Unlocking the Best Altura Car Loan Rates: Your Comprehensive Guide to Auto Financing

Unlocking the Best Altura Car Loan Rates: Your Comprehensive Guide to Auto Financing Carloan.Guidemechanic.com

Embarking on the journey to purchase a new or used vehicle is an exciting prospect. However, for many, the path to vehicle ownership can feel complex, especially when it comes to securing the right financing. Understanding car loan rates is paramount, and if you’re considering Altura Credit Union, you’re on the right track to exploring competitive options.

This super comprehensive guide is designed to demystify Altura Car Loan Rates, providing you with an in-depth look at everything you need to know. We’ll delve into the factors that influence these rates, walk you through the application process, and share expert tips to help you secure the best possible terms. Our goal is to equip you with the knowledge to make informed decisions, ensuring your auto financing experience is as smooth and advantageous as possible.

Unlocking the Best Altura Car Loan Rates: Your Comprehensive Guide to Auto Financing

Why Altura Credit Union for Your Car Loan? Understanding the Credit Union Advantage

Before diving into the specifics of Altura Car Loan Rates, it’s essential to understand the institution itself. Altura Credit Union isn’t just another financial institution; it’s a member-owned, not-for-profit cooperative dedicated to serving its community. This fundamental difference often translates into tangible benefits for its members.

Unlike traditional banks that are driven by maximizing shareholder profits, credit unions like Altura focus on providing value back to their members. This often manifests in more favorable loan terms, including lower interest rates on car loans, and fewer fees. Based on my experience in the financial sector, credit unions frequently offer a more personalized and member-centric service, which can be invaluable when navigating significant financial decisions like auto financing.

Choosing a credit union means you become a part-owner, not just a customer. This unique structure fosters a sense of community and a commitment to helping members achieve their financial goals. For anyone seeking competitive Altura Car Loan Rates, this cooperative model is a significant advantage worth considering.

Decoding Altura Car Loan Rates: What Factors Influence Your Interest?

When you apply for an auto loan, the interest rate you receive isn’t pulled from thin air. Several key factors contribute to the Altura Car Loan Rates you’re offered. Understanding these elements is crucial for preparing yourself and potentially improving your loan terms.

Let’s break down the primary determinants that Altura, like other lenders, will evaluate. Knowing these can empower you to proactively address any areas that might hinder you from securing the most favorable rate.

Your Credit Score: The Cornerstone of Your Rate

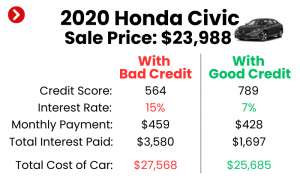

Your credit score is arguably the most critical factor influencing Altura Car Loan Rates. This three-digit number, often a FICO or VantageScore, acts as a snapshot of your financial reliability. It tells lenders how responsibly you’ve managed credit in the past.

Generally, the higher your credit score, the lower your interest rate will be. Lenders perceive borrowers with excellent credit (typically 720+) as lower risk, making them more willing to offer their most competitive Altura Car Loan Rates. Conversely, a lower credit score indicates a higher risk, leading to higher interest rates to compensate the lender for that perceived risk.

Pro tips from us: Before applying for any car loan, including one from Altura, obtain a copy of your credit report from all three major bureaus (Experian, Equifax, TransUnion). Review it for accuracy and dispute any errors. Even small improvements to your score can translate into significant savings over the life of your car loan.

Loan Term: The Length of Your Repayment Period

The loan term refers to the duration over which you agree to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72, or even 84 months). This choice significantly impacts both your monthly payment and the overall interest you’ll pay.

Shorter loan terms generally come with lower interest rates because the lender’s risk is reduced over a shorter period. While a shorter term means higher monthly payments, you’ll pay substantially less in total interest. Conversely, longer loan terms result in lower monthly payments, making the car seem more affordable upfront.

However, a common mistake to avoid is extending the loan term solely to lower monthly payments without considering the long-term cost. Longer terms usually carry higher interest rates, and you’ll end up paying much more in total interest over the life of the loan. It also means you might be "underwater" (owe more than the car is worth) for a longer period.

Down Payment: Your Upfront Investment

A down payment is the initial amount of money you pay towards the purchase of the vehicle. This upfront investment is highly beneficial when seeking attractive Altura Car Loan Rates.

Making a substantial down payment reduces the amount you need to borrow, which directly lowers your monthly payments. More importantly, it signals to Altura that you are financially committed to the purchase, reducing their lending risk. Lenders often reward this reduced risk with lower interest rates.

Based on my experience, aiming for a down payment of at least 10-20% of the vehicle’s purchase price can significantly improve your chances of securing better Altura Car Loan Rates. It also helps you build equity in the vehicle faster and reduces the likelihood of being upside down on your loan.

Vehicle Type and Age: New vs. Used

The type of vehicle you’re financing also plays a role in the Altura Car Loan Rates you might receive. New cars typically qualify for lower interest rates compared to used cars.

This is primarily because new cars hold their value better initially, are less prone to mechanical issues, and are easier for lenders to repossess and resell if necessary. Used cars, especially older models or those with high mileage, are considered higher risk due to potential depreciation and maintenance costs.

If you’re financing a used car, Altura may have specific limits on the age or mileage of the vehicle they are willing to finance. Be sure to inquire about these criteria when exploring your options.

Debt-to-Income (DTI) Ratio: Your Financial Capacity

Your debt-to-income (DTI) ratio is another crucial metric Altura will assess. It compares your total monthly debt payments to your gross monthly income. This ratio helps lenders determine your ability to comfortably take on additional debt.

A lower DTI ratio indicates that you have more disposable income to cover your loan payments, making you a more attractive borrower. Lenders typically prefer a DTI ratio of 36% or less, though some may go higher depending on other factors.

Ensuring your DTI is in a healthy range before applying for Altura Car Loan Rates can strengthen your application. This might involve paying down other debts or delaying your car purchase until your income-to-debt balance improves.

Membership Status and Relationship with Altura

As a credit union, Altura often rewards its loyal members. If you already have a checking account, savings account, or other loans with Altura and have a history of responsible financial behavior, this relationship can sometimes translate into slightly more favorable Altura Car Loan Rates or other member benefits.

It pays to be a committed member. Inquire about any special rates or discounts available to long-standing or multi-product members.

Altura Car Loan Options: New, Used, and Refinancing

Altura Credit Union offers a range of auto loan products designed to meet different member needs. Whether you’re buying a brand-new vehicle, a pre-owned gem, or looking to improve the terms of an existing loan, Altura likely has a solution.

Understanding these options can help you pinpoint the best fit for your situation and financial goals. Each loan type comes with its own nuances regarding Altura Car Loan Rates and terms.

New Car Loans

Altura’s new car loans are designed for individuals purchasing a brand-new vehicle directly from a dealership. These loans typically feature the most competitive Altura Car Loan Rates and the widest range of available loan terms, often extending up to 84 months.

Because new cars carry less risk for the lender, you’ll generally find more attractive interest rates and potentially higher loan amounts. Altura aims to make purchasing a new vehicle accessible and affordable for its members.

Used Car Loans

For those eyeing a pre-owned vehicle, Altura offers used car loans. While the Altura Car Loan Rates for used vehicles might be slightly higher than those for new cars, they remain highly competitive within the market.

Altura often has specific criteria for used car loans, such as limits on the vehicle’s age (e.g., no older than 7-10 years) and mileage. These restrictions help manage the risk associated with financing older vehicles. It’s always best to confirm these details directly with Altura before you start shopping.

Refinancing Car Loans

Based on my experience, refinancing an existing car loan can be a game-changer for many individuals. If you secured your original auto loan when your credit score was lower, interest rates were higher, or you simply weren’t aware of better options, refinancing with Altura could save you a significant amount of money.

Altura offers competitive refinancing options that could potentially lower your interest rate, reduce your monthly payment, or shorten your loan term. This is especially beneficial if your credit score has improved since you took out your initial loan, or if current market rates are lower. It’s a smart financial move to periodically check if refinancing could improve your financial situation.

The Altura Car Loan Application Process: A Step-by-Step Guide

Navigating the application process for Altura Car Loan Rates can seem daunting, but with a clear understanding of the steps involved, it becomes much simpler. Altura strives to make the process as straightforward as possible for its members.

Here’s a step-by-step guide to help you prepare and apply for your Altura car loan. Being well-prepared can expedite the approval process and reduce stress.

Step 1: Get Pre-Approved

One of the smartest moves you can make is to get pre-approved for a car loan before you even step foot in a dealership. Altura offers a pre-approval process that provides you with a conditional loan offer, including an estimated loan amount and Altura Car Loan Rates.

Pre-approval offers several significant advantages. It gives you a clear understanding of your budget, preventing you from falling in love with a car you can’t afford. More importantly, it turns you into a cash buyer at the dealership, giving you stronger negotiation power. You can focus on negotiating the vehicle price, knowing your financing is already secured.

Step 2: Gather Your Documents

Once you’re ready to apply, either for pre-approval or a full loan, you’ll need to provide certain documents. Pro tips from us: having these ready beforehand can significantly speed up the application process.

Typically, you’ll need:

- Proof of Identity: Government-issued ID (driver’s license, passport).

- Proof of Income: Pay stubs, tax returns, or bank statements to verify your employment and income.

- Proof of Residency: Utility bill or lease agreement.

- Vehicle Information (if applicable): For a specific car, you’ll need details like VIN, make, model, and mileage.

Altura’s loan officers can guide you on the exact documents required for your specific situation.

Step 3: Submit Your Application

Altura provides convenient ways to submit your car loan application. You can typically apply online through their website, visit a local Altura branch, or even apply over the phone.

The application form will ask for personal information, employment details, income, and financial history. Be thorough and accurate with your responses, as any discrepancies could delay the process.

Step 4: Await Decision & Finalize

After submitting your application, Altura will review your information, pull your credit report, and assess your eligibility. This process usually takes a relatively short amount of time, often within one business day for pre-approvals.

If approved, you’ll receive a loan offer outlining the Altura Car Loan Rates, loan term, and monthly payment. Carefully review all the terms and conditions. Once you accept, the necessary paperwork will be completed, and funds will be disbursed directly to the dealership or to you for refinancing.

Beyond the Rate: Hidden Costs and Smart Financial Strategies

While securing competitive Altura Car Loan Rates is crucial, it’s equally important to look beyond just the interest rate. There are other financial considerations and smart strategies that can significantly impact the true cost of your car loan and your overall financial well-being.

Ignoring these elements can lead to unexpected expenses or a less-than-optimal financial outcome. Our aim is to provide a holistic view of car financing.

APR vs. Interest Rate: Know the Difference

It’s common to confuse the interest rate with the Annual Percentage Rate (APR). While the interest rate is the cost of borrowing money, the APR represents the total cost of the loan, expressed as an annual percentage.

The APR includes the interest rate plus any additional fees charged by the lender, such as origination fees or application fees. When comparing Altura Car Loan Rates with offers from other lenders, always compare the APR, as it provides a more accurate picture of the total cost of borrowing.

Potential Fees to Consider

While credit unions often have fewer fees than banks, it’s wise to be aware of potential charges:

- Application Fees: Some lenders charge a small fee to process your loan application.

- Origination Fees: A fee charged for processing a new loan.

- Late Payment Fees: Penalties for missing a payment deadline.

- Prepayment Penalties: Though rare with Altura and most consumer auto loans, some lenders might charge a fee for paying off your loan early. Always confirm this.

Understanding these potential costs helps you budget accurately and avoid surprises.

Insurance: An Unavoidable Expense

Comprehensive auto insurance is a non-negotiable part of car ownership, especially when you have a loan. Lenders like Altura will require you to carry full coverage insurance (collision and comprehensive) until the loan is paid off, protecting their asset.

Beyond standard insurance, consider Gap Insurance. If your car is totaled or stolen, and you owe more on the loan than the car is worth, Gap insurance covers the difference between your insurance payout and your loan balance. This can be a wise investment, particularly if you made a small down payment or have a long loan term.

Budgeting: A Holistic Approach

Your car loan payment is just one piece of the puzzle. A truly smart financial strategy involves creating a comprehensive budget that accounts for all car-related expenses. This includes:

- Monthly loan payment

- Insurance premiums

- Fuel costs

- Maintenance and repairs (e.g., oil changes, tires)

- Registration and licensing fees

- Parking fees or tolls

For a deeper dive into budgeting strategies and how to incorporate your car loan, check out our guide on . A realistic budget ensures you can comfortably afford your car without straining your finances.

Utilizing Loan Calculators

Altura, like most financial institutions, provides online loan calculators. These tools are incredibly useful for estimating your monthly payments based on different loan amounts, interest rates (like potential Altura Car Loan Rates), and loan terms.

Use these calculators to experiment with various scenarios. See how a larger down payment or a shorter term impacts your monthly outlay and total interest paid. This hands-on approach helps you visualize the financial implications of your choices. For general financial education and tools, the Consumer Financial Protection Bureau offers excellent resources: https://www.consumerfinance.gov/consumer-tools/auto-loans/

Maximizing Your Chances for the Best Altura Car Loan Rates

Securing the most favorable Altura Car Loan Rates requires a proactive approach. It’s not just about applying; it’s about positioning yourself as the best possible borrower. Here are some actionable steps you can take to maximize your chances.

These strategies are based on industry best practices and can make a tangible difference in your overall borrowing experience and costs.

Improve Your Credit Score

This is paramount. Before you even think about applying, pull your credit reports and scores. If your score is not in the "good" to "excellent" range (generally 670+), take steps to improve it.

- Pay bills on time, every time: Payment history is the biggest factor.

- Reduce existing debt: Lowering your credit utilization ratio (amount of credit used vs. available) can boost your score.

- Avoid opening new credit accounts: Too many inquiries can temporarily lower your score.

- Keep old accounts open: A longer credit history is generally positive.

Even a 20-30 point increase can sometimes move you into a better rate tier.

Increase Your Down Payment

As discussed earlier, a larger down payment reduces the loan amount and the lender’s risk. This often translates directly into lower Altura Car Loan Rates. If possible, save aggressively to put down as much as you comfortably can.

Consider delaying your car purchase by a few months if it means accumulating a significantly larger down payment. The interest savings over the life of the loan can easily outweigh the inconvenience of waiting.

Shop Around (Even Within Altura)

While we are focusing on Altura Car Loan Rates, it’s always wise to compare offers. However, even within Altura, ask about any special promotions or member-specific rates that might not be widely advertised. Sometimes, having a direct conversation with a loan officer can uncover benefits tailored to your specific membership profile.

Don’t be afraid to ask questions and ensure you fully understand all the terms and conditions of any offer you receive.

Maintain a Low Debt-to-Income (DTI) Ratio

Keep your DTI ratio in check. If you have other outstanding debts (credit cards, student loans, personal loans), paying them down before applying for a car loan will reduce your DTI. This demonstrates to Altura that you have ample capacity to manage your new car payment without financial strain.

A healthy DTI ratio showcases your financial stability and responsibility, making you a more attractive candidate for their best rates.

Be Realistic About Your Budget

While it’s tempting to get the most car for your money, being realistic about what you can truly afford is key. Don’t stretch your budget to the absolute limit for a higher payment. Remember to factor in all the additional costs of car ownership beyond just the loan payment.

Choosing a car that comfortably fits within your budget, even if it means a slightly lower-tier model, will ultimately lead to a less stressful and more financially sustainable ownership experience.

Conclusion: Driving Away with Confidence

Navigating the world of auto financing, especially when seeking the best Altura Car Loan Rates, can seem complex. However, with the comprehensive knowledge shared in this guide, you are now equipped to approach the process with confidence and clarity. We’ve explored Altura Credit Union’s unique advantages, delved into the critical factors influencing your interest rates, outlined the various loan options, and provided a step-by-step application walkthrough.

Remember, securing an excellent car loan rate goes beyond just a number; it’s about understanding your financial health, preparing diligently, and making informed choices. By focusing on improving your credit score, making a substantial down payment, and carefully considering your loan terms, you can significantly enhance your position to receive the most favorable Altura Car Loan Rates.

Altura Credit Union stands as a strong option for competitive auto financing, offering member-focused service and advantageous rates. By leveraging the insights and expert tips provided, you can drive away in your dream car, knowing you’ve secured a loan that aligns with your financial goals and provides true value.

Ready to explore other financing avenues or deepen your understanding of automotive financial products? If you’re curious about other financing options, explore our article on . Make the informed choice, and enjoy the open road ahead!