Unlocking the Best Deals: Your Ultimate Guide to Occu Used Car Loan Rates

Unlocking the Best Deals: Your Ultimate Guide to Occu Used Car Loan Rates Carloan.Guidemechanic.com

Embarking on the journey to purchase a used car is an exciting prospect, offering fantastic value and a wide array of choices. However, for many, the financing aspect can feel like navigating a complex maze. One name that often comes up in the conversation about favorable car loans, especially for used vehicles, is Occu – a credit union known for its member-focused approach. Understanding Occu used car loan rates is crucial to making an informed decision that saves you money and aligns with your financial goals.

As an expert blogger and professional SEO content writer, I’ve delved deep into the world of auto financing. My mission today is to equip you with an unparalleled, in-depth understanding of how Occu approaches used car loans, what influences their rates, and most importantly, how you can position yourself to secure the most competitive financing available. This isn’t just about numbers; it’s about empowerment.

Unlocking the Best Deals: Your Ultimate Guide to Occu Used Car Loan Rates

The Occu Advantage: Why Consider a Credit Union for Your Used Car Loan?

Before we dive into the specifics of rates, it’s essential to understand the fundamental difference that sets credit unions like Occu apart from traditional banks. Unlike banks, which are for-profit entities, credit unions are non-profit financial cooperatives owned by their members. This structural difference translates directly into benefits for you, the borrower.

Based on my experience, credit unions often offer more competitive interest rates on loans and better terms on savings accounts because they return their profits to members in the form of these advantages, rather than distributing them to shareholders. This philosophy extends directly to their auto loan offerings, making Occu a compelling option for financing a used car. Their primary goal is to serve their members’ financial well-being, not to maximize corporate profits.

Decoding Occu Used Car Loan Rates: The Factors That Matter Most

When you apply for a used car loan with Occu, several critical factors come into play that ultimately determine the interest rate you’ll be offered. Understanding these elements is your first step towards securing the best possible deal. It’s not a one-size-fits-all scenario; your individual financial profile and the vehicle itself will heavily influence the outcome.

Your Credit Score: The Cornerstone of Your Loan Rate

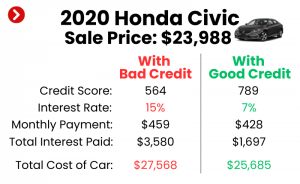

Without a doubt, your credit score is the single most influential factor in determining the interest rate on any loan, including Occu used car loans. This three-digit number acts as a financial report card, reflecting your history of borrowing and repayment. A higher credit score signals to Occu that you are a responsible borrower with a strong track record of fulfilling financial obligations.

Lenders use credit scores to assess risk. A strong score, typically above 700, suggests a lower risk of default, which in turn allows Occu to offer you lower interest rates. Conversely, a lower credit score indicates a higher perceived risk, leading to higher rates to compensate the lender for that increased risk. This is why cultivating and maintaining good credit is paramount when preparing for any significant loan.

The Loan Term: Balancing Monthly Payments and Total Cost

The loan term refers to the duration over which you agree to repay the loan, typically expressed in months (e.g., 36, 48, 60, or 72 months). This choice has a direct impact on both your monthly payment and the total interest you’ll pay over the life of the loan.

Generally, longer loan terms result in lower monthly payments, making the car more "affordable" on a month-to-month basis. However, a longer term also means you’ll be paying interest for a greater period, leading to a higher total cost of the loan. Shorter terms, while having higher monthly payments, often come with lower interest rates and result in significantly less total interest paid. Finding the right balance between a manageable monthly payment and minimizing the total interest cost is a key decision point.

Vehicle Age and Mileage: Assessing Collateral Risk

Unlike new car loans, used car loan rates can also be influenced by the specifics of the vehicle itself. Occu, like other lenders, considers the age and mileage of the used car you intend to purchase. This is because the vehicle serves as collateral for the loan.

Older vehicles or those with very high mileage are generally perceived as having a higher risk of mechanical issues or faster depreciation. This can make them riskier collateral for a lender. Consequently, loans for older, higher-mileage used cars might carry slightly higher interest rates compared to loans for newer, low-mileage used vehicles, even with the same borrower credit score.

Your Down Payment: Showing Financial Commitment

Making a down payment on your used car purchase signifies your financial commitment and reduces the amount you need to borrow. From Occu’s perspective, a larger down payment reduces their risk exposure. If you default on the loan, the amount they need to recover from selling the repossessed vehicle is smaller.

Pro tips from us: A substantial down payment can often translate into a lower interest rate, as it demonstrates your financial stability and reduces the loan-to-value (LTV) ratio. It also immediately builds equity in your vehicle and lowers your monthly payments. Even a modest down payment can make a noticeable difference in your overall loan terms.

Your Relationship with Occu: Membership Perks

As a credit union, Occu values its members. Your existing relationship with Occu can sometimes play a role in securing more favorable loan rates. If you’re an established member with other accounts (like checking, savings, or other loans) in good standing, Occu might view you as a more loyal and reliable borrower.

Some credit unions offer loyalty discounts on interest rates to long-standing members or those who set up automatic payments from an Occu account. While not always a guaranteed discount, your membership status and overall financial relationship can certainly contribute to a smoother application process and potentially better terms.

Navigating the Occu Used Car Loan Application Process

Applying for a used car loan with Occu is designed to be straightforward, but preparation is key. Knowing what to expect and what documents you’ll need can significantly streamline the process.

Eligibility Requirements: Are You Occu-Ready?

To apply for a loan with Occu, you first need to be a member. Membership eligibility typically revolves around a common bond, such as where you live, work, worship, or attend school. For Occu, this often includes specific counties or affiliations. It’s a quick process to join, usually requiring a small deposit into a savings account.

Beyond membership, standard loan eligibility criteria apply. You’ll need to be of legal age (18 or older), a U.S. citizen or permanent resident, and have a verifiable source of income. Occu will assess your debt-to-income ratio to ensure you can comfortably manage the new loan payments alongside your existing financial obligations.

Documents You’ll Need: Prepare for a Smooth Application

Being prepared with the right documentation is crucial for a swift application process. Common mistakes to avoid are showing up without all necessary papers, which can cause frustrating delays. Here’s a typical checklist of what Occu will likely request:

- Proof of Identity: A valid government-issued ID (driver’s license, state ID, passport).

- Proof of Income: Recent pay stubs (typically 2-3 months), W-2s, or tax returns if you’re self-employed.

- Proof of Residency: Utility bill, lease agreement, or mortgage statement.

- Vehicle Information: The specific year, make, model, VIN (Vehicle Identification Number), and mileage of the used car you intend to purchase.

- Proof of Insurance: You’ll need to show proof of comprehensive and collision insurance before the loan is finalized.

- Occu Membership Details: Your account number and membership information.

The Application Journey: Step-by-Step

Once you have your documents ready and confirm your eligibility, the application process generally follows these steps:

- Join Occu: If you’re not already a member, this is your first step. It’s usually a quick online or in-branch process.

- Pre-Approval Application: This is a highly recommended step. You can apply for pre-approval online, by phone, or in person. Occu will review your credit history and financial information to give you an estimate of how much you can borrow and at what interest rate. This allows you to shop for a car with confidence, knowing your budget.

- Vehicle Selection: With your pre-approval in hand, you can confidently shop for a used car that fits your budget and needs.

- Final Loan Application: Once you’ve found the perfect car, you’ll finalize the loan details with Occu, providing the vehicle-specific information.

- Closing and Funding: After approval, you’ll sign the loan documents. Occu will then disburse the funds, either directly to you, the dealership, or the private seller.

Pro Strategies for Securing the Best Occu Used Car Loan Rates

While some factors like the economy are beyond your control, there’s plenty you can do to influence the interest rate you receive on your Occu used car loan. These strategies are born from years of observing successful borrowers.

Boosting Your Credit Score: A Long-Term Investment

As discussed, your credit score is paramount. If your score isn’t where you’d like it to be, take steps to improve it before applying for a loan. This isn’t an overnight fix, but even small improvements can lead to better rates.

Actionable advice includes paying all your bills on time, reducing existing debt (especially credit card balances), and avoiding opening new credit accounts just before applying for a car loan. Regularly checking your credit report for errors and disputing them is also a smart move. A higher score translates directly into lower perceived risk for Occu, and thus, lower interest rates for you.

Making a Substantial Down Payment: Reduce Your Borrowing

We’ve touched on this, but it bears repeating: a larger down payment is your friend. Aim for at least 10-20% of the vehicle’s purchase price if possible. This not only reduces the total amount you need to borrow but also signals financial strength to Occu.

A higher down payment often means Occu views the loan as less risky, potentially leading to a better interest rate. Furthermore, it reduces your monthly payments and lessens the likelihood of being "upside down" on your loan (owing more than the car is worth) early in the ownership period.

Choosing the Right Loan Term: Balance is Key

While lower monthly payments can be tempting with longer loan terms, remember the trade-off in total interest paid. Carefully consider your budget and repayment capacity.

Pro tips from us: If you can comfortably afford a higher monthly payment, opting for a shorter loan term (e.g., 48 or 60 months instead of 72) will almost certainly save you a significant amount in interest over the life of the loan. Occu’s loan officers can help you model different scenarios to find the optimal term for your financial situation.

Considering a Co-Signer: If Your Credit Needs a Boost

If your credit score is still developing or has taken a hit, a co-signer with excellent credit can be a game-changer. A co-signer essentially guarantees the loan, promising to repay it if you default.

This significantly reduces Occu’s risk, often allowing you to qualify for a much lower interest rate than you would on your own. However, this is a serious commitment for the co-signer, as the loan will appear on their credit report, and their credit will be affected if payments are missed. Use this option wisely and only with someone you trust implicitly.

Negotiating with the Dealer: Leverage Your Pre-Approval

One of the biggest advantages of getting pre-approved for an Occu used car loan is the leverage it gives you at the dealership. With a pre-approval in hand, you walk into the dealership as a cash buyer, essentially.

You know exactly how much you can spend and what your interest rate will be. This allows you to focus purely on negotiating the vehicle price, rather than being swayed by the dealer’s financing offers. Sometimes, dealers may even try to beat your pre-approved rate to secure the sale. This is a powerful position to be in.

Beyond the Rate: Understanding Your Occu Loan Terms

While the interest rate is a major component, it’s not the only aspect of your Occu used car loan that warrants close attention. A comprehensive understanding of the full loan terms ensures there are no surprises down the road.

APR vs. Interest Rate: Know the Difference

It’s crucial to understand the distinction between the interest rate and the Annual Percentage Rate (APR). The interest rate is simply the cost of borrowing the principal amount. The APR, however, represents the total cost of the loan over a year, including the interest rate plus any additional fees or charges associated with the loan.

When comparing loan offers, always look at the APR, as it provides a more accurate picture of the true cost of borrowing. Occu, like all reputable lenders, will clearly disclose the APR.

Fees and Charges: What to Look For

While credit unions are known for their transparency and often fewer fees than traditional banks, it’s still wise to inquire about any potential charges. These might include:

- Application Fees: Less common for auto loans, but worth asking.

- Documentation Fees: For processing paperwork.

- Late Payment Fees: If you miss a payment.

- Prepayment Penalties: Very rare for consumer auto loans from credit unions, but always confirm that you can pay off your loan early without penalty. This is a significant benefit if you plan to accelerate your payments.

Payment Schedule and Flexibility: Occu’s Options

Understand your payment schedule (monthly, bi-weekly) and how you can make payments. Occu typically offers convenient options like online payments, automatic deductions from your Occu account, or payments by mail.

It’s also worth asking about any flexibility in case of financial hardship. While not guaranteed, some credit unions may offer options like payment deferrals in certain situations, highlighting their member-centric approach.

Common Mistakes to Avoid When Applying for an Occu Used Car Loan

Even the most prepared individuals can fall into common pitfalls. Based on my experience helping countless individuals navigate loan processes, here are some mistakes to actively avoid:

Not Checking Your Credit Score: The Blind Spot

A significant error is not checking your credit score and report before applying. This leaves you vulnerable to surprises and unable to correct potential errors that could unfairly lower your score.

Always pull your credit report from all three major bureaus (Experian, Equifax, TransUnion) at least a few months before you plan to apply. This gives you time to dispute any inaccuracies and understand your starting point. You can get free copies of your credit report annually from AnnualCreditReport.com.

Skipping Pre-Approval: Losing Your Leverage

Failing to get pre-approved for an Occu used car loan is a missed opportunity. Without pre-approval, you lose your negotiation power at the dealership and might feel pressured into accepting less favorable financing terms offered by the dealer.

Pre-approval arms you with a clear budget and an independent interest rate, allowing you to compare it directly with any dealer financing options. It puts you in control of the buying process.

Focusing Only on Monthly Payments: The Tunnel Vision Trap

One of the most common mistakes is becoming fixated solely on the monthly payment amount. While a low monthly payment is appealing, it can often hide a longer loan term and a significantly higher total interest cost.

Always ask for the total cost of the loan, including all interest and fees, across different loan term scenarios. A slightly higher monthly payment for a shorter term can save you thousands over the life of the loan.

Ignoring the Total Cost of the Loan: The Hidden Expense

This ties into the previous point. Many borrowers overlook the true, long-term cost of their loan. The initial interest rate might seem low, but if it’s stretched over 72 or even 84 months, the cumulative interest can be substantial.

Always calculate the total amount you will pay back (principal + total interest) before committing to a loan. This holistic view helps you make a truly financially sound decision.

Refinancing Your Existing Used Car Loan with Occu

Perhaps you already have a used car loan but didn’t get the best rate, or your financial situation has improved since you first financed your vehicle. Occu also offers refinancing options that could save you money.

When to Consider Refinancing: Is It Time for a Change?

You might consider refinancing your used car loan with Occu if:

- Your Credit Score Has Improved: A significantly higher score since your original loan could qualify you for a much lower interest rate.

- Interest Rates Have Dropped: Market rates may have decreased, making better offers available.

- You Want a Lower Monthly Payment: Refinancing to a longer term (though be mindful of total interest) could reduce your monthly outlay.

- You Want to Pay Off Your Loan Faster: Refinancing to a shorter term could accelerate your repayment, potentially with a lower rate.

- You’re Paying Too Much: If you feel your current rate is uncompetitive, it’s worth exploring Occu’s options.

The Benefits of Refinancing with Occu: A Fresh Start

Refinancing your used car loan with Occu can bring several compelling benefits. Based on my experience, the primary advantage is often a lower interest rate, which directly translates to reduced monthly payments or significant savings on the total cost of the loan over time.

Additionally, refinancing can allow you to change your loan term, either extending it for lower monthly payments or shortening it to pay off the car faster. Occu’s member-first approach means they are often willing to work with you to find a solution that genuinely improves your financial standing.

Occu’s Refinancing Process: Streamlined Savings

The refinancing process with Occu is very similar to applying for a new loan. You’ll need to provide updated financial information and details about your current loan and vehicle. Occu will review your credit and offer you new terms.

If approved and you accept the new terms, Occu will pay off your old loan, and you’ll begin making payments to Occu under your new, hopefully more favorable, terms. It’s a relatively simple process that can lead to substantial long-term savings.

Why Occu Stands Out for Used Car Financing

In a crowded financial landscape, Occu consistently distinguishes itself as a premier choice for used car financing. Their core values are truly reflected in their loan products and member services.

Member-Centric Approach: You Come First

Unlike traditional banks, Occu’s fundamental structure as a credit union means their focus is squarely on the financial well-being of their members. This translates into personalized service, a willingness to understand individual circumstances, and a commitment to offering fair and competitive products. You’re not just a customer; you’re a co-owner.

Competitive Rates: Savings in Your Pocket

Due to their non-profit status and lower operating costs compared to large banks, Occu often provides highly competitive interest rates on used car loans. These favorable rates directly contribute to lower monthly payments and reduced total interest paid over the life of your loan, putting more money back into your pocket.

Personalized Service: Beyond the Transaction

Pro tips from us: One of the standout features of credit unions like Occu is the personalized service you often receive. Loan officers are typically more accessible and willing to take the time to explain options, answer questions, and guide you through the process. This human touch can be invaluable, especially for first-time borrowers or those with unique financial situations.

Community Focus: Investing in Local Success

Occu is deeply rooted in the communities it serves. By choosing to finance your used car with Occu, you’re not just getting a loan; you’re supporting a local institution that reinvests in the community through various initiatives and services. This creates a positive feedback loop, strengthening the local economy for everyone.

Pro Tips from Our Experience

Having navigated countless car loan scenarios, here are some consolidated pro tips to ensure you secure the best possible Occu used car loan rates:

- Be Patient and Prepared: Don’t rush into a loan. Take time to improve your credit, save for a down payment, and gather all necessary documents.

- Utilize Pre-Approval: It’s your secret weapon for negotiation and clarity.

- Understand the Full Cost: Always look at the APR and the total amount you’ll pay over the loan term, not just the monthly payment.

- Ask Questions: Don’t hesitate to ask Occu’s loan officers about anything you don’t understand. They are there to help you.

- Consider Automatic Payments: Setting up auto-pay from your Occu account can sometimes lead to small interest rate reductions and ensures you never miss a payment.

- Maintain Good Credit Post-Loan: Your financial habits continue to matter. Consistently making on-time payments will further strengthen your credit for future endeavors.

Conclusion: Drive Away with Confidence and the Best Occu Used Car Loan Rates

Securing a used car loan doesn’t have to be a daunting experience. By understanding the factors that influence Occu used car loan rates, strategically preparing your finances, and leveraging the member-centric approach of a credit union, you can drive away with confidence, knowing you’ve secured the best possible financing for your next vehicle.

Occu offers a compelling combination of competitive rates, personalized service, and a commitment to its members’ financial well-being. By following the advice outlined in this comprehensive guide, you are well-equipped to navigate the process, avoid common pitfalls, and ultimately achieve your goal of owning a used car with financing that truly works for you. Don’t just get a loan; get a smart loan with Occu.

Disclaimer: This article provides general information about Occu used car loan rates and financing. Specific loan terms, eligibility criteria, and rates are subject to change and depend on individual financial circumstances and Occu’s current offerings. Always contact Occu directly or visit their official website for the most accurate and up-to-date information.

Internal Link Suggestion 1: For more insights on managing your credit, read our article: Understanding Your Credit Score: The Key to Better Loans

Internal Link Suggestion 2: Planning your car purchase? Check out our Essential Car Loan Application Checklist

External Link Suggestion: To learn more about the benefits of credit unions, visit MyCreditUnion.gov