Unlock Your Electric Future: The Definitive Guide to E Car Loans and EV Financing

Unlock Your Electric Future: The Definitive Guide to E Car Loans and EV Financing Carloan.Guidemechanic.com

The hum of an electric vehicle (EV) is becoming an increasingly common sound on our roads, signaling a quiet revolution in personal transportation. As the world shifts towards sustainability, owning an EV is no longer a distant dream but a tangible reality for many. Yet, the initial investment can seem daunting. This is where the E Car Loan steps in, acting as your crucial bridge to embracing a greener, more efficient future.

This comprehensive guide is designed to demystify EV financing, offering you an in-depth look at everything you need to know about securing an E Car Loan. From understanding the unique benefits to navigating the application process and uncovering hidden costs, we’ll equip you with the knowledge to make informed decisions. Our ultimate goal is to help you drive away in your dream electric vehicle, knowing you’ve secured the best possible financing.

Unlock Your Electric Future: The Definitive Guide to E Car Loans and EV Financing

1. What Exactly is an E Car Loan? Your Gateway to Electric Mobility

An E Car Loan, often referred to as an Electric Vehicle Loan or EV Financing, is a specialized type of automotive loan specifically designed for the purchase of electric vehicles. While it functions similarly to a traditional car loan, its unique nature lies in its targeted application and often more favorable terms. Lenders, recognizing the environmental and technological shift, are increasingly offering bespoke products to support EV adoption.

Unlike a standard car loan that might be used for any internal combustion engine (ICE) vehicle, an E Car Loan is exclusively for fully electric cars, plug-in hybrids, or sometimes even hydrogen fuel cell vehicles. This focus allows financial institutions to tailor their offerings, often aligning with government incentives and environmental initiatives. It’s more than just a loan; it’s a financial product that supports a sustainable lifestyle choice.

Based on my experience in the automotive financing sector, the rise of the E Car Loan reflects a broader trend. Lenders are adapting to market demands and governmental pushes towards greener transport. They understand that by offering attractive EV financing options, they not only cater to a growing consumer base but also contribute to corporate social responsibility goals. This specialized lending demonstrates a clear commitment to the future of transportation.

2. The Driving Benefits of Opting for an E Car Loan

Choosing an E Car Loan over a conventional auto loan can unlock a host of advantages. These benefits often translate into significant savings and a smoother path to EV ownership. Understanding these perks is key to maximizing your investment in an electric vehicle.

Lower Interest Rates: A Green Advantage

One of the most compelling benefits of an E Car Loan is the potential for lower interest rates. Many financial institutions offer reduced rates for electric vehicles as a way to promote sustainable practices and align with environmental goals. These ‘green’ loans are often subsidized or supported by government programs that incentivize eco-friendly purchases.

Lenders view EV loans as a strategic investment, often backed by the long-term cost savings associated with electric vehicles, such as lower fuel and maintenance expenses. This can make borrowers for EVs seem like a more stable investment, leading to more attractive interest rate offerings. Always compare these specialized rates against standard auto loan rates to see the tangible difference.

Specialized Terms and Conditions: Tailored for EVs

Beyond interest rates, E Car Loans often come with more flexible and specialized terms and conditions. This can include longer repayment periods, which can reduce monthly payments, or unique payment structures that align with the anticipated savings from owning an EV. Some loans might even integrate potential government rebates directly into the financing structure.

These specialized terms are designed to make EV ownership more accessible and affordable, especially given the typically higher upfront cost of electric vehicles compared to their gasoline counterparts. Lenders understand the unique value proposition of EVs and structure their loans accordingly. This tailored approach provides borrowers with greater financial flexibility and peace of mind.

Access to Government & Manufacturer Incentives: Double Your Savings

An E Car Loan can often work in tandem with various government incentives and manufacturer rebates, magnifying your overall savings. Many countries and regions offer tax credits, grants, or subsidies for purchasing new electric vehicles. These incentives are designed to make EVs more competitive and encourage wider adoption.

When you secure an EV loan, you can often factor in these anticipated incentives, potentially reducing the total amount you need to borrow or providing a lump sum back after purchase. Furthermore, many EV manufacturers offer their own financing deals or cash-back programs specifically for their electric models, which can be combined with favorable loan terms. Pro tips from us: Always research all available federal, state, and local incentives before you finalize your purchase and loan, as they can significantly impact your total cost.

Environmental Impact: Beyond Financial Savings

While financial benefits are a strong draw, an E Car Loan also supports a larger purpose: reducing your carbon footprint. By financing an electric vehicle, you are actively contributing to cleaner air, reduced reliance on fossil fuels, and a more sustainable future. This environmental benefit is a significant factor for many buyers.

Choosing an EV means zero tailpipe emissions, which directly improves air quality in urban areas and helps combat climate change. Many consumers find immense value in aligning their personal choices with their environmental values, making the E Car Loan a tool for responsible living. It’s an investment not just in a car, but in a healthier planet.

3. Navigating the Eligibility Criteria for Your EV Financing Journey

Just like any other loan, securing an E Car Loan requires meeting specific eligibility criteria. Understanding these requirements beforehand can streamline your application process and increase your chances of approval. Lenders assess several key factors to determine your creditworthiness and ability to repay the loan.

Credit Score: Your Financial Report Card

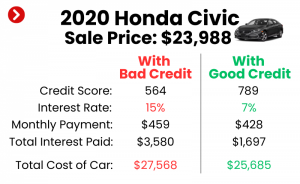

Your credit score is arguably the most critical factor in securing an E Car Loan. It’s a three-digit number that reflects your creditworthiness based on your payment history, outstanding debts, and length of credit history. A higher credit score (typically above 700) indicates lower risk to lenders and usually qualifies you for the best interest rates.

Lenders use your credit score to gauge your reliability as a borrower. A strong credit history demonstrates a consistent ability to manage debt responsibly. If your score is lower, you might still qualify for an EV loan, but potentially with a higher interest rate or stricter terms. Common mistakes to avoid are not checking your credit score before applying or making late payments on existing accounts, which can significantly drop your score.

Income Stability: Proof of Repayment Capacity

Lenders need assurance that you have a stable and sufficient income to comfortably make your monthly loan payments. This typically involves providing proof of employment, such as recent pay stubs, tax returns, or bank statements. They will also look at your debt-to-income (DTI) ratio, which compares your total monthly debt payments to your gross monthly income.

A low DTI ratio (ideally below 36%) suggests you have ample income left after covering your existing debts, making you a more attractive borrower. Demonstrating consistent employment and a healthy income level is crucial. Self-employed individuals may need to provide more extensive financial documentation, like multiple years of tax returns, to prove income stability.

Down Payment: Reducing Your Loan Burden

While not always mandatory, making a down payment on your electric vehicle can significantly improve your chances of loan approval and secure more favorable terms. A substantial down payment reduces the total amount you need to borrow, thereby lowering your monthly payments and the overall interest paid over the life of the loan.

From a lender’s perspective, a down payment demonstrates your commitment to the purchase and reduces their risk. It also helps prevent you from being "upside down" on your loan, where you owe more than the car is worth, especially in the early years of ownership. Pro tips from us: Aim for at least a 10-20% down payment if possible, as it can unlock better interest rates and provide greater financial flexibility.

Vehicle Type and Age: Must Be an Eligible EV

Naturally, to qualify for an E Car Loan, the vehicle you intend to purchase must be an eligible electric vehicle. This typically includes new battery electric vehicles (BEVs) and plug-in hybrid electric vehicles (PHEVs). Some lenders may also extend these specialized loans to used EVs, though terms might vary.

It’s essential to confirm with your chosen lender whether the specific make, model, and year of the EV you’re interested in qualifies for their specialized financing program. Lenders often have lists of approved vehicles, especially if their programs are tied to specific green initiatives. Ensure your dream EV fits the bill before you get too far into the application process.

4. The Application Process: Step-by-Step Towards Your Electric Dream

Applying for an E Car Loan is a structured process that, when approached methodically, can be smooth and efficient. Knowing what to expect at each stage can alleviate stress and ensure you’re well-prepared. This step-by-step guide will walk you through the journey from research to driving your new EV.

Step 1: Research and Compare Lenders

Before you even look at cars, begin by researching various lenders that offer Electric Vehicle Loans. This includes traditional banks, credit unions, online lenders specializing in auto loans, and even specific EV manufacturer financing programs. Each lender will have different rates, terms, and eligibility requirements.

Don’t settle for the first offer you receive. Based on my experience, shopping around and getting quotes from at least three to four different institutions can save you a substantial amount over the life of the loan. Compare not just interest rates, but also fees, loan terms, and any special features or incentives tied to their EV financing.

Step 2: Gather Your Essential Documents

Once you’ve identified potential lenders, start compiling all the necessary documentation. This preparation will significantly speed up your application. Typically, you’ll need:

- Proof of Identity: Government-issued ID (driver’s license, passport).

- Proof of Income: Recent pay stubs (2-3 months), W-2 forms, tax returns (for self-employed individuals).

- Proof of Residency: Utility bills, lease agreement, mortgage statements.

- Credit History Information: While lenders pull this, having a recent copy of your credit report for your own review is wise.

- Vehicle Information: Once you’ve chosen a specific EV, you’ll need details like VIN, make, model, and price.

Having these documents organized and readily accessible will make the application process much smoother and prevent delays.

Step 3: Get Pre-Approved for Your EV Loan

One of the most valuable steps in the process is getting pre-approved for an EV Financing loan. Pre-approval means a lender has provisionally agreed to lend you a certain amount of money, at a specific interest rate, before you’ve even picked out your exact vehicle. This process usually involves a "soft" credit check, which doesn’t negatively impact your credit score.

From my observations, pre-approval offers several key advantages. It gives you a clear budget, allowing you to shop for your electric vehicle with confidence. It also gives you leverage at the dealership, as you’re already a qualified buyer, potentially leading to better negotiation power on the car’s price. It transforms you into a cash buyer in the eyes of the dealer, which is a powerful position.

Step 4: Choose Your Electric Vehicle

With your pre-approval in hand, you can now confidently select your dream electric vehicle. Whether it’s a sleek sedan, a family-friendly SUV, or a compact urban EV, ensure it aligns with your budget and lifestyle needs. Remember to factor in not just the purchase price, but also potential charging infrastructure costs and insurance.

Make sure the chosen EV qualifies for the specific E Car Loan you’ve been pre-approved for. Double-check any specific requirements from the lender regarding vehicle make, model, or new vs. used status. This is the exciting part where your sustainable future starts to take shape!

Step 5: Finalize Your Loan and Drive Away

Once you’ve settled on your EV, the final step is to formalize the loan. This involves reviewing and signing the loan agreement, which outlines all the terms and conditions, including the interest rate, repayment schedule, and any associated fees. Read this document carefully and ask questions about anything you don’t understand.

After the paperwork is complete and the funds are disbursed to the dealership, you’re ready to pick up your new electric vehicle. Congratulations! You’ve successfully navigated the E Car Loan process and are now part of the growing community of EV owners.

5. Understanding EV Loan Interest Rates and Fees

While securing an E Car Loan is a significant step, a true understanding of its financial implications goes beyond just the monthly payment. Interest rates and associated fees play a crucial role in the total cost of your loan. Being informed about these elements empowers you to make smarter financial decisions.

Factors Affecting Your EV Loan Interest Rate

Several variables influence the interest rate you’ll be offered for your EV Financing:

- Credit Score: As mentioned, a higher credit score (excellent credit) will generally secure you the lowest rates, as you’re perceived as a lower risk.

- Loan Term: Shorter loan terms (e.g., 36 or 48 months) typically come with lower interest rates compared to longer terms (e.g., 72 or 84 months), though shorter terms mean higher monthly payments.

- Lender Type: Banks, credit unions, and online lenders each have different rate structures. Credit unions, for example, often offer highly competitive rates to their members.

- Market Conditions: Broader economic factors, such as the prime rate set by central banks, can influence prevailing interest rates across the board.

- Down Payment: A larger down payment reduces the loan-to-value (LTV) ratio, which can result in a more favorable interest rate.

Understanding these factors allows you to take steps to improve your standing before applying, potentially leading to significant savings.

Fixed vs. Variable Interest Rates: Which is Right for You?

When choosing an E Car Loan, you’ll typically encounter two main types of interest rates:

- Fixed Interest Rate: This means your interest rate remains the same throughout the entire loan term. Your monthly payment for the principal and interest will be consistent, making budgeting straightforward and predictable. The advantage is stability, protecting you from potential rate increases. The downside is you won’t benefit if market rates drop.

- Variable Interest Rate: With a variable rate, your interest rate can fluctuate over the loan term, usually tied to a benchmark rate like the prime rate. Your monthly payments could increase or decrease accordingly. The advantage is you might benefit from falling rates. However, the risk is that rising rates could make your loan more expensive.

Pro tips from us: Most auto loans, including Electric Vehicle Loans, are offered with fixed rates, which generally provide more stability and peace of mind for borrowers. Variable rates are less common for car loans but worth understanding if offered.

Common Fees Associated with EV Loans

Beyond the interest rate, be aware of potential fees that can add to the total cost of your EV Financing:

- Origination Fees: A fee charged by the lender for processing the loan. Not all lenders charge this, but it’s important to ask.

- Documentation Fees (Doc Fees): Charged by the dealership for preparing the sales contract and other paperwork. These can sometimes be negotiable.

- Late Payment Fees: Penalties incurred if you miss a payment deadline. Always aim to pay on time to avoid these.

- Prepayment Penalties: Some lenders might charge a fee if you pay off your loan early. This is less common with auto loans but always check your loan agreement.

- Title and Registration Fees: Standard government fees for transferring ownership and registering the vehicle in your name.

Always ask for a complete breakdown of all fees before signing any loan agreement. Pro tips from us: Always compare the Annual Percentage Rate (APR), not just the interest rate. APR includes the interest rate plus certain fees, giving you a more accurate picture of the total cost of borrowing.

6. Beyond the Loan: The True Cost of EV Ownership (and How to Manage It)

Securing an E Car Loan is just the first step. Understanding the full financial picture of owning an electric vehicle is crucial for long-term satisfaction and budgeting. While EVs boast lower running costs, there are still expenses to consider beyond your monthly loan payment.

Charging Costs: Fueling Your EV

The "fuel" for your EV is electricity, and its cost can vary significantly.

- Home Charging: This is typically the most cost-effective method. The cost depends on your electricity rates, which vary by region and time of day (peak vs. off-peak). Installing a Level 2 home charger can be an upfront expense, but it offers convenience and faster charging.

- Public Charging: Costs for public charging stations (Level 2 or DC Fast Chargers) are generally higher than home charging. Rates can be per kWh, per minute, or a flat fee. While convenient for longer trips, relying solely on public charging can quickly add up.

Many EV owners benefit from smart charging features that optimize charging during off-peak hours when electricity rates are lowest. Calculating your average daily or weekly mileage and researching local electricity rates will give you a good estimate of your charging costs.

Maintenance: Simpler, But Still Necessary

One of the significant advantages of EVs is their simplified mechanical design, leading to generally lower maintenance costs compared to ICE vehicles. There’s no oil to change, no spark plugs to replace, and fewer moving parts overall.

- Fewer Wear Parts: EVs typically have regenerative braking, which reduces wear on brake pads.

- Specific EV Components: While general maintenance is lower, EVs do have specific components like the battery pack, electric motors, and power electronics. These generally require less frequent servicing but can be expensive if they need replacement (though they often come with long warranties).

- Tires: Due to instant torque and heavier battery packs, EV tires might wear out faster than ICE vehicle tires.

For a deeper dive into EV maintenance, check out our guide on . Understanding these aspects helps you budget for the long haul.

Insurance: Evolving Costs

Historically, EV insurance premiums could be higher due to the higher purchase price of the vehicle and the specialized parts required for repair. However, this trend is evolving.

- Lower Risk Factors: Some insurers are starting to offer lower rates for EVs due to advanced safety features, lower accident rates, and the environmental benefits.

- Specific Models: Insurance costs will vary greatly depending on the specific EV model, your driving record, location, and coverage choices.

- Battery Replacement: While rare, the cost of battery replacement is a factor insurers consider.

It’s crucial to get multiple insurance quotes for the specific EV you plan to purchase before finalizing your decision. You might be pleasantly surprised by competitive rates.

Battery Degradation and Warranty: Long-Term Considerations

EV batteries naturally degrade over time, meaning their capacity to hold a charge slightly diminishes. However, modern EV batteries are designed to last for many years and miles.

- Warranties: Most EV manufacturers offer extensive warranties on their battery packs, typically 8 years or 100,000 miles (sometimes more), covering significant degradation or failure.

- Longevity: Many EVs are showing excellent battery longevity, with minimal real-world degradation over typical ownership periods.

Understanding these long-term aspects provides peace of mind and helps you appreciate the durability of modern EV technology, further justifying your E Car Loan investment.

7. Smart Strategies for Securing the Best E Car Loan Deal

Navigating the world of EV Financing doesn’t have to be overwhelming. With a few smart strategies, you can significantly improve your chances of securing the most favorable terms for your E Car Loan. These proactive steps can translate into substantial savings over the life of your loan.

Improve Your Credit Score Before Applying

Your credit score is paramount. Before you even think about applying for an Electric Vehicle Loan, take the time to review your credit report and actively work on improving your score if needed.

- Check for Errors: Obtain free copies of your credit report from all three major bureaus (Equifax, Experian, TransUnion) and dispute any inaccuracies.

- Pay Bills on Time: Payment history is the biggest factor in your score. Set up reminders or automatic payments.

- Reduce Debt: Lowering your credit card balances can improve your credit utilization ratio, which positively impacts your score.

- Avoid New Credit: Don’t open new credit accounts right before applying for a car loan, as this can temporarily lower your score.

A few months of focused effort can significantly boost your credit score, leading to lower interest rates on your E Car Loan.

Save for a Substantial Down Payment

As discussed, a larger down payment is one of the most effective ways to secure a better loan deal. It reduces the amount you need to borrow, lowers your monthly payments, and often qualifies you for a better interest rate.

- Demonstrates Commitment: Lenders see a significant down payment as a sign of your financial responsibility and commitment to the purchase.

- Reduces Risk: It lowers the lender’s risk, making them more willing to offer competitive terms.

- Avoid Negative Equity: A good down payment helps you avoid owing more than the car is worth, especially in the early years of ownership when depreciation is highest.

Even an extra 5% down can make a noticeable difference in your loan terms and overall interest paid.

Shop Around and Get Multiple Loan Quotes

Common mistakes to avoid are accepting the first loan offer you receive or only getting financing from the dealership. This is perhaps the most crucial piece of advice for any loan, including an E Car Loan.

- Compare Offers: Apply to several different lenders—banks, credit unions, and online lenders—to compare their interest rates, fees, and terms.

- Pre-Approval Power: Getting pre-approved by multiple lenders within a short window (typically 14-45 days, depending on the credit scoring model) will usually only count as one hard inquiry on your credit report, allowing you to shop without fear of damaging your score.

- Dealership Leverage: Having an outside loan offer in hand gives you leverage when negotiating with the dealership’s finance department. They may be willing to beat your outside offer to keep the financing in-house.

This comparison shopping can literally save you thousands of dollars over the life of your EV Financing.

Negotiate the Terms

Don’t be afraid to negotiate, not just the price of the EV, but also the terms of your E Car Loan.

- Interest Rate: If you have good credit and multiple offers, ask if your preferred lender can match or beat a competitor’s rate.

- Fees: Some fees might be negotiable, especially documentation fees from the dealership.

- Loan Term: While shorter terms mean higher monthly payments, they result in less interest paid overall. Consider what monthly payment you can comfortably afford while aiming for the shortest term possible.

Every percentage point off the interest rate or reduction in fees adds up to significant savings.

Consider a Shorter Loan Term (If Affordable)

While longer loan terms offer lower monthly payments, they come at the cost of paying significantly more interest over time. If your budget allows, opting for a shorter loan term for your E Car Loan can be a very smart financial move.

- Less Interest Paid: A 48-month loan will accrue much less interest than a 72-month loan, even if the interest rate is the same.

- Faster Equity Build-Up: You’ll pay off the car faster and build equity more quickly, potentially making your next car purchase easier.

- Higher Monthly Payments: The trade-off is higher monthly payments, so ensure you can comfortably afford them without straining your budget.

Balance your desire for lower overall cost with your ability to manage monthly expenses.

8. The Future of E Car Loans and Sustainable Transportation

The landscape of automotive financing is rapidly evolving, with E Car Loans at the forefront of this transformation. As electric vehicles become more mainstream and technology continues to advance, we can expect even more innovative and accessible financing options to emerge. This shift is not just about personal finance; it’s a critical component of building a more sustainable future.

Growing Market and Innovation in Financing

The global push for decarbonization and the increasing adoption of EVs are creating a robust market for specialized EV Financing. We’re seeing more financial institutions recognizing the long-term viability and growth potential of this segment. This competition among lenders is likely to lead to even more competitive rates and flexible loan products for consumers.

Expect to see new financing models that might integrate battery leasing options, vehicle-to-grid (V2G) capabilities, or even subscription services for EVs. These innovations aim to make electric mobility accessible to a wider demographic, addressing various financial needs and preferences. The future of E Car Loans is dynamic and consumer-centric.

Increasing Availability of Green Financial Products

Beyond direct E Car Loans, the financial sector is developing a broader range of "green" financial products. This includes green bonds, sustainable investment funds, and personal loans with environmental criteria. The trend indicates a wider commitment from financial institutions to support eco-friendly initiatives, with EV financing being a prime example.

This proliferation of green financial products means that supporting sustainable choices, like buying an EV, will become increasingly integrated into mainstream banking. It’s a positive feedback loop: as more people demand sustainable options, more financial products will be developed to meet that demand, making green choices even easier.

Long-Term Impact on Environment and Personal Finance

The widespread adoption of Electric Vehicle Loans plays a pivotal role in accelerating the transition to sustainable transportation. By making EVs more affordable and accessible, these loans directly contribute to reducing greenhouse gas emissions, improving air quality, and lessening our dependence on fossil fuels.

From a personal finance perspective, the long-term benefits extend beyond the initial loan. Lower running costs (electricity vs. gasoline), reduced maintenance, and potential government incentives contribute to significant savings over the vehicle’s lifespan. This makes an EV not just an environmentally responsible choice, but often a financially savvy one. For the latest updates on global EV adoption trends and policy, refer to reports from the International Energy Agency (IEA) – Placeholder for external link. The collective impact of individual choices, facilitated by accessible financing, will be transformative for both our wallets and our planet.

Conclusion: Powering Your Journey Towards a Greener Tomorrow

The decision to purchase an electric vehicle is a significant step towards a sustainable and technologically advanced future. With the right E Car Loan, this transition can be smooth, affordable, and incredibly rewarding. We’ve explored the unique advantages of EV financing, from lower interest rates and specialized terms to the invaluable support it provides in accessing government incentives.

Understanding the eligibility criteria, meticulously navigating the application process, and being savvy about interest rates and fees are all crucial components of securing the best deal. Moreover, looking beyond the loan to grasp the true cost of EV ownership – including charging, maintenance, and insurance – empowers you to budget effectively and enjoy your electric journey without financial surprises.

By leveraging smart strategies like improving your credit score, making a solid down payment, and diligently shopping around for lenders, you can unlock the most favorable EV Financing terms available. The future of transportation is undoubtedly electric, and with an E Car Loan, you’re not just buying a car; you’re investing in a cleaner environment, reduced running costs, and a more sustainable lifestyle. Embrace the electric revolution – your journey starts here.