Unlocking Financial Freedom: Your Ultimate Guide to the Shortest Car Loan

Unlocking Financial Freedom: Your Ultimate Guide to the Shortest Car Loan Carloan.Guidemechanic.com

Purchasing a car is a significant financial decision, often representing one of the largest expenditures in many people’s lives after a home. While the allure of low monthly payments on a long-term loan can be tempting, a growing number of savvy consumers are discovering the immense benefits of opting for the shortest car loan possible. This approach, though requiring a different financial mindset, can lead to substantial long-term savings and faster financial independence.

In this comprehensive guide, we will delve deep into everything you need to know about short-term car loans. We’ll explore their benefits, potential downsides, who they are best suited for, and crucial strategies to secure the best rates. Our goal is to equip you with the knowledge to make an informed decision, helping you navigate the complexities of car financing with confidence and clarity.

Unlocking Financial Freedom: Your Ultimate Guide to the Shortest Car Loan

What Exactly Constitutes a Shortest Car Loan?

When we talk about the "shortest car loan," we’re generally referring to loan terms that are significantly shorter than the industry average. While the standard car loan duration has crept up over the years, often extending to 60, 72, or even 84 months, a short-term loan typically falls within the 24 to 48-month range. Some lenders might even offer 12 or 18-month options for highly qualified borrowers.

The core principle behind a shorter loan is simple: you pay off the principal amount much faster. This accelerated repayment schedule directly impacts the total interest you accrue over the life of the loan. Unlike longer terms where interest costs can add up significantly, a shorter duration dramatically reduces this financial burden.

This approach prioritizes long-term savings over the lowest possible monthly payment. It’s a strategic choice for individuals who are financially stable and looking to minimize the total cost of their vehicle. Understanding this fundamental difference is the first step toward appreciating the power of a shortest car loan.

The Compelling Advantages of Opting for a Short Car Loan

Choosing a shorter car loan term isn’t just a different way to finance a vehicle; it’s a strategic financial move with numerous benefits. These advantages can significantly impact your overall financial health and provide a quicker path to asset ownership.

1. Significant Interest Savings

This is arguably the most compelling reason to choose a shortest car loan. When you borrow money, you pay interest on the outstanding principal balance. The longer that balance remains, the more interest you accumulate. By reducing the loan term, you drastically cut down the time interest has to accrue.

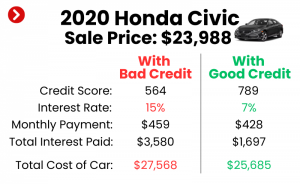

Consider this: a $30,000 car loan at 5% interest over 72 months might cost you thousands more in interest than the same loan over 36 months. Even if the monthly payment is higher for the shorter term, the overall cost difference can be substantial. Based on my experience, this is often the biggest motivator for financially astute buyers.

2. Faster Path to Ownership

There’s a unique sense of financial freedom that comes with owning your car outright. With a shortest car loan, you reach this milestone much sooner. This means no more monthly payments, freeing up a significant portion of your budget for other financial goals, such as saving, investing, or paying down other debts.

Psychologically, it’s incredibly empowering to know your vehicle is truly yours, free and clear. This accelerated ownership can reduce financial stress and provide greater peace of mind. You’re no longer tied to a long-term debt obligation.

3. Lower Overall Cost

Beyond just interest, a shorter loan often translates to a lower overall cost for your vehicle. While the sticker price remains the same, the true cost includes all interest and any associated fees over the loan’s lifetime. By minimizing the interest, you effectively pay less for the same car.

This financial efficiency means more of your money goes towards the actual vehicle and less towards the cost of borrowing. It’s a smart way to maximize your investment in a depreciating asset. Every dollar saved on interest is a dollar kept in your pocket.

4. Reduced Risk of Negative Equity

Negative equity, or being "upside down" on your car loan, occurs when you owe more on your car than it’s worth. This is a common problem with longer loan terms, especially given how quickly new cars depreciate. A shortest car loan significantly mitigates this risk.

By paying down the principal faster, you outpace the vehicle’s depreciation rate. This ensures you build equity more quickly, protecting you if you need to sell or trade in your car sooner than expected. It provides a crucial financial buffer against market fluctuations.

5. Financial Discipline and Freedom

Committing to a shortest car loan encourages robust financial discipline. The higher monthly payments necessitate careful budgeting and a clear understanding of your financial capacity. This discipline can spill over into other areas of your financial life, fostering healthier money habits.

Once the loan is paid off, the freed-up funds offer immense financial freedom. You can redirect those payments towards savings, retirement, a down payment on a home, or even a future car purchase. It’s an investment in your future financial flexibility.

Understanding the Potential Downsides: Is a Short Loan Right for Everyone?

While the benefits of a shortest car loan are compelling, it’s crucial to approach this decision with a balanced perspective. This financing strategy isn’t universally suitable, and understanding its potential drawbacks is just as important as knowing its advantages.

1. Higher Monthly Payments

This is the most immediate and significant trade-off. To pay off the same amount of principal in a shorter time frame, your individual monthly payments will be considerably higher compared to a longer-term loan. This requires a robust and stable monthly budget.

If your income is unpredictable or your current expenses are already high, these elevated payments could strain your finances. It’s essential to perform a thorough budget analysis before committing. Common mistakes to avoid are underestimating your monthly budget or failing to account for unexpected expenses.

2. Stricter Eligibility Requirements

Lenders perceive shorter loans as carrying a higher risk of default on individual payments, even if the overall loan term is safer. Consequently, they often impose stricter eligibility criteria. You’ll typically need an excellent credit score, a stable income, and a low debt-to-income ratio to qualify for the best rates.

If your credit isn’t stellar or your financial history has some blemishes, securing a shortest car loan might be more challenging or come with less favorable terms. Lenders want to be assured you can comfortably manage the higher payments.

3. Impact on Budget Flexibility

Committing to a high monthly car payment can reduce your financial flexibility. Should an unexpected expense arise—like a medical emergency, job loss, or home repair—those large car payments could become a significant burden. This reduces your buffer for life’s unforeseen challenges.

It’s vital to ensure that even with the higher car payment, you still have a healthy emergency fund and disposable income. Sacrificing your financial cushion for a shorter loan might not be the wisest long-term strategy. Always prioritize financial stability.

4. Less Room for Error

With a shorter loan, missing even one payment can have a more immediate and severe impact on your credit score and financial standing. There’s less leeway compared to longer terms where a slight delay might be less critical in the grand scheme. Every payment holds more weight.

This means you need to be highly disciplined with your payment schedule. Setting up automatic payments is highly recommended to avoid any oversights. The stakes are simply higher with a shortest car loan.

Who Benefits Most from a Shortest Car Loan?

While the allure of saving thousands in interest is universal, a shortest car loan is truly ideal for a specific profile of car buyer. Understanding if you fit this profile can help you determine if this strategy aligns with your financial goals and current situation.

Individuals with a stable and robust income are prime candidates. The ability to comfortably manage higher monthly payments without straining your budget is paramount. Your income should consistently exceed your expenses, leaving ample room for the car payment.

Those with an excellent credit score will find the most success. A strong credit history signals reliability to lenders, allowing you to secure the lowest interest rates on shorter terms. This combination maximizes your interest savings.

Buyers who prioritize long-term savings over low monthly payments are perfectly suited. If your primary goal is to minimize the total cost of ownership and achieve financial independence faster, the shortest car loan is your best ally. It’s about strategic long-term thinking.

Finally, people who tend to keep their cars for a long time benefit immensely. By paying off the loan quickly, you enjoy many years of car ownership without any monthly payments, maximizing the value of your purchase. You get to enjoy true, debt-free ownership.

How to Qualify for the Best Shortest Car Loan Rates

Securing the most favorable terms for a shortest car loan requires proactive preparation and smart financial decisions. Lenders look for specific indicators of reliability and repayment capacity.

1. Cultivate an Excellent Credit Score

Your credit score is the single most influential factor in determining your interest rate. Lenders use it to assess your risk. A score in the "excellent" range (typically 760+) will unlock the lowest rates and make you a highly attractive borrower for short-term loans.

Focus on paying all bills on time, keeping credit utilization low, and correcting any errors on your credit report. A robust credit history demonstrates your financial responsibility.

2. Demonstrate Stable Income and a Low Debt-to-Income Ratio

Lenders need assurance that you can comfortably afford the higher monthly payments. This means having a stable employment history and a consistent income stream. They will also scrutinize your debt-to-income (DTI) ratio.

Your DTI ratio compares your total monthly debt payments to your gross monthly income. A lower DTI (ideally below 36%) indicates you have plenty of disposable income to manage new debt. This is crucial for short-term loans.

3. Make a Healthy Down Payment

A substantial down payment reduces the amount you need to borrow, which in turn lowers your monthly payments (even on a short term) and the total interest paid. It also reduces the lender’s risk, often leading to better interest rates.

Pro tips from us: aiming for 20% or more as a down payment is an excellent strategy. It immediately builds equity and demonstrates your financial commitment. This can be a game-changer for securing the best rates.

4. Shop Around and Compare Lenders

Never settle for the first loan offer you receive. Different financial institutions—banks, credit unions, and online lenders—have varying rates and terms. Take the time to solicit quotes from several sources.

Credit unions, in particular, often offer very competitive rates to their members. Online lenders can also provide quick, streamlined processes. Compare not just interest rates but also any fees or penalties associated with the loan.

5. Consider a Co-signer (Use with Caution)

If your credit score isn’t quite excellent, a co-signer with strong credit can help you qualify for better terms. However, this should be approached with extreme caution. The co-signer is equally responsible for the loan, and any missed payments will impact their credit as well.

Only consider this option with someone you trust implicitly and who understands the full implications. It’s a significant financial commitment for both parties involved.

The Application Process: A Step-by-Step Guide

Navigating the loan application process for your shortest car loan can be straightforward if you’re prepared. Here’s a typical progression:

Step 1: Gather Necessary Documents. Before you even start applying, collect all relevant financial paperwork. This usually includes proof of income (pay stubs, tax returns), identification (driver’s license), proof of residence (utility bill), and information about your current debts. Having these ready will streamline the process.

Step 2: Get Pre-Approved. This is a critical step. Apply for pre-approval with several lenders before you even visit a dealership. Pre-approval gives you a firm offer of the loan amount and interest rate you qualify for, empowering you to negotiate the car price as a cash buyer. It also helps you understand what monthly payment you’re comfortable with.

Step 3: Compare Offers and Choose the Best Fit. Once you have multiple pre-approval offers, meticulously compare them. Look at the interest rate, any origination fees, and the exact monthly payment. Don’t be swayed by slightly lower monthly payments if it means a significantly longer term and more interest paid. Focus on the total cost of the loan.

Step 4: Finalize the Loan and Purchase the Car. With your chosen pre-approval in hand, you can confidently shop for your vehicle. Once you’ve selected the car, finalize the loan with your chosen lender. They will work with the dealership to complete the paperwork and transfer funds. This structured approach helps ensure you secure the best deal.

Strategic Tips for Managing and Paying Off Your Short Car Loan Even Faster

Even with a shortest car loan, there are still strategies you can employ to accelerate your debt repayment further, maximizing your interest savings and reaching true car ownership even quicker.

1. Make Extra Payments

This is the most direct way to pay off your loan faster. Any additional money you can put towards the principal reduces the amount on which interest is calculated. Even small, consistent extra payments can make a significant difference over time.

Consider rounding up your monthly payment, making an extra payment whenever you receive a bonus, or allocating a portion of tax refunds. Make sure any extra payments are applied directly to the principal.

2. Opt for Bi-weekly Payments

Instead of making one large payment each month, divide your monthly payment in half and pay it every two weeks. Since there are 26 bi-weekly periods in a year, this strategy results in you making 13 full monthly payments annually instead of 12.

This subtle shift can shave months off your loan term and save you hundreds in interest. It’s a painless way to accelerate repayment without feeling a huge pinch on your budget.

3. Refinance If Rates Drop or Your Credit Improves

Keep an eye on interest rates. If market rates fall significantly after you’ve taken out your loan, or if your credit score has substantially improved, consider refinancing. Refinancing means taking out a new loan to pay off your existing one, ideally at a lower interest rate.

This can further reduce your total interest paid, especially if you maintain a short loan term. Always calculate if the savings outweigh any refinancing fees.

4. Utilize Budgeting Tools and Apps

Staying on top of your finances is crucial for managing a shortest car loan. Use budgeting apps or spreadsheets to track your income and expenses. This helps you identify areas where you can cut back and free up more funds for extra loan payments.

For more budgeting tips, check out our article on . Understanding where your money goes empowers you to make smarter financial decisions.

Debunking Common Myths About Car Loans

Misconceptions about car financing can lead to costly mistakes. Let’s clarify some common myths that often deter people from considering a shortest car loan.

Myth 1: "Longer terms always mean cheaper cars." This is fundamentally false. While a longer term reduces your monthly payment, it significantly increases the total amount you pay for the car due to accrued interest. A "cheaper car" refers to the initial purchase price, not the overall cost of ownership with financing.

Myth 2: "You need perfect credit for any good loan." While excellent credit opens doors to the absolute best rates, you can still secure a good loan with strong credit (e.g., in the high 600s to low 700s). For a shortest car loan, however, the closer you are to perfect, the better your chances of securing the lowest possible rates.

Myth 3: "All lenders are the same." Absolutely not. Banks, credit unions, and online lenders each have different lending criteria, interest rates, and fee structures. Shopping around is paramount to finding the most competitive offer tailored to your financial profile. Pro tip: Credit unions often have some of the most favorable rates.

Real-Life Scenarios: When a Short Loan Makes Sense (and When it Doesn’t)

Understanding the theoretical benefits and drawbacks is one thing; seeing how a shortest car loan plays out in real-world scenarios is another.

Scenario 1: High Income, Excellent Credit, Long-Term Ownership Goal.

- Meet Sarah: Sarah earns a strong, stable income, has a credit score of 780, and plans to keep her new SUV for at least 8-10 years. She prioritizes long-term savings over low monthly payments.

- The Short Loan Fit: A 36-month loan makes perfect sense for Sarah. She can easily afford the higher monthly payments, will save thousands in interest, and will own her car outright in just three years, enjoying many years of debt-free driving. This aligns perfectly with her financial goals.

Scenario 2: Tight Budget, Average Credit, Frequent Car Upgrades.

- Meet Mark: Mark has an average credit score of 650, a moderate income with fluctuating expenses, and enjoys upgrading his car every 3-4 years. His budget is already stretched thin.

- The Short Loan Misfit: A shortest car loan would likely be a poor choice for Mark. His average credit might lead to a higher interest rate on a short term, and the higher monthly payments would strain his already tight budget. Given his tendency to upgrade frequently, the financial pressure and limited flexibility would outweigh any interest savings. A longer-term loan might be more appropriate for his current situation, even if it costs more overall.

The Future of Car Loans: Trends to Watch

The automotive and financial landscapes are constantly evolving, influencing how we finance vehicles. Staying aware of these trends can help you make even smarter decisions.

The rise of electric vehicles (EVs) is impacting loan terms. As EVs become more prevalent, their often higher initial cost might push some consumers towards longer loan terms, making the shortest car loan option even more valuable for those who can afford it to offset the higher price point. However, some lenders are also offering specialized "green car" loans with competitive rates.

Online lending platforms continue to grow in popularity, offering convenience and often highly competitive rates. Their streamlined application processes and ability to quickly compare offers from multiple lenders can be a huge advantage when seeking the shortest car loan. This increased transparency benefits consumers significantly.

We are also seeing a trend towards personalized loan options. As data analytics improve, lenders may offer more tailored interest rates and terms based on a highly individualized assessment of a borrower’s financial profile and even their driving habits (for usage-based insurance, which can indirectly affect loan decisions).

Conclusion: Is the Shortest Car Loan Your Path to Financial Freedom?

The shortest car loan represents a powerful financial tool for the right individual. It’s a deliberate choice to prioritize long-term savings and accelerated ownership over the immediate gratification of lower monthly payments. By embracing a shorter loan term, you can dramatically reduce the total cost of your vehicle, achieve financial freedom faster, and mitigate the risks associated with depreciation and negative equity.

While it demands a stable financial footing and disciplined budgeting, the rewards are undeniable. If you possess excellent credit, a robust income, and a clear vision for debt-free living, exploring the shortest car loan options could be one of the smartest financial decisions you make. Take the time to assess your financial situation, compare lenders diligently, and prepare yourself for a quicker path to owning your vehicle outright.

If you’re still weighing your options between different loan durations, our guide on might provide further clarity. For the latest interest rate trends and economic insights that can influence your car loan decision, refer to trusted external sources like the . Your journey to financial empowerment starts with informed choices.