Unlocking the Best APR Car Loan Rates: Your Definitive Guide to Smart Financing

Unlocking the Best APR Car Loan Rates: Your Definitive Guide to Smart Financing Carloan.Guidemechanic.com

Securing a new car is an exciting milestone, but the joy can quickly turn to stress if you’re not savvy about financing. One of the most critical numbers you’ll encounter during this process is the Annual Percentage Rate (APR). Understanding and optimizing your car loan APR isn’t just about saving a few dollars; it’s about making a financially sound decision that impacts your budget for years to come.

In today’s competitive market, finding the best APR car loan rates requires more than just accepting the first offer. It demands research, negotiation, and a clear understanding of what influences these rates. This comprehensive guide will equip you with the knowledge and strategies to navigate the complexities of car financing, ensuring you drive away with the best possible deal. We’ll delve deep into every facet, from deciphering your credit score to negotiating terms, so you can confidently secure favorable rates.

Unlocking the Best APR Car Loan Rates: Your Definitive Guide to Smart Financing

Understanding APR: More Than Just an Interest Rate

Before we dive into how to find the best rates, it’s crucial to grasp what APR truly represents. The Annual Percentage Rate (APR) is the total cost of borrowing money for a year, expressed as a percentage. It’s not just the interest rate; it encompasses the interest rate plus any additional fees associated with the loan, such as administrative charges, origination fees, or even certain insurance premiums rolled into the financing.

Think of the APR as the "true" cost of your loan. While a lender might quote you a low interest rate, a higher APR indicates that there are other costs being factored in. This is why comparing APRs across different loan offers is far more insightful than simply looking at interest rates alone. A lower APR means a lower overall cost for your car over the life of the loan.

Based on my experience, many car buyers mistakenly focus solely on the monthly payment or the advertised interest rate. This tunnel vision can lead to overlooking significant fees that inflate the overall cost. Always ask for the full APR when comparing loan offers to ensure you’re making an apples-to-apples comparison. It’s the single most important number to consider when evaluating affordability.

Key Factors Influencing Your Car Loan APR

Several critical elements come into play when lenders determine your car loan APR. Understanding these factors empowers you to take proactive steps to improve your chances of securing the best APR car loan rates.

Your Credit Score: The Ultimate Game Changer

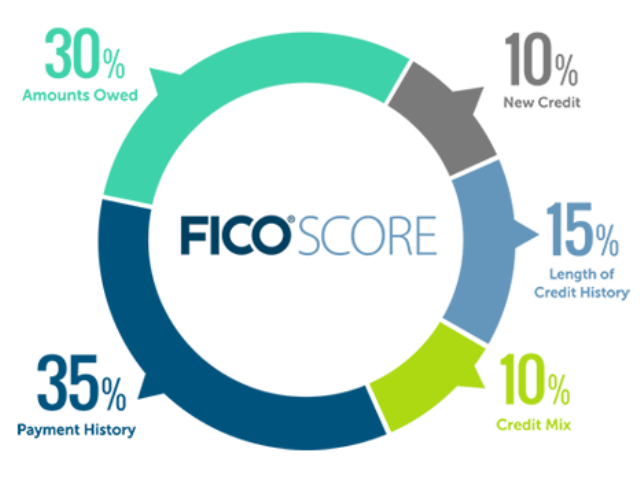

Your credit score is arguably the most significant factor lenders consider. It’s a three-digit number that reflects your creditworthiness – essentially, how reliable you are at paying back borrowed money. Lenders use this score to assess the risk of lending to you.

A higher credit score, typically above 700-720, signals lower risk to lenders. This translates directly into lower APRs. Conversely, a lower credit score indicates a higher risk, prompting lenders to offer higher APRs to compensate for that perceived risk. Common mistakes to avoid include applying for multiple loans without checking your credit first, as each hard inquiry can temporarily ding your score.

The Loan Term: Shorter Often Means Cheaper

The loan term refers to the length of time you have to repay the loan, usually expressed in months (e.g., 36, 48, 60, or 72 months). While a longer loan term means lower monthly payments, it almost always results in a higher overall APR and more total interest paid over the life of the loan.

Lenders perceive longer terms as riskier because more can happen over a longer period. Additionally, the longer you borrow money, the more interest accrues. Pro tips from us: if your budget allows, opt for the shortest loan term you can comfortably afford. This strategy will significantly reduce the total cost of your car and help you pay it off faster.

Your Down Payment: Reducing Risk, Lowering Rates

A substantial down payment works wonders for your car loan APR. When you put down a significant amount of money upfront, you reduce the amount you need to borrow. This lowers the lender’s risk exposure and can directly lead to a lower APR.

Beyond the APR, a larger down payment helps prevent you from being "upside down" on your loan, meaning you owe more than the car is worth. This is particularly relevant given how quickly new cars depreciate. Aim for at least 10-20% of the car’s purchase price as a down payment if possible.

Vehicle Type: New vs. Used Cars

Generally, new cars tend to have lower APRs compared to used cars. This is because new cars are seen as less of a risk by lenders. They have a known value, come with warranties, and their depreciation curve is somewhat predictable.

Used cars, on the other hand, vary widely in condition, mileage, and history, making them inherently riskier for lenders. As a result, used car loan APRs are often a percentage point or two higher than those for new vehicles. This doesn’t mean you shouldn’t buy a used car, but be aware of the potential difference in financing costs.

Lender Type: Explore All Your Options

Where you get your loan significantly impacts the APR you’ll receive. You have several avenues to explore, and each has its own advantages:

- Banks: Traditional banks often offer competitive rates, especially if you’re an existing customer with a good relationship.

- Credit Unions: These member-owned institutions are renowned for offering some of the lowest APRs, as their primary goal isn’t profit maximization.

- Online Lenders: A growing number of online platforms specialize in car loans, offering quick pre-approvals and competitive rates due to lower overheads.

- Dealership Financing: While convenient, dealership financing (often through captive lenders like Toyota Financial Services) may not always offer the best rates upfront. However, they sometimes have special promotions or rebates that can be attractive.

Based on my experience, shopping around and comparing offers from at least three different lender types is one of the most effective strategies for finding the best APR car loan rates. Don’t limit yourself to just one option.

Debt-to-Income Ratio (DTI): Your Financial Balance

Your debt-to-income (DTI) ratio is another metric lenders consider. It compares your total monthly debt payments to your gross monthly income. A lower DTI indicates that you have more disposable income to cover new loan payments, making you a less risky borrower. Aim for a DTI below 36% if possible, though some lenders may accept higher ratios.

The Journey to Securing the Best APR Car Loan Rates

Finding the optimal car loan APR isn’t a passive process; it’s a strategic journey that requires preparation and informed decision-making.

Step 1: Know Your Credit Score Inside and Out

Before you even start looking at cars, pull your credit reports from all three major bureaus (Experian, Equifax, TransUnion). You can do this annually for free at AnnualCreditReport.com. Review them for accuracy and dispute any errors immediately. Knowing your score gives you a realistic expectation of what APRs you might qualify for.

If your score isn’t where you want it to be, take steps to improve it. This could involve paying down existing debts, making all payments on time, and avoiding opening new lines of credit. Even a 20-30 point increase can sometimes push you into a better rate tier.

Step 2: Determine Your Realistic Budget

Don’t just think about the monthly payment; consider the total cost of ownership. This includes the car’s price, interest paid, insurance, maintenance, and fuel. Use online car loan calculators to estimate different scenarios based on various APRs and loan terms.

Understanding your budget upfront prevents you from falling in love with a car you can’t truly afford. It also helps you set a clear maximum loan amount, which is crucial for staying disciplined during negotiations.

Step 3: Get Pre-Approved Before You Shop

This is perhaps the most powerful step in your quest for the best APR car loan rates. Getting pre-approved means a lender has conditionally agreed to lend you a specific amount of money at a certain APR, based on your creditworthiness. This gives you immense leverage.

With a pre-approval in hand, you walk into the dealership as a cash buyer. You know your financing terms upfront, allowing you to negotiate the car’s price separately from the financing. If you’re looking for more details on this, check out our guide on The Ultimate Guide to Car Loan Pre-Approval. It empowers you to compare the dealership’s financing offer against a known benchmark.

Step 4: Shop Around for Lenders – Cast a Wide Net

As discussed, different lenders offer different rates. Don’t just rely on your bank or the dealership. Apply for pre-approval with several types of lenders: a local credit union, a major national bank, and at least one reputable online lender. Each application will result in a "hard inquiry" on your credit report, but credit bureaus typically treat multiple car loan inquiries within a short period (usually 14-45 days) as a single inquiry, minimizing the impact on your score.

Comparing multiple legitimate offers allows you to pick the one with the lowest APR and most favorable terms. This competitive process is key to unlocking the best possible deal.

Step 5: Negotiate Wisely – Separate Price and Financing

When you’re at the dealership, keep the negotiation process in two distinct phases: first, negotiate the vehicle’s purchase price, and second, discuss the financing. Having your pre-approval allows you to do this effectively. If the dealership can beat your pre-approved APR, great! If not, you already have a solid financing option in your back pocket.

Common mistakes to avoid here include letting the salesperson combine the price and financing discussion. They might try to distract you with low monthly payments that hide a higher APR or an extended loan term. Stay focused on the total price of the car and the APR.

Step 6: Understand the Fine Print – Read Every Word

Before signing any loan agreement, read it meticulously. Don’t rush. Ensure the APR, loan term, total loan amount, and any fees match what you were promised. Look out for any add-ons or hidden charges that might have been slipped in, such as unnecessary extended warranties or GAP insurance you didn’t request.

Pro tips from us: if anything is unclear, ask for clarification. If you feel pressured, take the documents home to review them without distraction. A reputable lender will allow you to do this.

Special Scenarios: Navigating Car Loans with Less-Than-Perfect Credit

While a high credit score is ideal for securing the best APR car loan rates, it’s not always a reality for everyone. If your credit score is less than perfect, don’t despair; you still have options, though you might face higher APRs initially.

One common mistake is to assume you won’t qualify and only apply to "buy here, pay here" dealerships. While these can be an option, they often come with extremely high APRs. Instead, consider these strategies:

- Make a Larger Down Payment: As mentioned earlier, a significant down payment reduces the risk for the lender and can help offset a lower credit score.

- Find a Co-signer: A co-signer with excellent credit can significantly improve your chances of approval and help you secure a lower APR. Be aware that the co-signer is equally responsible for the loan, so choose someone you trust and who understands the commitment.

- Consider a Secured Loan: Some lenders offer secured car loans where the car itself acts as collateral. While these might have lower APRs than unsecured options for those with poor credit, always understand the implications of default.

- Improve Your Credit First: If your need for a car isn’t immediate, dedicating a few months to improving your credit score can save you thousands in interest over the life of the loan. Focus on paying bills on time, reducing credit card balances, and avoiding new debt.

Refinancing Your Car Loan: A Path to Lower APRs

Even if you’ve already financed a car, you might not be stuck with your current APR. Refinancing your car loan involves taking out a new loan to pay off your existing one, ideally at a lower APR. This can be an excellent strategy if:

- Your Credit Score Has Improved: If you’ve diligently improved your credit score since you first bought the car, you might now qualify for a significantly lower APR.

- Market Rates Have Dropped: Interest rates fluctuate. If current car loan rates are lower than when you initially financed, refinancing could save you money.

- You Want to Change Loan Terms: You might want to shorten your loan term to pay it off faster (and save on interest) or extend it to lower your monthly payments (though this increases total interest).

- You Didn’t Get the Best Deal Initially: Perhaps you rushed into financing at the dealership without shopping around. Refinancing gives you a second chance to secure better terms.

Pro tips from us: always calculate the potential savings from refinancing. Consider any fees associated with the new loan, as these can sometimes eat into your savings. If you’re wondering if this is the right move for you, check out our article on Is Car Loan Refinancing Right For You?.

Tools and Resources for Smart Car Loan Shopping

To truly find the best APR car loan rates, leverage available tools and resources:

- Online Car Loan Calculators: Websites like Bankrate, NerdWallet, or even individual lender sites offer calculators to estimate monthly payments, total interest paid, and how different APRs impact your budget.

- Credit Monitoring Services: Many banks and credit card companies offer free credit score monitoring. Services like Credit Karma or Experian also provide insights and alerts.

- Consumer Financial Protection Bureau (CFPB): This government agency provides impartial information and resources on consumer finance, including car loans. Their website (consumerfinance.gov) is a trusted source for understanding your rights and avoiding predatory practices.

Pro Tips from Our Experts

Based on our years of experience in the finance industry, here are some invaluable tips to keep in mind throughout your car loan journey:

- Focus on the Total Cost, Not Just Monthly Payments: Lenders and dealerships often highlight low monthly payments. Always ask for the total amount you will pay over the life of the loan, including all interest and fees. This is the true measure of a good deal.

- Beware of Rolling Add-ons into Your Loan: Dealerships might offer extended warranties, GAP insurance, or other products. While some might be beneficial, ensure you understand their cost and whether it’s wise to finance them at your car loan APR. Often, paying for these separately or getting them from third parties can be cheaper.

- Don’t Be Afraid to Walk Away: If a deal doesn’t feel right, or if the APR isn’t what you expected, be prepared to walk away. There are always other cars and other lenders. Your patience can pay off with significant savings.

- Keep Excellent Documentation: Save all pre-approval letters, loan offers, and signed contracts. This documentation is crucial if any discrepancies arise later.

Conclusion: Your Path to the Best APR Car Loan Rates

Finding the best APR car loan rates might seem like a daunting task, but with the right knowledge and a strategic approach, it’s entirely achievable. Remember, a car loan is a significant financial commitment, and an informed decision can save you thousands of dollars over the life of your vehicle.

By understanding what APR truly means, knowing the factors that influence it, diligently checking your credit, getting pre-approved, and shopping around for lenders, you empower yourself to make the smartest financial choices. Don’t settle for the first offer; instead, arm yourself with information and negotiate with confidence. Your future self (and your wallet) will thank you for the effort. Start your research today, and drive away not just with your dream car, but with the best possible financing deal.