Unlock Your Financial Future: The Ultimate Guide to the Interest Paid Car Loan Calculator

Unlock Your Financial Future: The Ultimate Guide to the Interest Paid Car Loan Calculator Carloan.Guidemechanic.com

Buying a car is an exciting milestone, often one of the largest purchases many people make after a home. While the thrill of a new vehicle is undeniable, the financial realities – particularly the car loan – can quickly become overwhelming. Understanding the true cost of your car loan, especially the total interest you’ll pay, is crucial for smart financial planning. This is precisely where an Interest Paid Car Loan Calculator becomes your most powerful tool.

Far too many car buyers focus solely on the monthly payment, overlooking the significant amount of interest that accrues over the loan’s lifetime. This comprehensive guide will demystify car loan interest, show you how to leverage an advanced calculator, and empower you to make informed decisions that save you potentially thousands of dollars. Let’s dive deep into becoming a financially savvy car owner.

Unlock Your Financial Future: The Ultimate Guide to the Interest Paid Car Loan Calculator

What is an Interest Paid Car Loan Calculator, and Why is it Indispensable?

At its core, an Interest Paid Car Loan Calculator is a sophisticated online tool designed to help you estimate not only your monthly car loan payments but, more importantly, the total amount of interest you will pay over the entire duration of your loan. It takes several key pieces of information – the principal loan amount, the interest rate (APR), and the loan term – and crunches the numbers to give you a clear financial picture.

Based on my experience working with countless individuals navigating car financing, this calculator is more than just a simple payment estimator; it’s a financial crystal ball. It transforms complex amortization schedules into easy-to-understand figures, allowing you to see the long-term impact of your borrowing decisions. Without it, you’re essentially signing up for a major financial commitment blindfolded.

The true value lies in its ability to reveal the hidden costs beyond the sticker price. Many people are shocked to discover how much additional money they’re paying purely in interest, especially on longer loan terms. This transparency empowers you to negotiate better terms, make larger down payments, or choose a shorter loan duration, all with the goal of minimizing your overall expenditure.

How Car Loan Interest Works: The Fundamental Mechanics

Before you can effectively use an Interest Paid Car Loan Calculator, it’s essential to grasp the basic principles of how car loan interest functions. Understanding these fundamentals will give you context for the numbers the calculator presents and help you interpret the results more intelligently.

When you take out a car loan, you’re borrowing a sum of money (the principal) from a lender. In return for lending you that money, the lender charges you an additional fee, which is the interest. This interest is typically expressed as an Annual Percentage Rate (APR), which includes not just the interest rate but also any additional fees associated with the loan, providing a more accurate representation of the total cost of borrowing.

Every month, your car loan payment is divided into two main components: a portion that goes towards reducing your principal balance and a portion that covers the interest accrued since your last payment. Early in the loan term, a larger percentage of your payment goes towards interest, while later on, more of it goes towards the principal. This process is known as amortization, and it’s a critical concept the calculator helps visualize.

Decoding the Key Components of the Calculator

To get the most accurate and insightful results from an Interest Paid Car Loan Calculator, you need to understand the inputs it requires and what each one signifies for your finances. Each variable plays a significant role in determining your monthly payment and, crucially, your total interest paid.

Let’s break down these essential components:

1. Loan Amount (Principal)

This is the actual amount of money you need to borrow from the lender after considering your down payment, trade-in value, and any rebates. It’s the starting point for all calculations. A higher loan amount will naturally lead to higher monthly payments and, all else being equal, a greater total interest paid over the life of the loan.

The calculator uses this figure as the base from which to calculate interest charges. Remember, the less you borrow, the less interest you will accrue. This is why a substantial down payment can be a game-changer.

2. Interest Rate (APR)

The interest rate, often expressed as an Annual Percentage Rate (APR), is perhaps the most critical factor influencing your total interest paid. This percentage represents the cost of borrowing money for one year. A lower APR directly translates to less money paid in interest over the loan term.

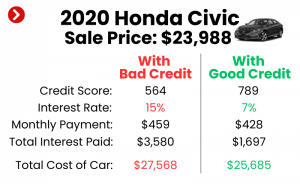

Your credit score is the primary determinant of the APR you’ll be offered. Lenders view borrowers with excellent credit as lower risk, thus offering them more favorable, lower interest rates. Conversely, a poor credit score will typically result in a much higher APR, significantly increasing your overall borrowing cost. for more in-depth information.

3. Loan Term (Months/Years)

The loan term refers to the duration over which you agree to repay the loan, usually expressed in months (e.g., 36, 48, 60, 72, or even 84 months). This variable has a profound impact on both your monthly payment and the total interest you’ll pay.

A longer loan term will result in lower monthly payments, making the car seem more affordable in the short term. However, stretching out your payments over a longer period means the lender charges you interest for more months, inevitably leading to a much higher total interest paid. Conversely, a shorter loan term will have higher monthly payments but dramatically reduce the total interest you pay over the loan’s life.

4. Down Payment

While not always a direct input into every basic calculator, the down payment is an extremely important factor that affects your principal loan amount. This is the initial sum of money you pay upfront towards the car’s purchase price.

A larger down payment reduces the amount you need to borrow, thereby lowering your principal. This, in turn, directly decreases both your monthly payments and the total interest you’ll pay over the loan term. It’s one of the most effective strategies for saving money on car financing.

5. Trade-in Value

Similar to a down payment, the value of a vehicle you trade in reduces the overall amount you need to finance. If you have an existing car that you sell to the dealership as part of the new car purchase, its value is deducted from the new car’s price.

This effectively functions like a down payment, lowering your principal loan amount. Utilizing a trade-in can significantly impact your total interest paid, making it a savvy financial move if you have an older vehicle to exchange.

Step-by-Step Guide: Using an Interest Paid Car Loan Calculator Effectively

Using an Interest Paid Car Loan Calculator is straightforward, but knowing how to interpret its results is where the real power lies. Let’s walk through a typical scenario.

Scenario: You’re looking at a car with a purchase price of $30,000. You plan to make a $5,000 down payment.

-

Determine Your Loan Amount: Subtract your down payment from the car’s price.

- $30,000 (Car Price) – $5,000 (Down Payment) = $25,000 (Loan Amount).

- Enter "$25,000" into the "Loan Amount" field of the calculator.

-

Input Your Interest Rate (APR): This is where shopping around for the best rate is crucial. Let’s assume you’ve been pre-approved for an APR of 6.5%.

- Enter "6.5%" into the "Interest Rate" field.

-

Choose Your Loan Term: Consider different terms to see their impact. Let’s start with a common 60-month (5-year) loan.

- Enter "60" into the "Loan Term (Months)" field.

-

Calculate! Click the "Calculate" or "Compute" button.

The calculator will instantly display:

- Your Estimated Monthly Payment: For our example, it might be around $489.

- Total Principal Paid: This will be your original loan amount, $25,000.

- Total Interest Paid: This is the game-changing number. For our example, it could be approximately $4,340.

- Total Cost of Loan: Principal + Interest = $29,340.

Pro tips from us: Always run calculations for several different interest rates and loan terms. This allows you to visually compare how each variable dramatically alters your total interest paid.

Beyond the Monthly Payment: What the Calculator Really Reveals

While knowing your monthly payment is essential for budgeting, the true magic of the Interest Paid Car Loan Calculator lies in its ability to highlight the often-overlooked total interest cost. This figure is where real savings can be found.

The Impact of Loan Term on Total Interest

This is perhaps the most eye-opening revelation for many car buyers. Consider our $25,000 loan at 6.5% APR:

- 60-month term: Monthly payment ~$489, Total Interest ~$4,340.

- 72-month term: Monthly payment ~$420, Total Interest ~$5,240. (You pay $900 more in interest for lower monthly payments.)

- 84-month term: Monthly payment ~$370, Total Interest ~$6,100. (You pay $1,760 more in interest!)

As you can see, extending the loan term to lower your monthly payment comes at a significant cost in the form of increased total interest. The calculator makes this trade-off undeniably clear, helping you decide if those lower monthly payments are truly worth the extra money spent over time.

The Power of a Better Interest Rate

Even a small difference in your APR can translate into substantial savings. Let’s revisit our $25,000 loan over 60 months:

- 6.5% APR: Monthly payment ~$489, Total Interest ~$4,340.

- 5.5% APR: Monthly payment ~$478, Total Interest ~$3,680. (You save $660 in interest!)

- 4.5% APR: Monthly payment ~$467, Total Interest ~$3,020. (You save $1,320 in interest!)

This demonstrates the critical importance of improving your credit score and shopping around for the best possible interest rate. The calculator visually reinforces the financial rewards of securing a lower APR.

The Advantage of a Larger Down Payment

Let’s assume you could make a $10,000 down payment instead of $5,000, reducing your loan amount to $20,000.

- $25,000 Loan (6.5% APR, 60 months): Monthly payment ~$489, Total Interest ~$4,340.

- $20,000 Loan (6.5% APR, 60 months): Monthly payment ~$391, Total Interest ~$3,470. (You save $870 in interest!)

Not only do you reduce your monthly payments, but you also significantly decrease the total interest paid because you’re borrowing less money from the outset. The calculator allows you to quickly model these scenarios and see the financial benefits.

Strategic Financial Planning with Your Car Loan Calculator

An Interest Paid Car Loan Calculator is not just for initial loan estimation; it’s a dynamic tool for strategic financial planning throughout your car ownership journey. Leveraging it effectively can save you money and give you greater control over your budget.

1. Budgeting Before Buying

Before you even step foot in a dealership, use the calculator to determine what loan amount and terms are truly affordable for your budget. Experiment with different car prices, down payment amounts, and interest rates to establish a realistic target. This proactive approach prevents you from falling in love with a car you can’t comfortably afford.

Based on my experience, many people get caught up in the emotion of buying a car and forget to do this crucial pre-planning. The calculator provides the cold, hard numbers you need to stay grounded.

2. Comparing Different Loan Offers

Once you receive loan offers from various lenders – your bank, credit union, and the dealership – plug each offer’s APR and term into the calculator. This side-by-side comparison will quickly reveal which offer is truly the most cost-effective in terms of total interest paid, not just the monthly payment. Don’t assume the lowest monthly payment is the best deal.

3. Considering Refinancing Options

If interest rates drop or your credit score improves significantly after you’ve purchased your car, you might consider refinancing. Use the calculator to compare your current loan’s remaining balance, rate, and term against a potential new refinance offer. It will clearly show you how much you could save in total interest and monthly payments by making the switch.

This is an often-overlooked strategy for existing car owners to reduce their financial burden. The calculator quantifies the benefits, making the decision clear.

4. The Power of Extra Payments

Want to pay off your car loan faster and save a substantial amount on interest? The calculator can help you visualize this. While most online calculators won’t directly calculate the impact of extra payments, you can simulate it by reducing your "loan term" or "loan amount" based on your payment strategy. For example, if you plan to pay an extra $50 per month, adjust the loan term down until the monthly payment matches your new target.

This shows you how many months you can shave off the loan and the corresponding interest savings. For a more precise calculation, look for calculators that offer an amortization schedule with extra payment options.

Common Mistakes to Avoid When Financing a Car

Even with a powerful tool like the Interest Paid Car Loan Calculator, it’s easy to fall into common traps that can cost you dearly. Being aware of these pitfalls is the first step toward avoiding them.

- Focusing Only on Monthly Payments: This is arguably the biggest mistake. A lower monthly payment often comes at the expense of a longer loan term and significantly more total interest paid. Always look at the "Total Cost of Loan" and "Total Interest Paid" figures.

- Ignoring the Total Cost of Interest: Many buyers don’t realize that the interest alone can add thousands of dollars to the car’s price. The calculator makes this cost transparent, forcing you to acknowledge it.

- Not Shopping Around for Rates: Accepting the first loan offer, especially from a dealership, can be a costly error. Lenders compete for your business. Use the calculator to compare rates from multiple sources (banks, credit unions, online lenders) before making a decision.

- Extending Loan Terms Too Long: While a 72 or 84-month loan might offer an appealingly low monthly payment, it dramatically increases the total interest you pay and prolongs the period you owe money on a depreciating asset. Pro tips from us: Aim for the shortest loan term you can comfortably afford.

- Rolling Negative Equity into a New Loan: If you owe more on your current car than it’s worth (negative equity), and you roll that balance into a new car loan, you’re starting your new purchase "underwater." This inflates your new loan amount, increases interest, and makes it harder to get ahead. The calculator will reflect this inflated principal and its financial consequences.

Pro Tips for Minimizing Your Car Loan Interest

Now that you’re an expert on the Interest Paid Car Loan Calculator and common pitfalls, let’s explore actionable strategies to significantly reduce the amount of interest you’ll pay over your car loan’s lifetime.

- Improve Your Credit Score: This is fundamental. A higher credit score signals lower risk to lenders, qualifying you for the lowest possible interest rates (APR). Before applying for a car loan, review your credit report for errors and take steps to improve your score, such as paying down other debts.

- Make a Larger Down Payment: As demonstrated by the calculator, a substantial down payment directly reduces the principal amount you need to borrow. Less principal means less interest charged over the loan term, leading to considerable savings. Aim for at least 20% if possible.

- Choose a Shorter Loan Term: While it means higher monthly payments, opting for a shorter loan term (e.g., 36 or 48 months instead of 60 or 72) drastically cuts down the total interest paid. The calculator will vividly illustrate these savings.

- Negotiate the Interest Rate: Don’t just accept the first rate you’re offered. If you’ve pre-qualified with multiple lenders, use those offers as leverage to negotiate a better rate with the dealership or your preferred lender. Every fraction of a percentage point counts.

- Consider Bi-Weekly Payments: Instead of making one monthly payment, paying half your monthly payment every two weeks results in 26 half-payments, or 13 full monthly payments per year. This extra payment annually can significantly reduce your principal faster, thereby cutting down on total interest and shortening your loan term.

- Pay More Than the Minimum: If your budget allows, making even a small extra payment each month directly reduces your principal. Since interest is calculated on your remaining principal balance, lowering that balance faster means less interest accrues over time. Be sure your lender applies extra payments directly to the principal.

- Avoid Add-Ons You Don’t Need: Dealerships often offer extended warranties, GAP insurance, and other add-ons that can be rolled into your loan. While some might be valuable, unnecessary ones inflate your loan amount, meaning you pay interest on them too. Evaluate each add-on carefully. For reliable information on consumer protection in auto loans, check out the Consumer Financial Protection Bureau’s resources:

Conclusion: Empowering Your Car Buying Journey

The journey to buying a new or used car doesn’t have to be a confusing maze of financial jargon and hidden costs. With an Interest Paid Car Loan Calculator at your fingertips, you gain an invaluable tool that brings transparency and control to the financing process. It moves you beyond simply looking at monthly payments and empowers you to understand the true cost of your loan – the total interest you’ll pay.

By actively using this calculator, experimenting with different scenarios, and applying the pro tips we’ve shared, you can make smarter, more informed decisions. You can negotiate from a position of strength, avoid common financial pitfalls, and ultimately save thousands of dollars over the lifetime of your car loan. Don’t just buy a car; buy it smart. Start exploring with an Interest Paid Car Loan Calculator today and take the driver’s seat of your financial future.