Unlock Your First Ride: Getting A Car Loan At 18 Without Credit – Your Comprehensive Guide

Unlock Your First Ride: Getting A Car Loan At 18 Without Credit – Your Comprehensive Guide Carloan.Guidemechanic.com

Getting your driver’s license at 18 is a monumental step towards independence. Suddenly, the open road beckons, and the thought of owning your own car becomes incredibly appealing. However, for many young adults, the dream hits a significant roadblock: how do you get a car loan at 18 without credit history?

This isn’t just a common question; it’s a critical financial challenge for countless aspiring car owners. Lenders typically rely on your credit score to assess your trustworthiness and ability to repay a loan. If you’re 18, chances are you haven’t had enough time or opportunities to build that essential credit profile. But don’t despair! While challenging, securing your first car loan at 18 is absolutely achievable with the right knowledge and strategic approach. This comprehensive guide will walk you through every step, offering expert advice and actionable strategies to help you drive off in your first car responsibly.

Unlock Your First Ride: Getting A Car Loan At 18 Without Credit – Your Comprehensive Guide

The Credit Hurdle: Why Lenders Hesitate with No Credit History

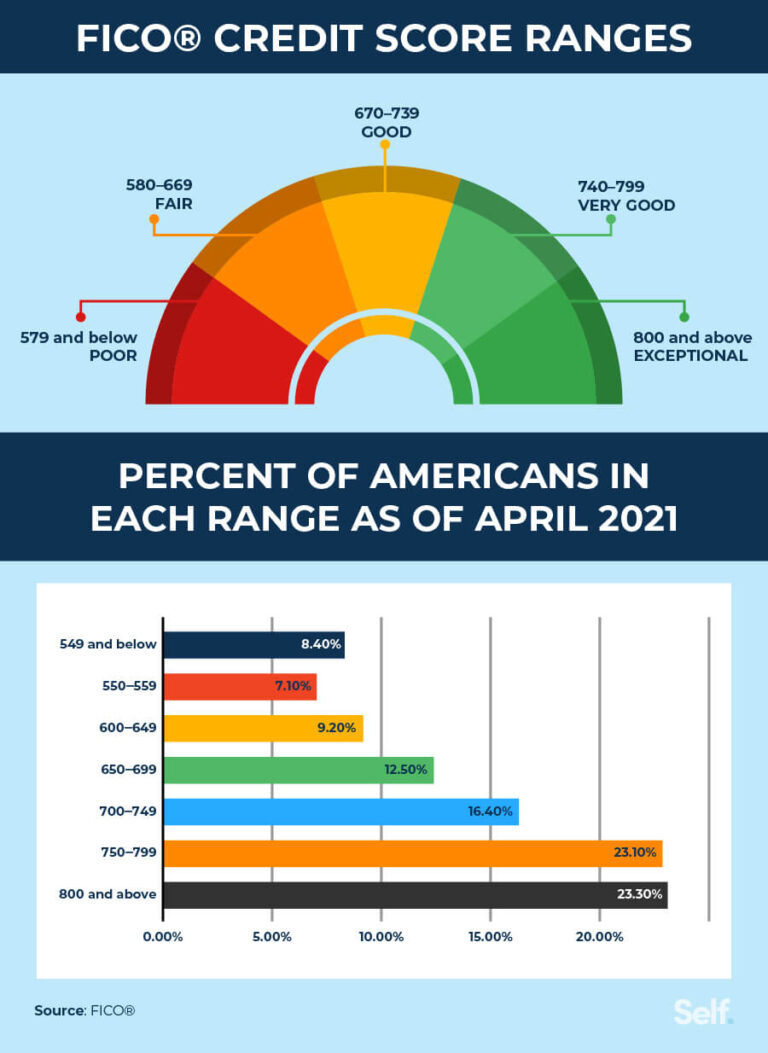

Before diving into solutions, it’s vital to understand the problem. What exactly is a credit score, and why is it so crucial for lenders? A credit score is a three-digit number that represents your creditworthiness, essentially a report card of your financial responsibility. It’s built on your history of borrowing and repaying money, from credit cards to mortgages.

When you apply for an auto loan, lenders look at this score to gauge the risk of lending to you. A high score (typically above 700) indicates you’re a low-risk borrower, while a low score or, in your case, no score at all, suggests an unknown risk. Since you haven’t had a chance to establish a borrowing history, lenders have no data to confirm you’ll repay your car loan. This lack of information makes them understandably cautious.

Based on my experience, one of the biggest misconceptions young adults have is that simply having a job is enough. While income is crucial, it’s only one piece of the puzzle. Lenders want to see a proven track record of managing debt responsibly. Without that, you’ll need to employ alternative strategies to demonstrate your reliability.

Building Your Foundation: The Pre-Application Checklist

Securing a car loan at 18 without credit requires thorough preparation. Don’t jump into applications blindly. Instead, focus on strengthening your financial position and understanding your options before approaching any lender. This groundwork will significantly improve your chances of approval.

1. Solidify Your Income and Employment Status

Lenders need assurance that you can afford your monthly payments. This makes a stable income and verifiable employment absolutely essential. If you’re currently working, ensure you have pay stubs, bank statements, or an employment letter to prove your earnings.

The longer you’ve been at your current job, the better. Lenders prefer stability. If you’re just starting a new job, it might be wise to wait a few months to establish a consistent work history.

2. Create a Realistic Budget

Before you even think about a specific car, understand what you can truly afford. This isn’t just about the monthly car payment; it includes insurance, fuel, maintenance, and potential repair costs. These "hidden" costs can quickly add up, making an otherwise affordable car a financial burden.

Pro tips from us: Use a budgeting app or a simple spreadsheet to track your income and expenses for a month or two. This will give you a clear picture of your disposable income and help you set a realistic price range for your car. Don’t forget to factor in insurance, which can be significantly higher for young drivers.

3. Save for a Substantial Down Payment

This is perhaps the single most impactful step you can take when trying to get a car loan at 18 without credit. A significant down payment reduces the amount you need to borrow, which in turn lowers the lender’s risk. It also demonstrates your financial discipline and commitment.

Aim for at least 10-20% of the car’s purchase price, but ideally, save even more. A larger down payment not only increases your approval odds but also leads to lower monthly payments and less interest paid over the life of the loan. This is a critical factor for young driver car finance.

4. Research Your Car Options and Total Cost of Ownership

Don’t fall in love with a car before you’ve done your homework. For your first car loan, practicality and affordability should be your guiding principles. Consider reliable, fuel-efficient used cars rather than brand-new models. New cars depreciate rapidly, and the loan amount will be higher.

Research not only the purchase price but also insurance costs, typical maintenance expenses, and fuel efficiency for specific models. A cheaper car to buy might be expensive to insure or maintain. Understanding the total cost of ownership will prevent future financial surprises.

Strategies for Getting Approved: Your Path to a Car Loan

With your foundation in place, it’s time to explore the specific strategies that can help an 18-year-old secure a car loan without an established credit history. Each approach has its nuances, and understanding them is key to making the right choice for your situation.

A. The Power of a Co-signer

One of the most effective ways for an 18-year-old to get a car loan without credit is to apply with a co-signer. A co-signer is someone, usually a parent or close family member, with good credit who agrees to take legal responsibility for the loan if you fail to make payments.

How it helps: The co-signer’s strong credit history and income essentially "back" your loan application. This significantly reduces the risk for the lender, making them much more likely to approve you. It also often allows you to qualify for better interest rates than you would on your own.

Responsibilities and Risks: While beneficial for you, being a co-signer carries significant responsibility. If you miss payments, it negatively impacts their credit score, and they are legally obligated to repay the loan in full. This arrangement requires a high degree of trust and open communication. Ensure both you and your co-signer fully understand the commitment involved before proceeding.

B. Making a Substantial Down Payment

As mentioned earlier, a large down payment is a game-changer. When you put down a significant amount of your own money, you’re essentially borrowing less from the lender. This immediately lowers their risk because they have less capital at stake.

Benefits beyond approval: Beyond increasing your chances of approval, a substantial down payment offers several financial advantages. It reduces your monthly payment, making the loan more affordable. It also means you’ll pay less interest over the loan’s term, saving you money in the long run.

Saving strategies: Start saving early and consistently. Consider a part-time job, cutting unnecessary expenses, or setting up an automatic savings transfer from your checking account. Every dollar saved for your down payment is a step closer to your car and a more favorable loan. This is a top car finance tip for young adults.

C. Exploring Dealership Financing and "Buy Here, Pay Here" Options

Many dealerships offer their own financing options, sometimes through captive finance companies (e.g., Toyota Financial Services) or through partnerships with various banks. Some dealerships also offer "Buy Here, Pay Here" (BHPH) financing.

Dealership Financing: These can sometimes be more flexible, especially if they have programs designed for first-time buyers or those with limited credit. However, the interest rates might be higher to compensate for the increased risk. Always compare their offers with those from other lenders.

Buy Here, Pay Here (BHPH): BHPH lots cater specifically to individuals with no credit or bad credit. They approve loans in-house, making the process quick and easy. However, common mistakes to avoid here are overlooking the extremely high interest rates and often less favorable loan terms. While they offer a solution, these loans can be very expensive and may not always report to credit bureaus, meaning they won’t help you build credit. Use BHPH as a last resort and proceed with extreme caution.

D. Building Credit First (Even a Little Bit)

While you’re aiming for a car loan without credit, taking a few months to build even a thin credit file can significantly improve your odds and secure better terms. This strategy involves taking small, manageable steps to establish a positive payment history.

Secured Credit Cards: These cards require a cash deposit, which becomes your credit limit. Using it responsibly and paying off the balance in full each month will start building your credit history.

Credit Builder Loans: Offered by some credit unions and small banks, these loans essentially put money into a savings account that you can’t access until you’ve made all your payments. Your on-time payments are reported to credit bureaus.

Becoming an Authorized User: If a trusted family member has excellent credit, they might add you as an authorized user on one of their credit cards. This can give your credit score a boost, provided they use the card responsibly and pay on time.

Even a few months of positive activity on these products can provide lenders with enough data to see you as a more reliable borrower for an auto loan for beginners.

E. Non-Traditional Lenders and Credit Unions

Don’t limit your search to big banks. Credit unions, in particular, are known for their community-focused approach and often offer more flexible lending criteria than large commercial banks. They might be more willing to work with young members who have limited credit history, especially if you have a relationship with them.

Local Banks and Community Lenders: Smaller local banks might also be more willing to consider individual circumstances rather than relying solely on a rigid credit score. Building a personal relationship with a loan officer can sometimes open doors.

Online Lenders: Some online lenders specialize in loans for those with less-than-perfect credit. However, always research their reputation and terms carefully, as interest rates can vary wildly.

F. Choosing the Right Car for Your First Loan

The type of car you choose plays a significant role in your loan approval chances and affordability. For your first car loan at 18, it’s wise to be pragmatic.

Used Over New: A reliable used car is almost always a better choice for a first-time borrower with no credit. They are less expensive, meaning you’ll need a smaller loan amount, reducing the risk for the lender.

Affordable and Practical: Focus on models known for their reliability, good fuel economy, and lower insurance costs. Avoid luxury brands or high-performance vehicles, which will come with higher price tags, steeper insurance premiums, and potentially more expensive maintenance. This helps keep your total monthly car expenses manageable.

The Application Process: What to Expect

Once you’ve chosen your strategy and prepared your finances, it’s time to apply for the loan. This process can feel daunting, but being prepared will make it smoother.

1. Gather Your Documents:

You’ll need several documents to verify your identity, income, and residence. This typically includes:

- Government-issued photo ID (driver’s license).

- Proof of income (recent pay stubs, employment letter, bank statements).

- Proof of residence (utility bill, lease agreement).

- Social Security number.

- References (sometimes required, especially with limited credit).

2. Fill Out the Application Accurately:

Be honest and thorough when completing the loan application. Any discrepancies or missing information can delay the process or lead to rejection.

3. Understand the Terms and Conditions:

This is crucial. Don’t sign anything until you fully understand the loan’s terms. Pay close attention to:

- Interest Rate (APR): This is the cost of borrowing money, expressed as a percentage. For those with no credit, expect a higher APR than someone with excellent credit.

- Loan Term: This is the length of time you have to repay the loan (e.g., 36, 48, 60 months). Longer terms mean lower monthly payments but more interest paid overall.

- Monthly Payment: Ensure this fits comfortably within your budget.

- Total Amount Repaid: Calculate the total cost of the car, including interest, over the life of the loan.

Pro tips from us: Ask questions if anything is unclear. Bring a trusted adult, even if they aren’t co-signing, to help review the documents. This is a major financial commitment, and you deserve to understand every aspect.

Common Pitfalls and How to Avoid Them

Even with the best intentions, young car buyers can fall into common traps. Being aware of these will help you navigate the process more successfully.

1. High-Interest Rates: Without a credit history, lenders view you as a higher risk, which translates to higher interest rates. Don’t just accept the first offer. Shop around and compare rates from multiple lenders. While you might not get the lowest rates, avoid anything excessively high (e.g., over 20% APR) unless it’s an absolute last resort.

2. Unaffordable Payments: It’s tempting to stretch the loan term to get a lower monthly payment, but this means paying significantly more in interest over time. Common mistakes to avoid include focusing solely on the monthly payment without considering the total cost. Ensure your payment, plus insurance and other car expenses, doesn’t strain your budget.

3. Ignoring Insurance Costs: For 18-year-olds, car insurance can be surprisingly expensive. Get several insurance quotes before finalizing your car purchase. A car that seems affordable on paper can become a financial burden once insurance is added. This is a critical aspect of getting a car loan at 18 without credit.

4. Impulse Buying: Don’t let excitement override common sense. Take your time, do your research, and avoid making a decision under pressure from a salesperson. Stick to your budget and chosen car type.

5. Not Reading the Fine Print: Loan agreements are legally binding documents. Always read the entire contract carefully, paying attention to any fees, penalties for late payments, and early payoff clauses. If you don’t understand something, ask for clarification.

Building Credit Responsibly After Getting the Loan

Congratulations, you’ve secured your first car loan! This is not just about owning a car; it’s a golden opportunity to build a strong credit history that will benefit you for years to come.

Make Payments On Time, Every Time: This is the most critical aspect of building good credit. Your payment history accounts for the largest portion of your credit score. Set up automatic payments or calendar reminders to ensure you never miss a due date. Even a single late payment can significantly damage your budding credit score.

Understand the Impact: A car loan is an installment loan, meaning you pay a fixed amount over a set period. Successfully managing this type of debt demonstrates your ability to handle credit responsibly. This will look very favorable to future lenders when you apply for things like apartments, mortgages, or other lines of credit.

Monitor Your Credit: After a few months, consider getting a free credit report from AnnualCreditReport.com to see how your loan payments are being reported. Regularly checking your credit allows you to spot any errors and track your progress.

Pro Tips for Young Car Buyers

To further enhance your chances and ensure a smooth process, consider these additional expert recommendations:

- Get Pre-Approved (If Possible): Even with no credit, some credit unions or online lenders might offer pre-approval with a co-signer or a substantial down payment. Pre-approval gives you a clear idea of what you can afford and gives you leverage at the dealership.

- Don’t Settle for the First Offer: Shop around for both the car and the loan. Visit multiple dealerships and apply to several lenders (within a short timeframe to minimize credit score impact if inquiries are made). This allows you to compare offers and negotiate for the best terms.

- Understand the Total Cost, Not Just Monthly Payments: As emphasized earlier, look beyond the monthly payment. Factor in the interest rate, loan term, down payment, and all associated fees to calculate the true total cost of the car over the life of the loan.

- Factor in Maintenance Costs: Older, used cars, while more affordable to purchase, might require more maintenance. Research the typical repair costs for the models you’re considering and budget for potential upkeep.

Conclusion: Your Road to Responsible Car Ownership Starts Now

Getting a car loan at 18 without credit is undoubtedly a challenge, but as we’ve explored, it’s far from impossible. By understanding the credit landscape, preparing your finances meticulously, and strategically leveraging options like co-signers, substantial down payments, and alternative lenders, you can absolutely secure your first auto loan.

This journey is about more than just getting a set of wheels; it’s about taking your first significant step into the world of financial responsibility. A car loan, managed wisely, can be a powerful tool for building a strong credit history, paving the way for future financial successes. Remember to be patient, do your homework, and always prioritize affordability and responsible borrowing. Your independence and your future financial health are worth the effort.

Start your journey today by assessing your financial situation, saving diligently for that down payment, and exploring the best options available to you. The open road awaits!

Internal Link Suggestion 1:

Internal Link Suggestion 2:

External Link Suggestion: For more in-depth information on managing your finances and understanding credit, visit the Consumer Financial Protection Bureau (CFPB) at https://www.consumerfinance.gov/.