Unlocking the Best Auto Loan: How Car Loan Interest Rates Are Shaped by Your Credit Score

Unlocking the Best Auto Loan: How Car Loan Interest Rates Are Shaped by Your Credit Score Carloan.Guidemechanic.com

The dream of a new car often comes with the practical reality of financing. For most of us, a car loan is a necessary step to turn that dream into a driveway reality. However, the cost of that loan—specifically, the interest rate you pay—can vary dramatically, adding thousands of dollars to the total price of your vehicle.

What many prospective car owners don’t fully realize is the profound impact their credit score has on these interest rates. It’s not just a number; it’s a powerful financial indicator that lenders scrutinize to assess your reliability as a borrower. A higher score signals less risk, often translating into significantly lower interest rates and more favorable loan terms.

Unlocking the Best Auto Loan: How Car Loan Interest Rates Are Shaped by Your Credit Score

In this comprehensive guide, we’ll delve deep into the intricate relationship between your credit score and car loan interest rates. We’ll explore what makes up your credit score, how different credit tiers affect your borrowing costs, and crucially, what actionable steps you can take to improve your score and secure the most advantageous financing possible. Our goal is to empower you with the knowledge to navigate the auto loan landscape confidently and save a substantial amount of money in the process.

What Exactly is a Credit Score, and Why Does it Dictate Your Auto Loan Rate?

Before we dissect the impact, it’s essential to understand what a credit score is and why it holds so much sway with lenders. Think of your credit score as a financial report card, a three-digit number that summarizes your entire credit history and predicts your likelihood of repaying a debt.

Lenders use this score as a quick, standardized way to assess the risk associated with lending you money. A higher score indicates a lower risk of default, making you a more attractive borrower. Conversely, a lower score suggests a higher risk, prompting lenders to either deny your application or offer less favorable terms, often with a much higher interest rate, to compensate for that perceived risk.

The Core Function of Your Credit Score

Your credit score provides a snapshot of your financial responsibility. It tells potential lenders how consistently you’ve paid your bills on time, how much debt you currently carry, and how long you’ve been managing credit. For a car loan, this risk assessment is paramount.

Lenders want assurance that you’ll make your monthly payments reliably. Based on my experience, a strong credit score effectively communicates that you are a responsible borrower, making them more willing to offer you their best rates. This directly translates into lower monthly payments and a reduced total cost for your vehicle over the life of the loan.

FICO vs. VantageScore: Understanding the Key Players

While many people refer to "their credit score" generically, there are actually several different scoring models in use. The two most prominent are FICO Score and VantageScore. Both aim to do the same thing – predict creditworthiness – but they use slightly different methodologies and weighting of factors.

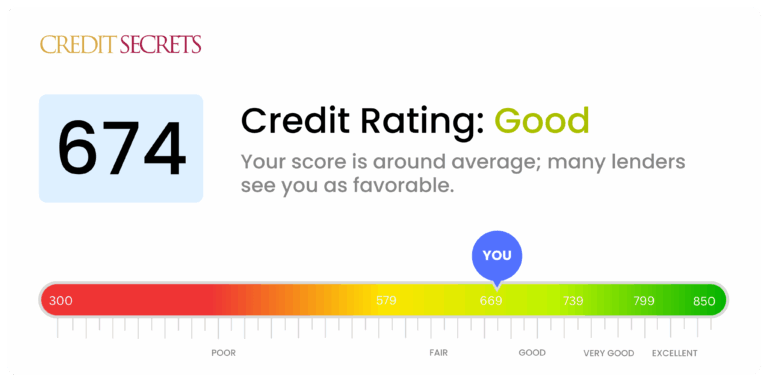

The FICO Score is arguably the most widely used by lenders, including those offering auto loans. Its range typically runs from 300 to 850. VantageScore also uses a similar range, though its initial versions had different scales. Understanding that FICO is often the score lenders rely on can help you focus your credit monitoring efforts.

The Building Blocks of Your Score

Your credit score isn’t a random number; it’s meticulously calculated based on several key factors derived from your credit reports. Understanding these components is the first step toward improving your score.

Firstly, payment history is by far the most crucial factor, accounting for approximately 35% of your FICO score. Consistently making payments on time demonstrates reliability, while late payments can significantly damage your score. Secondly, credit utilization (the amount of credit you’re using compared to your total available credit) makes up about 30%. Keeping this ratio low, ideally under 30%, signals that you’re not over-reliant on credit.

Thirdly, the length of your credit history (15%) considers how long your credit accounts have been open and how long it’s been since you used them. Older, well-managed accounts are generally better. Fourthly, new credit (10%) looks at how many new accounts you’ve recently opened and how many hard inquiries appear on your report. Too many new accounts in a short period can be seen as risky. Finally, your credit mix (10%) reflects the variety of credit accounts you have, such as credit cards, installment loans (like car loans), and mortgages. A healthy mix shows you can manage different types of credit responsibly. Pro tips from us include regularly monitoring your credit reports from all three major bureaus (Equifax, Experian, TransUnion) to ensure accuracy and identify any potential issues.

The Credit Score Spectrum: How Each Tier Impacts Your Car Loan Interest Rate

The 300-850 credit score range isn’t monolithic; it’s divided into several tiers, each associated with a different level of risk and, consequently, different interest rates. Understanding where you fall on this spectrum is critical for setting realistic expectations and planning your car purchase.

Excellent Credit (780-850): The VIP Lane

Borrowers with excellent credit scores are considered the crème de la crème by lenders. These individuals typically have an impeccable payment history, very low credit utilization, a long history of responsible credit management, and a diverse credit mix. They are seen as virtually no risk.

For these borrowers, auto loan interest rates are the lowest possible, often referred to as "prime rates." You can expect to see highly competitive offers, frequently in the single-digit range. Lenders actively compete for these customers, offering the best terms to attract them. For example, you might qualify for rates as low as 3-5%, or even promotional rates below that. This translates into significantly lower monthly payments and substantial savings over the loan’s term.

Very Good Credit (740-779): Strong & Reliable

Individuals with very good credit scores are also highly valued by lenders. They demonstrate a strong track record of financial responsibility, with perhaps only minor or very old blemishes on their credit history. They are perceived as low risk and reliable borrowers.

Interest rates for this tier are very competitive, though they might be slightly higher than those offered to borrowers with excellent credit. You’ll still secure favorable terms and likely have multiple lenders vying for your business. Expect rates in the range of, for instance, 4-6%. While not the absolute lowest, these rates are still excellent and represent a solid financial position.

Good Credit (670-739): The Solid Foundation

The "good" credit range is where a large portion of the population falls. Borrowers in this category have a solid foundation of responsible credit behavior, but they might have a slightly higher credit utilization, a more recent late payment (but not a pattern), or a shorter credit history compared to those in higher tiers.

Lenders view these borrowers as acceptable risks. You will likely qualify for a car loan, and the interest rates will be favorable, though not the rock-bottom rates seen in the excellent or very good tiers. Expect rates to be in the range of 6-9%, for example. While these rates are perfectly manageable, there’s still room for improvement to unlock even better terms.

Fair Credit (580-669): Room for Improvement

This credit tier indicates that while you generally pay your bills, there might be some issues in your credit history. This could include higher credit utilization, a few recent late payments, or a limited credit history that makes it harder for lenders to assess your risk confidently.

For borrowers with fair credit, interest rates start to climb noticeably. Lenders perceive a moderate risk and will charge more to compensate. You’ll still be able to get a car loan, but the terms will be less appealing. For example, rates could be in the 10-15% range, or even higher. This significantly increases the total cost of the car, making it crucial to consider improving your score before buying, if possible.

Poor Credit (300-579): High-Risk Territory

Borrowers with poor credit scores present a high risk to lenders. This tier is typically characterized by significant delinquencies, collections, charge-offs, bankruptcies, or a very limited credit history ("thin file"). Lenders are very cautious about extending credit.

Securing an auto loan with poor credit is challenging, and if approved, the interest rates will be very high. You’ll likely be directed to subprime lenders who specialize in high-risk loans. Based on my experience, these rates can make a car significantly more expensive over the loan term, sometimes doubling or tripling the amount of interest paid compared to someone with excellent credit. For instance, rates can easily range from 15-25%+, or even higher in some cases. Often, these loans may require a co-signer or a substantial down payment to mitigate the lender’s risk.

Beyond the Score: Other Critical Factors Influencing Your Auto Loan Rate

While your credit score is undeniably the most significant determinant of your car loan interest rate, it’s not the only factor. Several other elements play a crucial role in shaping the final offer you receive. Understanding these can help you optimize your overall financial position before applying.

Debt-to-Income (DTI) Ratio

Your Debt-to-Income (DTI) ratio is a measure of how much of your gross monthly income goes towards paying your debts. Lenders calculate it by dividing your total monthly debt payments by your gross monthly income. For example, if your monthly debts (mortgage/rent, credit cards, student loans, etc.) are $1,500 and your gross income is $4,000, your DTI is 37.5%.

Lenders use DTI to assess your ability to take on additional debt, like a car loan. A high DTI indicates that you might be stretched thin financially, making you a higher risk even with a decent credit score. Most lenders prefer a DTI under 43%, with lower being better, as it suggests you have more disposable income to comfortably make your car payments.

Loan Term Length

The length of your loan, often expressed in months (e.g., 36, 48, 60, 72, or even 84 months), also significantly impacts your interest rate. Generally, shorter loan terms come with lower interest rates, while longer terms carry higher rates.

This is because a shorter term means the lender gets their money back sooner, reducing their risk over time. While a longer term might offer a lower monthly payment, making the car seem more affordable, you’ll end up paying significantly more in total interest over the life of the loan. It’s a common trap to focus solely on the monthly payment without considering the total cost of borrowing.

Down Payment Amount

The amount of money you put down upfront on your vehicle directly affects the amount you need to borrow. A larger down payment reduces the principal loan amount, which in turn reduces the lender’s risk. This is because your "Loan-to-Value" (LTV) ratio decreases.

A lower LTV ratio, meaning you owe less than the car is worth, makes you a more attractive borrower. Lenders are more likely to offer better interest rates when they know their investment is well-protected. A substantial down payment also reduces your monthly payments and the total interest you’ll pay over the loan’s duration.

Vehicle Type and Age

Believe it or not, the type and age of the vehicle you’re buying can also influence your interest rate. New cars often come with lower interest rates, partly due to manufacturer incentives and partly because they hold their value better initially, making them less risky collateral for the lender.

Used cars, on the other hand, tend to have slightly higher interest rates. This is because they depreciate faster, have a shorter lifespan, and may pose a higher mechanical risk. Lenders see them as riskier collateral. Additionally, older, less reliable vehicle models might also attract higher rates due to concerns about their long-term value and your ability to maintain them.

Market Conditions and Lender Competition

Finally, broader economic factors and the competitive landscape among lenders play a role. When the Federal Reserve raises its benchmark interest rate, it typically causes interest rates across the board, including auto loan rates, to increase. Conversely, a period of low interest rates can lead to more favorable loan offers.

Furthermore, the level of competition among banks, credit unions, and online lenders can impact rates. In a highly competitive market, lenders might lower their rates to attract more customers. This is why shopping around for multiple offers is always a smart strategy, regardless of your credit score.

Strategic Moves to Boost Your Credit Score for Superior Car Loan Rates

If your credit score isn’t where you want it to be, don’t despair. There are concrete steps you can take to improve it, potentially saving you thousands on your next car loan. This isn’t an overnight fix, but consistent effort will yield significant results.

Prioritize On-Time Payments

This is the single most impactful action you can take to improve your credit score. Your payment history accounts for a huge portion of your score. Every late payment can drag your score down, and conversely, a consistent record of on-time payments builds a strong foundation.

Set up automatic payments for all your bills, or at the very least, calendar reminders a few days before each due date. If you’re struggling to make a payment, contact your creditor immediately; they might be willing to work with you. Establishing a long history of timely payments will steadily elevate your credit score.

Keep Credit Utilization Low

As we discussed, credit utilization is the amount of credit you’re using compared to your total available credit. Aim to keep this ratio below 30% across all your credit cards and lines of credit. Ideally, strive for under 10% for the best impact.

To achieve this, pay down credit card balances as much as possible. If you have multiple cards, focus on the one with the highest balance or the highest interest rate first. Another strategy is to request a credit limit increase on an existing card, but only if you trust yourself not to increase your spending along with it. A higher limit with the same balance automatically lowers your utilization.

Address and Dispute Credit Report Errors

Errors on your credit report can unfairly drag down your score. These could include incorrect late payments, accounts that aren’t yours, or inaccurate balances. It’s crucial to regularly check your credit reports for mistakes.

You are entitled to a free copy of your credit report from each of the three major bureaus (Equifax, Experian, and TransUnion) once every 12 months via AnnualCreditReport.com. Review them carefully. If you find an error, dispute it directly with the credit bureau and the creditor. For a detailed guide on how to dispute errors, you can refer to trusted resources like Experian’s guide: https://www.experian.com/blogs/ask-experian/credit-education/report-disputes/. Correcting errors can provide a quick boost to your score.

Avoid Unnecessary New Credit Applications

Each time you apply for new credit, a "hard inquiry" is placed on your credit report, which can temporarily ding your score by a few points. While applying for a car loan is necessary, avoid opening new credit cards or other lines of credit in the months leading up to your car purchase.

However, there’s a specific exception for auto loans: credit scoring models understand that people shop around. Multiple hard inquiries for the same type of loan (like a car loan) within a short period (typically 14-45 days, depending on the scoring model) are usually counted as a single inquiry. This "rate shopping" window allows you to compare offers without multiple penalties.

Consider a Secured Credit Card (If Credit is Very Low)

If your credit score is very low or you have little to no credit history, a secured credit card can be an excellent tool for building credit. With a secured card, you put down a cash deposit that typically becomes your credit limit. This deposit acts as collateral, making it less risky for the issuer.

By using the secured card responsibly – making small purchases and paying them off in full and on time every month – you’ll establish a positive payment history. This activity is reported to the credit bureaus, helping to build or rebuild your credit score over time. For more information on how these cards work, you might find our article, "," particularly helpful.

Navigating the Car Loan Application Process Like a Pro

Even with a great credit score, the car loan application process can feel daunting. However, being prepared and proactive can significantly improve your chances of securing the best possible rates and terms. Don’t just show up at the dealership and hope for the best.

Get Pre-Approved First

One of the most powerful strategies for car buyers is to get pre-approved for a loan before stepping foot on a dealership lot. Pre-approval means a lender has reviewed your credit and financial situation and offered you a specific loan amount at a particular interest rate, contingent on the final vehicle choice.

The benefits are numerous. Firstly, you’ll know exactly what you can afford, preventing you from falling in love with a car outside your budget. Secondly, a pre-approval gives you leverage during negotiations with the dealer. You’ll have a benchmark interest rate, and the dealer will know you’re serious and have financing secured, encouraging them to try and beat your existing offer. Remember, pre-approvals usually involve a soft inquiry initially, which doesn’t affect your score.

Shop Around for the Best Offers

Never settle for the first loan offer you receive, especially not the one presented by the dealership’s finance department without comparison. While dealerships can sometimes offer competitive rates, they are also looking to maximize their profit.

Shop around with multiple lenders: your bank, credit unions (which often have excellent rates), and various online auto loan providers. Apply for pre-approval with at least 2-3 different institutions. As mentioned earlier, multiple inquiries for an auto loan within a specific window (typically 14-45 days) will count as a single inquiry on your credit report, so you won’t harm your score by comparing offers. Common mistakes to avoid are settling for the first offer you receive without comparing it to others. This simple step can save you hundreds, if not thousands, of dollars over the life of your loan.

Read the Fine Print Carefully

Once you have a loan offer, it’s absolutely critical to read the fine print before signing anything. Don’t just focus on the monthly payment. Look at the total cost of the loan, including all fees and charges.

Pay close attention to the Annual Percentage Rate (APR), which includes the interest rate plus certain fees, giving you a more accurate representation of the true cost of borrowing. Check for any prepayment penalties, which could cost you money if you decide to pay off the loan early. Ensure there are no hidden fees or clauses you don’t understand. If something is unclear, ask for clarification. Don’t feel pressured to sign until you are completely comfortable and informed.

Pro Tips from Us: Securing Your Dream Car with the Best Financing

As expert bloggers and professional SEO content writers who’ve explored countless financial topics, we’ve gathered some insights that can help you navigate the car buying and loan process even more effectively. These "pro tips" go beyond the basics to give you an edge.

Tip 1: Negotiate Everything

Many people think negotiation only applies to the car’s price. However, everything is negotiable when buying a car. This includes the trade-in value of your old vehicle, any add-ons or warranties, and critically, the terms of your loan.

Even if you have a pre-approval, use it as a bargaining chip. Tell the dealer what rate you’ve been offered and challenge them to beat it. They often have access to various lenders and might be able to find an even better deal to secure your business. A few points off your interest rate can save you a significant amount.

Tip 2: Consider a Co-Signer (For Lower Scores)

If your credit score is in the fair or poor range, securing a favorable interest rate on your own can be tough. In such cases, considering a co-signer with excellent credit can be a game-changer. A co-signer essentially guarantees the loan, promising to make payments if you default.

This significantly reduces the lender’s risk, often allowing you to qualify for much lower interest rates than you would on your own. However, it’s crucial to understand the implications for both parties. The loan will appear on the co-signer’s credit report, and any missed payments will negatively affect their score as well. Choose a co-signer who fully understands and trusts this responsibility.

Tip 3: The Power of a Down Payment

We’ve touched on the down payment, but it deserves emphasis. While saving for a substantial down payment might delay your car purchase slightly, the financial benefits are immense. A larger down payment reduces the total amount you need to borrow, which directly translates into less interest paid over the life of the loan.

It also gives you immediate equity in the vehicle, reducing the risk of being "upside down" (owing more than the car is worth). Furthermore, lenders often look more favorably on borrowers who put down a significant amount, signaling their commitment and reducing their perceived risk. Aim for at least 20% if possible, especially for new cars, to minimize depreciation impact.

Tip 4: Refinancing as a Future Option

Your credit score isn’t static. If you have to settle for a higher interest rate now due to a less-than-perfect credit score, all is not lost. You can work diligently to improve your credit score over the next 6-12 months by making all your payments on time and reducing other debts.

Once your score has improved significantly, you can explore refinancing your car loan. Refinancing involves taking out a new loan, often with a different lender, to pay off your existing car loan. If your credit has improved, you’ll likely qualify for a lower interest rate, which will reduce your monthly payments and the total interest paid. This strategy can be a smart move for long-term savings. For a deeper dive into this, you might find our article, "," particularly insightful.

The Long-Term Impact of Your Car Loan on Your Financial Health

Securing a car loan is more than just getting the keys to a new vehicle; it’s a significant financial commitment with long-lasting implications for your overall financial health. Understanding these long-term effects can help you make more informed decisions.

Building Positive Credit History

A car loan, when managed responsibly, can be an excellent tool for building a strong credit history. Making consistent, on-time payments each month demonstrates your reliability to lenders and positively contributes to your payment history, which is the largest factor in your credit score.

As you steadily pay down your loan, your credit score can gradually improve, opening doors to better rates on future loans, mortgages, and even credit cards. This positive credit behavior becomes a valuable asset, proving your ability to manage