Unlock Your Dream Ride: The Ultimate Guide to Using a Car Loan Calculator in NC

Unlock Your Dream Ride: The Ultimate Guide to Using a Car Loan Calculator in NC Carloan.Guidemechanic.com

The excitement of getting a new car – the fresh scent, the smooth ride, the promise of new adventures – is a feeling almost everyone can relate to. But before you hit the open roads of North Carolina, there’s a crucial step that can make or break your car-buying experience: understanding the financing. For many, this part feels like navigating a dense fog, filled with confusing terms and hidden costs.

This is where your most powerful tool comes into play: the Car Loan Calculator NC. It’s not just a simple online gadget; it’s your personal financial compass, designed to give you clarity and confidence. In this comprehensive guide, we’ll dive deep into how to use this essential tool, understand its outputs, and leverage it to secure the best possible deal on your next vehicle in the Tar Heel State.

Unlock Your Dream Ride: The Ultimate Guide to Using a Car Loan Calculator in NC

Why a Car Loan Calculator is Your Best Friend (Especially in NC)

Buying a car is one of the most significant financial decisions many people make, second only to purchasing a home. Without proper planning, you could end up with monthly payments that strain your budget or pay far more in interest than necessary. This is precisely why a reliable car loan calculator is indispensable.

First and foremost, it demystifies the complex world of car financing. Instead of guessing what your monthly payment might be, the calculator provides concrete figures based on various inputs. This immediate feedback helps you visualize your financial commitment clearly, transforming abstract numbers into tangible realities.

Secondly, a calculator empowers you to budget effectively. Knowing your approximate monthly payment allows you to assess your affordability and determine how a car loan fits into your overall financial picture. It helps prevent the common pitfall of falling in love with a car that’s ultimately out of your price range.

Finally, having these figures at your fingertips gives you significant negotiation power. When you walk into a dealership armed with a clear understanding of what you can afford and what a reasonable loan term looks like, you’re less likely to be swayed by high-pressure sales tactics. You can confidently discuss loan terms, interest rates, and overall costs, ensuring you’re getting a fair deal.

How a Car Loan Calculator Works: The Core Components

At its heart, a car loan calculator is a sophisticated tool that takes several key pieces of information and computes your potential monthly payment and total loan cost. Understanding each component is vital for accurate results.

1. Loan Amount (Principal)

This is the total sum of money you intend to borrow after any down payment or trade-in value has been subtracted. It represents the actual price of the vehicle you are financing, plus any additional fees rolled into the loan. Be realistic about the vehicle price you’re targeting.

2. Interest Rate (APR)

The Annual Percentage Rate (APR) is arguably the most crucial factor, as it represents the true cost of borrowing money. It’s expressed as a percentage and directly impacts how much extra you’ll pay over the life of the loan. A lower APR means less money spent on interest.

Your creditworthiness, the loan term, and current market conditions heavily influence the APR you qualify for. Shopping around for the best rates before visiting a dealership can save you thousands of dollars.

3. Loan Term

The loan term refers to the duration over which you will repay the loan, typically expressed in months (e.g., 36, 48, 60, 72, or even 84 months). While a longer term can result in lower monthly payments, it almost always leads to paying significantly more in total interest over time. Conversely, a shorter term means higher monthly payments but less overall interest paid.

4. Down Payment

A down payment is the initial sum of money you pay upfront towards the purchase of the vehicle. Making a larger down payment reduces the amount you need to borrow, which in turn lowers your monthly payments and the total interest accrued. It also demonstrates financial stability to lenders, potentially helping you secure a better interest rate.

5. Trade-in Value

If you’re trading in your current vehicle, its value will be deducted from the purchase price of your new car, similar to a down payment. It reduces the amount you need to finance, offering the same benefits as a cash down payment. Always research your trade-in value beforehand to ensure you’re getting a fair offer.

6. Sales Tax & Fees (NC Specifics!)

Don’t forget these crucial additions! In North Carolina, you’ll primarily contend with the 3% Highway Use Tax (HUT) on the sales price of the vehicle. This is effectively North Carolina’s sales tax on vehicles and is capped at $1,500 for certain heavy-duty vehicles, but for most passenger cars, it’s a straightforward 3%.

Beyond HUT, you might encounter dealer documentation fees, title fees, and registration fees. While some of these are fixed, others can vary, so it’s essential to factor them into your overall cost. Always ask for a detailed breakdown of all fees.

Understanding the Numbers: What Your Calculation Reveals

Once you input all the necessary information into your Car Loan Calculator NC, it will present you with several key outputs. These numbers are your roadmap to financial understanding.

1. Monthly Payment

This is the most immediate and often the most scrutinized output. It tells you exactly how much you’ll need to pay each month for the duration of your loan. It’s crucial to ensure this figure comfortably fits within your monthly budget, leaving room for other essential expenses and savings.

2. Total Interest Paid

This number reveals the full cost of borrowing money over the entire loan term. It’s the amount you pay in addition to the principal loan amount. This figure often surprises people, highlighting the importance of securing a low APR and considering a shorter loan term if feasible. It makes the abstract concept of "interest" very real.

3. Total Cost of the Loan

This is the grand total you will pay for your vehicle, encompassing the original loan amount plus all the interest accrued over the loan term. It’s the ultimate figure to consider when evaluating the true expense of your car purchase. Comparing this total cost across different loan offers can provide invaluable insights.

Factors Influencing Your Car Loan in North Carolina

While the calculator provides estimates, several underlying factors will determine the actual loan terms you’re offered by lenders in North Carolina. Understanding these can help you improve your chances of securing favorable rates.

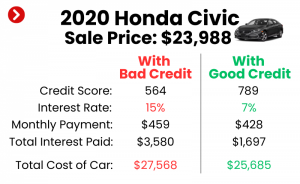

1. Your Credit Score

This is, without a doubt, the most significant factor. Lenders use your credit score to assess your creditworthiness and the likelihood of you repaying the loan. A higher credit score (generally 700+) indicates lower risk, leading to lower interest rates. Conversely, a lower score will result in higher rates to compensate the lender for the increased risk.

It’s wise to check your credit score well before applying for a car loan. This gives you time to correct any errors and understand where you stand.

2. Your Income & Debt-to-Income (DTI) Ratio

Lenders want to ensure you have a stable income sufficient to cover your monthly payments. Your debt-to-income (DTI) ratio, which compares your total monthly debt payments to your gross monthly income, is also crucial. A lower DTI ratio (ideally below 40%) signals that you’re not overextended financially and are more likely to manage new debt responsibly.

3. Vehicle Type (New vs. Used)

New cars often come with lower interest rates from lenders, primarily because they are considered less risky due to their higher value and manufacturer warranties. Used cars, while generally more affordable upfront, can sometimes have slightly higher interest rates, reflecting their increased depreciation and potential for unforeseen issues. However, specific promotional offers can sometimes reverse this trend.

4. Loan Term

As discussed, the length of your loan directly impacts your interest rate. Shorter terms typically come with lower interest rates because the lender’s risk exposure is reduced. Longer terms, while offering lower monthly payments, carry higher overall interest rates due to the extended period of risk for the lender.

5. Market Conditions

General economic factors, such as the Federal Reserve’s interest rate policies, can influence auto loan rates across the board. When interest rates are low nationally, you’re likely to find more favorable car loan rates. These conditions are outside your control but are important to be aware of.

6. Lender Type

The type of institution you borrow from can also affect your rates and terms.

- Banks: Offer competitive rates, especially to customers with good credit.

- Credit Unions: Often known for offering slightly better rates due to their member-owned structure.

- Captive Finance Companies: These are financing arms of car manufacturers (e.g., Toyota Financial Services, Ford Credit). They often have special promotional rates, especially for new cars.

- Online Lenders: Can provide quick approvals and competitive rates, often through streamlined digital processes.

Pro Tips for Using Your NC Car Loan Calculator Effectively

To truly maximize the benefits of your Car Loan Calculator NC, adopt these expert strategies. Based on my experience guiding countless individuals through the car buying process, these tips can significantly improve your outcome.

-

Shop Around for Rates Before You Visit the Dealership: This is a golden rule. Don’t wait until you’re at the dealership to think about financing. Get pre-approved by several lenders (banks, credit unions, online lenders) beforehand. This gives you a benchmark rate and strengthens your negotiation position. The dealership might even beat your pre-approved rate to earn your business.

-

Experiment with Different Scenarios: Play around with the calculator. See how increasing your down payment by $1,000 impacts your monthly payment and total interest. Compare a 60-month term to a 72-month term. This "what-if" analysis helps you understand the trade-offs and find a comfortable balance between monthly payments and total cost.

-

Factor In Additional Ownership Costs: Your car payment is just one piece of the puzzle. Remember to consider insurance, fuel, maintenance, and potential repair costs when determining your overall affordability. A lower monthly payment might seem attractive, but if the car is a gas guzzler or known for expensive repairs, your total budget could still be strained.

-

Understand Pre-Approval vs. Final Approval: Pre-approval gives you an estimate based on a soft credit check and the information you provide. Final approval comes after a hard credit check and verification of all your financial details. While pre-approval is a strong indicator, it’s not a guarantee until the final paperwork is signed.

-

Don’t Just Focus on the Monthly Payment: This is a common mistake. While a low monthly payment is appealing, it can sometimes mask a very long loan term or a high interest rate, leading to a much higher total cost. Always look at the total interest paid and the total cost of the loan to understand the true financial impact.

Navigating Car Loans with Less-Than-Perfect Credit in North Carolina

Having a less-than-stellar credit score doesn’t mean you can’t get a car loan in North Carolina, but it does mean you’ll likely face higher interest rates. Lenders view lower credit scores as a higher risk, and they compensate for this risk by charging more. However, there are strategies to improve your situation.

- Be Prepared for Higher Rates: Acknowledge that your initial offers might not be ideal. Use the Car Loan Calculator NC to see how higher interest rates impact your payments, so you’re not surprised.

- Consider a Larger Down Payment: Putting down more cash upfront reduces the amount you need to borrow, which can offset some of the impact of a higher interest rate and show the lender your commitment.

- Opt for a Shorter Loan Term: If your budget allows, a shorter loan term can sometimes help reduce the interest rate, even with lower credit. It also means you pay off the car faster, reducing the total interest paid.

- Find a Co-signer: If you have a trusted friend or family member with excellent credit, they can co-sign the loan. Their strong credit history can help you qualify for a better rate, but remember, they become equally responsible for the debt.

- Explore Secured Loans: Some lenders offer secured auto loans, where the car itself acts as collateral. While these might have slightly better rates than unsecured options for those with poor credit, it means the car can be repossessed if you default.

- Focus on Building Credit: If you’re not in a rush, take time to improve your credit score. Pay all your bills on time, reduce existing debt, and avoid opening new credit accounts. For more in-depth advice, you might find our guide on Understanding Your Credit Score: A Comprehensive Guide helpful.

The NC Specifics: What to Know About Auto Loans in North Carolina

Beyond the general financing principles, there are a few North Carolina-specific details you should be aware of when calculating and securing your car loan.

- Highway Use Tax (HUT): As mentioned, the 3% Highway Use Tax is a significant part of your vehicle’s cost. This tax is typically paid at the time of vehicle registration and is based on the purchase price or fair market value, whichever is greater. It’s often rolled into your loan, increasing the amount you finance. You can find more detailed information on vehicle taxes and fees on the official NC Department of Motor Vehicles website.

- Documentation Fees: While dealers in North Carolina are allowed to charge documentation fees (or "doc fees"), these should be clearly itemized and explained. These fees cover the cost of preparing and processing paperwork. While negotiable to some extent, they are generally a standard charge.

- Title and Registration Fees: These are state-mandated fees for transferring ownership and registering your vehicle with the NC DMV. They are relatively minor compared to the HUT but still contribute to your overall cost.

- North Carolina Lemon Law: While not directly related to your loan calculation, it’s reassuring to know that North Carolina has a Lemon Law to protect consumers who purchase new vehicles with significant, unfixable defects. This provides a layer of protection for your investment.

Common Mistakes to Avoid When Financing a Car in NC

Navigating the car financing landscape can be tricky, and even experienced buyers can make missteps. Common mistakes to avoid when securing your car loan in North Carolina are:

- Focusing Only on the Monthly Payment: This is perhaps the biggest pitfall. A dealership might stretch out your loan term to 84 months to offer a "low" monthly payment, but this drastically increases the total interest you’ll pay and can leave you upside down on your loan (owing more than the car is worth) for years. Always consider the total cost.

- Not Getting Pre-Approved: Walking into a dealership without a pre-approval is like going to a battle without a weapon. You lose significant leverage when you rely solely on the dealer’s financing options.

- Ignoring the Total Cost of the Loan: Beyond the monthly payment, the total amount of principal plus interest over the entire loan term is your true cost. Overlooking this number can lead to financial regret.

- Falling for Unnecessary Add-ons: Be wary of high-pressure sales for extended warranties, GAP insurance (while often beneficial, compare prices), paint protection, or other add-ons that significantly inflate your loan amount and interest. Evaluate each one carefully and decide if it truly adds value for you.

- Not Reading the Fine Print: Before signing any document, read the loan agreement thoroughly. Understand all the terms, conditions, and any prepayment penalties. If something is unclear, ask for clarification.

- Neglecting Your Trade-in Value Research: Don’t just accept the dealer’s first offer for your trade-in. Research its value using reputable sources like Kelley Blue Book or Edmunds. Knowing its true worth ensures you’re getting a fair deal, or helps you decide to sell it privately instead. For more negotiation tips, check out our article on Navigating Car Dealerships: Tips for a Smooth Purchase.

Beyond the Calculator: Steps to Secure Your Car Loan in NC

Once you’ve diligently used your Car Loan Calculator NC and feel confident in your budget, here are the practical steps to finalize your car loan:

- Gather Your Documents: Lenders will require documentation such as proof of income (pay stubs, tax returns), proof of residency (utility bills), driver’s license, and potentially bank statements. Having these ready will expedite the approval process.

- Compare Loan Offers: Review all your pre-approved offers and any offers from the dealership. Look beyond just the interest rate; compare terms, fees, and any specific conditions.

- Finalize Your Vehicle Choice: Once you have your financing in order, you can confidently choose the car that fits your budget and needs.

- Read the Final Loan Agreement: Before signing, carefully read the final loan agreement. Ensure all terms, rates, and figures match what you discussed and agreed upon. Don’t hesitate to ask questions if anything is unclear.

- Complete the Purchase: Once the loan is signed, you’re ready to complete the purchase, register your vehicle with the NC DMV, and drive off in your new car!

The Future of Car Financing: Trends to Watch

The world of car financing is continually evolving. We’re seeing a growing trend towards fully online loan applications and approvals, making the process faster and more convenient. Digital lenders are becoming increasingly competitive, pushing traditional institutions to innovate. As electric vehicles (EVs) become more prevalent, expect to see specialized financing options and incentives tailored to these eco-friendly choices. Staying informed about these trends can help you make even smarter financing decisions in the years to come.

Conclusion: Empower Yourself with the Car Loan Calculator NC

The journey to owning your dream car in North Carolina doesn’t have to be fraught with financial anxiety. By embracing the power of the Car Loan Calculator NC, you transform from a passive buyer into an empowered, informed consumer. It’s more than just a tool; it’s your guide to understanding the true cost of borrowing, setting a realistic budget, and confidently negotiating the best possible deal.

Take the time to experiment with different scenarios, understand the key components, and apply the expert tips we’ve shared. Arm yourself with knowledge about North Carolina’s specific taxes and fees, and steer clear of common financing mistakes. With the Car Loan Calculator NC as your trusted companion, you’ll not only secure a car loan that fits your financial well-being but also enjoy the open roads of North Carolina with true peace of mind. Start calculating, start planning, and drive away with confidence!