Unlock Your Savings: A Deep Dive into Fifth Third Bank Refinance Car Loan

Unlock Your Savings: A Deep Dive into Fifth Third Bank Refinance Car Loan Carloan.Guidemechanic.com

Are you currently paying a high interest rate on your car loan? Perhaps your financial situation has improved since you first purchased your vehicle, or you’re simply looking for ways to reduce your monthly expenses. If so, refinancing your car loan could be a smart move, and Fifth Third Bank offers compelling options that are worth exploring.

In this super comprehensive guide, we’ll delve into everything you need to know about a Fifth Third Bank refinance car loan. We’ll explore the benefits, walk you through the application process, discuss eligibility, and share expert tips to ensure you secure the best possible terms. Our goal is to equip you with the knowledge to make an informed decision and potentially save a significant amount of money over the life of your auto loan.

Unlock Your Savings: A Deep Dive into Fifth Third Bank Refinance Car Loan

Why Consider Refinancing Your Car Loan? More Than Just a Lower Payment

Many drivers initially focus on securing any financing just to get behind the wheel of their desired vehicle. Over time, however, circumstances change, and the terms of that initial loan might no longer be the best fit. This is where refinancing comes into play, offering a powerful tool to optimize your financial health.

Lowering Your Interest Rate: One of the most compelling reasons to pursue a Fifth Third auto loan refinance is the potential to secure a lower interest rate. If your credit score has improved since you first took out your loan, or if market rates have dropped, you could qualify for a significantly better rate. A lower interest rate directly translates to less money paid over the loan term.

Reducing Your Monthly Payments: For many, the immediate benefit of a Fifth Third Bank car loan refinance is a more manageable monthly payment. By extending the loan term or securing a lower interest rate, you can free up cash flow in your budget, making your finances feel less strained. This extra breathing room can be incredibly valuable for everyday expenses or saving for other goals.

Shortening Your Loan Term: Conversely, if your primary goal is to pay off your vehicle faster and save on total interest, refinancing can help. If you’re in a better financial position now, you might opt for a shorter loan term with slightly higher monthly payments but significantly less interest paid overall. This accelerates your journey to becoming debt-free.

Gaining Financial Flexibility: A refinance can also provide an opportunity to adjust the terms to better suit your current financial strategy. Perhaps you want to align your car payment due date with other bills, or you need a different loan structure. A Fifth Third Bank refinance can offer that flexibility, tailoring the loan to your evolving needs.

Based on my experience, many people overlook the power of refinancing, sticking with their original loan even when better options are available. Regularly reviewing your loan terms, especially if your credit has improved, is a pro tip that can lead to substantial savings.

Is Fifth Third Bank the Right Choice for Your Auto Loan Refinance?

When it comes to financial institutions, Fifth Third Bank has a long-standing reputation and offers a comprehensive suite of banking services. For auto loan refinancing, they stand out for several reasons, making them a strong contender for your consideration.

Fifth Third Bank is known for its customer-centric approach and competitive rates, especially for well-qualified borrowers. They understand that every borrower’s situation is unique and strive to offer solutions that cater to individual needs. Their online application process is designed to be straightforward, providing a user-friendly experience from start to finish.

One of the advantages of choosing a major bank like Fifth Third is the stability and resources they offer. They often have the capacity to provide competitive interest rates and flexible terms. This can be particularly beneficial if you’re looking for a reliable lender with a proven track record in the auto loan market.

Pro tips from us: While we’re focusing on Fifth Third Bank, it’s always wise to compare offerings from a few different lenders. However, Fifth Third consistently features as a strong option due to its established presence and commitment to competitive auto loan products. Their customer service also tends to be very accessible, which can be a huge plus during the application process.

Understanding Fifth Third Bank’s Car Refinance Process

Navigating the refinancing journey might seem daunting at first, but with Fifth Third Bank, the process is streamlined and designed for clarity. We’ll break down each step to give you a clear roadmap from application to approval.

Step 1: Research and Preparation – Laying the Groundwork

Before you even begin an application, a little preparation goes a long way. Start by gathering all the details of your current car loan. This includes your existing interest rate, your current monthly payment, the remaining balance, and the number of payments left.

Next, it’s crucial to check your credit score. Many online services offer free credit score checks, and knowing where you stand will give you a good indication of the rates you might qualify for. A higher credit score generally leads to better interest rates on a Fifth Third Bank car loan refinance. You’ll also want to understand your vehicle’s current market value, as this plays a role in the loan-to-value ratio.

Finally, define your financial goals. Are you aiming for a lower monthly payment, a shorter loan term, or a reduced total cost? Clearly understanding your objective will help you evaluate Fifth Third’s offers effectively.

Step 2: The Application Process – Submitting Your Information

Once you’re prepared, you can begin the application for your Fifth Third auto loan refinance. Fifth Third Bank typically offers an online application, which is convenient and can be completed from the comfort of your home. You’ll need to provide personal information such as your name, address, Social Security number, and employment details.

You’ll also be asked for information about your current vehicle, including its make, model, year, VIN, and mileage. Be ready to provide details about your current loan, including the lender’s name and account number. Accuracy is paramount here; double-check all information before submitting to avoid delays.

Common mistakes to avoid are not having all your documents readily available or rushing through the application. Taking your time and ensuring everything is accurate can significantly speed up the approval process.

Step 3: Underwriting and Approval – What Fifth Third Bank Looks For

After you submit your application, Fifth Third Bank’s underwriting team will review your information. They’ll assess several factors to determine your creditworthiness and the terms they can offer. Key considerations include your credit history, your debt-to-income (DTI) ratio, and the value of your vehicle.

They will pull your credit report, which will result in a hard inquiry. This is a normal part of the loan application process. Fifth Third Bank uses this information to gauge your ability to repay the loan responsibly. If everything looks good, you may receive a conditional approval, outlining the potential terms of your new loan.

Step 4: Loan Closing and Funding – Finalizing Your Refinance

If you receive an offer from Fifth Third Bank that meets your financial goals, the next step is to review the loan documents carefully. Pay close attention to the interest rate, loan term, monthly payment, and any fees associated with the refinance. Ensure you understand all the terms before signing.

Once you accept the offer and sign the necessary paperwork, Fifth Third Bank will finalize the refinance. They will typically pay off your old car loan directly, and your new loan with Fifth Third Bank will commence. You’ll then begin making your monthly payments to Fifth Third Bank according to the new terms.

Eligibility Requirements for a Fifth Third Auto Loan Refinance

To qualify for a Fifth Third Bank refinance car loan, you’ll need to meet specific criteria. While exact requirements can vary, here are the common factors they consider to assess your eligibility and determine your interest rate.

Credit Score: Your credit score is arguably the most significant factor. Generally, a good to excellent credit score (typically 670 or higher) will qualify you for the most competitive interest rates. However, Fifth Third Bank may consider applicants with lower scores, albeit with potentially higher rates. Improving your credit score before applying can yield substantial benefits. for more detailed strategies.

Debt-to-Income (DTI) Ratio: This ratio compares your total monthly debt payments to your gross monthly income. A lower DTI indicates that you have more disposable income to manage new debt, making you a less risky borrower. Fifth Third Bank will look for a healthy DTI to ensure you can comfortably afford the new monthly payments.

Vehicle Age and Mileage: Most lenders, including Fifth Third Bank, have limitations on the age and mileage of the vehicle being refinanced. Older cars or those with very high mileage might be deemed less valuable or more prone to issues, making them harder to refinance. Typically, vehicles under seven to ten years old with less than 100,000 to 120,000 miles are preferred.

Loan Amount and Existing Loan Status: There might be minimum or maximum loan amounts for refinancing. Additionally, your existing loan must be in good standing, meaning you haven’t been consistently delinquent on payments. Fifth Third Bank usually won’t refinance a loan that is already severely past due.

Residency and Income: You will need to be a U.S. resident and typically provide proof of stable income to demonstrate your ability to repay the loan. This ensures the bank is lending responsibly and to individuals who can meet their obligations.

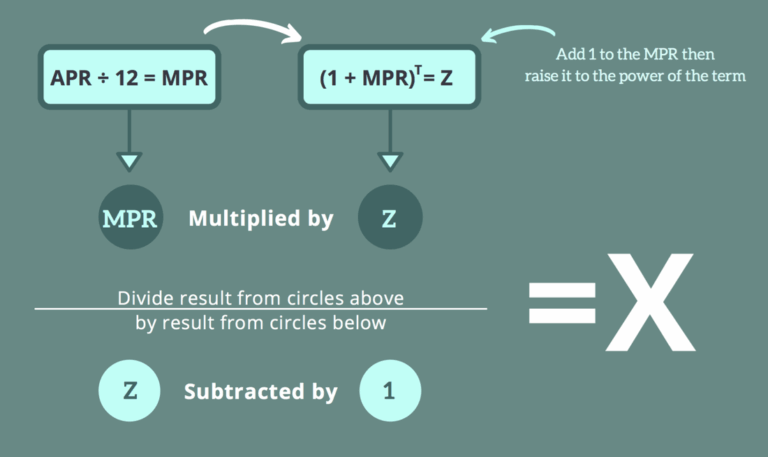

What Factors Influence Your Fifth Third Refinance Rate?

The interest rate you receive on your Fifth Third Bank refinance car loan isn’t arbitrary. It’s carefully calculated based on a combination of factors, each reflecting your risk profile as a borrower and the prevailing economic conditions. Understanding these influences can help you strategize for the best possible outcome.

Your Credit Score: As mentioned, your credit score is paramount. A higher score signifies a history of responsible borrowing and repayment, which makes you a lower risk in the eyes of Fifth Third Bank. This directly translates to access to their most favorable interest rates. Conversely, a lower score might lead to higher rates to offset the perceived risk.

The Loan Term You Choose: The length of your new auto loan refinance term significantly impacts the interest rate. Shorter loan terms typically come with lower interest rates because the bank gets its money back sooner, reducing their long-term risk. Longer terms, while offering lower monthly payments, often carry slightly higher interest rates over the life of the loan.

Your Vehicle’s Value and Loan-to-Value (LTV) Ratio: The current market value of your car plays a crucial role. Fifth Third Bank assesses the loan-to-value (LTV) ratio, which compares the amount you want to borrow to the car’s actual value. If you owe significantly more than your car is worth (high LTV), it can be harder to get a favorable rate, as the bank has less collateral.

Current Market Interest Rates: The broader economic environment and the Federal Reserve’s interest rate policies also influence car refinance rates. When overall interest rates are low, lenders can offer more competitive rates. When rates are high, all loan products, including auto refinancing, tend to be more expensive. You can monitor current economic trends and interest rate movements from reliable sources like the Federal Reserve.

Your Debt-to-Income (DTI) Ratio: A healthy DTI ratio reassures Fifth Third Bank that you are not over-extended with other debts. If a significant portion of your income is already allocated to existing debt payments, it might indicate a higher risk, potentially leading to a higher refinance rate.

Maximizing Your Savings with a Fifth Third Bank Car Refinance

Securing a Fifth Third Bank refinance car loan is just the first step. To truly maximize your financial benefits and achieve significant savings, consider these expert strategies.

Strategically Choose Your Loan Term: While a longer term can lower your monthly payment, it often means paying more interest over the life of the loan. If your budget allows, opt for the shortest term you can comfortably afford. This strategy minimizes the total interest paid and helps you become debt-free faster. Weigh the balance between monthly affordability and total cost savings.

Make Extra Payments When Possible: Even if you’ve secured a fantastic low-interest rate, making additional payments whenever you can will accelerate your principal reduction. This means less interest accrues over time, leading to substantial overall savings. Even small, consistent extra payments can make a big difference.

Maintain or Improve Your Credit Score: Your credit score is a dynamic entity. Continuing to make all your payments on time, keeping credit utilization low, and avoiding new debt can further improve your score. A consistently excellent credit history can open doors to even better financial products in the future, should you need them.

Set Up Automatic Payments: Automating your monthly payments with Fifth Third Bank ensures you never miss a due date. This not only protects your credit score but also helps you avoid any potential late fees. Some lenders even offer a slight interest rate reduction for setting up automatic payments.

Review Your Loan Annually: Don’t just set it and forget it. Your financial situation and market rates can change. It’s a good practice to review your auto loan annually. If interest rates have dropped significantly, or your credit score has drastically improved, you might even consider refinancing again in the future (though be mindful of any application fees).

Pro tips from us: Always remember that your car loan is a tool. Use it strategically. If you find yourself with extra cash, consider whether putting it towards your auto loan principal is a better use than other options, especially if your loan rate is higher than savings account yields. for broader financial advice.

Potential Drawbacks and Things to Consider

While a Fifth Third Bank refinance car loan offers numerous advantages, it’s also important to be aware of potential downsides and factors to consider before committing. A thorough understanding ensures you make the most informed decision.

Temporary Impact on Credit Score: When you apply for a refinance, Fifth Third Bank will perform a hard inquiry on your credit report. This can cause a small, temporary dip in your credit score. However, if you’re approved and manage the new loan responsibly, your score will typically recover and often improve over time.

Application Fees: While many lenders offer fee-free auto refinancing, some might charge an application or processing fee. Always clarify any potential costs upfront with Fifth Third Bank. Even a small fee could negate some of your potential savings if your interest rate reduction is minimal.

Extending the Loan Term: If your primary goal is to lower your monthly payment by extending the loan term, be mindful that this means you’ll be paying interest for a longer period. While individual payments are lower, the total amount of interest paid over the loan’s life could increase, even with a lower interest rate. Carefully calculate the total cost before committing to a longer term.

Prepayment Penalties on Your Current Loan: Although rare with auto loans, it’s crucial to check your existing loan agreement for any prepayment penalties. Some lenders might charge a fee if you pay off your loan early. This is an important detail to confirm before initiating a refinance with Fifth Third Bank, as it could offset some of your savings.

Vehicle Depreciation: Cars depreciate rapidly. If you extend your loan term significantly, there’s a higher chance you might end up "upside down" on your loan, meaning you owe more than the car is worth. This can create challenges if you need to sell or trade in the vehicle before the loan is paid off.

Conclusion: Is a Fifth Third Bank Refinance Car Loan Right for You?

Refinancing your car loan with Fifth Third Bank presents a significant opportunity to optimize your financial situation, whether your goal is to reduce your monthly payments, lower your total interest paid, or gain more control over your budget. With its straightforward process, competitive rates, and commitment to customer service, Fifth Third Bank stands out as a reliable and effective option for auto loan refinancing.

By understanding the eligibility requirements, preparing thoroughly for the application process, and strategically choosing your loan terms, you can unlock substantial savings. Remember to consider all the factors, including potential drawbacks, to ensure this financial move aligns perfectly with your personal goals.

Don’t let high interest rates or burdensome monthly payments hold you back. Explore the possibilities of a Fifth Third Bank refinance car loan today. Take the proactive step to review your current loan and see how much you could save, putting you on the fast track to financial freedom and peace of mind.