Unlocking the Best Car Loan Deals with a 756 Credit Score: Your Comprehensive Guide

Unlocking the Best Car Loan Deals with a 756 Credit Score: Your Comprehensive Guide Carloan.Guidemechanic.com

Having a 756 credit score is like holding a golden ticket in the world of auto financing. This excellent score places you among the most creditworthy borrowers, opening doors to the most favorable car loan terms available. It signifies a strong financial history, consistent payment behavior, and a low risk profile in the eyes of lenders.

This comprehensive guide is designed to empower you. We’ll explore exactly what a 756 credit score means for your car loan prospects, the incredible advantages it brings, and how to strategically leverage it to secure the absolute best deal on your next vehicle. Our goal is to provide you with in-depth knowledge, turning your excellent credit into significant savings.

Unlocking the Best Car Loan Deals with a 756 Credit Score: Your Comprehensive Guide

Understanding Your 756 Credit Score: A Golden Ticket to Savings

A 756 credit score falls squarely into the "Very Good" to "Excellent" range, depending on the specific scoring model (like FICO or VantageScore). This is a phenomenal score that demonstrates to lenders you are a highly reliable borrower. It’s a testament to your responsible financial management over time.

Lenders view a 756 credit score as a strong indicator of low risk. They perceive you as someone who consistently pays bills on time, manages debt wisely, and is unlikely to default on a loan. This perception is crucial because it directly influences the terms and rates they are willing to offer you. In essence, you’ve earned their trust.

Based on my experience in the financial industry, a score like 756 truly puts you in a prime position. Most lenders reserve their lowest interest rates and most flexible terms for individuals within this credit tier. You’re not just approved; you’re courted by financial institutions eager to have your business.

The Unbeatable Advantages of a 756 Credit Score for Car Loans

The benefits of securing a car loan with a 756 credit score are substantial and far-reaching. They extend beyond just getting approved; they translate into tangible savings and greater financial flexibility throughout the life of your loan. Let’s delve into these key advantages.

Lower Interest Rates: Significant Savings Over Time

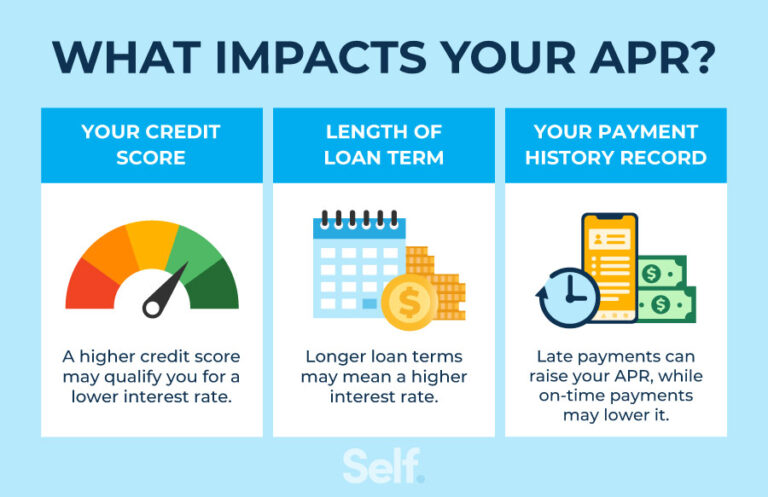

The most significant advantage of a 756 credit score for a car loan is undoubtedly access to the lowest available interest rates. Lenders offer their best rates to borrowers with excellent credit because the risk of default is minimal. Even a slight reduction in your Annual Percentage Rate (APR) can save you thousands of dollars over a typical 5-7 year car loan term.

Consider this: on a $30,000 car loan over 60 months, a borrower with a 756 score might qualify for an APR of 3.5%, while someone with an average score (say, 650) might get 7.5%. This difference alone could mean paying nearly $4,000 more in interest for the average borrower. Your excellent credit directly puts more money back into your pocket.

These lower rates not only reduce your overall loan cost but also make your monthly payments more manageable. This financial breathing room can be incredibly valuable, freeing up funds for other expenses or savings goals. It’s a direct reward for your diligent credit management.

Better Loan Terms: Flexibility and Control

Beyond just interest rates, your 756 credit score opens the door to more favorable loan terms in general. Lenders are more willing to be flexible with repayment schedules and loan durations for low-risk borrowers. This means you have more control over structuring a car loan that perfectly fits your budget and financial goals.

You might be offered longer repayment periods without a significant increase in the interest rate, leading to lower monthly payments. Alternatively, if you prefer to pay off your loan faster, you can opt for shorter terms, knowing you’ll still receive a competitive rate. This flexibility is a powerful tool in your car buying journey.

This level of control allows you to tailor the loan to your specific needs, rather than being limited to restrictive options. It’s about optimizing your cash flow while still benefiting from a great overall deal.

Wider Range of Lenders: More Options, More Competition

With a 756 credit score, virtually every type of lender will be eager to offer you an auto loan. This includes major national banks, local credit unions, online lenders, and even manufacturer financing programs. This broad access to the lending market is a huge advantage.

Having a wider pool of lenders means you can shop around more effectively and pit lenders against each other. Each institution will be vying for your business, which drives down rates and improves terms. You’re not limited to just one or two options; you have the power to choose the offer that best suits you.

Pro tips from us: Always get pre-approved by at least 3-4 different lenders before stepping foot in a dealership. This strategy provides you with multiple competitive offers, giving you leverage in negotiations. It ensures you have a benchmark to compare against any financing options the dealership might present.

Less Scrutiny and Easier Approval: Streamlined Process

An excellent credit score significantly streamlines the car loan approval process. Lenders require less documentation and often make quicker decisions for borrowers with strong credit. This means less hassle, fewer hoops to jump through, and a faster path to driving your new vehicle.

You’ll likely experience a more straightforward application, potentially needing fewer supporting documents than someone with a lower score. The confidence lenders have in your credit history translates into a smoother, more efficient experience. This can be a huge relief, especially if you’re in a hurry to purchase a car.

The reduced scrutiny also means less stress during what can often be a complex process. You can focus more on choosing the right car and less on proving your creditworthiness.

Negotiating Power: Leverage Your Score

Your 756 credit score isn’t just for getting a good loan; it’s a powerful negotiating tool for the car itself. When a dealership knows you have pre-approved financing at a low rate, they understand they can’t inflate prices or interest rates on you. This knowledge gives you significant leverage.

You can confidently negotiate the price of the vehicle, knowing that your financing is already secured and favorable. Dealers are often more willing to make concessions on the car’s price or offer better trade-in values to a buyer who represents a "sure thing" for a sale.

Use your excellent credit as an asset in all aspects of the transaction. Don’t be afraid to walk away if the deal isn’t right, as you know other lenders and dealerships will be eager for your business.

Lower Insurance Premiums (Indirect Benefit): An Added Bonus

While not directly tied to the car loan itself, an excellent credit score can indirectly lead to lower car insurance premiums. Many insurance companies use credit-based insurance scores as one factor in determining rates, especially in states where it’s permitted. A higher credit score often correlates with lower risk, which can translate into cheaper insurance.

This means your responsible credit management continues to pay dividends even after you’ve secured your car loan. It’s another layer of savings that further reduces the overall cost of vehicle ownership. This is a benefit often overlooked but significantly impactful.

Navigating the Car Loan Process with Your Excellent Credit

Even with a 756 credit score, approaching the car loan process strategically is essential to maximize your advantages. Don’t just assume the best deals will fall into your lap; proactive steps are required to ensure you secure optimal terms.

Pre-Approval is Key: Your Financial Blueprint

Getting pre-approved for a car loan before you even step onto a dealership lot is arguably the most crucial step. Pre-approval provides you with a concrete understanding of how much you can borrow, at what interest rate, and for what term. This knowledge empowers you immensely.

It transforms you into a cash buyer in the eyes of the dealership, allowing you to focus solely on negotiating the car’s price. You won’t be swayed by attractive "monthly payment" figures that might hide an unfavorable interest rate or an excessively long loan term. You’ll know your financial limits and options upfront.

To get pre-approved, you’ll typically need to provide personal information, employment details, and income verification. Lenders will perform a "soft inquiry" (which doesn’t affect your score) to give you initial offers, and a "hard inquiry" (which might slightly dip your score temporarily) once you formally apply. However, multiple auto loan inquiries within a short period (usually 14-45 days) are often grouped as a single inquiry by credit bureaus, minimizing impact.

Shop Around for Lenders: Don’t Settle

With your 756 credit score, you have access to a vast array of lenders. Don’t make the mistake of accepting the first offer you receive, even if it seems good. Take the time to compare offers from various sources: national banks, local credit unions, and reputable online lenders.

Credit unions, in particular, are often known for offering highly competitive auto loan rates to their members. Online lenders can also provide streamlined application processes and attractive rates. Cast a wide net to ensure you’re seeing the full spectrum of options available to someone with your credit standing.

This comparison shopping allows you to identify the absolute best interest rate and terms. Even a quarter-point difference in APR can save you hundreds of dollars over the life of the loan.

Understand the Loan Offer: Read the Fine Print

Before signing any documents, thoroughly understand every aspect of the car loan offer. Focus on the Annual Percentage Rate (APR), which includes the interest rate plus any fees. This is the true cost of borrowing. Also, confirm the total loan amount, the number of payments, and the total cost of the loan over its term.

Be wary of any hidden fees, mandatory add-ons, or prepayment penalties. A 756 credit score should allow you to avoid such unfavorable terms. If a lender tries to include these, it might be a sign to look elsewhere.

Common mistakes to avoid are rushing through the paperwork or relying solely on what the salesperson tells you. Always take the time to read every line of the contract yourself and ask questions until you fully understand everything.

Down Payment Strategy: Even with Great Credit, It Helps

While your excellent credit might qualify you for a no-down-payment loan, making a significant down payment is almost always a wise financial move. A larger down payment reduces the amount you need to borrow, which in turn lowers your monthly payments and the total interest you’ll pay over the loan’s life.

It also helps prevent you from being "upside down" on your loan, where you owe more than the car is worth, especially in the early years of ownership when depreciation is highest. Aim for at least 10-20% of the car’s purchase price as a down payment if possible.

Choosing the Right Vehicle: Beyond the Loan

Even with the best car loan terms, choosing the right vehicle that fits your budget and needs is paramount. Don’t let the excitement of a great loan push you into buying a car you can’t truly afford or don’t truly need. Your 756 credit score gives you financial flexibility, but discipline is still key.

Consider factors like fuel efficiency, insurance costs, maintenance expenses, and depreciation when making your vehicle choice. The best car loan in the world won’t make an unsuitable car a good long-term financial decision.

Maximizing Your 756 Score: Strategies for the Best Deal

Your excellent credit score is a powerful asset, but knowing how to wield it effectively is what truly secures you the best car loan deal. There are specific strategies you can employ to ensure you’re getting maximum value.

Know Your FICO Score: The Industry Standard

While you know you have a 756 score, it’s beneficial to know which specific FICO Auto Score lenders are likely to use. FICO offers industry-specific scores, and an auto lender will typically pull a FICO Auto Score 2, 4, 5, or 8. These scores place more emphasis on your past auto loan payment history.

Knowing this specific score, or at least understanding that auto lenders use a slightly different lens, helps you set realistic expectations. While your general 756 score is fantastic, understanding the nuances of auto-specific scores can give you an edge in conversations with lenders. Many credit card companies or financial apps offer free access to one of your FICO scores.

Negotiate Beyond the Interest Rate: Look at the Whole Package

Your excellent credit should empower you to negotiate every aspect of the deal, not just the interest rate. Once you’ve secured a great APR through pre-approval, turn your attention to other potential costs.

This includes the car’s purchase price, trade-in value (if applicable), and any additional fees like documentation fees or extended warranty costs. Don’t let a great interest rate distract you from an inflated vehicle price. Always ensure you’re getting a fair market price for the car itself.

Be particularly vigilant about dealership add-ons, such as paint protection, fabric guards, or unnecessary extended warranties. These often have high markups and can significantly inflate the total cost of your loan. Your 756 credit score means you don’t need these "extras" to qualify for favorable terms.

Consider Refinancing: A Future Option

Even if you secure a fantastic rate with your 756 credit score, market conditions can change. Interest rates fluctuate, and new lender incentives emerge. Keep an eye on the market; if rates drop significantly after you’ve purchased your car, you might be able to refinance your loan for an even better deal.

Refinancing means taking out a new loan to pay off your existing one, ideally at a lower interest rate or with more favorable terms. This is particularly effective if your credit score has improved even further since your initial purchase, or if general interest rates have declined. Your excellent credit makes you a prime candidate for refinancing anytime.

Leverage Manufacturer Incentives: Double the Savings

Many auto manufacturers offer special financing deals, cash-back incentives, or low APR promotions (sometimes even 0% APR) to well-qualified buyers. With your 756 credit score, you are precisely the "well-qualified buyer" they are targeting.

Combine your excellent credit with these manufacturer incentives for maximum savings. Sometimes, you might have to choose between a low APR offer and a cash-back rebate; calculate which option provides the most overall savings for your specific situation. Don’t miss out on these extra layers of discounts that your credit score enables.

The Power of a Co-signer (Rarely Needed, but an Option)

While highly unlikely with a 756 credit score, a co-signer could theoretically be considered if you faced an unusual situation, such as having a very short credit history despite perfect payments, or if you were aiming for an exceptionally large loan that pushed your debt-to-income ratio. However, for most car loans, your 756 score will make a co-signer completely unnecessary. It’s good to know the option exists for those with less established credit, but your score bypasses this need.

For further reading on how different financial factors impact your auto loan, consider exploring our article on Understanding APR vs. Interest Rate: What You Need to Know for Your Car Loan.

Potential Pitfalls Even with a 756 Credit Score

Even with excellent credit, it’s crucial to remain vigilant during the car buying process. Your high score doesn’t make you immune to common dealership tactics or financial missteps. Knowing these pitfalls can help you navigate the process more effectively.

Dealership Markups: The Hidden Costs

While you’ll qualify for the best rates, some dealerships might attempt to mark up the interest rate they present to you, even if their lender is offering a lower "buy rate." They do this to make an additional profit on the financing. This is why having your own pre-approval in hand is so critical.

By knowing your pre-approved rate, you can immediately identify if a dealership is attempting to add extra margin. Don’t be afraid to challenge their offer or walk away if they can’t match or beat your external pre-approval. Your 756 credit score gives you that power.

Add-ons and Extras: Inflating the Loan

Dealerships are notorious for pushing high-profit add-ons like extended warranties, gap insurance (which can be worthwhile, but often cheaper elsewhere), paint protection packages, and VIN etching. While some of these might have value, they are often heavily marked up and can significantly inflate your total loan amount.

With your excellent credit, you won’t need these extras to qualify for a good rate. Carefully evaluate each add-on and only agree to those you genuinely need and can’t obtain more affordably elsewhere. Remember, every dollar added to the purchase price increases your loan amount and the interest you’ll pay.

Long Loan Terms: More Interest Over Time

While a 756 credit score can qualify you for very long loan terms (72 or even 84 months) at a low interest rate, consider the total cost. Longer terms mean lower monthly payments, but you’ll pay significantly more in total interest over the life of the loan.

For example, a $30,000 loan at 3.5% over 60 months costs about $2,700 in interest. The same loan over 84 months could cost closer to $3,900 in interest, an extra $1,200. Evaluate if the lower monthly payment is worth the additional interest and the longer period you’ll be making payments.

Impulse Buying: Financial Discipline is Key

Even with access to great financing, buying a car on impulse can lead to regret. Take your time, research vehicles thoroughly, and stick to your budget. Your 756 credit score is a tool for smart financial decisions, not an excuse for overspending.

Avoid falling in love with a car that’s beyond your true affordability, even if the monthly payments seem manageable due to a long loan term. Always consider the total cost of ownership, including insurance, maintenance, and fuel.

Not Reading the Fine Print: Understand Everything

As mentioned before, always read every single line of your loan agreement and purchase contract. Ensure that the interest rate, terms, and total price match what you agreed upon. Look for discrepancies, hidden fees, or clauses that might be disadvantageous.

For a deeper understanding of consumer rights and auto loan practices, we recommend consulting resources like the Consumer Financial Protection Bureau (CFPB) at www.consumerfinance.gov.

Maintaining and Further Improving Your Excellent Credit

Your 756 credit score is a fantastic achievement, and it’s important to maintain it, or even improve it further. Consistent good financial habits are the bedrock of strong credit.

On-Time Payments: The Foundation

The single most impactful factor in your credit score is your payment history. Continue to make all your loan and credit card payments on time, every time. A single late payment can ding your excellent score.

Set up automatic payments or reminders to ensure you never miss a due date. This diligent habit will keep your 756 score robust and healthy.

Keep Credit Utilization Low: Manage Your Debt Wisely

Credit utilization refers to the amount of revolving credit you’re using compared to your total available credit. Keep this percentage low, ideally below 30%, but even lower is better for excellent scores. This shows lenders you’re not reliant on credit.

Even if you have a lot of available credit, avoid maxing out your credit cards. This signals responsible credit management and contributes positively to your score.

Monitor Your Credit Report: Catch Errors Early

Regularly check your credit reports from all three major bureaus (Equifax, Experian, TransUnion) for inaccuracies or fraudulent activity. You can get a free report from each bureau once a year at AnnualCreditReport.com. Errors can negatively impact your score without your knowledge.

Promptly dispute any incorrect information you find. Protecting your credit report is an active process that ensures your 756 score accurately reflects your financial responsibility.

Avoid Opening Too Many New Accounts: Strategic Credit Growth

While it’s good to have a mix of credit, opening too many new accounts in a short period can temporarily lower your credit score. Each new application results in a hard inquiry, and too many can make you appear risky to lenders.

Be strategic about when and why you apply for new credit. Only open accounts you genuinely need, and space out applications over time.

For more insights into safeguarding your financial future, check out our article on The Importance of Credit Monitoring for Long-Term Financial Health.

Conclusion: Drive Away with Confidence

Your 756 credit score is a testament to your excellent financial management, and it positions you perfectly to secure the best possible car loan. This guide has shown you that having such a score isn’t just about getting approved; it’s about unlocking lower interest rates, more flexible terms, and significant savings throughout your loan’s lifespan.

By understanding the advantages, diligently shopping for lenders, leveraging your pre-approval, and being a savvy negotiator, you can transform your 756 credit score into a powerful tool for your next vehicle purchase. Remember to stay vigilant against common pitfalls and maintain your excellent credit habits for continued financial success.

Drive away with confidence, knowing you’ve secured a fantastic car loan deal that truly reflects your outstanding creditworthiness. Your 756 credit score car loan is not just a transaction; it’s a smart financial move that sets you up for success.