Unlocking the Best APR for Your Car Loan: A Comprehensive Guide for Good Credit Borrowers

Unlocking the Best APR for Your Car Loan: A Comprehensive Guide for Good Credit Borrowers Carloan.Guidemechanic.com

The open road, the scent of a new interior, the thrill of a fresh set of wheels – owning a car is a dream for many. When you possess good credit, that dream isn’t just within reach; it comes with the distinct advantage of securing highly favorable financing. For individuals with a strong financial history, understanding the Annual Percentage Rate (APR) for a car loan is the cornerstone of making a smart, cost-effective purchase.

This comprehensive guide is designed to empower you, the good credit borrower, with all the knowledge needed to navigate the car loan landscape. We’ll dive deep into what APR truly means, what constitutes "good credit" in a lender’s eyes, and crucially, how to leverage your excellent financial standing to lock in the absolute best car loan rates available. Our ultimate goal is to help you save thousands over the life of your loan, ensuring your new vehicle is a source of joy, not financial stress.

Unlocking the Best APR for Your Car Loan: A Comprehensive Guide for Good Credit Borrowers

What Exactly is APR and Why Does it Matter So Much?

Before we delve into specific rates for good credit borrowers, it’s vital to clarify what APR actually represents. Many people often confuse the interest rate with the APR, but there’s a crucial difference that can significantly impact the total cost of your car loan.

APR stands for Annual Percentage Rate. While the interest rate is the percentage charged by the lender for borrowing the principal amount, the APR is a broader measure. It encompasses not only the interest rate but also any additional fees or charges associated with the loan, expressed as a single annual percentage. These fees might include origination fees, documentation fees, or other processing costs.

Based on my experience, many people focus solely on the interest rate advertised, missing the bigger picture. The APR provides a more accurate, holistic view of the true cost of borrowing. A loan might have a seemingly low interest rate, but if it’s burdened with high fees, its APR could be considerably higher, meaning you’ll pay more overall. Therefore, comparing APRs across different lenders gives you a clearer, apples-to-apples comparison of loan offers.

A lower APR directly translates to less money paid over the life of the loan. Even a difference of one or two percentage points can save you hundreds, if not thousands, of dollars, especially on larger loan amounts and longer terms. This is why understanding and securing the lowest possible APR is paramount for any borrower, particularly those with good credit who are in a prime position to demand favorable terms.

Defining "Good Credit" in the Context of Car Loans

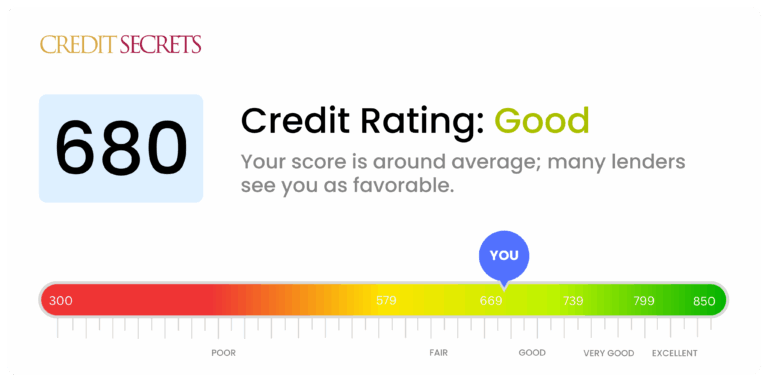

When lenders talk about "good credit," they are primarily referring to your credit score, most commonly the FICO score, along with your overall credit report. While scores vary, generally a FICO score of 670 and above is considered "good." However, for the very best car loan rates, you’re often looking at scores in the "very good" (740-799) or "excellent" (800+) ranges.

Lenders use your credit score as a quick indicator of your creditworthiness. A higher score signals that you are a responsible borrower with a history of making timely payments and managing debt effectively. This reduces the perceived risk for the lender, making them more willing to offer you lower interest rates and better loan terms.

Several key factors contribute to a strong credit score:

- Payment History: This is the most significant factor, accounting for about 35% of your FICO score. Consistently paying bills on time is crucial.

- Amounts Owed (Credit Utilization): This looks at how much credit you’re using compared to your available credit limits. Keeping your credit utilization low (ideally below 30%) is beneficial.

- Length of Credit History: A longer history of responsible credit use generally leads to a higher score.

- Credit Mix: Having a healthy mix of different types of credit (e.g., credit cards, installment loans) can positively impact your score.

- New Credit: While opening new accounts can be good, too many in a short period can temporarily lower your score.

For car loan purposes, lenders also scrutinize your debt-to-income ratio (DTI). Even with a great credit score, if your existing debt obligations are too high relative to your income, it can make lenders hesitant or lead to a slightly higher APR. They want to ensure you have sufficient disposable income to comfortably manage new car loan payments.

The Sweet Spot: Typical APRs for Good Credit Borrowers

With a solid credit profile, you enter a highly competitive market where lenders are eager to earn your business. This translates into significantly lower APRs compared to those with fair or poor credit. While market conditions and specific lender policies can cause fluctuations, good credit borrowers can generally expect to see APRs in a desirable range.

As of early 2024, someone with good credit (FICO 670-739) might typically qualify for new car loan APRs ranging from around 5% to 7%. If you fall into the "very good" (740-799) or "excellent" (800+) credit tiers, those rates can drop even further, potentially into the 3% to 5% range for new vehicles. Used car loan rates tend to be slightly higher, often by 1-2 percentage points, due to the perceived higher risk and depreciation rate of pre-owned vehicles.

Pro tips from us: Don’t just settle for the first offer you receive, even if it seems good. Your strong credit profile gives you significant leverage. Always aim to get pre-approved from several different lenders before you even step foot in a dealership. This strategy allows you to compare actual offers based on your credit and choose the best one.

Remember, these are general ranges. The specific APR you’re offered will depend on several other factors, which we will explore in detail next. Even within the "good credit" spectrum, there are nuances that can influence your final rate.

Factors That Influence Your Car Loan APR (Even with Good Credit)

While good credit is your golden ticket, it’s not the only determinant of your final APR. Several other variables come into play, and understanding them can help you optimize your loan terms even further.

Credit Score Tier within "Good"

Even if your credit is "good," there’s a difference between a FICO score of 680 and one of 780. Lenders often categorize borrowers into tiers, and moving from a "good" score to a "very good" or "excellent" score can unlock incrementally lower APRs. A higher score signals an even lower risk profile, and lenders reward this with their most competitive rates. It’s always worth checking if a few small improvements to your credit score could push you into a better tier.

Loan Term (Length of the Loan)

The length of your loan, typically expressed in months (e.g., 36, 48, 60, 72, 84 months), significantly impacts your APR. Generally, shorter loan terms come with lower APRs. This is because a shorter loan represents less risk for the lender. They get their money back faster, reducing their exposure to market fluctuations or your potential change in financial circumstances. While longer terms offer lower monthly payments, they almost always result in a higher APR and ultimately, more interest paid over the life of the loan.

New vs. Used Car

Financing a new car typically results in a lower APR than financing a used car, even for borrowers with identical good credit scores. New cars often come with manufacturer incentives, and their value depreciates more predictably than used cars. Lenders perceive new cars as less risky collateral. Used cars, on the other hand, have a more varied history, higher potential for maintenance issues, and faster depreciation, leading lenders to charge a slightly higher APR to mitigate these risks.

Down Payment Amount

Making a substantial down payment is one of the most effective ways to lower your APR. A larger down payment reduces the amount you need to borrow, which directly lowers the lender’s risk. When you have more equity in the vehicle from the start, you’re less likely to default on the loan. Lenders often reward this reduced risk with a more attractive APR. Aiming for at least 10-20% of the car’s purchase price as a down payment is a smart strategy.

Debt-to-Income Ratio (DTI)

Even with an excellent credit score, a high debt-to-income ratio can be a red flag for lenders. Your DTI compares your total monthly debt payments to your gross monthly income. If your existing debt obligations (mortgage, student loans, credit card payments) are already consuming a large portion of your income, lenders may be hesitant to offer you the lowest APR, fearing you might struggle to manage another monthly payment. A DTI below 36% is generally considered healthy, with some lenders preferring it even lower.

Co-Signer or Co-Borrower

If you’re on the lower end of the "good credit" spectrum, or if your DTI is a concern, adding a co-signer with exceptional credit can sometimes help you secure a lower APR. A co-signer essentially guarantees the loan, taking on the responsibility if you default. While it can be a useful tool, it comes with risks for the co-signer, so it should be approached with careful consideration and open communication.

Lender Type

Different types of lenders have different risk appetites and funding costs, which can influence their APR offerings. You’ll find car loans from:

- Banks: Traditional institutions, often competitive, especially if you have an existing relationship.

- Credit Unions: Member-owned, often known for offering some of the lowest APRs due to their non-profit structure.

- Online Lenders: Streamlined application processes, often competitive rates, and quick decisions.

- Dealership Financing: Convenient, but often involves the dealership acting as an intermediary, potentially marking up the rates from their lending partners.

Shopping around extensively across these different lender types is crucial to finding the best deal.

Market Conditions and Economic Climate

Broader economic factors also play a role. When the Federal Reserve raises or lowers interest rates, it impacts the cost of borrowing for lenders, which in turn affects the APRs they offer to consumers. During periods of economic uncertainty, lenders might become more conservative, leading to slightly higher rates. Conversely, a stable or growing economy might see more competitive rates.

How to Secure the Absolute Lowest APR for Your Car Loan

You have good credit, now let’s make sure you capitalize on it. Here’s a strategic roadmap to ensure you get the most competitive APR possible for your car loan.

1. Check Your Credit Score and Report Thoroughly

Your first step should always be to obtain copies of your credit report from all three major bureaus (Experian, Equifax, TransUnion) and your FICO score. Review them meticulously for any errors or inaccuracies. Even a small mistake, like a misreported late payment or an old collection account, could be artificially lowering your score. Dispute any errors immediately; correcting them could significantly boost your score and improve your loan offers. You can get free copies of your credit reports annually from AnnualCreditReport.com.

2. Shop Around Aggressively for Pre-Approvals

This is perhaps the single most impactful step. Do not rely solely on the dealership’s financing. Instead, apply for pre-approvals from multiple lenders: your bank, credit unions, and reputable online lenders. Pre-approvals give you a concrete loan offer, including the APR, before you even choose a car. This empowers you with a "cash offer" in hand, allowing you to negotiate the car’s price separately from the financing.

Common mistakes to avoid are applying to too many lenders at once without understanding the impact on your score. Fortunately, FICO models treat multiple hard inquiries for the same type of loan (like an auto loan) within a short window (typically 14-45 days) as a single inquiry. This "rate shopping window" allows you to compare multiple offers without significantly harming your credit score. Use this window wisely!

3. Consider a Shorter Loan Term (If Affordable)

While longer terms mean lower monthly payments, they almost always come with a higher APR and result in paying more interest over the loan’s life. If your budget allows, opting for a 36-month or 48-month loan instead of a 60-month or 72-month one can significantly reduce your APR. Calculate the total cost of each loan option to see the real savings.

4. Make a Substantial Down Payment

As discussed, a larger down payment reduces the principal amount borrowed and the lender’s risk. Aim for at least 10-20% of the car’s purchase price, or even more if possible. Not only will this likely lower your APR, but it will also reduce your monthly payments and help prevent you from being "upside down" on your loan (owing more than the car is worth).

5. Negotiate the Car Price First

When at the dealership, focus on negotiating the vehicle’s price before discussing financing. Dealers often try to bundle these conversations, which can make it harder to see where you might be overpaying. By having your pre-approved loan in hand, you can firmly say, "I have my financing sorted; let’s talk about the best price for this car." This separation of concerns ensures you’re getting a fair deal on both the vehicle and the loan.

6. Leverage Special Offers and Manufacturer Incentives

Manufacturers and dealerships frequently offer special financing deals, such as 0% APR for qualified buyers or significant cash rebates. While 0% APR deals are often reserved for those with excellent credit, they are worth exploring. Be aware that sometimes choosing a low APR offer might mean forfeiting a cash rebate. Compare the total savings of each option; sometimes the cash rebate is more valuable than the low APR, especially on shorter loan terms.

7. Improve Your Credit Score (If Possible)

If you’re not in a rush, taking a few months to improve your credit score can yield significant returns. Focus on paying down high-interest debt, making all payments on time, and avoiding new credit applications. Even a 20-point increase can sometimes move you into a better credit tier, unlocking lower APRs.

The Application Process: What to Expect

Once you’ve done your research and secured pre-approvals, the actual application process is relatively straightforward. You’ll typically need to provide:

- Proof of identity (driver’s license, social security number)

- Proof of income (pay stubs, tax returns, bank statements)

- Proof of residency (utility bill)

- Information about the vehicle you intend to purchase (if not already finalized)

Understanding pre-approvals vs. full approval: A pre-approval is an initial offer based on a soft credit pull and the information you provided. It’s a strong indication of what you qualify for. A full approval, however, requires a hard credit inquiry (which will temporarily dip your score slightly) and a thorough verification of all your financial details. The final APR might slightly differ from the pre-approval if your financial situation or credit report details change upon closer inspection.

It’s absolutely critical to read the fine print of any loan agreement before signing. Pay close attention to:

- The final APR

- The total loan amount

- The monthly payment

- Any fees (origination, documentation, etc.)

- Prepayment penalties (though less common for car loans, always check)

- Late payment fees

For a deeper dive into understanding pre-approvals and how they empower you, check out our guide on .

Beyond the APR: Other Important Considerations

While securing a low APR is a primary goal, a truly smart car loan decision involves looking at the bigger picture.

Total Loan Cost

Focusing solely on the monthly payment can be misleading. A very low monthly payment often comes with a longer loan term and a higher total interest paid. Always calculate the total cost of the loan (principal + total interest) to understand the true financial commitment. Your good credit puts you in a position to afford a shorter term with lower total interest.

Monthly Payments and Affordability

Even with a low APR, ensure the monthly payment fits comfortably within your budget. Use an online car loan calculator to play with different loan terms and down payment amounts. A general rule of thumb is that your total car expenses (payment, insurance, fuel, maintenance) shouldn’t exceed 10-15% of your net monthly income.

Loan Fees

While the APR incorporates most fees, it’s good to be aware of any specific charges. Some lenders may have low APRs but higher origination fees, which can negate some of the savings. Always ask for a breakdown of all fees.

Prepayment Penalties

Most auto loans do not have prepayment penalties, meaning you can pay off your loan early without incurring extra charges. This is a huge benefit if you anticipate having extra funds down the line. However, always confirm this in your loan agreement. Some lenders, particularly those dealing with subprime loans, might include them.

GAP Insurance

Guaranteed Asset Protection (GAP) insurance covers the "gap" between what you owe on your car loan and what your car is worth if it’s totaled or stolen. Cars depreciate quickly, and often, in the early years of a loan, you owe more than the car’s market value. While not directly related to APR, it’s an important consideration, especially if you’re making a small down payment or have a long loan term. You can often get GAP insurance for less from your auto insurance provider than from the dealership.

For up-to-date information on current national average car loan rates and to compare them against your offers, you can consult reputable financial sources like Experian’s State of the Automotive Finance Market Report (https://www.experian.com/automotive/automotive-finance-market-trends.html).

Common Mistakes Even Good Credit Borrowers Make

Even with the advantage of good credit, it’s easy to fall into traps that can lead to paying more than you should.

- Not Shopping Around for Loans: This is the most common and costly mistake. Assuming your current bank or the dealership offers the best rate is a guaranteed way to leave money on the table. Your good credit demands competitive offers.

- Focusing Only on Monthly Payments: Dealerships are masters at negotiating based on monthly payments. They can stretch out loan terms or add fees to lower the monthly cost, but drastically increase the total amount you pay. Always ask for the total price, including interest.

- Ignoring the Total Cost of the Loan: As mentioned, a lower monthly payment isn’t always a win. Always compare the total amount you’ll pay back, including all interest and fees, across different loan offers.

- Accepting Dealer Financing Without External Quotes: While convenient, dealership financing often involves a markup from the lender they work with. Armed with pre-approvals, you can either beat their offer or force them to match it.

- Not Understanding the Loan Terms: Don’t be afraid to ask questions. If something in the contract isn’t clear, get clarification before signing. Ignorance is not bliss when it comes to financial agreements.

From my observations, one of the biggest pitfalls is the emotional rush of buying a car. People often make rash decisions under pressure at the dealership. By doing your homework and securing pre-approvals beforehand, you remove that emotional element and approach the purchase with a clear, strategic mind.

When is a Higher APR Still "Good"? (Context Matters)

While our focus is on securing the lowest possible APR, it’s worth noting that "good" is relative to your specific situation. Sometimes, a slightly higher APR might still be a good choice for you.

For example, if you prioritize a very short loan term (e.g., 24 months) to pay off the car quickly, the APR might be marginally higher than a 36-month option, but your total interest paid could still be less due to the shorter duration. Or, if a particular vehicle is essential for your work and only available through a specific dealer with slightly less favorable financing than you’d prefer, a marginally higher APR might be an acceptable trade-off for immediate need.

The ultimate goal is not just the absolute lowest number, but the best possible APR for your specific financial goals and circumstances. Your good credit allows you to have these choices and make informed decisions, rather than being forced into less desirable terms.

If you’re also exploring options for refinancing an existing car loan, our article on offers valuable insights into lowering your current APR.

Conclusion: Your Good Credit is Your Power

Navigating the car loan market can seem daunting, but with good credit, you hold a powerful advantage. Understanding the intricacies of APR, knowing what lenders look for, and diligently shopping around are your keys to unlocking the most favorable terms available.

Remember, a low APR for your car loan with good credit isn’t just about a number; it’s about significant savings over the life of your loan, greater financial flexibility, and the peace of mind that comes from a smart financial decision. Don’t let your hard-earned good credit go to waste. Arm yourself with knowledge, compare offers, negotiate wisely, and drive away not just with a new car, but with the confidence that you secured the best deal possible. Start your research today and make your next car purchase a financially savvy one!