Pay down existing debts, make all payments on time, and avoid opening new lines of credit.

A higher credit score not only increases your approval chances but also unlocks the lowest available interest rates. Consider obtaining a free copy of your credit report from AnnualCreditReport.com to identify any errors and understand your current standing. could be placed here.

Save for a Sizable Down Payment

A larger down payment immediately reduces the amount you need to borrow, which can lead to better loan terms. It also demonstrates financial responsibility to the lender.

Common mistakes to avoid are thinking you don’t need a down payment at all. While 100% financing is available, putting down even 10-20% of the vehicle’s price can make a significant difference in your monthly payments and the total interest you’ll pay.

Consider a Co-Signer (If Applicable)

If you have limited credit history or a lower credit score, having a creditworthy co-signer can significantly improve your chances of approval and help you secure a better interest rate.

A co-signer essentially guarantees the loan, sharing the responsibility if you default. However, understand that this is a serious commitment for both parties, as the co-signer’s credit will also be impacted.

Negotiate Wisely at the Dealership with Pre-Approval

As mentioned, pre-approval is your secret weapon. With your SDCCU pre-approval in hand, you can confidently negotiate the car’s purchase price without the added pressure of securing financing on the spot.

Pro tips from us: Always negotiate the price of the car first, separate from discussing financing. Once you’ve agreed on a price, you can then compare the dealership’s financing offer (if any) against your SDCCU pre-approval. This approach ensures you’re getting the best deal on both the vehicle and the loan.

Explore Auto Loan Protections

SDCCU often offers optional protection products that can provide peace of mind. These might include:

- Guaranteed Asset Protection (GAP) Insurance: This covers the difference between what you owe on your loan and your car’s actual cash value if it’s totaled or stolen. Given how quickly new cars depreciate, GAP can be invaluable.

- Mechanical Breakdown Protection (MBP): Similar to an extended warranty, MBP helps cover the cost of unexpected repairs after your manufacturer’s warranty expires.

While these add to the overall cost, they can save you from significant financial headaches down the road. Discuss these options with your SDCCU loan officer.

Common Mistakes to Avoid When Applying for an SDCCU Car Loan

Even with the best intentions, borrowers can sometimes make missteps that complicate their car loan journey. Being aware of these common pitfalls can help you avoid them.

Not Getting Pre-Approved

This is perhaps the biggest mistake. Walking into a dealership without pre-approved financing leaves you vulnerable to potentially higher interest rates offered by the dealer, who may mark up the rate for profit.

Common mistakes to avoid are letting the dealership handle all aspects of your financing without having a benchmark from SDCCU. Always secure your own financing first, then compare.

Ignoring Your Credit Report

Many people don’t review their credit report until they need a loan. Errors on your report can unfairly lower your score, impacting your loan eligibility and interest rate.

Pro tips from us: Check your credit report well in advance of applying for any loan. Dispute any inaccuracies promptly. This small effort can save you hundreds, if not thousands, of dollars over the life of your SDCCU Car Loan.

Overlooking Hidden Fees and the Full Cost

While SDCCU is transparent with its terms, it’s easy to get caught up in the excitement of buying a car and overlook certain costs. Always ask for a full breakdown of all fees associated with the loan.

Common mistakes to avoid are focusing solely on the monthly payment. Ensure you understand the total cost of the loan, including the APR, any potential application fees, and the cost of any added protection products.

Stretching Your Budget Too Thin

It’s tempting to finance the most expensive car you can get approved for. However, remember that car ownership involves more than just loan payments. There’s insurance, fuel, maintenance, and potential repairs.

Based on my experience, a common mistake is neglecting these additional costs. Create a realistic budget that includes all potential car-related expenses before committing to a loan. You want your car to be a source of joy, not financial stress.

Not Comparing Offers (Even with SDCCU in Mind)

Even if you’re committed to SDCCU, it’s wise to understand the broader market. While SDCCU often provides excellent rates, briefly comparing their offer with one or two other reputable lenders can affirm you’re getting the best deal.

This practice also reinforces your negotiating position. However, be mindful of too many hard inquiries on your credit report; keep comparisons within a short timeframe (usually 14-45 days) so they count as a single inquiry.

Beyond the Loan: SDCCU Membership Benefits for Car Owners

Choosing an SDCCU Car Loan means you become a member, opening the door to a host of other benefits that extend beyond your vehicle financing.

Comprehensive Financial Education Resources

SDCCU is committed to empowering its members with financial knowledge. They offer workshops, articles, and tools to help you manage your money, plan for the future, and make informed decisions.

This can be incredibly valuable for new car owners looking to budget effectively, or for anyone seeking to improve their overall financial literacy. These resources are designed to help you succeed long-term.

Other Tailored Loan Products

As an SDCCU member, you gain access to a wide array of other financial products, from mortgages and personal loans to credit cards and lines of credit. This allows for a holistic banking relationship.

For instance, if you ever need a personal loan for unexpected car repairs or upgrades, your existing relationship with SDCCU can streamline the application process and potentially lead to better terms.

Community Engagement and Member Perks

SDCCU actively engages with the San Diego community through various events, sponsorships, and initiatives. As a member, you’re part of this larger community.

They often provide special member-only perks, discounts, and opportunities, further enhancing the value of your membership. This commitment to local engagement differentiates them from many national banks.

SDCCU Car Loan vs. Other Lenders: The Credit Union Advantage Revisited

While banks and dealership financing options are prevalent, credit unions like SDCCU offer a distinct model. Banks are profit-driven for shareholders, while dealerships often seek to maximize profit on financing.

SDCCU’s member-owned structure means their primary goal is to serve their members. This often translates into:

- Lower Rates: Often more competitive than traditional banks.

- Fewer Fees: Credit unions typically have lower fees, or sometimes none at all, compared to banks.

- Personalized Service: A focus on individual member needs and financial well-being.

- Community Investment: Profits are reinvested locally, benefiting the community.

For those in Southern California seeking a reliable, member-focused auto financing partner, SDCCU stands out as a compelling choice.

Conclusion: Drive Your Future with an SDCCU Car Loan

Securing an SDCCU Car Loan is more than just obtaining financing; it’s about partnering with a trusted financial institution that puts your interests first. With competitive rates, flexible terms, personalized service, and a deep commitment to the community, SDCCU offers a compelling package for anyone looking to finance a new or used vehicle, or refinance an existing loan.

By understanding the types of loans available, diligently preparing for the application process, and applying the pro tips we’ve discussed, you can confidently navigate the path to car ownership. Avoid common mistakes, leverage the power of pre-approval, and remember that a well-planned SDCCU auto loan can pave the way for a smooth ride ahead.

Ready to take the next step towards your dream car? Explore SDCCU’s current car loan rates and begin your application today. Your journey to a new set of wheels, backed by a trusted local partner, starts here.