Unlocking the Best Auto Deals: Your Definitive Guide to MFCU Car Loan Rates

Unlocking the Best Auto Deals: Your Definitive Guide to MFCU Car Loan Rates Carloan.Guidemechanic.com

Navigating the world of car loans can feel like a complex journey, filled with jargon, varying rates, and numerous choices. For many Michigan residents, a trusted financial partner often comes to mind: Michigan First Credit Union (MFCU). But what exactly are MFCU car loan rates, and how can you ensure you’re getting the best possible deal? This comprehensive guide is designed to demystify the process, offering you an in-depth look at everything you need to know to secure your next vehicle with confidence.

As an expert blogger and professional SEO content writer who has delved deep into the financial landscape for years, I’ve seen countless individuals struggle to understand the nuances of auto financing. My mission here is to equip you with the knowledge and actionable insights necessary to approach your car loan journey prepared and empowered, specifically focusing on the competitive offerings from Michigan First Credit Union. We’ll break down the factors influencing your rate, walk through the application process, and share expert tips to save you money.

Unlocking the Best Auto Deals: Your Definitive Guide to MFCU Car Loan Rates

What Exactly is Michigan First Credit Union (MFCU)? Why Does It Matter for Your Car Loan?

Before we dive into the specifics of MFCU car loan rates, it’s crucial to understand the institution itself. Michigan First Credit Union is a member-owned financial cooperative, deeply rooted in the Michigan community. Unlike traditional banks, which are typically for-profit entities accountable to shareholders, credit unions like MFCU are structured to serve their members. This fundamental difference often translates into tangible benefits for you, the borrower.

Being member-owned means that any profits generated by the credit union are typically returned to its members in the form of lower loan rates, higher savings rates, and reduced fees. This cooperative model fosters a strong sense of community and a commitment to member well-being, which is a significant advantage when you’re seeking financing for a major purchase like a car. They prioritize building long-term relationships rather than maximizing quarterly profits.

From my experience in the financial industry, credit unions frequently offer more competitive interest rates on auto loans compared to larger commercial banks. This isn’t a universal rule, but it’s a consistent trend worth noting. When you’re comparing MFCU car loan rates against other lenders, this member-centric approach often puts them in a strong position to provide excellent value.

Why Consider MFCU for Your Next Auto Loan? Beyond Just the Rates

While competitive MFCU car loan rates are undoubtedly a major draw, there are several other compelling reasons why Michigan First Credit Union stands out as an excellent choice for your auto financing needs. Understanding these benefits can help you make a more informed decision that goes beyond just the percentage number.

Firstly, the personalized service at credit unions is often unparalleled. When you apply for an auto loan with MFCU, you’re not just another application number. Their loan officers often take the time to understand your individual financial situation, offering tailored advice and solutions. This human touch can be incredibly valuable, especially if your financial history isn’t perfectly straightforward or if you have specific questions about the loan process.

Secondly, MFCU is deeply committed to the communities it serves. This local focus means they understand the economic landscape of Michigan and are often more flexible and empathetic to the needs of local residents. This community-first approach can translate into more accessible loan products and a greater willingness to work with members to achieve their financial goals, including car ownership.

Finally, credit unions are known for their transparency. You’ll typically find that the terms and conditions of an MFCU auto loan are clear and straightforward, without hidden fees or complex clauses designed to confuse. This transparency builds trust, which is essential when committing to a long-term financial obligation. It ensures you fully understand what you’re signing up for.

Deciphering MFCU Car Loan Rates: What Factors Influence Your Cost?

Understanding the actual number you’ll pay for your MFCU car loan requires a deeper look into the various factors that lenders consider. It’s not just a single, static rate; rather, it’s a dynamic figure tailored to your unique financial profile and the specifics of the loan itself. Knowing these elements empowers you to proactively improve your standing and potentially secure a better rate.

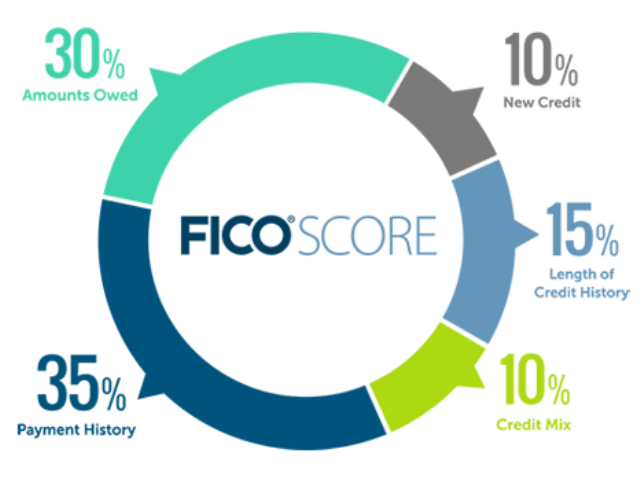

The most significant factor influencing your MFCU car loan rates is undoubtedly your credit score. Lenders use this three-digit number as a primary indicator of your creditworthiness and your likelihood of repaying the loan. A higher credit score signals a lower risk to the lender, which typically translates into lower interest rates. Conversely, a lower score will often result in a higher rate to compensate the lender for the increased risk.

Another critical element is the loan term, which is the length of time you have to repay the loan. Shorter loan terms, such as 36 or 48 months, generally come with lower interest rates because the lender’s money is tied up for a shorter period. Longer terms, like 60 or 72 months, spread the payments out, making them lower monthly, but usually come with higher interest rates, increasing the total cost of the loan over time.

The amount of your down payment also plays a crucial role. A larger down payment reduces the amount you need to borrow, which lowers the lender’s risk exposure. This reduced risk can often translate into more favorable MFCU car loan rates. Furthermore, a significant down payment can help you avoid being "upside down" on your loan, where you owe more than the car is worth.

Finally, the type of vehicle you’re purchasing (new vs. used), its age, and even your relationship with Michigan First Credit Union can subtly influence your rate. New cars often qualify for slightly lower rates due to their higher resale value and perceived reliability. Building a strong banking relationship with MFCU, by having other accounts or loans with them, can sometimes give you an edge, potentially qualifying you for loyalty discounts or more flexible terms.

APR vs. Interest Rate: A Crucial Distinction for Your MFCU Auto Loan

When you’re comparing MFCU car loan rates, you’ll often encounter two terms: "interest rate" and "Annual Percentage Rate" (APR). While they sound similar, understanding the difference is absolutely vital for accurately assessing the true cost of your loan. Failing to grasp this distinction is a common mistake that can lead to unexpected expenses.

The interest rate is simply the percentage charged by the lender for borrowing the principal amount. It represents the cost of borrowing money, expressed as a percentage of the loan amount, typically on an annual basis. This is the core cost of the loan itself, without factoring in additional fees.

The Annual Percentage Rate (APR), however, provides a more comprehensive picture of the total cost of borrowing. The APR includes the interest rate plus any additional fees associated with the loan, such as origination fees, processing fees, or closing costs. Essentially, it annualizes all the costs of the loan into a single percentage, making it the most accurate figure to use when comparing loan offers from different lenders.

Pro tips from us: Always focus on the APR when evaluating MFCU car loan rates or any other loan offers. A loan might advertise a very attractive interest rate, but if it comes with substantial fees, its APR could be significantly higher than another loan with a slightly higher interest rate but no additional fees. The APR is your best friend for true cost comparison.

How to Find Current MFCU Car Loan Rates: Your First Steps

Once you understand the factors at play, your next step is to actually find out what MFCU car loan rates are currently available. Michigan First Credit Union makes this process relatively straightforward, offering several convenient avenues for prospective borrowers.

The easiest and most common way to get an initial idea of MFCU’s rates is by visiting their official website. Most credit unions and banks prominently display their current auto loan rates, often segmented by loan term (e.g., 36 months, 60 months, 72 months) and sometimes by vehicle type (new vs. used). While these posted rates are generally the lowest available for highly qualified borrowers, they provide an excellent benchmark. Look for a dedicated "Loans" or "Auto Loans" section on their site.

Another effective method is to directly contact an MFCU branch or their call center. Speaking with a loan officer allows you to discuss your specific situation and get more personalized information. They can often provide a more accurate estimate of the rate you might qualify for, especially if you provide some basic information about your credit history and the vehicle you’re considering. This personal interaction can also clarify any questions you might have.

MFCU, like many modern financial institutions, also offers online car loan calculators. These tools are incredibly useful for estimating your potential monthly payments based on a given loan amount, interest rate, and term. While the interest rate entered into these calculators is usually an estimate, they help you visualize the financial impact of different loan scenarios. You can plug in various rates and terms to see what fits your budget.

The MFCU Car Loan Application Process: A Step-by-Step Walkthrough

Applying for an auto loan with Michigan First Credit Union is a structured process designed to be as efficient as possible. Understanding each step can help you prepare thoroughly, ensuring a smooth and timely approval. Based on my experience, being prepared significantly reduces stress and potential delays.

Step 1: Gather Your Documents. Before you even begin the application, collect all necessary documentation. This typically includes:

- Proof of identity (Driver’s License or State ID).

- Proof of income (recent pay stubs, W-2s, or tax returns if self-employed).

- Proof of residence (utility bill, lease agreement).

- Information about the vehicle you intend to purchase (if known, including VIN, make, model, year, and mileage).

- Social Security Number.

Step 2: Check Your Credit Score. Before applying, obtain a copy of your credit report from one of the three major bureaus (Equifax, Experian, TransUnion) and check your score. This allows you to identify any errors and gives you an idea of the MFCU car loan rates you might qualify for. You can typically get a free report annually.

Step 3: Choose Your Application Method. MFCU offers flexibility. You can apply:

- Online: This is often the quickest method, allowing you to complete the application from the comfort of your home.

- In-person: Visit an MFCU branch to speak directly with a loan officer. This is ideal if you prefer face-to-face interaction or have complex questions.

- By Phone: You can also call their loan department to apply over the phone.

Step 4: Complete the Application. Fill out the application accurately and completely. Provide all requested financial and personal information. Be honest; any discrepancies can delay or even jeopardize your approval. This is where your gathered documents come in handy.

Step 5: Await a Decision. Once you submit your application, MFCU will review your financial information and credit history. This process can range from minutes for highly qualified online applicants to a few business days for more complex cases. They will then inform you of their decision, which could be an approval, a request for more information, a counter-offer, or a denial.

Step 6: Review and Finalize. If approved, carefully review the loan offer, paying close attention to the APR, loan term, and any specific conditions. If you’re satisfied, sign the necessary documents to finalize your MFCU auto loan.

Pro Tips to Secure the Best MFCU Car Loan Rates

While your credit score is a major determinant, there are several proactive steps you can take to improve your chances of securing the most favorable MFCU car loan rates. These strategies can collectively save you hundreds, if not thousands, of dollars over the life of your loan.

-

Boost Your Credit Score: This is paramount. Pay all your bills on time, keep your credit utilization low, and avoid opening new lines of credit just before applying for a car loan. Even small improvements to your score can lead to a noticeable difference in the interest rate offered. Consider tools like Experian Boost if you have eligible accounts.

-

Make a Larger Down Payment: As discussed, a substantial down payment reduces the loan amount and the lender’s risk. Aim for at least 10-20% of the vehicle’s purchase price if possible. This not only lowers your monthly payments but can also qualify you for better rates.

-

Opt for a Shorter Loan Term: While longer terms mean lower monthly payments, they almost always come with higher interest rates and a greater total cost. If your budget allows, choose the shortest loan term you can comfortably afford. This strategy minimizes the amount of interest you pay over time.

-

Consider a Co-signer (Strategically): If your credit isn’t stellar, a co-signer with excellent credit can significantly improve your chances of approval and help you secure lower MFCU car loan rates. However, be aware that the co-signer is equally responsible for the debt, so choose someone you trust implicitly and who understands the commitment.

-

Pre-qualification vs. Pre-approval: Understand the difference. Pre-qualification gives you an estimate of what you might qualify for, without a hard credit inquiry. Pre-approval involves a more thorough check (hard inquiry) but gives you a firm offer for a specific loan amount and rate. Getting pre-approved with MFCU before car shopping gives you strong negotiating power at the dealership, as you know your financing is secured.

-

Maintain a Relationship with MFCU: If you’re already a long-standing member with other accounts in good standing at Michigan First Credit Union, you might be eligible for member-exclusive benefits or slightly better rates. Loyalty often pays off.

Refinancing Your Existing Car Loan with MFCU: A Path to Savings

Many people overlook the opportunity to refinance their existing car loan, potentially missing out on significant savings. If you currently have an auto loan with another lender, or if your financial situation has improved since you first took out your loan, exploring refinancing options with Michigan First Credit Union could be a very smart move.

When does refinancing make sense?

- Your Credit Score Has Improved: If your credit score has significantly increased since you purchased your car, you might qualify for much lower MFCU car loan rates now.

- Interest Rates Have Dropped: The overall market interest rates might have decreased, making it a good time to secure a lower rate.

- You Want a Lower Monthly Payment: Refinancing to a longer term can reduce your monthly outlay, though it might increase the total interest paid.

- You Want to Pay Off Your Loan Faster: Conversely, refinancing to a shorter term with lower rates can help you accelerate debt repayment.

- You Want to Remove a Co-signer: If a co-signer was needed initially, improved credit might allow you to refinance the loan solely in your name.

The process for refinancing with MFCU is very similar to applying for a new car loan. You’ll submit an application, provide financial documentation, and they will evaluate your creditworthiness. If approved, MFCU will pay off your old loan, and you’ll begin making payments to them, ideally at a more favorable rate. Based on my experience, many individuals find substantial savings by simply taking the time to explore this option.

Common Mistakes to Avoid When Applying for a Car Loan

Even with the best intentions, borrowers often make common missteps that can negatively impact their car loan experience and overall cost. Being aware of these pitfalls can help you navigate the process more effectively when seeking MFCU car loan rates.

-

Not Checking Your Credit Score: As mentioned, your credit score is paramount. Neglecting to review it before applying means you’re going into the process blind, unaware of potential issues or your likely rate tier. Always pull your credit report and score first.

-

Applying to Too Many Lenders at Once: While it’s good to shop around, submitting numerous loan applications within a short period can negatively impact your credit score. Each "hard inquiry" can cause a slight dip. Group your applications within a 14-45 day window, as FICO scoring models often treat multiple auto loan inquiries within that period as a single inquiry.

-

Focusing Only on the Monthly Payment: Dealerships often try to negotiate based solely on what you can afford monthly. While important, this can lead to longer loan terms and higher total interest paid. Always consider the total cost of the loan, including the purchase price and all interest and fees.

-

Ignoring the Total Cost of Ownership: Beyond the loan, remember to factor in insurance, maintenance, fuel, and potential depreciation. A low monthly car payment doesn’t mean it’s an affordable car if other costs are prohibitive.

-

Not Reading the Fine Print: Always read your loan agreement thoroughly before signing. Understand all terms, conditions, penalties for late payments, and any pre-payment clauses. If anything is unclear, ask questions until you fully understand.

MFCU Auto Loan Options Beyond Traditional Purchases

Michigan First Credit Union understands that vehicle ownership comes in many forms. Their auto loan offerings often extend beyond just financing a brand-new car from a dealership. Knowing these additional options can open up more possibilities for you.

For instance, MFCU provides competitive rates for used car loans. Buying a used vehicle can be a smart financial decision, and credit unions typically offer attractive financing even for older models, within certain age and mileage limits. Always check their specific criteria for used vehicle financing.

Another common scenario is a lease buyout. If you’re currently leasing a vehicle and decide you want to purchase it at the end of your lease term, MFCU can help finance that buyout. This can often be a more cost-effective solution than returning the leased vehicle and starting a new loan or lease.

Depending on their specific offerings, MFCU might also provide loans for other types of vehicles, such as motorcycles, recreational vehicles (RVs), boats, or even ATVs. If you’re looking to finance any kind of personal transport, it’s always worth checking with your credit union first.

The Power of Being Pre-Approved with MFCU

One of the most powerful strategies you can employ when car shopping is to secure a pre-approval for an auto loan from MFCU before you step foot in a dealership. This single step can dramatically shift the negotiating power in your favor.

When you walk into a dealership with an MFCU pre-approval letter in hand, you’re no longer just a potential buyer; you’re a cash buyer, in the eyes of the dealer. You already know how much you can borrow and at what interest rate. This allows you to focus solely on negotiating the purchase price of the vehicle, rather than getting entangled in discussions about financing terms, which can often be used to obscure the true cost.

Based on my experience, dealers often try to maximize their profit by adjusting both the vehicle price and the financing terms. By separating these two negotiations, you simplify the process and protect yourself from unfavorable loan rates or inflated prices. You can simply present your MFCU pre-approval and challenge the dealer to beat it. More often than not, they will try, potentially saving you even more money.

Conclusion: Driving Away with Confidence with MFCU Car Loan Rates

Securing the right car loan is a significant financial decision, and understanding all the moving parts, especially when it comes to MFCU car loan rates, is key to making an informed choice. Michigan First Credit Union, with its member-centric approach, often provides highly competitive options and personalized service that can make your car buying experience smoother and more affordable.

By thoroughly researching current rates, understanding the factors that influence your eligibility, preparing your documentation, and employing smart strategies like improving your credit and getting pre-approved, you put yourself in the best possible position. Remember to always focus on the APR, read the fine print, and consider the total cost of your loan, not just the monthly payment.

Our goal throughout this comprehensive guide has been to empower you with the expertise needed to navigate the auto loan landscape confidently. Armed with this knowledge, you are well-equipped to unlock the best possible MFCU car loan rates and drive away in your new vehicle with peace of mind.