Unlock Your Dream Ride: The Ultimate Guide to the SECU Used Car Loan Calculator

Unlock Your Dream Ride: The Ultimate Guide to the SECU Used Car Loan Calculator Carloan.Guidemechanic.com

Buying a used car can be an exciting journey, opening doors to affordability, reliability, and the freedom of the open road. However, for many, the path to ownership is often clouded by questions about financing: "How much can I truly afford?", "What will my monthly payments look like?", and "Am I getting the best deal?". Navigating the complexities of interest rates, loan terms, and down payments can feel overwhelming.

This is where a powerful tool like the SECU Used Car Loan Calculator becomes your indispensable co-pilot. It’s more than just a number cruncher; it’s a strategic ally designed to bring clarity and confidence to your car buying experience. In this comprehensive guide, we’ll dive deep into how this calculator works, why it’s crucial for every prospective buyer, and how you can leverage its insights to make smart, informed decisions. Our ultimate goal is to empower you to drive away in your ideal used car, knowing you’ve secured a loan that fits comfortably within your budget.

Unlock Your Dream Ride: The Ultimate Guide to the SECU Used Car Loan Calculator

Decoding the Mystery: What is a SECU Used Car Loan Calculator?

At its core, a loan calculator is a digital tool that helps you estimate the costs associated with borrowing money. Specifically, a SECU Used Car Loan Calculator is tailored to the nuances of financing a pre-owned vehicle through the State Employees’ Credit Union (SECU). It allows you to input key financial variables and, in return, provides a clear projection of your potential monthly payments, total interest paid, and the overall cost of your loan.

This sophisticated tool simplifies what would otherwise be a complex series of calculations. Instead of manually figuring out amortization schedules, the calculator does the heavy lifting instantly. It acts as a financial crystal ball, giving you a sneak peek into your future financial commitments before you even step onto a dealership lot. Its primary function is to demystify the loan process, transforming abstract financial terms into concrete, understandable figures.

Why Every Used Car Buyer Needs a Loan Calculator (Especially SECU’s)

Think of the SECU Used Car Loan Calculator as your personal financial advisor for car buying. It’s not just about crunching numbers; it’s about gaining control and making empowered decisions. Here’s why it’s an absolute must-have for anyone considering a used car loan:

Budgeting Brilliance: Setting Realistic Financial Boundaries

One of the biggest mistakes car buyers make is falling in love with a car they can’t truly afford. The calculator helps you avoid this heartbreak by establishing a clear budget from the outset. By experimenting with different loan amounts, you can quickly see what price range of vehicles aligns with your comfortable monthly payment.

This proactive approach ensures that your used car purchase enhances your life, rather than becoming a source of financial stress. Based on my experience, many buyers overlook the crucial step of budgeting before shopping, leading to emotional decisions that can have long-term negative impacts on their finances.

Payment Prediction: Understanding Your Monthly Commitment

Your monthly car payment will be a regular fixture in your budget for years to come. The SECU Used Car Loan Calculator provides an accurate estimate of this critical figure, allowing you to integrate it into your existing financial plan. You can adjust variables like the loan term or down payment to find a monthly payment that feels manageable.

This foresight prevents surprises and ensures that your new car payment doesn’t strain your other financial obligations. Knowing your exact monthly outlay empowers you to plan your finances with precision.

Interest Insights: Unveiling the True Cost of Borrowing

The sticker price of a used car only tells part of the story. The total amount you pay for the vehicle will also include the interest accrued over the life of the loan. The calculator clearly breaks down how much interest you’ll pay in total, revealing the true cost of borrowing.

Understanding this figure is vital for making cost-effective decisions. Pro tips from us: a lower interest rate and a shorter loan term will significantly reduce the total interest you pay, saving you hundreds or even thousands of dollars over time.

Term Tweakability: Experimenting with Loan Durations

Loan terms, often ranging from 24 to 72 months (or even longer), have a dramatic impact on both your monthly payment and the total interest. The calculator allows you to instantly see how extending or shortening the loan term affects these figures. A longer term means lower monthly payments but typically higher total interest paid.

Conversely, a shorter term results in higher monthly payments but less interest overall. Experimenting with these variables helps you strike the perfect balance between affordability and cost efficiency.

Empowered Negotiation: Gaining Leverage with Pre-Calculated Figures

Walking into a dealership with a clear understanding of your financing options puts you in a powerful negotiating position. If you’ve already used the SECU Used Car Loan Calculator to determine your ideal loan amount, monthly payment, and even an estimated interest rate (based on SECU’s current offerings and your credit profile), you’re less likely to be swayed by unfavorable terms.

You can confidently discuss financing with the dealer, knowing exactly what kind of deal you’re looking for. This preparation can lead to significant savings and a more favorable loan agreement.

Avoiding Pitfalls: Preventing Overcommitment

One of the common mistakes to avoid is overextending yourself financially. Without a calculator, it’s easy to get caught up in the excitement of a purchase and agree to payments that are unsustainable. The calculator serves as a reality check, providing a clear picture of your financial commitment.

It helps ensure that your car purchase aligns with your long-term financial health, rather than becoming a burden. This preventative measure is invaluable for smart financial planning.

Key Factors Influencing Your SECU Used Car Loan Calculation

Several critical variables feed into the SECU Used Car Loan Calculator to produce your estimated payment. Understanding each of these components is fundamental to accurately predicting your loan costs and making informed decisions.

Loan Amount: The Core of Your Borrowing

The loan amount is simply the total sum of money you need to borrow after your down payment and trade-in (if any) have been applied. This figure directly correlates with the price of the used car you intend to purchase. A higher loan amount will naturally result in higher monthly payments and a greater total interest paid, assuming all other factors remain constant.

When inputting this into the calculator, it’s crucial to consider the actual sale price of the vehicle you’re eyeing. Remember to also factor in any additional costs like taxes, registration fees, and extended warranties if you plan to roll them into the loan.

Interest Rate (APR): The Cost of Borrowing

The interest rate, often expressed as an Annual Percentage Rate (APR), is arguably the most significant factor impacting the total cost of your loan. It represents the percentage of the loan principal that lenders charge you for borrowing their money. A lower APR means you’ll pay less interest over the life of the loan, resulting in significant savings.

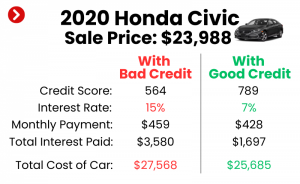

Several factors influence the interest rate you’ll be offered, including your credit score, the loan term, the age of the used car, and SECU’s current market rates. Pro tips from us: a strong credit score is your best friend here, as it signals to lenders that you are a low-risk borrower, qualifying you for the most competitive rates.

Loan Term (Repayment Period): Balancing Payments and Total Cost

The loan term refers to the length of time you have to repay the loan, typically measured in months (e.g., 36, 48, 60, or 72 months). This variable has a direct inverse relationship with your monthly payment and a direct relationship with the total interest paid. A longer loan term will result in lower monthly payments, making the car seem more affordable in the short term.

However, stretching out the repayment period means you’ll be paying interest for a longer duration, significantly increasing the total amount of interest you’ll ultimately pay. Common mistakes to avoid are choosing an excessively long loan term just to achieve a low monthly payment, as this can cost you much more in the long run. Conversely, a shorter term means higher monthly payments but substantial savings on total interest.

Down Payment: Your Upfront Investment

A down payment is the initial sum of money you pay towards the purchase of the car, reducing the amount you need to borrow. This upfront investment is a powerful tool for reducing your overall loan cost. A larger down payment directly decreases your loan amount, which in turn lowers your monthly payments and reduces the total interest you’ll pay over the life of the loan.

Beyond the financial savings, making a substantial down payment can also make you a more attractive borrower to lenders, potentially qualifying you for better interest rates. It demonstrates financial responsibility and reduces the lender’s risk.

A Step-by-Step Guide: How to Use the SECU Used Car Loan Calculator Effectively

Using the SECU Used Car Loan Calculator is straightforward, but maximizing its potential requires a strategic approach. Follow these steps to unlock its full power:

- Locate the Calculator: Begin by navigating to the official SECU website and finding their auto loan or used car loan section. The calculator is usually prominently displayed there.

- Input Your Desired Loan Amount: Start with the approximate price of the used car you’re considering, minus any down payment or trade-in value you anticipate. For example, if a car costs $20,000 and you plan a $4,000 down payment, your loan amount would be $16,000.

- Enter Your Estimated Interest Rate: This is where things can get a bit tricky if you haven’t been pre-approved. You can use SECU’s advertised "starting at" rates for used cars as a baseline, but remember these are typically for borrowers with excellent credit. A more realistic approach might be to use a slightly higher rate if your credit score isn’t perfect. If you’ve already been pre-approved by SECU, use that specific rate.

- Select Your Desired Loan Term: Choose the number of months you’d like to take to repay the loan (e.g., 48, 60, 72 months).

- Interpret the Results: The calculator will instantly display your estimated monthly payment, and often, the total interest you’ll pay over the life of the loan. This gives you a clear picture of your financial commitment.

- Experiment with Scenarios: This is where the real value comes in. Don’t just run one calculation. Try different scenarios:

- Vary the Down Payment: How does an extra $1,000 down payment affect your monthly payment and total interest?

- Adjust the Loan Term: What’s the difference between a 60-month and a 72-month loan? Is the lower monthly payment worth the extra interest?

- Consider Different Interest Rates: What if your credit score improves and you qualify for a lower rate? Or if it’s slightly higher than anticipated?

Pro tips from us: Always run several scenarios. This iterative process helps you identify the sweet spot where your monthly payment is manageable, and the total cost of the loan is acceptable.

Beyond the Calculator: Maximizing Your SECU Used Car Loan Approval & Savings

While the calculator is an incredible tool, securing the best possible SECU used car loan involves more than just plugging in numbers. It requires proactive steps to strengthen your financial profile.

Credit Score Optimization: Your Financial Report Card

Your credit score is a three-digit number that profoundly impacts the interest rate you’ll be offered. A higher score signifies lower risk to lenders, leading to more favorable terms. Strategies to improve it include consistently paying all your bills on time, reducing outstanding debt, and avoiding opening too many new credit accounts in a short period.

From years of observing loan applications, I can confirm that even a small improvement in your credit score can translate into significant savings on interest over the life of a car loan. It’s truly worth the effort to monitor and improve your credit.

Pre-Approval Power: Knowing Your Buying Muscle

Getting pre-approved for a loan by SECU before you start serious car shopping is one of the smartest moves you can make. Pre-approval gives you a concrete loan amount and an actual interest rate you qualify for. This transforms you into a "cash buyer" at the dealership, giving you immense negotiating power.

You’ll know exactly how much you can spend, which simplifies your car search and prevents you from falling for cars outside your budget. It also streamlines the final purchasing process.

Smart Down Payment Strategies: Boosting Your Equity

Saving up for a substantial down payment is a highly effective strategy for reducing your overall loan cost. Not only does it lower your monthly payments, but it also reduces the total interest paid and can help you qualify for better rates. Aim for at least 10-20% of the car’s purchase price if possible.

Even a modest down payment can make a noticeable difference in your financial burden. Consider setting up an automatic savings plan specifically for your car down payment.

Understanding SECU’s Specific Offerings: Member Benefits

As a credit union, SECU often offers competitive rates and member-focused benefits that might not be available at traditional banks. This could include flexible repayment options, personalized service, and sometimes even discounts for existing members. Familiarize yourself with their specific used car loan programs.

Remember, credit unions like SECU are member-owned, meaning their profits are often returned to members in the form of lower rates and fees. Check their membership eligibility requirements if you’re not already a member.

Debt-to-Income Ratio: A Lender’s Perspective

Lenders, including SECU, will also look at your debt-to-income (DTI) ratio. This ratio compares your total monthly debt payments to your gross monthly income. A lower DTI ratio indicates that you have more disposable income to manage new debt, making you a less risky borrower. Aim to keep your DTI below 36% for the best loan opportunities.

Common Mistakes to Avoid When Using a Car Loan Calculator

Even with a sophisticated tool like the SECU Used Car Loan Calculator, it’s easy to make missteps that can lead to inaccurate projections or poor financial decisions. Based on countless consultations, these errors frequently derail the best intentions:

- Ignoring Additional Costs: Many buyers only factor in the car’s price. Remember to account for sales tax, registration fees, title fees, and potential add-ons like extended warranties or GAP insurance. These can significantly increase the total loan amount.

- Underestimating Interest Rates: Using a generic "average" interest rate found online, or SECU’s absolute lowest advertised rate, can lead to a misleadingly low monthly payment estimate. Always strive to get a personalized rate quote or use a conservative estimate if you’re unsure of your credit’s impact.

- Focusing Only on Monthly Payment: While an affordable monthly payment is important, obsessing over it without considering the total interest paid can be a costly mistake. A lower monthly payment often comes at the expense of a longer loan term and much higher total interest.

- Not Shopping Around (Even for the Calculator): While we’re focusing on SECU, it’s wise to understand the market. Briefly compare SECU’s general rates and calculator results with those from other reputable lenders (banks, other credit unions) to ensure you’re getting a competitive offer. This broader view helps confirm SECU’s value.

- Forgetting Pre-Approval: Relying solely on the calculator without getting pre-approved by SECU means you don’t have a guaranteed rate or loan amount. Pre-approval provides concrete figures, transforming estimates into realities.

Real-World Scenarios: How the SECU Used Car Loan Calculator Empowers You

Let’s look at how the SECU Used Car Loan Calculator can be applied to common car buying dilemmas:

- Scenario 1: Budgeting for a Specific Car: You’ve found a used sedan for $18,000. You have $3,000 for a down payment. You input $15,000 as the loan amount. By trying 48, 60, and 72-month terms with an estimated 6% APR, you quickly see how your monthly payment changes from, say, $352 (48 months) to $290 (60 months) to $248 (72 months). This helps you decide which term fits your budget without overstretching.

- Scenario 2: Deciding Between Two Cars: You’re torn between a $15,000 compact car and a $22,000 SUV. Using the calculator, you can quickly compare the estimated monthly payments for each vehicle, assuming the same down payment and loan term. This quantitative comparison helps you make a logical choice based on affordability, not just desire.

- Scenario 3: Comparing Different Down Payment Options: You’re considering a $20,000 car. What’s the impact of a $2,000 down payment versus a $5,000 down payment? The calculator will show you how that $3,000 difference upfront translates into a significant reduction in your monthly payment and total interest, highlighting the value of saving more.

- Scenario 4: Impact of Credit Score on Rates: You estimate your credit score might qualify you for 7% APR, but you’re working to improve it and hope for 5% APR. The calculator can instantly show you the difference in monthly payments and total interest paid between these two rates, motivating you to boost your score.

Frequently Asked Questions About SECU Used Car Loans

Here are some common questions prospective buyers have about SECU and their used car loans:

- What credit score do I need for a SECU loan? While SECU doesn’t publish a minimum credit score, generally, higher scores (670+) will qualify for their best rates. They consider your entire financial picture, so even with a lower score, you might still qualify, albeit potentially at a higher interest rate.

- Can I get a SECU loan with bad credit? SECU is known for being member-focused. While a low credit score might make it challenging, they may offer options like secured loans or require a co-signer. It’s always best to speak directly with a SECU loan officer to discuss your specific situation.

- What documents do I need for a SECU car loan? Typically, you’ll need proof of income (pay stubs, tax returns), identification (driver’s license), proof of residence, and information about the vehicle you intend to purchase. For pre-approval, some of these may be requested upfront.

- How long does SECU pre-approval last? Pre-approvals usually have an expiration date, often around 30-60 days. This gives you ample time to shop for a car with confidence, but be mindful of the timeframe.

Your Road to a Smarter Used Car Purchase Starts Here

The journey to owning a used car should be exciting and financially sound, not stressful. The SECU Used Car Loan Calculator is an incredibly powerful tool designed to give you the clarity, control, and confidence you need to make informed decisions. It empowers you to budget wisely, understand the true cost of borrowing, and negotiate from a position of strength.

Don’t leave your used car financing to guesswork. Leverage the insights provided by this calculator to explore different scenarios, optimize your loan terms, and ultimately secure a used car loan that aligns perfectly with your financial goals. Your dream car is within reach, and with the right tools, you can drive it home without a single regret. Start your calculations today and embark on a smarter, more confident car buying adventure!