Unlocking Massive Savings: What Happens If I Pay $100 Extra On My Car Loan Every Month?

Unlocking Massive Savings: What Happens If I Pay $100 Extra On My Car Loan Every Month? Carloan.Guidemechanic.com

Are you currently navigating the world of car ownership and looking for smart ways to manage your finances? Many of us dream of being debt-free, and one common question that arises for car owners is whether making an extra payment, even a small one, can truly make a difference. The answer, in short, is a resounding yes.

Imagine the impact of consistently contributing just an additional $100 towards your car loan each month. This seemingly modest amount can trigger a powerful chain reaction, drastically altering your loan’s trajectory. This comprehensive guide will meticulously break down the profound effects of this simple financial strategy, revealing how it can save you thousands in interest, accelerate your payoff, and provide invaluable peace of mind. Let’s dive deep into understanding the hidden power of that extra $100.

Unlocking Massive Savings: What Happens If I Pay $100 Extra On My Car Loan Every Month?

The Core Mechanics: What Exactly Happens When You Pay $100 Extra?

When you make a standard car loan payment, a portion goes towards the interest accrued since your last payment, and the remainder reduces your principal balance. In the early stages of a loan, a larger percentage often goes to interest. This is how lenders make their money.

However, when you consistently pay $100 extra on your car loan, you’re not just adding to your monthly contribution; you’re strategically attacking the very foundation of your debt. This additional sum bypasses the immediate interest calculation and directly targets the principal.

Direct Principal Reduction: The Foundation of Savings

Every extra dollar you pay, especially when designated correctly, goes straight to chipping away at your car loan’s principal balance. The principal is the original amount of money you borrowed. By reducing this figure more quickly, you immediately shrink the base on which future interest is calculated.

Think of it like this: your interest is determined by your outstanding principal balance. The smaller that balance becomes, the less interest accumulates over time. This creates a powerful snowball effect, where each extra payment not only reduces your principal but also sets the stage for even greater interest savings in the future.

Significant Interest Savings: Your Wallet Will Thank You

This is arguably the most compelling reason to make an extra payment. Interest is the cost of borrowing money, and it’s calculated on your remaining loan balance. When you reduce your principal ahead of schedule, you are effectively telling the lender, "I need less time to pay back this amount, so you’ll accrue less interest from me."

Based on my experience, even small, consistent payments can lead to substantial interest savings over the life of your loan. The money you save on interest can then be redirected towards other financial goals, such as building an emergency fund, investing, or tackling other debts. This strategy helps you keep more of your hard-earned money.

Accelerate Your Loan Payoff: Freedom Sooner

The direct consequence of reducing your principal and saving on interest is a significantly faster loan payoff. By consistently paying an additional $100 each month, you’re essentially making more than 12 standard payments per year. This accelerates the rate at which you pay down the debt.

What might have been a 60-month loan could potentially transform into a 48-month or even shorter loan term. Imagine the relief of being debt-free months or even years ahead of schedule. This frees up a significant portion of your monthly budget, offering incredible financial flexibility for future aspirations.

Deeper Dive: The Tangible Benefits of an Extra $100 Payment

Let’s explore the multifaceted advantages that come with committing to an extra $100 payment on your car loan. These benefits extend beyond simple numbers, impacting your overall financial health and peace of mind.

1. Significant Interest Savings Over Time

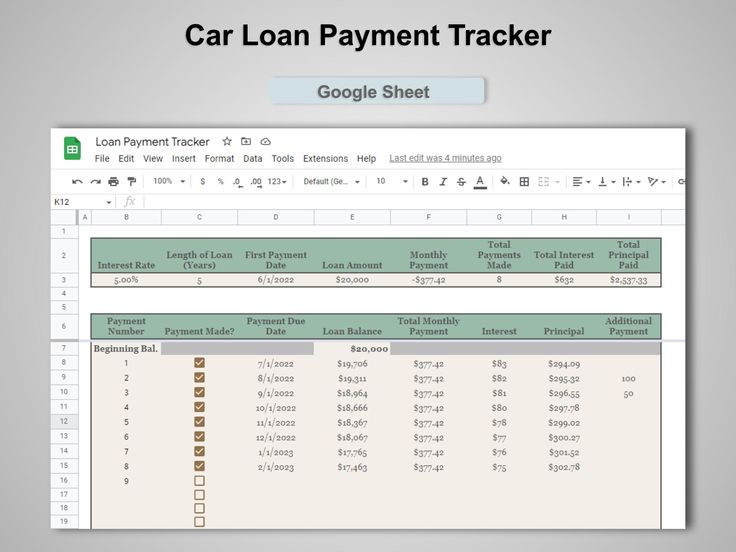

This is where the magic truly happens. To illustrate, let’s consider a common scenario:

- Original Loan: $25,000

- Interest Rate: 7%

- Loan Term: 60 months (5 years)

- Original Monthly Payment: Approximately $495.00

- Total Interest Paid (Original): Roughly $4,700

Now, let’s introduce the consistent extra $100 payment:

- New Monthly Payment: $495 + $100 = $595.00

- New Loan Term: Approximately 47 months (nearly 1 year and 1 month sooner!)

- Total Interest Paid (With Extra $100): Roughly $3,050

- Total Interest Saved: Approximately $1,650!

This example clearly demonstrates how a seemingly small, consistent effort—just $100 extra—can lead to thousands of dollars in savings. Pro tips from us: These savings are not just theoretical; they are real dollars that stay in your pocket rather than going to the lender. The earlier you start making these extra payments, the greater the cumulative savings will be due to the power of compounding in reverse.

2. Accelerate Your Loan Payoff

As shown in our example, paying an extra $100 per month can shave over a year off your 5-year car loan. This is a substantial reduction in your repayment timeline. For larger loans or longer terms, the impact can be even more dramatic.

Imagine the feeling of driving a car that is truly yours, free and clear, months or years before you anticipated. This accelerated payoff frees up a significant portion of your monthly budget much sooner. This newly available cash flow can then be reallocated to other financial priorities, whether it’s building a down payment for a house, boosting your retirement savings, or paying off other higher-interest debts.

3. Build Equity Faster

Car equity is the difference between your car’s market value and the amount you still owe on your loan. When you make extra payments, you reduce your principal balance more quickly, which directly increases your equity in the vehicle. This is particularly beneficial for several reasons.

Firstly, if you ever need to sell or trade in your car, having more equity means you’re less likely to be "upside down" on your loan (owing more than the car is worth). Secondly, higher equity provides a stronger financial position should you need to use your car as collateral for another loan in the future, though this is generally not recommended. Building equity faster means you own a larger piece of your asset sooner.

4. Financial Flexibility & Peace of Mind

Being burdened by debt can be a significant source of stress. By actively working to pay down your car loan faster, you’re taking control of your financial future. The mental relief that comes with knowing you’re on a quicker path to debt freedom is invaluable.

Once the car loan is paid off, that $495 (or whatever your original payment was) becomes available in your monthly budget. This newfound financial flexibility can be used to build a robust emergency fund, invest for your future, or simply provide a cushion for unexpected expenses. This shift from obligation to opportunity is a powerful motivator.

5. Improve Your Debt-to-Income Ratio (DTI)

Your debt-to-income (DTI) ratio is a key metric lenders use to assess your ability to manage monthly payments and repay debts. It’s calculated by dividing your total monthly debt payments by your gross monthly income. A lower DTI is generally more favorable.

While paying an extra $100 doesn’t immediately change your DTI, paying off your car loan sooner does. Once the car loan is eliminated, your total monthly debt obligations decrease significantly, thereby lowering your DTI. This improved ratio can be highly beneficial when applying for other major loans in the future, such as a mortgage, potentially allowing you to qualify for better rates or larger loan amounts. It signifies you have more disposable income relative to your debt.

Important Considerations Before You Pay Extra

While the benefits of making extra car loan payments are compelling, there are crucial steps and considerations to address before you start. Skipping these could negate your efforts or even cost you money.

1. Check for Prepayment Penalties

Common mistakes to avoid are assuming all loans are the same. Before sending in any extra cash, meticulously review your car loan agreement for any mention of "prepayment penalties." A prepayment penalty is a fee charged by some lenders if you pay off your loan earlier than scheduled. These are less common with car loans today compared to mortgages, but they do exist.

You can find this information in your original loan documents, often under sections related to early payoff or terms and conditions. If your loan does have such a penalty, calculate if the interest savings outweigh the penalty fee. In most cases, it’s still worth paying extra, but it’s essential to be aware of any potential costs. If you’re unsure, a quick call to your lender can clarify this.

2. Ensure Payments are Applied to Principal

This is perhaps the most critical step. When you send in an extra payment, you must explicitly instruct your lender to apply the additional amount directly to the principal balance. If you don’t specify, some lenders might default to applying the extra money to the next month’s payment, effectively just advancing your due date rather than reducing the principal.

To ensure proper application, contact your lender. Many have an online portal where you can designate extra payments to principal. Otherwise, call their customer service line or, for added security, send a written instruction with your payment. Always verify that your principal balance has decreased after making an extra payment.

3. Prioritize Your Emergency Fund First

Based on my experience in personal finance, a robust emergency fund should always be your top financial priority, even before aggressively paying down debt. An emergency fund provides a crucial safety net for unexpected events like job loss, medical emergencies, or unforeseen car repairs.

Before you start funneling an extra $100 into your car loan, ensure you have at least 3-6 months’ worth of living expenses saved in an easily accessible, high-yield savings account. Without this buffer, an unexpected expense could force you into higher-interest debt, undoing all your good work. Don’t deplete your savings for extra loan payments.

4. Tackle Higher-Interest Debts First

While car loan interest rates can be significant, they are often lower than other forms of debt, particularly credit card debt or some personal loans. If you have outstanding debts with interest rates significantly higher than your car loan (e.g., 18-25% on a credit card versus 7% on a car loan), it generally makes more financial sense to pay down those higher-interest debts first.

This strategy, often called the "debt avalanche" method, saves you the most money in the long run. Once those high-interest debts are cleared, you can then redirect those freed-up funds towards your car loan. For more on managing multiple debts and choosing the best strategy, check out our guide on .

5. Consider Opportunity Cost

Every dollar you spend or save has an opportunity cost – what you give up by choosing one option over another. While paying down your car loan is a wise move, consider if that extra $100 could potentially generate a higher return elsewhere.

For instance, if you have access to a retirement account with an employer match, contributing enough to get the full match is often a better "return" than the interest saved on your car loan. Similarly, if you have aggressive investment goals and your car loan rate is very low, you might weigh the potential investment returns against the guaranteed savings from early loan payoff. This is a personal decision based on your financial goals and risk tolerance.

Practical Strategies for Making Extra Payments

Committing to an extra $100 is one thing; consistently making it happen is another. Here are some practical strategies to integrate extra payments seamlessly into your financial routine.

1. Set Up Automatic Payments

The easiest way to ensure consistency is to automate your extra payments. Many lenders allow you to set up recurring additional principal payments through their online portal. This way, the money is transferred automatically each month, and you don’t have to remember to do it manually.

This "set it and forget it" approach ensures you stay on track without conscious effort. It removes the temptation to skip a payment when funds feel tight.

2. Implement Bi-Weekly Payments

This is a clever strategy that allows you to make an extra payment each year without feeling the pinch of a large lump sum. Instead of making one full car payment once a month, divide your monthly payment by two and pay that amount every two weeks.

Since there are 52 weeks in a year, you’ll end up making 26 half-payments, which equates to 13 full monthly payments annually instead of 12. Pro tips from us: This stealthy method adds an entire extra payment to your principal each year, significantly accelerating your payoff without requiring a huge change to your budget.

3. Round Up Your Payments

If a full extra $100 feels too daunting initially, start smaller by simply rounding up your monthly payment. For example, if your payment is $347, pay $350 or $360. If it’s $488, pay $500.

Even an extra $12 or $50 per month adds up over time and gets you into the habit of contributing more than the minimum. As your budget allows, you can gradually increase this rounded-up amount towards your $100 goal.

4. Utilize Windfalls and Unexpected Income

Whenever you receive unexpected money, consider dedicating a portion of it to your car loan. This could include:

- Tax refunds: Instead of spending it, put a significant chunk towards your principal.

- Work bonuses: A great way to make a large dent in your loan.

- Gifts: Birthday money or holiday gifts can be strategically used.

- Unexpected income: Even a small side gig income can be directed to the loan.

These lump-sum payments can have an even more profound impact on reducing your principal and future interest. They are "found money" that can be put to work for your financial freedom.

5. Make Budgeting Adjustments

Finding an extra $100 in your monthly budget might seem challenging, but it’s often achievable with a close look at your spending. Start by tracking your expenses for a month to identify areas where you can cut back.

Could you reduce your dining out budget by $50 and your entertainment by $50? Perhaps cancel an unused subscription, pack your lunch more often, or find a cheaper coffee routine. Small, consistent adjustments can easily free up that $100 without feeling like a major sacrifice. For practical budgeting tips and tools to help you identify these savings, consider resources like .

Conclusion

The decision to pay an extra $100 on your car loan each month is a powerful financial move that can yield impressive returns. It’s not just about an arbitrary number; it’s about leveraging the mechanics of interest and principal to your advantage. By consistently making this small additional payment, you unlock significant interest savings, accelerate your path to debt freedom, build equity faster, and gain invaluable peace of mind.

Remember to first check for prepayment penalties, always specify that extra payments go to principal, and ensure your emergency fund is robust. Once those foundations are secure, embrace strategies like automation, bi-weekly payments, or utilizing windfalls to make your extra contributions effortless. The journey to financial independence is paved with consistent, smart decisions. Start today, and watch that extra $100 transform your car loan into a testament to your financial discipline.