Unlock Your Dream Ride: The Ultimate Guide to Securing a Telhio Car Loan

Unlock Your Dream Ride: The Ultimate Guide to Securing a Telhio Car Loan Carloan.Guidemechanic.com

Embarking on the journey to purchase a new vehicle is an exciting prospect, filled with the promise of new adventures and increased independence. However, the path to car ownership often involves navigating the complexities of auto financing. For residents of Central Ohio, Telhio Credit Union stands out as a beacon of member-focused financial solutions, especially when it comes to securing a car loan.

This comprehensive guide is designed to be your definitive resource for understanding everything about Telhio Car Loans. We’ll delve deep into the advantages of choosing a credit union, walk you through the application process, explain eligibility requirements, and share expert tips to maximize your chances of approval. Our goal is to equip you with the knowledge and confidence needed to make an informed decision, ensuring you drive away with not just a car, but a smart financial solution tailored to your needs.

Unlock Your Dream Ride: The Ultimate Guide to Securing a Telhio Car Loan

Understanding Telhio Credit Union: More Than Just a Bank

Before diving into the specifics of car loans, it’s crucial to understand what sets Telhio Credit Union apart. Unlike traditional banks, which are typically for-profit entities beholden to shareholders, Telhio is a not-for-profit financial cooperative owned entirely by its members. This fundamental difference shapes every aspect of its operations, particularly its approach to lending.

As a member-owned institution, Telhio’s primary mission is to serve the financial well-being of its members and the communities it operates within. This means that any profits generated are reinvested back into the credit union, leading to better interest rates on loans, higher returns on savings, and reduced fees compared to many commercial banks. It’s a financial model built on mutual benefit and community support.

Based on my experience in the financial landscape, the credit union difference often translates to a more personal and understanding approach to customer service. You’re not just an account number; you’re a co-owner, and Telhio strives to build lasting relationships rather than just processing transactions. This philosophy is especially beneficial when seeking a significant financial product like a car loan, where personalized advice and flexible solutions can make a real difference.

Why Choose a Telhio Car Loan? Unpacking the Benefits

When considering where to finance your next vehicle, Telhio Credit Union offers a compelling suite of advantages that cater directly to the needs of its members. These benefits extend beyond just competitive rates, encompassing a holistic approach to car financing.

1. Highly Competitive Interest Rates

One of the most significant drawcards for Telhio Car Loans is their consistently competitive interest rates. Because credit unions operate on a not-for-profit model, they can often offer lower Annual Percentage Rates (APRs) on loans compared to many traditional banks. This translates directly into lower monthly payments and less interest paid over the life of your loan, saving you a substantial amount of money.

Pro tips from us: always compare the APR, not just the advertised interest rate. The APR includes all fees and charges associated with the loan, giving you a true picture of its total cost. Telhio prides itself on transparency, ensuring you understand exactly what you’re paying for.

2. Flexible Loan Terms Tailored to Your Budget

Telhio understands that every financial situation is unique. They offer a variety of loan terms, ranging from shorter periods for those who want to pay off their car quickly to longer terms that result in lower monthly payments. This flexibility allows you to choose a payment plan that comfortably fits within your budget, without stretching your finances thin.

Whether you prefer a 36-month sprint or a more manageable 72-month marathon, Telhio works with you to find a term that aligns with your financial goals. This personalized approach is a hallmark of credit union service, ensuring your loan works for you, not against you.

3. Personalized Member Service and Local Support

As a Telhio member, you’re not just a customer; you’re part of a community. This philosophy translates into exceptional, personalized service. When you apply for a car loan, you’ll likely interact with local loan officers who understand the Central Ohio market and are dedicated to helping you achieve your financial goals.

This localized support means you can walk into a branch, speak directly with an expert, and get answers to your questions without navigating complex automated phone systems. This level of personal connection can be invaluable, especially when making a significant financial decision like purchasing a car.

4. The Strategic Advantage of Pre-Approval

Telhio offers a robust pre-approval process for car loans, a benefit that cannot be overstated. Getting pre-approved means Telhio reviews your financial standing and determines how much you can borrow before you even step foot on a dealership lot. This process provides you with a clear budget and a powerful negotiation tool.

With a Telhio pre-approval in hand, you transform from a casual shopper into a cash buyer. Dealers will view you as a serious buyer, often leading to better pricing on the vehicle itself, as you’ve already secured your financing. It simplifies the car-buying experience, making it less stressful and more focused on finding the right vehicle at the right price.

5. Transparency and No Hidden Fees

Transparency is a core value at Telhio. You won’t find unexpected fees or confusing jargon hidden in the fine print of your car loan agreement. They are committed to providing clear, straightforward information about your loan, ensuring you understand all terms and conditions upfront.

This commitment to honesty builds trust and helps members feel confident in their financial decisions. It’s a refreshing change from some lending institutions where fees can sometimes accumulate, catching borrowers off guard.

Types of Telhio Car Loans: Tailored Solutions for Every Need

Telhio Credit Union understands that car buying isn’t a one-size-fits-all endeavor. They offer a diverse range of auto loan products designed to meet various needs, whether you’re buying new, used, or even looking to improve your existing loan.

1. New Car Loans

For those dreaming of a brand-new vehicle, Telhio provides competitive new car loans. These loans typically come with the most favorable interest rates and terms, reflecting the lower risk associated with financing a new asset. Telhio can finance a wide range of new vehicles, helping you drive off the lot in the car of your dreams.

When applying for a new car loan, Telhio will consider the vehicle’s MSRP, your creditworthiness, and your chosen loan term. Their aim is to make the process as smooth as possible, from application to signing the final papers.

2. Used Car Loans

Purchasing a used car can be a smart financial move, offering excellent value. Telhio also specializes in used car loans, providing flexible options for pre-owned vehicles. While rates for used cars might be slightly higher than new car loans due to factors like depreciation and potential mechanical issues, Telhio remains highly competitive.

It’s important to note that specific criteria for used car loans may apply, such as maximum vehicle age or mileage limits. These guidelines help protect both the borrower and the credit union, ensuring the financed vehicle retains sufficient value over the loan term. Always check with Telhio for their current used car lending parameters.

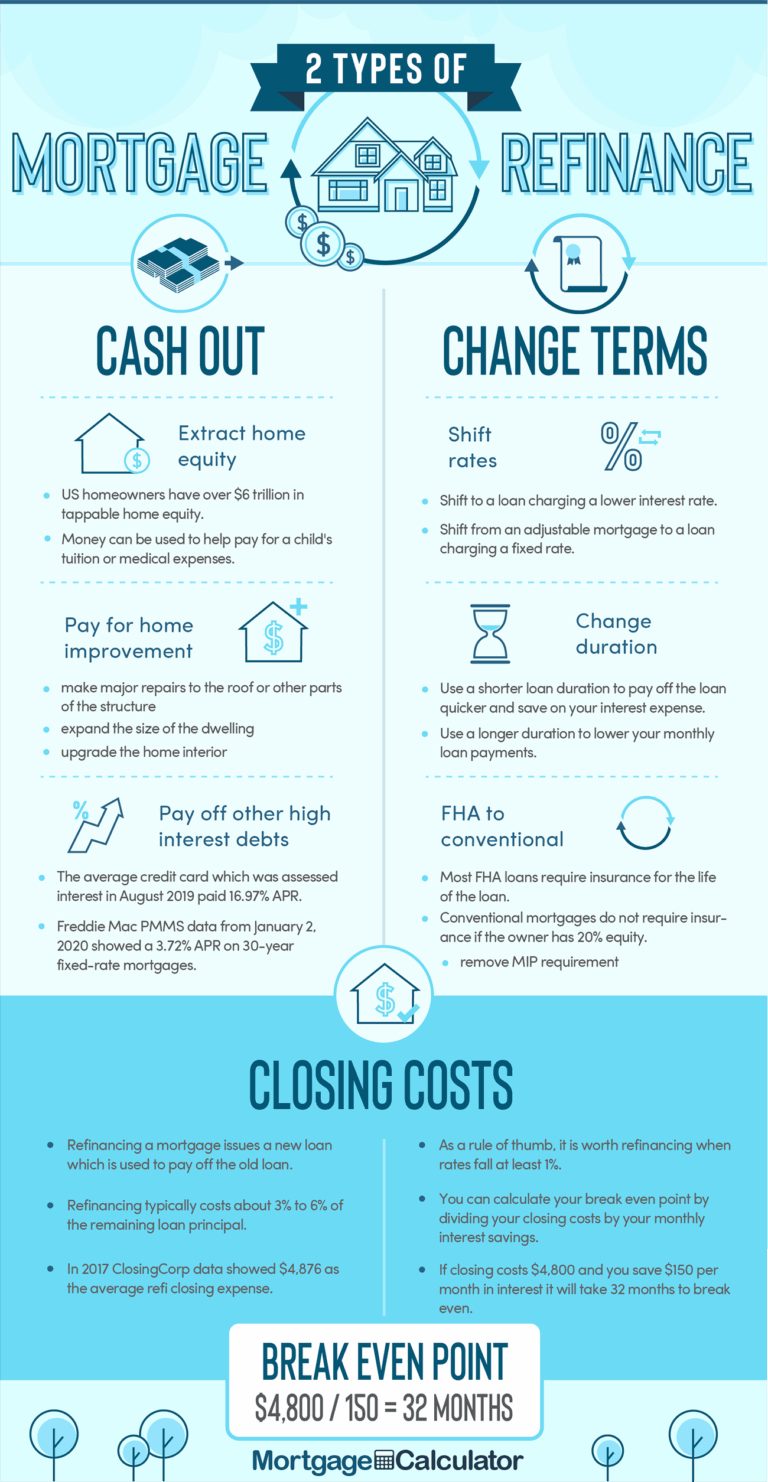

3. Refinancing Your Current Auto Loan

Many people overlook the opportunity to refinance their existing car loan, but it can be a highly effective way to save money or adjust your monthly budget. Telhio offers excellent refinancing options for those looking to switch their current auto loan from another lender.

Why Refinance?

- Lower Interest Rate: If your credit score has improved since you first took out your loan, or if market rates have dropped, you could qualify for a significantly lower interest rate.

- Lower Monthly Payments: A lower interest rate or an extended loan term can reduce your monthly payments, freeing up cash flow for other expenses.

- Shorter Loan Term: If you have extra cash, you might refinance to a shorter term, paying off your car faster and saving on total interest paid.

Common mistakes to avoid when refinancing include not checking your credit score beforehand. A good credit score is key to securing the best refinancing rates. Also, be sure to compare the total cost of the new loan, including any potential fees, against the savings you’ll achieve. Pro tip: Telhio makes the refinancing process straightforward, often saving members hundreds or even thousands of dollars over the life of their loan.

4. Lease Buyout Loans

If you’re currently leasing a vehicle and have fallen in love with it, a lease buyout loan from Telhio can help you purchase it outright. When your lease term ends, you typically have the option to buy the car at a pre-determined residual value. Telhio can finance this purchase, allowing you to keep the vehicle you’ve grown accustomed to.

This option is particularly appealing if the market value of your leased car is higher than its residual value, or if you simply prefer the convenience of owning the vehicle you’ve been driving. Telhio streamlines the process, making the transition from leasing to ownership seamless.

The Telhio Car Loan Application Process: A Step-by-Step Guide

Securing a Telhio Car Loan is a straightforward process designed to be as efficient and user-friendly as possible. By following these steps, you can navigate your application with confidence.

Step 1: Become a Telhio Member

Since Telhio is a credit union, the first and most crucial step is to become a member. Eligibility for Telhio membership typically includes living, working, worshipping, or attending school in one of the Central Ohio counties they serve. Family members of existing Telhio members are also often eligible.

Becoming a member usually involves opening a savings account with a small initial deposit, often as little as $5. This simple act opens the door to all of Telhio’s financial products and services, including their competitive car loans.

Step 2: Gather Your Documents

Preparation is key to a smooth application process. Before you apply, it’s wise to gather all necessary documentation. Having these items ready will significantly speed up the review and approval process.

Based on my experience, having all your documents ready significantly speeds up the process. You’ll typically need:

- Personal Identification: Government-issued ID (driver’s license, state ID).

- Proof of Income: Recent pay stubs, W-2s, or tax returns (if self-employed).

- Proof of Residence: Utility bill, lease agreement, or mortgage statement.

- Credit History Information: While Telhio will pull your credit report, it’s good to have an understanding of your own credit.

- Vehicle Information (if already chosen): VIN, make, model, year, mileage, and purchase price.

Step 3: Apply for Pre-Approval

This is a step we strongly recommend, even if you haven’t picked out your car yet. Applying for pre-approval with Telhio gives you a significant advantage in the car-buying process.

Benefits of Pre-Approval:

- Clear Budget: You’ll know exactly how much car you can afford, preventing you from falling in love with a vehicle outside your price range.

- Stronger Negotiation Power: With pre-approved financing, you can negotiate with dealerships as if you were a cash buyer. This removes the financing aspect from the sales pitch, allowing you to focus purely on the vehicle’s price.

- Faster Dealership Process: Once you find your car, the financing portion is already handled, making the final purchase much quicker and less stressful at the dealership.

You can typically apply for pre-approval online through Telhio’s website, over the phone, or by visiting one of their local branches. The online application is often the quickest and most convenient option.

Step 4: Shop for Your Vehicle

With your Telhio pre-approval in hand, you are now empowered to shop for your vehicle with confidence. Focus on finding the car that meets your needs and budget. Remember, your pre-approval amount is your maximum, but you don’t have to spend it all.

Pro tip: Don’t forget to factor in additional costs beyond the vehicle’s price, such as sales tax, registration fees, and car insurance, when determining your overall budget.

Step 5: Finalize Your Loan

Once you’ve found your perfect car, the final step is to finalize your loan with Telhio. You’ll provide the specific vehicle details (VIN, purchase agreement) to your Telhio loan officer. They will then review everything, prepare the final loan documents, and explain any remaining details.

This stage involves signing the loan agreement, which will outline your interest rate, monthly payment, loan term, and any other relevant conditions. Telhio will then disburse the funds directly to the dealership or, in the case of a private sale, to the seller.

Understanding Telhio Car Loan Requirements & Eligibility

To ensure a smooth application process, it’s helpful to understand the key requirements Telhio Credit Union looks for when evaluating a car loan application. Meeting these criteria will significantly increase your chances of approval.

1. Telhio Membership

As discussed, being a member is non-negotiable. If you’re not yet a member, this will be the first step in your car loan journey. Telhio’s community-focused eligibility ensures that their benefits are shared among those within their service area or connected to their existing membership base.

2. Credit Score and History

Your credit score is a critical factor in determining your loan eligibility and the interest rate you’ll receive. Telhio, like other lenders, uses your credit score as an indicator of your financial responsibility and ability to repay debt. A higher credit score (generally 670 and above) indicates lower risk and typically qualifies you for the best rates.

However, even if your credit isn’t perfect, Telhio often has programs or advice to help. They may offer loans for individuals with less-than-perfect credit, albeit possibly at a slightly higher interest rate, or suggest steps to improve your creditworthiness before applying. They are more likely than a large bank to consider your overall financial picture rather than just a single number.

3. Debt-to-Income (DTI) Ratio

Lenders assess your debt-to-income (DTI) ratio to understand how much of your monthly income is allocated to debt payments. This ratio helps determine if you can comfortably afford an additional car payment. A lower DTI ratio indicates a healthier financial situation and a greater capacity to take on new debt.

Telhio will calculate your DTI by dividing your total monthly debt payments (including the proposed car payment) by your gross monthly income. While there isn’t a universal cut-off, a DTI below 43% is generally considered favorable, though Telhio will review each case individually.

4. Proof of Income and Employment Stability

Telhio needs assurance that you have a stable and sufficient income source to make your monthly loan payments. This typically involves providing recent pay stubs, W-2 forms, or tax returns for self-employed individuals. Consistency in employment is also viewed favorably, demonstrating reliability.

Longer employment history with the same employer often signals stability, which can be a positive factor in your application.

5. Vehicle Specifics (for Used Cars)

For used car loans, the vehicle itself also plays a role in the approval process. Telhio may have specific requirements regarding:

- Vehicle Age: There might be a maximum age limit (e.g., no older than 10 years).

- Mileage: A maximum mileage cap (e.g., no more than 100,000 or 120,000 miles).

- Vehicle Value: The loan amount will be based on the vehicle’s market value, often determined by resources like Kelley Blue Book or NADA guides.

These restrictions help ensure the vehicle maintains sufficient collateral value throughout the loan term.

Maximizing Your Chances for Telhio Car Loan Approval

While meeting the basic requirements is essential, there are proactive steps you can take to significantly boost your likelihood of Telhio car loan approval and secure the best possible terms.

1. Improve Your Credit Score

Your credit score is paramount. Before applying, obtain a free copy of your credit report from AnnualCreditReport.com and review it for any inaccuracies. Dispute any errors promptly.

To actively improve your score:

- Pay Bills on Time: Payment history is the most significant factor.

- Reduce Existing Debt: Especially credit card balances, which lower your credit utilization.

- Avoid Opening New Credit Lines: Too many new inquiries can temporarily lower your score.

- Keep Old Accounts Open: A longer credit history is beneficial.

2. Reduce Your Debt-to-Income Ratio

Lowering your existing debt before applying for a car loan makes you a more attractive borrower. Focus on paying down high-interest debts like credit card balances.

Even a small reduction in your monthly debt obligations can positively impact your DTI, demonstrating greater financial capacity to take on a new car payment.

3. Save for a Down Payment

Making a larger down payment on your vehicle offers multiple advantages. It reduces the amount you need to borrow, which in turn lowers your monthly payments and the total interest paid over the loan term.

A substantial down payment also signals financial responsibility to Telhio and can offset slightly lower credit scores, as it reduces the credit union’s risk. Pro tip: Aim for at least 10-20% of the vehicle’s purchase price as a down payment if possible.

4. Consider a Co-Signer

If you have a limited credit history or a less-than-perfect credit score, adding a creditworthy co-signer can significantly improve your chances of approval. A co-signer, typically a trusted family member or friend, agrees to be equally responsible for the loan if you default.

However, understand the implications: if you fail to make payments, the co-signer’s credit will also be negatively impacted, and they will be legally obligated to repay the debt. Common mistakes people make include not fully discussing the responsibilities with a co-signer beforehand.

5. Know Your Budget and Stick to It

Before you even start shopping, determine how much you can realistically afford for a monthly car payment, including insurance and maintenance. Don’t just focus on the loan amount Telhio approves you for; consider your entire financial picture.

Telhio’s pre-approval helps set a maximum, but you should always choose a payment that fits comfortably within your budget, ensuring you don’t overextend yourself.

Telhio Car Loan vs. Traditional Banks: A Head-to-Head Comparison

While both credit unions and traditional banks offer car loans, understanding their fundamental differences can highlight why Telhio might be the superior choice for many borrowers.

Telhio Credit Union:

- Member-Owned: Profits are returned to members through better rates and services.

- Lower Rates: Often provides more competitive interest rates and lower fees due to its not-for-profit structure.

- Personalized Service: Focuses on building relationships and offering tailored solutions. You’re a member, not just a customer.

- Community Focus: Invests in the local community and understands local needs.

- Flexible Underwriting: May be more willing to work with members with less-than-perfect credit, considering their overall financial situation.

Traditional Banks:

- Shareholder-Owned: Focuses on maximizing profits for shareholders.

- Rates Can Vary: While competitive, their rates may not always match the lowest offerings from credit unions, especially for average credit scores.

- Standardized Service: Often offers more generalized customer service, which can feel less personal.

- Broader Reach: Typically has a larger branch network and wider geographical presence.

- Strict Criteria: May adhere more rigidly to credit score thresholds and automated decision-making.

For those prioritizing competitive rates, personalized attention, and a financial partner invested in their community, Telhio Credit Union often comes out ahead in the car loan arena.

Frequently Asked Questions (FAQ) about Telhio Car Loans

Here are answers to some common questions people have about securing an auto loan with Telhio Credit Union.

Q: Can I apply for a Telhio Car Loan online?

A: Yes, Telhio offers a convenient online application process for car loans and pre-approval, allowing you to apply from the comfort of your home. You can also apply by phone or in person at any branch.

Q: How long does it take to get approved for a Telhio Car Loan?

A: Approval times can vary, but Telhio is known for its efficient process. Many applicants receive a decision within one business day, especially if all required documents are submitted promptly. Pre-approval can often be even quicker.

Q: What if my credit isn’t perfect? Can I still get a Telhio Car Loan?

A: Telhio strives to assist all its members. While a strong credit score helps secure the best rates, Telhio may offer solutions for individuals with less-than-perfect credit. They encourage you to speak with a loan officer to discuss your options and potential steps to improve your creditworthiness.

Q: Can I get a Telhio Car Loan for a private party sale?

A: Yes, Telhio often provides financing for private party vehicle purchases. The process will involve Telhio verifying the vehicle’s title and value, and ensuring all necessary paperwork is completed for a smooth transfer of ownership.

Q: What’s the difference between APR and interest rate?

A: The interest rate is the percentage you pay on the principal loan amount. The Annual Percentage Rate (APR) is a broader measure of the cost of borrowing money, including the interest rate plus any additional fees or charges associated with the loan. The APR provides a more accurate representation of the total cost of your loan over a year. Telhio focuses on transparent APR disclosures.

Your Road Ahead: Driving Towards Financial Freedom with Telhio

Securing a car loan doesn’t have to be a daunting task. With Telhio Credit Union, you gain a trusted financial partner committed to providing transparent, competitive, and personalized auto loan solutions. From the initial pre-approval to driving your new vehicle off the lot, Telhio aims to make the process as smooth and beneficial as possible for its members.

By understanding the unique advantages of a credit union, preparing your application thoroughly, and leveraging the expert tips shared in this guide, you are well-positioned to unlock your dream ride with confidence. Telhio’s dedication to lower rates, flexible terms, and exceptional member service truly sets them apart.

Don’t let the financing process deter you from your next adventure. Explore the possibilities with a Telhio Car Loan today and experience the difference of a financial institution that genuinely puts its members first. Visit Telhio’s official website or contact their friendly loan officers to take the first step towards driving away in your ideal vehicle. Your journey to smart car ownership begins here.