Unlocking the Best Deals: Your Comprehensive Guide to Mayo Credit Union Car Loan Rates

Unlocking the Best Deals: Your Comprehensive Guide to Mayo Credit Union Car Loan Rates Carloan.Guidemechanic.com

Are you dreaming of a new car, a reliable used vehicle, or perhaps looking to lower your current auto loan payments? Navigating the world of car financing can feel overwhelming, with countless options and terms to decipher. However, for many, a credit union like Mayo Credit Union offers a refreshing, member-focused alternative to traditional banks.

This comprehensive guide is designed to be your ultimate resource for understanding Mayo Credit Union car loan rates. We’ll delve deep into everything you need to know, from the application process and factors influencing your rate to expert tips for securing the best possible deal. Our goal is to empower you with the knowledge to make informed decisions and drive away with confidence.

Unlocking the Best Deals: Your Comprehensive Guide to Mayo Credit Union Car Loan Rates

Why a Credit Union? The Mayo Advantage for Your Car Loan

When considering where to finance your next vehicle, credit unions often stand out. Unlike banks, which are for-profit entities, credit unions are non-profit financial cooperatives owned by their members. This fundamental difference translates into tangible benefits for you, the borrower.

Based on my extensive experience in consumer finance, credit unions typically offer more competitive interest rates on loans and higher yields on savings accounts. This is because their profits are reinvested back into the organization, benefiting members through better services and more favorable terms. Mayo Credit Union exemplifies this cooperative spirit.

Member-First Philosophy

Mayo Credit Union, like other credit unions, operates with a "people helping people" philosophy. This means their primary focus isn’t on maximizing shareholder profits, but on serving the financial needs of their member-owners. You’ll often find a more personalized and attentive customer service experience compared to larger, more impersonal banking institutions.

This member-first approach can be particularly beneficial when discussing your car loan options. They are often more willing to work with you, understand your unique financial situation, and offer flexible solutions that might not be available elsewhere. It’s about building a relationship, not just processing a transaction.

Potentially Lower Rates and Fees

One of the most compelling reasons to consider Mayo Credit Union for your auto loan is the potential for lower interest rates. Because they operate on a non-profit model, credit unions can pass on savings to their members in the form of reduced rates and fewer, or lower, fees. This can significantly reduce the overall cost of your car loan over its lifetime.

While rates fluctuate, it’s always a smart move to compare Mayo Credit Union’s offerings against other lenders. You might be pleasantly surprised by the savings you could achieve. Even a half-percent difference in APR can translate into hundreds or even thousands of dollars saved over the life of a multi-year car loan.

Decoding Mayo Credit Union Car Loan Rates: What You Need to Know

Understanding car loan rates goes beyond just looking at a number. Several factors influence the rate you’re offered, and being aware of these can help you prepare and potentially secure a better deal. Mayo Credit Union, like any lender, assesses various criteria to determine your eligibility and the specific rate you qualify for.

Pro tips from us: Don’t just focus on the advertised "best rates." These are typically reserved for borrowers with excellent credit scores. It’s crucial to understand what factors you can influence to improve your rate.

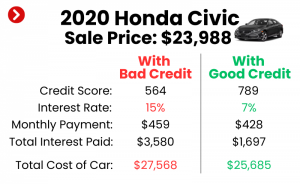

Your Credit Score: The Ultimate Rate Driver

Your credit score is arguably the most significant factor influencing your Mayo Credit Union car loan rate. This three-digit number is a snapshot of your creditworthiness, reflecting your history of borrowing and repaying debt. A higher credit score signals lower risk to lenders, often resulting in more favorable interest rates.

Credit scores generally range from 300 to 850, with scores above 700 typically considered good to excellent. Lenders use various scoring models, but the underlying principle remains the same: responsible credit behavior leads to better scores. For a deeper dive into improving your credit score, check out our in-depth guide on (Internal Link Placeholder 1).

Loan Term: How Long You’ll Pay

The loan term, or the length of time you have to repay the loan, also plays a crucial role in determining your interest rate. Generally, shorter loan terms come with lower interest rates because the lender’s risk is reduced. You’re paying off the principal more quickly.

While a longer loan term might offer lower monthly payments, it typically results in a higher overall interest rate and more interest paid over the life of the loan. It’s a balance between affordability and the total cost of borrowing. Mayo Credit Union will offer various terms, so consider what fits your budget and financial goals.

New vs. Used Car: A Rate Difference

Lenders often differentiate between new and used car loan rates. New cars typically command slightly lower interest rates than used cars. This is primarily because new cars are seen as less risky collateral; they have a predictable value and are less prone to mechanical issues early on.

Used cars, while often more affordable upfront, can carry a slightly higher interest rate due to factors like depreciation, mileage, and potential wear and tear. However, Mayo Credit Union strives to offer competitive rates for both categories, recognizing the diverse needs of its members. Always compare rates for the specific type of vehicle you’re interested in.

Down Payment Amount

Making a substantial down payment can significantly impact your car loan rate and terms. A larger down payment reduces the amount you need to borrow, which lowers the lender’s risk. This can translate into a lower interest rate for you.

Furthermore, a healthy down payment can help you avoid being "upside down" on your loan, where you owe more than the car is worth. This provides a buffer against depreciation and gives you more equity in your vehicle from the start. Mayo Credit Union appreciates borrowers who demonstrate financial stability through a solid down payment.

How to Find Mayo Credit Union’s Current Car Loan Rates

Finding the most up-to-date Mayo Credit Union car loan rates is straightforward. Your best first step is to visit their official website. Most credit unions prominently display their current loan rates for various products, including auto loans, on their site. Look for sections like "Loans," "Auto Loans," or "Rates."

If you can’t find the specific information you need online, or if you prefer a personal touch, don’t hesitate to contact Mayo Credit Union directly. Their loan officers are excellent resources and can provide you with personalized rate quotes based on your specific situation. This is especially useful for understanding any special offers or promotions they might have. For direct information, you can visit their official auto loan page at Mayo Credit Union Auto Loans (External Link Placeholder).

Navigating the Mayo Credit Union Car Loan Application Process

Applying for a car loan at Mayo Credit Union is designed to be a smooth and transparent process. Understanding the steps involved can help you prepare thoroughly and avoid common delays. Based on my experience, preparation is key to a stress-free application.

Common mistakes to avoid are rushing the application without gathering all necessary documents or not checking your credit score beforehand. These can lead to unnecessary setbacks or even a denial.

Step-by-Step Application Guide

- Pre-Approval: This is often the smartest first step. Pre-approval involves submitting a preliminary application to Mayo Credit Union to see how much you qualify for and at what interest rate, before you even start car shopping. It gives you buying power and a clear budget.

- Gather Documents: Once you’re ready to formally apply or have your pre-approval, you’ll need specific documentation.

- Complete the Application: Whether online or in person, fill out the application accurately and completely. Be honest about your financial situation.

- Review and Approval: Mayo Credit Union will review your application, credit history, and supporting documents. They will then inform you of their decision.

- Loan Closing and Funding: Upon approval, you’ll sign the necessary loan documents, and the funds will be disbursed, either directly to you or to the dealership.

Required Documentation

To ensure a seamless application, have the following documents ready:

- Proof of Identity: Government-issued ID (driver’s license, passport).

- Proof of Income: Recent pay stubs, W-2s, or tax returns (if self-employed).

- Proof of Residence: Utility bill, lease agreement, or mortgage statement.

- Social Security Number: For credit checks.

- Vehicle Information (if applicable): Make, model, year, VIN (Vehicle Identification Number) for the car you intend to purchase.

- Current Insurance Information: Proof of auto insurance will be required before you drive off.

Having these documents organized and readily available will significantly speed up the approval process. Mayo Credit Union aims to make this as efficient as possible for their members.

New vs. Used: How Mayo Credit Union Car Loan Rates Differ

The type of vehicle you purchase—brand new or pre-owned—will influence the terms and rates of your Mayo Credit Union car loan. It’s an important distinction that borrowers should understand before they commit.

While the core application process remains similar, the financial specifics can vary. This is due to differing risk assessments associated with new versus used vehicles.

New Car Loan Considerations

Financing a new car often comes with the benefit of slightly lower interest rates, as discussed earlier. New vehicles are considered less risky collateral due to their higher initial value and manufacturer warranties. Additionally, new car loans typically have predictable depreciation curves.

When you finance a new car with Mayo Credit Union, you can expect competitive rates and terms designed to make that brand-new vehicle accessible. However, remember that new cars depreciate rapidly in the first few years, so consider your long-term ownership plans.

Used Car Loan Considerations

Used car loans, while potentially carrying a slightly higher interest rate, offer the advantage of a lower purchase price and slower depreciation after the initial drop. Mayo Credit Union understands the value in purchasing a used vehicle and provides competitive rates tailored for pre-owned vehicles.

When applying for a used car loan, the age and mileage of the vehicle might also play a role in the terms offered. Older vehicles or those with very high mileage could have different rate structures. Always be transparent about the vehicle you’re looking to finance.

Refinancing Your Auto Loan with Mayo Credit Union: A Smart Move?

Perhaps you already have a car loan but are looking for ways to reduce your monthly payments or lower your overall interest paid. Refinancing your auto loan with Mayo Credit Union could be an excellent strategy.

Based on my experience, many people overlook the opportunity to refinance, often paying more interest than necessary. It’s a financial move that can save you significant money over time.

When is Refinancing a Good Idea?

Refinancing makes sense in several scenarios:

- Your Credit Score Has Improved: If your credit score has significantly improved since you first took out your loan, you’re likely eligible for a better interest rate.

- Interest Rates Have Dropped: Market interest rates can fluctuate. If rates are lower now than when you originally financed, refinancing can lock in a better deal.

- You Want Lower Monthly Payments: By extending the loan term (though this might mean more interest overall), you can reduce your monthly payment, freeing up cash flow.

- You Want to Pay Off Faster: Conversely, if you can afford higher payments, refinancing to a shorter term with a lower rate can save you a lot in interest and get you debt-free sooner.

- You Have a High-Interest Loan: If you originally financed through a dealership with a high rate, refinancing with Mayo Credit Union can often secure a more favorable rate.

The Mayo Credit Union Refinancing Process

Refinancing with Mayo Credit Union is similar to applying for a new loan. You’ll submit an application, provide income and identity verification, and they’ll assess your creditworthiness. If approved, Mayo Credit Union will pay off your old loan, and you’ll begin making payments to them under your new, hopefully more advantageous, terms.

It’s a straightforward process that could lead to substantial savings. Don’t hesitate to explore this option if you believe your current loan terms aren’t serving your best interests.

Optimizing Your Credit Score for Superior Mayo Credit Union Car Loan Rates

As we’ve established, your credit score is paramount in securing the best Mayo Credit Union car loan rates. Taking proactive steps to improve it can translate directly into thousands of dollars saved over the life of your loan.

Pro tips from us: Building and maintaining good credit is an ongoing process. Small, consistent efforts yield significant long-term benefits.

Strategies to Boost Your Credit Score

- Pay Bills on Time, Every Time: Payment history is the biggest factor in your credit score. Set up automatic payments or reminders to ensure you never miss a due date.

- Reduce Credit Card Balances: Keep your credit utilization ratio low (the amount of credit you’re using compared to your total available credit). Aim for under 30% utilization.

- Avoid Opening Too Many New Credit Accounts: Each new application can temporarily ding your score. Only apply for credit when absolutely necessary.

- Review Your Credit Report Regularly: Check your credit report for errors or fraudulent activity. You can get a free report annually from AnnualCreditReport.com. Dispute any inaccuracies immediately.

- Maintain a Long Credit History: The longer your positive credit history, the better. Avoid closing old, paid-off accounts, as this can shorten your average credit age.

By consistently applying these strategies, you’ll not only improve your credit score but also demonstrate to Mayo Credit Union that you are a reliable and responsible borrower, paving the way for the most competitive rates.

Beyond the Numbers: Holistic Car Loan Considerations at Mayo CU

While interest rates are undeniably important, a truly smart car loan decision involves looking beyond just the Annual Percentage Rate (APR). Mayo Credit Union offers several other advantages and considerations that contribute to the overall value of your auto financing.

Common mistakes to avoid are solely focusing on the monthly payment or neglecting to read the fine print. A holistic view ensures you understand the full scope of your commitment.

Loan Terms and Flexibility

Mayo Credit Union understands that life happens. They often offer more flexible loan terms and repayment options compared to larger, more rigid institutions. This could include options for bi-weekly payments, which can help you pay off your loan faster and save on interest, or possibilities for payment adjustments during unexpected financial hardship.

Discussing your needs and potential future scenarios with a loan officer can reveal the flexibility embedded in their loan products. This personalized approach is a hallmark of credit union service.

Exceptional Customer Service

The member-centric approach of Mayo Credit Union extends to its customer service. When you have questions about your loan, need assistance, or encounter a financial challenge, you’re more likely to receive personalized, empathetic support. This level of service can be invaluable, especially during a long-term commitment like a car loan.

You’re not just a number; you’re a valued member. This distinction can make a significant difference in your overall borrowing experience.

Additional Services and Protections

Many credit unions, including Mayo Credit Union, offer additional services that can enhance your auto loan and protect your investment. These might include:

- Guaranteed Asset Protection (GAP) Insurance: This covers the "gap" between what your insurance company pays if your car is totaled or stolen and the amount you still owe on the loan.

- Payment Protection: This can cover your loan payments in the event of job loss, disability, or other qualifying life events.

- Extended Warranties: Sometimes offered through partnerships, these can provide peace of mind beyond the manufacturer’s warranty.

Always inquire about these supplementary services. While they add to the cost, they can provide crucial financial security and peace of mind. For a deeper dive into understanding different types of auto insurance, read our article on (Internal Link Placeholder 2).

Pro Tips and Common Pitfalls When Securing a Mayo Credit Union Car Loan

To ensure you get the absolute best deal and experience when financing your car with Mayo Credit Union, consider these expert tips and be aware of common mistakes to avoid.

Pro Tips for Car Loan Success

- Get Pre-Approved: As mentioned, pre-approval gives you a clear budget and allows you to negotiate with the dealership as a cash buyer. This empowers you to focus on the car price, not just the monthly payment.

- Shop Around (Even Within CUs): While Mayo Credit Union offers great rates, it’s always wise to compare their offer with a couple of other credit unions or even a local bank. This ensures you’re getting the most competitive rate available to you.

- Read the Fine Print: Always, always read the entire loan agreement before signing. Understand all terms, conditions, fees, and penalties. If something isn’t clear, ask for clarification.

- Don’t Just Focus on the Monthly Payment: While monthly affordability is crucial, also consider the total cost of the loan over its term. A lower monthly payment over a longer term often means paying significantly more in interest overall.

- Be Prepared to Negotiate: Even with competitive credit union rates, there might be room for negotiation, especially on dealer-added products or services. Knowledge is power.

Common Pitfalls to Avoid

- Not Checking Your Credit Score: Going into a loan application blind is a recipe for disappointment. Know your score and clean up any errors beforehand.

- Extending the Loan Term Too Much: While it lowers monthly payments, a 72- or 84-month loan often means paying far more interest than the car is worth, and you risk being upside down on your loan for a long time.

- Skipping Pre-Approval: Without pre-approval, you lose your negotiating leverage at the dealership and might be swayed into less favorable financing terms.

- Ignoring Additional Fees: Be aware of any origination fees, documentation fees, or prepayment penalties. Mayo Credit Union is known for transparency, but it’s always good to confirm.

- Impulse Buying: Don’t rush into a car purchase. Take your time, research vehicles, and secure financing beforehand. A rushed decision can be a costly one.

Conclusion: Drive Away Confidently with Mayo Credit Union

Securing a car loan is a significant financial decision, and choosing the right lender is paramount. Mayo Credit Union stands out as an excellent option for its member-focused philosophy, competitive rates, flexible terms, and exceptional customer service. By understanding the factors that influence your loan rate, preparing for the application process, and implementing our expert tips, you can significantly enhance your chances of getting the best possible deal.

Whether you’re purchasing a new car, a reliable used vehicle, or looking to refinance your existing auto loan, Mayo Credit Union offers a transparent and supportive environment to help you achieve your goals. Take the time to visit their website, explore their current offerings, and speak with their knowledgeable loan officers. Empower yourself with knowledge, apply with confidence, and drive away knowing you’ve made a smart financial choice with Mayo Credit Union.