Unlocking the Best Deals: A Deep Dive into Credit Human Car Loan Rates and Smart Auto Financing

Unlocking the Best Deals: A Deep Dive into Credit Human Car Loan Rates and Smart Auto Financing Carloan.Guidemechanic.com

Navigating the world of auto loans can often feel like deciphering a complex puzzle. With so many lenders, terms, and interest rates to consider, finding the right financing for your next vehicle purchase is crucial. For many, Credit Human stands out as a strong contender, known for its member-focused approach and competitive offerings. But what exactly are Credit Human car loan rates, how are they determined, and how can you secure the best possible deal?

As an expert blogger and professional SEO content writer, my mission is to demystify this process for you. This comprehensive guide will not only explore the intricacies of Credit Human’s auto loan landscape but also equip you with the knowledge and strategies to confidently approach your car financing journey. We’ll delve deep into the factors that influence your rate, walk through the application process, and share insider tips to save you money. Let’s drive into the details!

Unlocking the Best Deals: A Deep Dive into Credit Human Car Loan Rates and Smart Auto Financing

Understanding Credit Human: More Than Just a Bank

Before we dive into the specifics of car loan rates, it’s essential to understand what makes Credit Human unique. Unlike traditional banks, Credit Human is a credit union. This means it’s a not-for-profit financial cooperative owned by its members.

This fundamental difference translates into several benefits. Instead of focusing on maximizing shareholder profits, credit unions typically return profits to members through lower loan rates, higher savings rates, and fewer fees. This member-centric model is a significant reason why many people consider Credit Human for their auto financing needs.

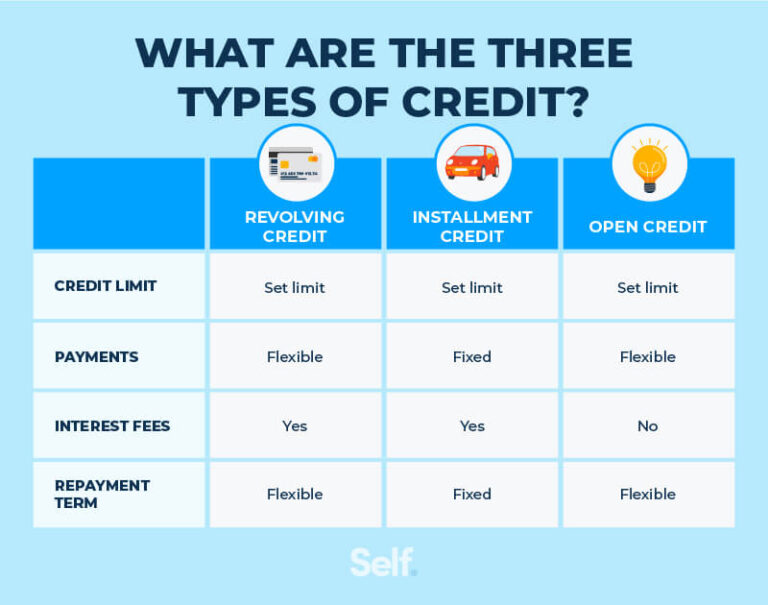

The Foundation of Auto Loans: Key Terms You Need to Know

To truly understand Credit Human car loan rates, let’s first establish a solid understanding of basic car loan terminology. Familiarity with these terms will empower you during your loan application and negotiation.

- Interest Rate: This is the cost of borrowing money, expressed as a percentage of the loan amount. A lower interest rate means you pay less over the life of the loan.

- Annual Percentage Rate (APR): The APR is the total cost of borrowing, including the interest rate and any additional fees, expressed as an annual percentage. It provides a more complete picture of the loan’s cost.

- Loan Term: This refers to the length of time you have to repay the loan, usually expressed in months (e.g., 36, 48, 60, 72 months). A longer term typically means lower monthly payments but more interest paid overall.

- Principal: The original amount of money you borrow before interest and fees are added.

- Down Payment: An upfront sum of money you pay towards the purchase of a car. A larger down payment can reduce your loan amount and potentially secure a lower interest rate.

- Credit Score: A three-digit number representing your creditworthiness. Lenders use it to assess the risk of lending to you. Higher scores generally lead to better rates.

Why Credit Human Stands Out for Car Loans

Credit Human has built a strong reputation for providing competitive auto loan options. Their commitment to their members often translates into tangible advantages when it comes to financing a vehicle.

Based on my experience, many individuals find Credit Human’s approach to be more personal and transparent compared to larger, more impersonal financial institutions. They prioritize building relationships, which can be particularly beneficial if you’re looking for more than just a transaction.

Furthermore, their cooperative structure often allows them to offer rates that are highly competitive in the market. This can lead to significant savings over the life of your car loan.

A Deep Dive: Credit Human Car Loan Rates Explained

Now, let’s get to the core of the matter: Credit Human car loan rates. It’s important to understand that there isn’t a single, fixed rate for everyone. Your specific rate will be influenced by several key factors.

Credit Human, like other lenders, assesses your individual financial profile to determine the risk associated with lending to you. The lower the perceived risk, the more favorable the interest rate you’re likely to receive.

Factors Influencing Your Credit Human Auto Loan Rate

Securing the best possible Credit Human car loan rate hinges on understanding and optimizing these crucial elements. Each factor plays a significant role in the lender’s decision-making process.

1. Your Credit Score and History:

This is arguably the most significant factor. Your credit score (e.g., FICO or VantageScore) is a numerical representation of your creditworthiness. It reflects your payment history, amounts owed, length of credit history, new credit, and credit mix.

A higher credit score signals to Credit Human that you are a responsible borrower with a proven track record of repaying debts. Generally, scores above 700 are considered good, while those above 760 are excellent. Borrowers with excellent credit will almost always qualify for the lowest advertised Credit Human car loan rates. Conversely, a lower score indicates higher risk, resulting in a higher interest rate to compensate the lender for that risk.

2. The Loan Term (Length of the Loan):

The duration over which you choose to repay your loan also impacts your interest rate. Shorter loan terms (e.g., 36 or 48 months) typically come with lower interest rates. While your monthly payments will be higher, you’ll pay less interest overall.

Longer loan terms (e.g., 60, 72, or even 84 months) reduce your monthly payment, making the car more affordable in the short term. However, Credit Human will often charge a slightly higher interest rate for longer terms because the risk of something going wrong (like default or the car depreciating below the loan amount) increases over a longer period.

3. Your Down Payment Amount:

Making a substantial down payment can significantly improve your loan terms. When you put down a larger sum upfront, you reduce the amount you need to borrow.

This lowers the risk for Credit Human, as you have more equity in the vehicle from day one. Lenders are more comfortable offering better rates when the loan-to-value (LTV) ratio is lower. A strong down payment demonstrates your financial commitment and can unlock more favorable auto loan rates.

4. Debt-to-Income (DTI) Ratio:

Your DTI ratio is a measure of your monthly debt payments compared to your gross monthly income. Credit Human will assess this to ensure you can comfortably afford the new car payment in addition to your existing financial obligations.

A lower DTI ratio indicates that you have more disposable income and are less likely to struggle with payments. Lenders typically prefer a DTI ratio below 36%, though it can vary. A high DTI might lead to a higher interest rate or even loan denial, as it suggests you might be overextended financially.

5. Vehicle Information (New vs. Used, Age, Mileage):

The type of vehicle you’re financing also plays a role. New cars generally qualify for lower interest rates compared to used cars. This is because new cars typically have a higher resale value and are less likely to require immediate costly repairs, making them a lower risk for the lender.

For used vehicles, Credit Human will consider the car’s age, mileage, and overall condition. Older cars with high mileage may be seen as a higher risk due to potential mechanical issues and faster depreciation, leading to slightly higher interest rates.

How Credit Human Determines Your Rate: A Member-Focused Approach

Credit Human’s unique credit union structure often means they take a more holistic view of their members. While the factors above are universal, their emphasis on membership can subtly influence the outcome.

- Relationship Banking: If you’re an existing Credit Human member with other accounts (checking, savings, other loans) and a positive financial history with them, this relationship can sometimes work in your favor. They have a clearer picture of your financial habits.

- Membership Benefits: Credit unions are designed to benefit members. This philosophy means they strive to offer competitive rates as a core service. They might have specific programs or discounts available only to members.

- Pre-approval Process: Engaging in Credit Human’s pre-approval process is an excellent way to understand your potential rate before you even step foot in a dealership. This empowers you with a concrete offer, giving you significant leverage.

Current Rate Trends & How to Find Specific Rates

Interest rates are dynamic and influenced by broader economic conditions, including the Federal Reserve’s monetary policy. When the Fed raises its benchmark interest rate, it typically leads to higher borrowing costs across the board, including auto loans. Conversely, rate cuts can lead to lower loan rates.

Pro tips from us: To get the most accurate and up-to-date Credit Human car loan rates, the best approach is always to:

- Visit their Official Website: Credit Human typically publishes their current range of auto loan rates on their website. Look for a dedicated "Rates" or "Auto Loans" section.

- Contact a Loan Officer: Speaking directly with a Credit Human loan officer allows you to discuss your specific situation and get a personalized rate quote. They can also explain any current promotions.

- Use Their Online Pre-qualification Tool: Many lenders, including Credit Human, offer online tools that allow you to get pre-qualified for a loan without a hard credit inquiry. This gives you an idea of your potential rate range.

For general interest rate trends that might influence Credit Human’s offerings, a reliable external source like the Federal Reserve Bank’s website can provide valuable context on current economic conditions and monetary policy decisions.

Pro Tips for Securing the Best Credit Human Car Loan Rate

Based on my experience helping countless individuals navigate auto financing, there are several actionable steps you can take to significantly improve your chances of securing an excellent rate from Credit Human.

1. Know Your Credit Score (and Improve It!):

Before applying for any loan, obtain a copy of your credit report from all three major bureaus (Experian, Equifax, TransUnion). Review it for errors and dispute any inaccuracies. If your score isn’t where you want it, take steps to improve it, such as paying down existing debts, making all payments on time, and avoiding new credit applications. For a deeper understanding of improving your credit score, check out our guide on .

2. Get Pre-Approved Before Shopping:

This is perhaps the most crucial tip. Getting pre-approved by Credit Human gives you a clear understanding of:

- The maximum amount you can borrow.

- The interest rate you qualify for.

- Your estimated monthly payment.

Armed with this information, you become a cash buyer at the dealership, allowing you to negotiate the car’s price separately from the financing. This prevents the dealer from inflating the interest rate.

3. Make a Substantial Down Payment:

As discussed, a larger down payment reduces the loan amount and lowers the risk for Credit Human. Aim for at least 10-20% of the vehicle’s purchase price if possible. This not only lowers your monthly payments but also helps you build equity faster.

4. Choose a Shorter Loan Term (If Affordable):

While lower monthly payments from a longer term can be tempting, remember that shorter terms generally come with lower interest rates and less overall interest paid. If your budget allows, opt for the shortest term you can comfortably afford.

5. Maintain a Low Debt-to-Income Ratio:

Before applying, try to pay down other debts if possible. This will improve your DTI ratio, making you a more attractive borrower to Credit Human.

6. Don’t Be Afraid to Negotiate (Even with a Pre-Approval):

Even with a pre-approval from Credit Human, the dealership might try to offer you their own financing. Compare their offer to Credit Human’s. Sometimes, a dealership might beat your pre-approved rate to close a sale, but having Credit Human’s offer gives you a strong baseline for negotiation.

The Credit Human Application Process: What to Expect

Applying for a Credit Human car loan is generally straightforward, especially if you’re already a member. The process is designed to be efficient and user-friendly.

1. Gather Your Documents:

Before you begin, have the following information readily available:

- Personal identification (Driver’s License, Social Security Number).

- Proof of income (pay stubs, tax returns if self-employed).

- Proof of residence (utility bill, lease agreement).

- Vehicle information (if you’ve already chosen a car – VIN, make, model, year, mileage).

- Trade-in information (if applicable).

2. Apply Online, By Phone, or In-Person:

Credit Human offers multiple convenient ways to apply. You can complete an application online through their website, call their loan department, or visit a local branch to speak with a loan officer directly.

3. Review the Offer:

Once your application is processed, Credit Human will provide you with a loan offer outlining the approved amount, interest rate, and loan term. Review all the details carefully.

4. Finalize the Loan:

If you accept the offer, you’ll sign the necessary paperwork. Credit Human will then disburse the funds directly to you, the dealership, or issue a check.

Common mistakes to avoid are rushing through the application or not fully understanding the terms. Always ask questions if anything is unclear.

Beyond the Rate: Other Factors to Consider with Credit Human

While Credit Human car loan rates are a primary concern, a truly smart financing decision involves looking at the bigger picture.

- Fees and Charges: Always inquire about any potential origination fees, application fees, or prepayment penalties. Credit Human, as a credit union, typically has fewer fees than traditional banks, but it’s always wise to confirm.

- Customer Service and Support: How easy is it to reach a representative if you have questions or issues? Credit Human’s member-centric model usually means excellent customer service.

- Payment Flexibility: Does Credit Human offer flexible payment options, such as bi-weekly payments or the ability to change your payment date if needed?

- Online Account Management: A robust online portal and mobile app can make managing your auto loan payments and tracking your balance incredibly convenient.

Refinancing Your Existing Car Loan with Credit Human

Perhaps you already have a car loan but are unhappy with the interest rate or monthly payment. Credit Human often provides excellent options for refinancing existing auto loans.

When does refinancing make sense?

- Improved Credit Score: If your credit score has significantly improved since you took out your original loan, you might qualify for a much lower rate.

- Lower Interest Rates: If market interest rates have dropped since your initial loan, refinancing can save you money.

- High Original Rate: If you had a less-than-stellar credit score when you first financed, you might have ended up with a high rate that can now be reduced.

- Lower Monthly Payments: Extending the loan term (though this might mean more interest overall) can lower your monthly payments, freeing up cash flow.

Based on my experience, many people overlook refinancing as a powerful tool to save money. If any of these scenarios apply to you, reaching out to Credit Human to explore their refinancing options could be a very wise move.

Member Benefits: More Than Just a Loan

Choosing Credit Human for your car loan often comes with additional perks beyond competitive rates. As a member, you’re part of a community.

- Financial Education: Credit Human often provides resources and workshops to help members improve their financial literacy, manage budgets, and plan for the future.

- Community Involvement: Credit unions are deeply rooted in their communities, often participating in local events and initiatives.

- Other Financial Products: As a member, you gain access to a full suite of financial products, from checking and savings accounts to mortgages and personal loans, often with member-exclusive benefits.

If you’re still weighing your options between new and used vehicles, our article on might offer further insights to help you make an informed decision before applying for your loan.

Conclusion: Driving Towards Smart Auto Financing with Credit Human

Securing the right Credit Human car loan rate is a pivotal step in making your vehicle purchase affordable and sustainable. By understanding the factors that influence your rate, meticulously preparing your application, and leveraging the benefits of being a Credit Human member, you position yourself for success.

Remember, the lowest possible interest rate is within reach if you take the time to build your credit, save for a down payment, and approach the process strategically. Credit Human’s commitment to its members, combined with their competitive auto loan offerings, makes them a strong choice for many looking to finance their next car. Drive confidently, knowing you’ve made an informed decision for your financial future.