Unlocking the Best Car Loan Finance Rates: Your Ultimate Guide to Saving Thousands

Unlocking the Best Car Loan Finance Rates: Your Ultimate Guide to Saving Thousands Carloan.Guidemechanic.com

Navigating the world of car financing can feel like deciphering a complex puzzle. For many, a car purchase represents one of the largest financial commitments outside of a home. And at the heart of this commitment lies the car loan finance rate – a seemingly small percentage that can dramatically impact the total cost of your vehicle over its lifetime.

Understanding and securing the best car loan finance rates isn’t just about saving a few dollars; it’s about making an informed financial decision that empowers you. This comprehensive guide will equip you with the knowledge and strategies to confidently approach car financing, ensuring you get the most favorable terms available. Our goal is to transform you from a passive borrower into an empowered negotiator, ready to save thousands.

Unlocking the Best Car Loan Finance Rates: Your Ultimate Guide to Saving Thousands

Understanding Car Loan Finance Rates: The Core Concepts

Before diving into strategies, it’s crucial to grasp the fundamental concepts behind car loan finance rates. These are the building blocks of any auto loan agreement.

What is an APR (Annual Percentage Rate)?

When you see a car loan offer, you’ll primarily encounter the Annual Percentage Rate (APR). This isn’t just the interest rate; it’s a more holistic measure of the cost of borrowing money. The APR includes the interest rate plus any additional fees associated with the loan, such as administrative charges or origination fees, expressed as a yearly percentage.

Think of it this way: the interest rate is what the lender charges you to borrow the principal amount. The APR, however, gives you the true, total cost of that borrowing on an annual basis. It’s the most accurate figure for comparing different loan offers.

Fixed vs. Variable Rates: A Critical Distinction

Car loans typically come with either fixed or variable interest rates, and understanding the difference is vital for your financial planning.

A fixed-rate loan means your interest rate, and consequently your monthly payment, remains the same for the entire duration of the loan. This offers predictability and stability, making budgeting easier. You’ll always know exactly what to expect, regardless of market fluctuations.

In contrast, a variable-rate loan features an interest rate that can change over time. These rates are usually tied to a benchmark index, like the prime rate. If the benchmark rate goes up, your interest rate and monthly payments will also increase. While variable rates might start lower than fixed rates, they carry the risk of higher payments in the future, making them less common for standard auto loans but worth being aware of.

Based on my experience, for the vast majority of car buyers, a fixed-rate loan provides invaluable peace of mind. The stability it offers allows for clear financial planning without the stress of potential payment increases.

Factors That Influence Your Car Loan Rates

Your car loan rate isn’t arbitrarily assigned; it’s the result of several key factors that lenders assess to determine their risk. Understanding these elements puts you in a better position to influence the outcome.

Your Credit Score: The Ultimate Predictor

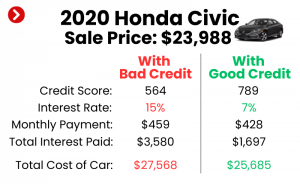

Without a doubt, your credit score is the single most influential factor in determining the car loan rates you’ll be offered. Lenders use this three-digit number to gauge your creditworthiness – essentially, how likely you are to repay the loan. A higher credit score signals a lower risk to lenders, which typically translates into lower interest rates.

Credit scores, like FICO or VantageScore, range from approximately 300 to 850. Generally, scores above 720 are considered excellent, while those below 600 may indicate a higher risk, leading to significantly higher rates. A difference of just 50 points in your score can mean hundreds, if not thousands, of dollars in interest over the life of the loan.

Loan Term: The Length of Your Commitment

The loan term refers to the duration over which you agree to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72, or even 84 months). The loan term has a direct impact on both your monthly payment and the total interest paid.

A longer loan term will result in lower monthly payments, which can make a more expensive car seem affordable. However, a longer term almost always means you’ll pay significantly more in total interest over the life of the loan. Conversely, a shorter loan term leads to higher monthly payments but substantially reduces the total interest paid. It’s a critical balance between affordability now and total cost later.

Down Payment: Reducing Your Risk and Loan Amount

A down payment is the initial amount of money you pay upfront for the car, reducing the total amount you need to borrow. Making a substantial down payment signals financial stability to lenders, and it directly reduces their risk. A larger down payment means you’re financing less, which often results in a lower interest rate offer.

Furthermore, a larger down payment helps you avoid being "upside down" on your loan, a situation where you owe more than the car is worth. This is particularly important as cars depreciate rapidly in their early years.

Debt-to-Income Ratio (DTI): Your Financial Balance

Your debt-to-income (DTI) ratio is a percentage that compares your total monthly debt payments to your gross monthly income. Lenders use this ratio to assess your ability to manage monthly payments and take on additional debt. A lower DTI ratio indicates that you have more disposable income available to cover your loan payments, making you a less risky borrower.

Typically, lenders prefer a DTI ratio below 36%, though this can vary. A high DTI might lead to a higher interest rate or even a loan denial, as it suggests you might be overextended financially.

Vehicle Type and Age: Asset Value and Risk

The type and age of the vehicle you’re financing also play a role in determining your interest rate. New cars generally command lower interest rates than used cars. This is because new cars are seen as less risky collateral; they have a predictable value and are less likely to require immediate costly repairs.

Used cars, on the other hand, often come with slightly higher rates due to factors like their unknown maintenance history and faster depreciation. Lenders perceive a greater risk when financing an older vehicle, which can translate into a higher APR for the borrower.

Lender Type: Where You Borrow Matters

The institution from which you obtain your loan can also influence the rates offered. Different lenders have different business models and risk appetites.

Banks, credit unions, online lenders, and dealership finance departments each have their own advantages and disadvantages. We’ll delve deeper into these options later, but understanding that the source of your loan can impact the rate is a key piece of the puzzle.

Strategies to Secure the Best Car Loan Finance Rates

Now that you understand the factors at play, let’s explore actionable strategies to help you secure the most competitive car loan finance rates possible. These steps require a bit of preparation but can lead to significant savings.

1. Improve Your Credit Score Before You Apply

Since your credit score is paramount, taking steps to improve it before applying for a car loan is a highly effective strategy.

Pro tips from us: Before you even start shopping for a car, pull your credit report from all three major bureaus (Equifax, Experian, TransUnion) via AnnualCreditReport.com. Review it meticulously for any errors or discrepancies. Dispute any inaccuracies immediately, as even small errors can negatively impact your score.

Beyond corrections, focus on paying all your bills on time, every time. Payment history is the biggest factor in your score. Try to reduce existing credit card debt to lower your credit utilization ratio, which is the amount of credit you’re using compared to your total available credit. Keeping this ratio below 30% is generally recommended. For a deeper dive into improving your credit score, check out our guide on . (Internal Link Placeholder)

2. Save for a Larger Down Payment

While it might seem challenging, saving for a larger down payment is one of the most straightforward ways to lower your car loan finance rate and overall cost. A larger down payment reduces the amount you need to borrow, which directly translates to less interest paid over time.

Additionally, lenders view borrowers with significant down payments as less risky, often rewarding them with more favorable interest rates. Aim for at least 20% of the vehicle’s purchase price, if possible. This not only lowers your monthly payments but also helps prevent you from owing more than the car is worth early in its life.

3. Shop Around for Lenders (Pre-approval is Key)

This is perhaps the most crucial strategy for securing the best rates. Never settle for the first loan offer you receive, especially not one from a dealership without comparison. Shopping around for pre-approval from multiple lenders empowers you with leverage.

Apply to banks, credit unions, and online lenders before you even step foot on a dealership lot. Most lenders will conduct a "soft" credit inquiry for initial pre-qualification, which doesn’t affect your score. Once you’re ready for a firm offer, multiple "hard" inquiries within a short period (typically 14-45 days, depending on the scoring model) are usually grouped as a single inquiry, minimizing the impact on your credit score. This allows you to compare actual offers side-by-side.

4. Consider a Shorter Loan Term (If Affordable)

While a longer loan term offers lower monthly payments, it invariably leads to paying significantly more in total interest. If your budget allows, opting for the shortest loan term you can comfortably afford will save you a substantial amount of money over the life of the loan.

For example, a 48-month loan will have higher monthly payments than a 72-month loan for the same car, but your total interest paid could be thousands less. It’s a balance between your current cash flow and your long-term financial goals.

5. Understand Add-ons and Extras

Common mistakes to avoid are accepting unnecessary add-ons and extras during the financing process. Dealerships often offer extended warranties, GAP insurance, paint protection, or undercoating. While some of these might be valuable, others are overpriced or redundant.

When these items are rolled into your car loan, they increase your principal balance, meaning you’ll pay interest on them for the entire loan term. Scrutinize every additional charge and only accept what you truly need and understand. Often, these items can be purchased separately for less, or they might not be necessary at all.

6. Negotiate the Price of the Car First

A common pitfall is to combine the car price negotiation with the loan negotiation. Savvy car buyers separate these two processes. First, negotiate the lowest possible purchase price for the vehicle itself. Once you’ve agreed on a price, then shift your focus to financing.

By separating these steps, you prevent confusion and ensure you’re getting the best deal on both fronts. If you’ve already secured pre-approval at a great rate, you can then use that as leverage to either beat or match the dealership’s financing offer.

Where to Find the Best Car Loan Rates

Knowing where to look is just as important as knowing what to look for. Various types of lenders offer car loans, each with its own set of advantages.

Credit Unions: Member-Focused Benefits

Credit unions are often lauded for offering some of the most competitive car loan rates. As not-for-profit financial institutions, they are owned by their members and tend to pass on savings in the form of lower interest rates and fewer fees.

Membership is typically required, but joining is often straightforward, sometimes just requiring a small donation or affiliation with a specific community or employer. Their member-centric approach often means more flexible terms and personalized service.

Online Lenders: Speed and Convenience

The rise of online lenders has revolutionized car financing, offering unparalleled convenience and often very competitive rates. These platforms allow you to compare offers from multiple lenders in minutes, often with quick approval processes.

Many online lenders specialize in auto loans, streamlining the application and approval process entirely digitally. They can be particularly useful for those who prefer to handle the entire car-buying journey from home, providing pre-approval before ever visiting a dealership.

Banks: Traditional and Accessible

Traditional banks remain a popular choice for car loans. They offer a wide range of loan products and are generally accessible, especially if you already have an existing relationship with them. While their rates can vary, established banks often provide competitive options for customers with good to excellent credit.

It’s always worth checking with your current bank, as they might offer loyalty discounts or special rates to existing account holders.

Dealership Financing: Convenience with Caution

Dealerships offer in-house financing, often through partnerships with various banks and financial institutions. This can be incredibly convenient, allowing you to complete the entire purchase and financing process in one place. Dealerships may also offer promotional rates, especially on new vehicles, to move inventory.

However, from my professional vantage point, while dealership financing offers convenience, it’s almost always beneficial to arrive with a pre-approved offer in hand. This allows you to compare the dealership’s offer against a known benchmark, ensuring you’re getting the best deal rather than simply accepting their first proposal.

The Application Process: What to Expect

Once you’ve done your research and identified potential lenders, the application process itself is relatively straightforward. However, knowing what to expect can ease any anxiety.

Documents You’ll Need

Lenders will typically require several documents to verify your identity, income, and residence. Be prepared to provide:

- Government-issued ID: Such as a driver’s license or passport.

- Proof of Income: Pay stubs, W-2s, or tax returns (especially for self-employed individuals).

- Proof of Residence: Utility bills or a lease agreement.

- Social Security Number: For credit checks.

- Vehicle Information: If you’ve already chosen a specific car (VIN, make, model, year).

Having these documents ready will significantly speed up the application process.

Understanding the Loan Offer

Once approved, you’ll receive a loan offer outlining the terms. This is where you put your knowledge to use. Pay close attention to:

- The APR: This is the most critical number for comparison.

- The Loan Term: Ensure it aligns with your budget and long-term financial goals.

- The Total Cost of the Loan: This figure, which includes the principal and all interest, gives you the true price of borrowing.

- Any Fees: Look out for origination fees, application fees, or prepayment penalties.

Read every line of the loan agreement before signing. Don’t hesitate to ask questions about anything you don’t understand.

Common Mistakes to Avoid When Financing a Car

Many individuals, in their excitement, overlook crucial details that can lead to higher costs or less favorable terms. Being aware of these common pitfalls can save you from making costly errors.

Not Checking Your Credit Score

Failing to review your credit score and report before applying is a major oversight. You might miss errors that could be dragging your score down, or you might be unaware of a low score that will significantly impact your rates. Knowing your score empowers you to either improve it or manage your expectations.

Only Shopping at the Dealership

Relying solely on dealership financing without exploring outside options is a missed opportunity. While convenient, dealership rates aren’t always the best. Always secure pre-approval from independent lenders to use as a bargaining chip.

Focusing Solely on Monthly Payments

It’s easy to get fixated on a low monthly payment. However, a low payment often comes with a longer loan term and a much higher total interest cost. Always consider the total cost of the loan over its entire duration, not just the monthly installment.

Ignoring the Total Cost of the Loan

This mistake goes hand-in-hand with focusing only on monthly payments. The total cost of the loan includes the principal amount borrowed plus all the interest you’ll pay over the life of the loan. A seemingly small difference in APR can translate into thousands of dollars over several years.

Adding Unnecessary Extras

As mentioned earlier, rolling overpriced or unnecessary add-ons into your loan increases your principal and, consequently, the amount of interest you’ll pay. Be discerning about every additional item presented during the financing process.

Refinancing Your Car Loan: A Second Chance

Even if you’ve already financed a car, it’s not too late to potentially improve your rates. Refinancing your car loan means taking out a new loan to pay off your existing one, ideally at a lower interest rate or with more favorable terms.

Refinancing makes sense if your credit score has significantly improved since you took out the original loan, if market interest rates have dropped, or if you simply found a better offer elsewhere. It can substantially reduce your monthly payments or the total interest you pay over the remaining life of the loan, providing a valuable opportunity for savings. If you’re still weighing your options between buying new or used, our article on (Internal Link Placeholder) can provide further insights.

Conclusion: Your Path to Smart Car Financing

Securing the best car loan finance rates is not about luck; it’s about preparation, knowledge, and strategic action. By understanding the factors that influence rates, diligently working on your credit, shopping around for lenders, and carefully reviewing every offer, you place yourself in a powerful position. This diligent approach can lead to significant savings, freeing up your hard-earned money for other financial goals.

Don’t let the complexity of car financing deter you. Arm yourself with the information from this guide, take proactive steps, and embark on your car-buying journey with confidence. Your informed decisions today will pave the way for a more financially sound tomorrow. For official consumer advice on car buying and loans, resources like the Consumer Financial Protection Bureau (CFPB) offer valuable information and tools. (External Link Placeholder – will link to a relevant CFPB page like https://www.consumerfinance.gov/consumer-tools/auto-loans/)