Unlocking Financial Freedom: Your Comprehensive Guide to Grants That Help Pay Off Car Loans

Unlocking Financial Freedom: Your Comprehensive Guide to Grants That Help Pay Off Car Loans Carloan.Guidemechanic.com

The weight of a car loan can feel like a constant burden, impacting your monthly budget and overall financial well-being. Many individuals dream of finding a way to alleviate this pressure, often wondering if there are "grants to pay off car loans" available. While the idea of a direct grant to simply erase your existing car debt is largely a myth, this comprehensive guide will delve deep into the reality of financial assistance.

As an expert in financial literacy and a professional SEO content writer, I’ve seen firsthand the confusion surrounding debt relief. We’ll explore not only the rare instances where direct help might exist but, more importantly, the myriad of indirect strategies and legitimate programs that can significantly reduce your financial strain, effectively freeing up funds to tackle that car loan. Our ultimate goal is to equip you with actionable knowledge, enabling you to navigate your financial challenges with confidence and clarity.

Unlocking Financial Freedom: Your Comprehensive Guide to Grants That Help Pay Off Car Loans

The Truth About "Grants to Pay Off Car Loans": Setting Realistic Expectations

Let’s address the elephant in the room right away. The concept of a direct "grant to pay off a car loan" is, for most people, a misconception. Unlike grants for education, housing, or starting a business, which are specifically designed to fund particular endeavors without repayment, grants rarely exist for the sole purpose of paying off personal consumer debt like an existing car loan.

Based on my experience researching financial aid and debt relief programs, grant-giving organizations typically prioritize forward-looking initiatives or immediate crisis intervention. They aim to help people achieve specific goals or overcome acute emergencies, rather than retroactively paying off debts incurred through personal choices. Understanding this fundamental distinction is crucial for setting realistic expectations and focusing your efforts on genuinely viable solutions.

Reframing Your Search: Indirect Pathways to Car Loan Relief

Since direct grants for existing car loans are exceptionally rare, our strategy shifts. We need to explore programs and resources that can indirectly help you manage or reduce your car loan burden. This often involves receiving assistance in other areas of your life, which then frees up your own funds to put towards your vehicle payments.

Think of it as optimizing your entire financial ecosystem. By lowering expenses in other critical categories, you create a surplus. This surplus can then be strategically directed towards your car loan, providing the relief you’re seeking.

Understanding Key Categories of Assistance (Not Direct Car Loan Grants)

While you won’t find a "Car Loan Payoff Grant" application, several categories of assistance can provide significant indirect relief. It’s about looking at your entire financial picture.

1. Emergency Financial Assistance Programs

These programs are designed to help individuals and families facing immediate financial crises, often preventing homelessness, utility shut-offs, or food insecurity. While they don’t directly pay off car loans, receiving help with these essential expenses can free up a substantial portion of your budget.

-

Non-Profit Organizations and Charities:

- The Salvation Army: Offers a range of services, including emergency financial assistance for utilities, rent, and sometimes transportation costs like gas vouchers or minor car repairs. Their focus is on preventing immediate crises.

- United Way: Often acts as a hub, connecting individuals to local resources through its 211 helpline. They can direct you to local agencies that provide assistance with housing, food, and other essential needs.

- Catholic Charities: Provides emergency assistance, including help with food, housing, and sometimes limited financial aid for critical needs. Eligibility varies by diocese and local program availability.

- Local Community Action Agencies: These agencies are often funded by federal and state programs to combat poverty at the local level. They offer various services, including energy assistance, food programs, and sometimes emergency financial aid.

- How They Help: By covering or subsidizing critical living expenses, these organizations allow you to reallocate funds that would otherwise go towards rent, utilities, or food, directly to your car loan. This strategic reallocation is a powerful form of indirect relief.

-

Application Process Insights: Typically, you’ll need to demonstrate genuine financial hardship, provide proof of income and expenses, and show that you’ve explored other options. Be prepared to fill out detailed applications and attend interviews. Patience and persistence are key here.

2. Government Assistance Programs

Various federal and state government programs aim to support low-income individuals and families. Again, these are not for car loan payments, but they significantly ease your overall financial burden.

- Temporary Assistance for Needy Families (TANF): This program provides cash assistance to help families with children achieve self-sufficiency. While it has strict eligibility requirements and time limits, the cash aid can be used for various needs, indirectly freeing up your budget for other debts.

- Supplemental Nutrition Assistance Program (SNAP) / Food Stamps: By providing benefits to purchase food, SNAP reduces one of your most significant monthly expenses. The money you save on groceries can then be put towards your car loan.

- Low Income Home Energy Assistance Program (LIHEAP): This program helps low-income households with their heating and cooling costs. Reducing your utility bills, especially during extreme weather, can free up a considerable amount of money.

- Medicaid/CHIP: Access to affordable healthcare through Medicaid or the Children’s Health Insurance Program (CHIP) can prevent medical debt from spiraling and allow you to prioritize other financial obligations, including your car loan.

- How They Indirectly Help: These programs act as financial shock absorbers. By ensuring your basic needs are met, they reduce the pressure on your personal budget, making it possible to allocate more funds towards your car loan. Eligibility for these programs is typically based on income thresholds and family size.

3. Work-Related Transportation Programs

In some specific cases, programs aimed at helping individuals get to and from work might offer a unique, albeit indirect, form of transportation assistance.

- Vocational Rehabilitation Services: If you have a disability that impacts your ability to work, state vocational rehabilitation agencies might offer assistance. This can include help with transportation costs, vehicle modifications, or even assistance with purchasing a new car if it’s directly tied to your employment needs. However, paying off an existing car loan is usually not their purview.

- Workforce Development Boards: Local workforce development boards, often part of your state’s Department of Labor, sometimes offer limited assistance for job seekers or those starting new employment. This might include gas vouchers, bus passes, or very rarely, assistance with minor car repairs essential for employment.

- Specific Demographics: Programs for veterans or individuals transitioning out of homelessness sometimes include transportation support to help them maintain employment. It’s always worth exploring these specialized resources if they apply to your situation.

Strategies to Directly Reduce Your Car Loan Burden (Self-Help)

Beyond external assistance, there are powerful self-help strategies you can employ to directly reduce the burden of your car loan. These methods don’t involve grants but are often the most effective paths to financial relief.

1. Refinancing Your Car Loan

Refinancing is one of the most impactful ways to reduce your monthly car payment or total interest paid. This involves taking out a new loan to pay off your existing car loan, ideally with better terms.

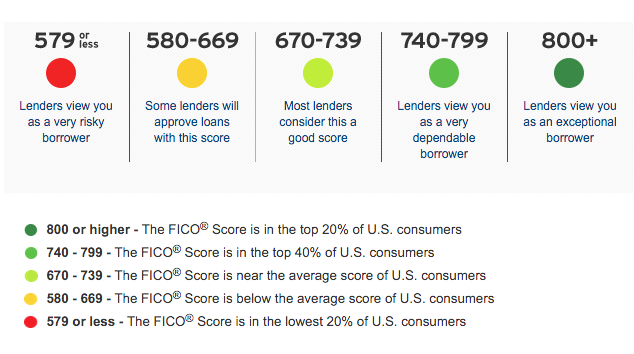

- Lower Interest Rates: If your credit score has improved since you first took out the loan, or if market rates have dropped, you could qualify for a significantly lower Annual Percentage Rate (APR). A lower APR means less money goes to interest and more to the principal, accelerating your payoff.

- Lower Monthly Payments: You might choose to extend the loan term, which typically results in lower monthly payments. While this means paying more interest over the life of the loan, it can provide crucial immediate budget relief.

- Shorter Loan Term: Conversely, if you can afford it, refinancing to a shorter term can save you a substantial amount in interest and get you debt-free faster.

- Eligibility and Process: Lenders will look at your credit score, debt-to-income ratio, and the value of your vehicle. Pro tips from us: Compare offers from multiple lenders – banks, credit unions, and online lenders – to find the best rate. Don’t just accept the first offer. You’ll need your current loan details, vehicle information, and personal financial documents.

- Common mistakes to avoid: Not checking your credit score before applying, accepting an offer without comparing, or extending the loan term so much that you end up upside down on your loan (owing more than the car is worth).

2. Selling Your Car and Buying a Cheaper One

This is a more drastic but highly effective solution if your car loan is truly overwhelming your finances. If you owe more than your car is worth (you’re "upside down" or have negative equity), this option becomes more complicated but not impossible.

- Assess Your Car’s Value: Use resources like Kelley Blue Book (KBB) or Edmunds to determine your car’s trade-in and private party resale value.

- Understand Your Loan Payoff: Contact your lender to get an exact payoff amount.

- The Swap: If your car’s value is greater than or equal to your loan payoff, you can sell it and use the proceeds to clear the debt. You can then purchase a more affordable, used vehicle, perhaps even one you can pay for in cash, eliminating monthly payments entirely.

- Dealing with Negative Equity: If you owe more than the car is worth, you’ll need to pay the difference out of pocket to sell it. This can be challenging but might still be worthwhile if the new, cheaper car significantly reduces your overall transportation costs.

3. Negotiating with Your Lender

While not always successful, it’s worth exploring options with your current lender, especially if you’re experiencing a temporary financial hardship.

- Deferment or Forbearance: Some lenders might allow you to temporarily pause or reduce payments for a few months. Be aware that interest usually continues to accrue during this period, potentially increasing your total cost. This is typically reserved for extreme situations like job loss or medical emergencies.

- Loan Modification: In very rare cases, and usually only with significant documented hardship, a lender might agree to modify the terms of your loan, such as lowering the interest rate or extending the term. This is less common for car loans than for mortgages.

- Proactive Communication: Based on my experience, proactive communication is key. Don’t wait until you miss a payment. Contact your lender as soon as you anticipate difficulty and explain your situation clearly and calmly.

4. Budgeting and Frugality

This is perhaps the most accessible and fundamental strategy for anyone looking to free up funds to pay down debt. By meticulously tracking and optimizing your spending, you can create the necessary surplus.

- Create a Detailed Budget: Understand exactly where every dollar goes. Use budgeting apps or spreadsheets to categorize your income and expenses.

- Identify Non-Essential Spending: Where can you cut back? Dining out less, canceling unused subscriptions, reducing entertainment costs, or finding cheaper alternatives for everyday items can quickly add up.

- "Snowball" or "Avalanche" Method: Once you free up extra cash, apply it aggressively to your car loan. The "debt snowball" involves paying off the smallest debt first for psychological wins, while the "debt avalanche" prioritizes debts with the highest interest rates to save the most money. Choose the method that motivates you most.

- Building an Emergency Fund: While not directly paying off your car loan, having an emergency fund (3-6 months of living expenses) prevents you from falling further into debt when unexpected costs arise. This indirectly protects your ability to make car loan payments.

How to Find and Apply for Assistance: Your Action Plan

Finding and applying for assistance requires diligent research and a systematic approach.

-

Start Local:

- Dial 211: This national helpline (available in most areas) connects you with local social services, non-profits, and government programs. It’s an excellent starting point for identifying resources in your community.

- Visit Local Government Websites: Your city or county government website will often list departments that offer social services, housing assistance, or workforce development programs.

- Community Centers and Churches: Many local churches and community centers run their own assistance programs or can direct you to others.

-

Online Search Strategies:

- Be specific with your search terms. Instead of just "grants," try "emergency financial assistance ," "utility assistance ," or "food banks near me."

- Look for official government websites (.gov) and reputable non-profit organizations (.org).

-

Required Documentation:

- Proof of Income: Pay stubs, tax returns, benefit statements.

- Proof of Residency: Utility bills, lease agreements.

- Identification: Driver’s license, state ID.

- Proof of Hardship: Eviction notices, utility shut-off notices, medical bills, layoff notices.

- Expense Documentation: Bills for rent, utilities, medical, and your car loan statements.

- Having these documents organized and ready will significantly streamline your application process.

-

Persistence and Patience:

- Applying for assistance can be a lengthy process. You might need to call multiple organizations, fill out several applications, and follow up regularly. Don’t get discouraged by initial rejections; learn why you were denied and explore other avenues.

Watch Out for Scams: Protect Yourself!

The desperation of financial hardship makes people vulnerable to scams. When searching for "grants to pay off car loans," you are likely to encounter fraudulent schemes.

- Upfront Fees: Legitimate grants and assistance programs never ask for an upfront fee to apply or process your application. This is a major red flag.

- Guarantees of Approval: No legitimate program can guarantee approval, especially without a thorough review of your circumstances. Be highly suspicious of anyone promising guaranteed money.

- Requests for Personal Banking Information: Be wary of requests for your bank account numbers, PINs, or Social Security number via unofficial channels (e.g., email or unsolicited phone calls). Only provide this information to verified, secure application portals.

- Unsolicited Offers: If you receive an unsolicited email, phone call, or social media message offering you a "grant," proceed with extreme caution. Legitimate programs don’t typically reach out to individuals this way.

- Pro tips from us: Always verify the legitimacy of any organization or program. Check their website, look for reviews, and if in doubt, contact a reputable financial counseling agency like the National Foundation for Credit Counseling (NFCC) for advice.

Beyond the Loan: Building Long-Term Financial Health

Getting your car loan under control is a significant step, but it’s also an opportunity to build a more secure financial future.

- Financial Literacy: Educate yourself on budgeting, saving, investing, and debt management. The more you know, the better equipped you’ll be to make sound financial decisions.

- Emergency Fund: Prioritize building an emergency fund. Aim for at least 3-6 months of living expenses. This acts as a buffer against unexpected costs, preventing you from falling back into debt.

- Improve Your Credit Score: A good credit score opens doors to better interest rates on future loans and credit cards. Pay bills on time, keep credit utilization low, and regularly check your credit report for errors.

- Debt Management Plans (DMPs): If you have multiple debts, a non-profit credit counseling agency can help you consolidate payments into a single, affordable monthly payment through a Debt Management Plan. While not a grant, it’s a structured approach to becoming debt-free.

Conclusion: Taking Control of Your Car Loan Debt

While the direct "grant to pay off car loans" might be an elusive dream, the journey to financial relief is far from impossible. This comprehensive guide has shown that by understanding the true nature of financial assistance, exploring indirect support programs, and implementing robust self-help strategies, you can significantly reduce the burden of your car loan.

Remember, the path to financial freedom is a marathon, not a sprint. It requires diligence, smart choices, and a proactive approach. By leveraging the information and strategies outlined here – from seeking emergency aid to refinancing and meticulous budgeting – you are empowered to take control of your financial situation. Start today by researching local resources, refining your budget, and communicating with your lender. Your journey towards a lighter financial load begins now.