Unlock Your Ride: The Ultimate Guide to Securing the Best Used Car Loan & Easy Approval

Unlock Your Ride: The Ultimate Guide to Securing the Best Used Car Loan & Easy Approval Carloan.Guidemechanic.com

Getting behind the wheel of a pre-owned vehicle offers incredible value, allowing you to access a wider range of models and features for a fraction of the cost of a new car. However, the journey to financing a used car can feel like navigating a complex maze. Many prospective buyers find themselves overwhelmed by the options, jargon, and the ever-present question: "What’s the best way to get a used car loan with a high chance of approval and excellent rates?"

As an expert blogger and professional SEO content writer, I understand the nuances of the automotive financing world. Based on my experience, securing the right used car loan isn’t about luck; it’s about strategic preparation and understanding the process. This comprehensive guide is designed to empower you with the knowledge and actionable steps needed to secure the best used car loan, ensuring a smooth ride from application to ownership. Let’s dive deep and unlock your dream ride!

Unlock Your Ride: The Ultimate Guide to Securing the Best Used Car Loan & Easy Approval

Understanding the Landscape of Used Car Loans

Before we delve into the ‘how-to,’ it’s crucial to grasp the unique aspects of used car loans. While the appeal of a pre-owned vehicle is undeniable – think depreciation savings and lower insurance costs – the financing can sometimes differ significantly from a new car loan.

Lenders often perceive used cars as having a higher risk profile. This is primarily due to factors like vehicle age, mileage, and potential for unforeseen mechanical issues, which can impact the car’s resale value and the lender’s collateral. Consequently, interest rates for used car loans might be slightly higher than for new car loans, and loan terms can sometimes be shorter.

However, this doesn’t mean securing an affordable used car loan is impossible. With the right approach, you can significantly mitigate these perceived risks in the eyes of lenders. Our goal is to position you as an ideal borrower, regardless of the vehicle’s age or mileage.

The Pre-Approval Power Play: Your First & Best Step

If there’s one piece of advice I can offer that will fundamentally change your used car buying experience, it’s this: get pre-approved for a used car loan before you even step foot in a dealership. This single action is a game-changer, transforming you from a hopeful buyer into a powerful, informed negotiator.

Pre-approval means a lender has reviewed your financial information – your credit history, income, and existing debts – and has conditionally agreed to lend you a specific amount of money at a particular interest rate and term. It’s a concrete offer, not just an estimate. Think of it as having cash in your pocket.

Why is pre-approval so crucial? Firstly, it clarifies your budget. You’ll know exactly how much you can afford, preventing you from falling in love with a car outside your financial reach. Secondly, and perhaps most importantly, it gives you immense negotiating power. When a dealer knows you already have financing, they are more likely to offer competitive pricing on the vehicle itself, rather than trying to inflate the price or profit heavily on the financing.

Common mistakes to avoid are letting the dealership be your first and only stop for financing. While convenient, this often leads to less favorable terms because they know you haven’t shopped around. Always secure your own financing first, then compare it to any offers the dealer might present.

To get pre-approved, you’ll typically apply through banks, credit unions, or online lenders. The process usually involves a "soft inquiry" on your credit, which doesn’t negatively impact your score. Once you receive an offer, you’ll have a clear understanding of your borrowing capacity and the rates available to you.

Sharpening Your Financial Profile for Loan Success

Lenders look at a holistic picture of your financial health when evaluating a loan application. By proactively strengthening key areas, you significantly increase your chances of securing the best rates and easiest approval for your used car loan.

1. Your Credit Score: The Ultimate Determinant

Your credit score is arguably the most critical factor in securing favorable used car financing. It’s a numerical representation of your creditworthiness, based on your payment history, credit utilization, length of credit history, new credit, and credit mix. A higher score signals less risk to lenders, translating into lower interest rates and better terms.

Understanding your credit score is the first step. You can obtain free copies of your credit report from the three major bureaus (Experian, Equifax, and TransUnion) annually via AnnualCreditReport.com. Review these reports for any errors and dispute them immediately. Even small inaccuracies can drag down your score.

To improve your score, focus on consistent, on-time payments for all your debts. Reduce your credit utilization by paying down credit card balances; keeping it below 30% is generally recommended. Avoid opening new credit accounts unnecessarily right before applying for a car loan, as this can temporarily lower your score.

2. Debt-to-Income (DTI) Ratio: Why It Matters

Your debt-to-income (DTI) ratio is another critical metric lenders scrutinize. It represents the percentage of your gross monthly income that goes towards paying your monthly debt obligations. A lower DTI ratio indicates that you have more disposable income available to comfortably manage a new car payment.

To calculate your DTI, sum up all your monthly debt payments (credit cards, student loans, mortgage/rent, etc.) and divide that by your gross monthly income. Lenders typically prefer a DTI ratio of 36% or less, though some may go higher depending on other factors.

Strategies to lower your DTI include paying off small debts, avoiding new loans, and increasing your income if possible. Even a slight reduction in your DTI can make a significant difference in how lenders perceive your ability to repay a used car loan.

3. The Down Payment: Your Game Changer

Making a substantial down payment is one of the most effective ways to improve your loan terms and increase your approval chances. A larger down payment reduces the amount you need to borrow, which directly lowers your monthly payments and the total interest you’ll pay over the life of the loan.

Pro tips from us: Aim for at least 10-20% of the used car’s purchase price. This not only makes you a more attractive borrower but also helps prevent you from being "upside down" on your loan (owing more than the car is worth) early in your ownership. It also signals financial stability to lenders.

Even a modest down payment shows commitment and reduces the lender’s risk. If you can save up a larger sum, it’s often worth the wait, as the long-term savings on interest can be substantial.

4. Proof of Income & Stability: What Lenders Look For

Lenders want assurance that you have a stable source of income to repay the loan. Be prepared to provide documentation such as recent pay stubs (typically the last two or three months), W-2 forms, and potentially bank statements.

Self-employed individuals may need to provide tax returns from the past two years and detailed bank statements. A consistent employment history is also viewed favorably. Lenders prefer to see a steady job for at least six months to a year, indicating reliable income.

If you’ve recently changed jobs, especially within the same industry and at a higher pay rate, it might still be seen positively. The key is demonstrating a clear and consistent ability to earn and manage income.

Navigating Your Lending Options: Where to Find Your Loan

Once your financial profile is optimized, it’s time to explore where to secure your used car loan. There are several avenues, each with its own advantages and disadvantages. Always compare offers from multiple sources to find the best fit.

1. Banks & Credit Unions

Traditional banks and credit unions are often excellent sources for used car loans, especially if you have good to excellent credit. They typically offer competitive interest rates and a wide range of loan products. If you have an existing relationship with a bank or credit union, you might even qualify for special member rates or expedited processing.

Credit unions, in particular, are known for their member-focused approach and often provide slightly lower interest rates than traditional banks because they are non-profit organizations. Membership is usually required, but it’s often easy to join. They also tend to be more understanding and flexible with borrowers who have less-than-perfect credit.

The main drawback can be a slower application process compared to online lenders, and their criteria might be stricter for those with lower credit scores.

2. Online Lenders

The digital age has brought forth a plethora of online lenders specializing in auto loans. These platforms offer unparalleled convenience, allowing you to apply for a used car loan from the comfort of your home, often receiving decisions within minutes. Many online lenders cater to a broader spectrum of credit scores, from excellent to subprime.

Online lenders are great for quick comparisons and often provide a streamlined application experience. They can be particularly useful for those who might not qualify for the best rates at traditional institutions but still want competitive options.

However, it’s crucial to thoroughly vet online lenders. Read reviews, check their reputation, and ensure they are legitimate. Always compare their offers against traditional banks and credit unions to ensure you’re getting the best deal.

3. Dealership Financing

Most car dealerships offer financing options directly through their own finance departments. This can be very convenient, allowing for a one-stop-shop experience where you can select your car and arrange financing simultaneously. Dealerships often work with a network of lenders and can sometimes find competitive rates, especially if they are trying to move inventory.

However, relying solely on dealership financing without pre-approval can be a common mistake. Dealers sometimes mark up interest rates to increase their profit, and without an outside offer to compare, you might unknowingly accept less favorable terms. While convenient, always approach dealership financing with your pre-approval in hand to ensure you’re getting a truly competitive offer.

Decoding the Loan Offer: What to Look For

Once you start receiving loan offers, it’s essential to understand the key components to compare them effectively. Don’t just look at the monthly payment; delve into the details to understand the true cost of borrowing.

1. Interest Rate (APR): The True Cost of Borrowing

The interest rate is the percentage charged by the lender for the use of their money. The Annual Percentage Rate (APR) is even more important as it represents the total cost of borrowing, including the interest rate and any additional fees. A lower APR means you’ll pay less over the life of the loan.

Always compare the APRs across different offers. Even a difference of one or two percentage points can translate into hundreds or even thousands of dollars in savings over several years. Understand whether the rate is fixed (stays the same throughout the loan) or variable (can change). For a used car loan, a fixed rate is generally preferred for predictability.

2. Loan Term: Shorter vs. Longer

The loan term is the duration over which you will repay the loan, typically expressed in months (e.g., 36, 48, 60, 72 months). A shorter loan term means higher monthly payments but less interest paid overall. A longer loan term results in lower monthly payments but significantly more interest paid over time.

Pro tips from us: While a longer term might make monthly payments more affordable, it also means you’ll be paying interest for a longer period. Try to strike a balance that fits your budget without extending the loan unnecessarily. Avoid stretching a used car loan too long, as the car’s value may depreciate faster than you pay off the loan, leaving you "upside down."

3. Fees: Origination, Processing, Prepayment Penalties

Scrutinize the fine print for any additional fees. Common fees include origination fees (charged for processing the loan), documentation fees, and sometimes even prepayment penalties (a fee for paying off your loan early).

While some fees are standard, others might be negotiable or avoidable. Be wary of excessive fees that add significant costs to your loan. Always ask for a clear breakdown of all charges associated with the loan.

4. Total Cost of the Loan: A Holistic View

Beyond the monthly payment, calculate the total cost of the loan by multiplying your monthly payment by the number of months in the loan term, then add any upfront fees. This gives you a clear picture of how much you’ll pay in total.

Comparing the total cost of the loan from different lenders provides the most accurate assessment of which offer is truly the best value. Sometimes, a slightly higher monthly payment on a shorter term can result in a much lower total cost.

Special Situations: Getting a Used Car Loan with Challenges

Not everyone has a perfect credit score or a long, pristine credit history. It’s still possible to secure a used car loan, but it might require a slightly different approach and more strategic planning.

1. Bad Credit: Is It Possible?

Yes, getting a used car loan with bad credit is absolutely possible, though it will likely come with higher interest rates. Lenders view bad credit as a higher risk, so they compensate by charging more for the loan.

Strategies for securing a used car loan with bad credit include:

- Larger Down Payment: This significantly reduces the lender’s risk.

- Co-signer: A co-signer with good credit can dramatically improve your approval chances and secure a better rate.

- Subprime Lenders: These lenders specialize in working with borrowers with lower credit scores. However, their rates will be higher.

- Credit Unions: As mentioned, credit unions can sometimes be more flexible.

- Secured Loan: Some lenders offer secured loans where the car itself acts as collateral.

Common mistakes to avoid are jumping at the first "guaranteed approval" offer without scrutinizing the terms. These often come with exorbitant interest rates and fees. Always compare multiple offers, even if your credit isn’t ideal.

2. No Credit History: Building Your Path to Approval

If you’re new to credit, getting a used car loan can be a challenge because lenders have no data to assess your risk. However, it’s not insurmountable.

Consider these approaches:

- Secured Loan: Similar to bad credit, a secured loan might be an option.

- Co-signer: Having a co-signer with established credit can be a huge advantage.

- Alternative Data: Some lenders are starting to consider alternative data like rent payments, utility bills, and bank account activity to assess creditworthiness.

- Build Credit First: If possible, take some time to build a small credit history with a secured credit card or a small installment loan before applying for a car loan.

The key is to demonstrate reliability and a willingness to manage financial responsibilities. Be transparent with lenders about your situation, and be prepared to provide extensive documentation of your income and stability.

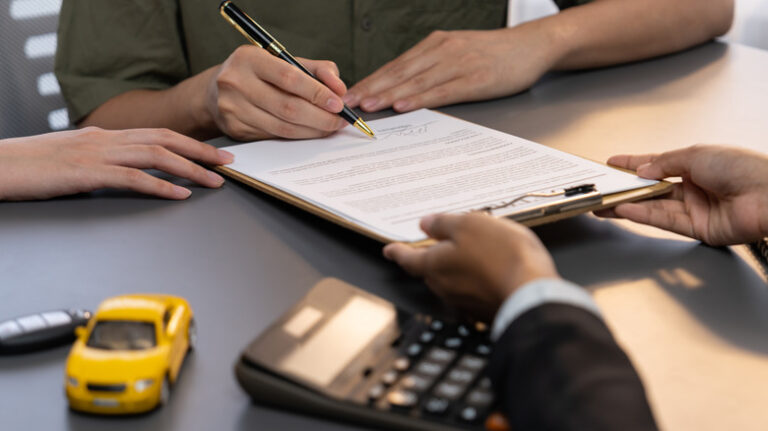

The Final Steps: Sealing the Deal

You’ve done your homework, secured pre-approval, and found the perfect used car and loan offer. Now, it’s time to finalize everything.

Before signing any documents, carefully review the entire loan contract. Ensure all the terms you agreed upon – interest rate, loan term, monthly payment, and fees – are accurately reflected. Don’t hesitate to ask questions if anything is unclear.

Understand any additional products offered by the dealership, such as extended warranties, gap insurance, or service plans. While some can be valuable, others might be unnecessary or overpriced. Make informed decisions and only purchase what you truly need.

Finally, understand the process for title and registration. In most cases, the dealership will handle the initial paperwork, but confirm what you need to do to complete the process and legally transfer ownership.

Conclusion: Your Road to a Great Used Car Loan

Securing the best way to get a used car loan doesn’t have to be a daunting task. By taking a proactive, informed approach – understanding your financial profile, getting pre-approved, comparing lenders, and meticulously reviewing offers – you position yourself for success. This ultimate guide has equipped you with the strategies to navigate the complexities of used car financing, ensuring you get the most favorable terms and an easy approval process.

Remember, preparation is your most powerful tool. Don’t rush the process, and always advocate for your best financial interests. With these insights, you’re not just buying a used car; you’re making a smart financial decision that will serve you well for years to come. Now, go forth, secure that ideal used car loan, and enjoy the open road ahead!