Unlock Your Dream Ride: The Ultimate Guide to Suncoast Car Loans

Unlock Your Dream Ride: The Ultimate Guide to Suncoast Car Loans Carloan.Guidemechanic.com

Securing the right car loan can feel like navigating a complex maze. For residents across Florida, particularly in the Suncoast region, finding a reliable and advantageous financing partner is paramount. This is where Suncoast Car Loan options emerge as a beacon of opportunity, offering member-focused benefits that often surpass traditional banking institutions.

As an expert blogger and professional SEO content writer, I understand the importance of making informed financial decisions. Based on my extensive experience in the auto finance sector, delving into Suncoast Credit Union’s offerings reveals a truly compelling proposition for anyone looking to finance their next vehicle. This comprehensive guide will illuminate every facet of obtaining a Suncoast Car Loan, ensuring you’re equipped with the knowledge to drive away with confidence.

Unlock Your Dream Ride: The Ultimate Guide to Suncoast Car Loans

Understanding Suncoast Car Loans: Why Choose a Credit Union?

When considering vehicle financing, many instinctively turn to large national banks or dealership financing. However, overlooking credit unions like Suncoast could mean missing out on significant advantages. Suncoast Credit Union operates with a distinct philosophy: its members are its owners. This fundamental difference translates into tangible benefits for car loan applicants.

Unlike profit-driven banks, Suncoast’s primary goal is to serve its membership. This often results in more competitive interest rates, lower fees, and a more personalized loan experience. Based on my observations over the years, credit unions are consistently able to offer better terms because they return profits to members through improved services and rates, rather than distributing them to external shareholders.

Choosing a Suncoast Car Loan means you’re not just a number; you’re part of a community. Their dedicated loan officers often go the extra mile to understand your financial situation and tailor a solution that fits your budget. This personalized approach can be invaluable, especially for those with unique credit histories or specific financial goals.

Types of Suncoast Car Loans Available

Suncoast Credit Union offers a diverse portfolio of auto loan products designed to meet various needs, whether you’re buying new, used, or simply looking to improve your current loan terms. Understanding these options is the first step towards finding your ideal financing solution.

New Car Loans

Dreaming of that brand-new car smell and the latest features? Suncoast’s new car loans are specifically tailored for financing vehicles straight from the dealership. These loans typically come with competitive rates, reflecting the lower risk associated with brand-new automobiles.

When you secure a new Suncoast Car Loan, you’re often looking at flexible terms that can make monthly payments more manageable. It’s crucial to remember that while longer terms might mean lower monthly payments, they can also lead to more interest paid over the life of the loan. Pro tips from us include always balancing affordability with the total cost of borrowing.

Used Car Loans

Purchasing a pre-owned vehicle can be a smart financial move, offering excellent value. Suncoast provides robust used car loan options that are just as attractive as their new car counterparts. These loans are designed to finance vehicles that have had previous owners, often with specific age and mileage restrictions.

The terms and rates for used car loans might vary slightly compared to new car loans, primarily due to factors like the vehicle’s age, mileage, and overall condition. Based on my experience, Suncoast often offers highly competitive rates for used vehicles, making quality pre-owned cars more accessible. Always ensure the used vehicle you’re interested in meets their eligibility criteria before applying.

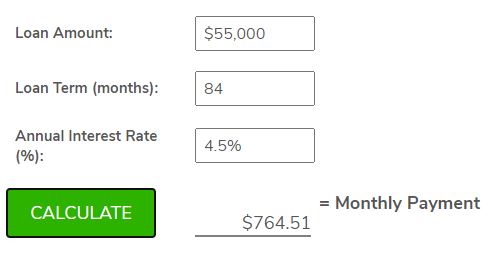

Auto Loan Refinancing

Perhaps you already have a car loan but are unhappy with the interest rate or monthly payment. Auto loan refinancing through Suncoast could be your solution. This process involves taking out a new loan to pay off your existing car loan, ideally with more favorable terms.

Refinancing can be a game-changer if your credit score has improved since you first financed your car, or if interest rates have dropped. It can also help if you want to lower your monthly payments by extending the loan term, or reduce the total interest paid by shortening it. Our professional advice is to regularly review your current loan against prevailing rates to see if refinancing with Suncoast Car Loan could save you money.

Lease Buyout Loans

At the end of a car lease, you often have the option to purchase the vehicle. If you’ve fallen in love with your leased car and want to make it permanently yours, Suncoast offers lease buyout loans. These loans are specifically designed to finance the residual value of your leased vehicle.

This option can be particularly beneficial if the car’s market value is higher than its residual value, or if you simply prefer to avoid the hassle of finding a new car. A Suncoast Car Loan for a lease buyout can provide a straightforward path to ownership, often with competitive rates that make the transition smooth and affordable.

Navigating the Suncoast Car Loan Application Process

Applying for a car loan can seem daunting, but Suncoast Credit Union strives to make the process as clear and efficient as possible. Understanding the steps involved and preparing adequately can significantly smooth your journey to approval.

Step-by-Step Application Guide

- Become a Member: Since Suncoast is a credit union, you’ll need to be a member to apply for a loan. Membership eligibility is typically based on living or working in specific Florida counties, or being related to an existing member. This is a quick and easy step, often done online.

- Gather Your Documents: Preparation is key. Have all necessary financial information at hand before you begin.

- Apply for Pre-Approval: This is a highly recommended step. Pre-approval gives you a clear understanding of how much you can borrow and at what rate, before you even step foot in a dealership.

- Shop for Your Car: With pre-approval in hand, you can shop with confidence, knowing your budget and financing terms.

- Finalize the Loan: Once you’ve found your perfect vehicle, Suncoast will work with you to complete the final loan paperwork.

Required Documents

To ensure a smooth application, be prepared to provide:

- Proof of Identity: Government-issued ID (driver’s license, passport).

- Proof of Income: Pay stubs, tax returns, or employment verification letters.

- Proof of Residency: Utility bill or lease agreement.

- Social Security Number: For credit checks.

- Vehicle Information (if applicable): VIN, make, model, year, and mileage for the car you intend to purchase.

Online vs. In-Branch Application

Suncoast offers the convenience of both online and in-branch applications. The online portal provides a streamlined process, allowing you to apply from the comfort of your home. However, if you prefer face-to-face interaction or have complex questions, visiting a local branch can provide personalized assistance. Based on my experience, both methods are efficient, but the online option is perfect for those who are tech-savvy and prefer speed.

Pre-Approval Benefits

Securing pre-approval for your Suncoast Car Loan offers several critical advantages. Firstly, it transforms you into a cash buyer at the dealership, giving you stronger negotiation power on the vehicle price. Dealers know you’re serious and have your financing sorted, which can lead to better deals.

Secondly, pre-approval helps you establish a clear budget, preventing you from falling in love with a car outside your financial comfort zone. It also separates the financing discussion from the car price negotiation, simplifying the overall buying process. Pro tips from us: always get pre-approved before serious car shopping.

Common Mistakes to Avoid Are:

- Not checking your credit score beforehand: This can lead to surprises and missed opportunities for better rates.

- Skipping pre-approval: You lose negotiating leverage and might be pressured into less favorable dealership financing.

- Ignoring the total cost of the loan: Focus only on monthly payments, not the overall interest paid.

- Providing incomplete documentation: This causes delays in the application process.

- Accepting the first offer: Always compare rates, even within Suncoast’s offerings if your financial situation has changed.

Key Factors Influencing Your Suncoast Car Loan Approval and Rates

Several critical elements come into play when Suncoast Credit Union evaluates your car loan application. Understanding these factors will empower you to improve your chances of approval and secure the most favorable interest rates.

Credit Score

Your credit score is arguably the most significant factor. It’s a numerical representation of your creditworthiness, reflecting your history of borrowing and repayment. A higher credit score signals lower risk to lenders, which typically translates into better interest rates on your Suncoast Car Loan.

If your score isn’t where you’d like it to be, focusing on improving it before applying can save you thousands over the life of the loan. This means paying bills on time, reducing outstanding debt, and avoiding opening too many new credit lines simultaneously.

Income and Debt-to-Income Ratio

Lenders want assurance that you can comfortably afford your monthly loan payments. Your income and your debt-to-income (DTI) ratio play a crucial role here. Your DTI is calculated by dividing your total monthly debt payments by your gross monthly income. A lower DTI indicates you have more disposable income to manage new debt.

Suncoast will assess your stable income source and evaluate your DTI to determine your repayment capacity. A strong, consistent income combined with a manageable DTI ratio significantly boosts your chances of approval and favorable terms.

Down Payment

Making a substantial down payment on your vehicle is one of the smartest financial moves you can make. It reduces the amount you need to borrow, which directly lowers your monthly payments and the total interest you’ll pay over the loan term.

Furthermore, a larger down payment signals financial stability to Suncoast, potentially leading to better interest rates. It also provides an immediate equity buffer, protecting you from being "upside down" on your loan (owing more than the car is worth) early in its life.

Loan Term

The loan term refers to the length of time you have to repay the loan. Suncoast typically offers various terms, from short (e.g., 36 months) to long (e.g., 72 or 84 months). While longer terms result in lower monthly payments, they also mean you’ll pay more in total interest because you’re borrowing the money for a longer period.

Based on my professional opinion, choosing the shortest loan term you can comfortably afford is usually the most financially savvy decision. It minimizes interest costs and gets you out of debt faster. However, if monthly budget constraints are paramount, a longer term with a Suncoast Car Loan can provide necessary flexibility.

Vehicle Age and Type

The vehicle itself plays a role in the loan assessment. Newer vehicles, especially those with good resale value, are generally considered less risky by lenders. They tend to depreciate slower and are less prone to mechanical issues that could impact your ability to make payments.

Older vehicles or those with high mileage might come with slightly higher interest rates or require a larger down payment due to increased risk. Suncoast, like other lenders, considers the vehicle’s market value and its expected lifespan when approving a loan.

Pro Tips for Securing the Best Suncoast Car Loan Deal

Navigating the car loan landscape can be tricky, but with the right strategies, you can significantly improve your chances of landing an exceptional deal with Suncoast Credit Union. Here are some insider tips from us.

Improve Your Credit Score Beforehand

This cannot be stressed enough. A few months of diligent effort to boost your credit score can unlock significantly lower interest rates. Pay off small debts, dispute any errors on your credit report, and ensure all your payments are on time. Even a 20-point increase can make a difference in your Suncoast Car Loan terms.

Save for a Larger Down Payment

Aim for at least 10-20% of the vehicle’s purchase price as a down payment. This reduces the amount you finance, lowers your monthly payments, and shows Suncoast that you’re a responsible borrower. A substantial down payment also reduces your risk of negative equity.

Shop Around (Even Within Suncoast’s Offerings)

While Suncoast offers competitive rates, it’s still wise to compare their specific offers against your pre-approval from other institutions if you’ve explored multiple options. Also, don’t hesitate to ask Suncoast if there are any special promotions or slightly better rates you might qualify for based on a slightly different term or down payment.

Negotiate the Car Price First

When you’re at the dealership, keep your car purchase and your financing separate. Negotiate the absolute best price for the vehicle before discussing financing. If you’ve secured a Suncoast Car Loan pre-approval, you can confidently tell the dealer you already have financing, removing their ability to make up for a lower car price with a higher interest rate.

Understand the Fine Print

Before signing any loan document, read every line. Pay close attention to the interest rate (APR), the loan term, any fees (origination, late payment), and prepayment penalties (though these are less common with credit unions). If anything is unclear, ask your Suncoast loan officer for clarification. It’s your money and your commitment, so be fully informed.

Consider a Co-Signer (Pros and Cons)

If your credit score is less than ideal, or if you’re a young borrower without much credit history, a co-signer with excellent credit can significantly improve your chances of approval and secure a better rate on your Suncoast Car Loan.

However, understand the implications: the co-signer is equally responsible for the debt. If you miss payments, it impacts their credit, and they could be liable for the full amount. This should only be considered with someone you trust implicitly, and who understands the full scope of their commitment.

Beyond the Loan: Suncoast’s Member Benefits and Resources

Obtaining a Suncoast Car Loan is just one aspect of the value a credit union offers. As a member, you gain access to a wider ecosystem of financial support and resources designed to help you thrive. This holistic approach sets credit unions apart.

Suncoast Credit Union often provides comprehensive financial education resources. These can range from workshops on budgeting and debt management to online articles and tools that help you understand various financial products. Leveraging these resources can empower you to make smarter decisions not just about your car loan, but across your entire financial life.

Beyond auto loans, Suncoast typically offers a full suite of banking services, including checking and savings accounts, mortgages, personal loans, and credit cards. Consolidating your financial services with one institution can often simplify management and, in some cases, lead to better overall rates or benefits due to your comprehensive relationship with the credit union. They may also partner with insurance providers to offer competitive rates on auto insurance, further streamlining your car ownership experience.

Common Myths and Misconceptions About Car Loans

Misinformation can lead to poor financial decisions. Let’s debunk some prevalent myths surrounding car loans, especially as they relate to securing a Suncoast Car Loan.

Myth 1: "You Need Perfect Credit to Get a Car Loan."

Reality: While excellent credit will undoubtedly secure you the best rates, it’s a misconception that you need a flawless score to get approved. Suncoast, like many lenders, considers a range of credit scores. They look at your overall financial picture, including income, employment history, and debt-to-income ratio. There are often programs for those with fair or even limited credit, though rates may be higher.

Myth 2: "Pre-Approval is a Commitment."

Reality: Pre-approval for a Suncoast Car Loan is a conditional offer, not a binding commitment. It simply tells you how much you’re approved for and at what rate, giving you valuable information to shop for a vehicle. You are under no obligation to accept that specific loan or even purchase a car if you change your mind. It’s a powerful tool for empowering you, not restricting you.

Myth 3: "Always Take the Longest Term for Lower Payments."

Reality: While a longer loan term (e.g., 72 or 84 months) will indeed result in lower monthly payments, it almost always means you’ll pay significantly more in total interest over the life of the loan. You’ll also build equity slower and could be "upside down" on your loan for a longer period. As an expert, I advise balancing affordability with the total cost; shorter terms are generally more financially advantageous if manageable.

Myth 4: "Dealership Financing is Always the Easiest and Best Option."

Reality: Dealership financing can be convenient, but it’s not always the best deal. Dealers often work with multiple lenders and may mark up interest rates to increase their profit. By securing a Suncoast Car Loan pre-approval, you empower yourself to compare offers and ensure you’re getting the most competitive rate, rather than simply accepting the dealer’s first offer.

Conclusion: Your Journey to a Smart Suncoast Car Loan

Navigating the world of auto financing can be complex, but with the comprehensive insights provided in this guide, you are now well-equipped to make an informed decision. Choosing a Suncoast Car Loan means opting for a member-centric approach, often leading to competitive rates, flexible terms, and personalized service that goes beyond what traditional banks typically offer.

From understanding the various loan types—new, used, refinancing, and lease buyouts—to mastering the application process and knowing the key factors that influence your rates, you have a robust framework. Remember to leverage pro tips like improving your credit score, making a substantial down payment, and always securing pre-approval to strengthen your negotiating position.

By avoiding common mistakes and debunking prevalent myths, you can approach your car purchase with confidence and clarity. Suncoast Credit Union stands as a strong partner for your auto financing needs in Florida, offering not just a loan, but a pathway to responsible vehicle ownership and broader financial well-being. Drive smart, drive confidently, and let Suncoast help you get behind the wheel of your dream car. Start your Suncoast Car Loan journey today and experience the credit union difference.