Unlocking the Best Drives: A Comprehensive Guide to LAFCU Car Loan Rates

Unlocking the Best Drives: A Comprehensive Guide to LAFCU Car Loan Rates Carloan.Guidemechanic.com

Embarking on the journey to purchase a new vehicle is an exciting prospect. Whether it’s the smell of a brand-new interior or the practicality of a reliable pre-owned car, securing the right financing is often the key to turning that dream into a reality. In the world of auto loans, LAFCU Car Loan Rates stand out as a highly competitive option, offering a unique blend of community focus and financial advantage.

As an expert blogger and professional SEO content writer, I understand the importance of making informed financial decisions. This comprehensive guide will delve deep into everything you need to know about LAFCU’s auto loan offerings. Our goal is to equip you with the knowledge to navigate the application process confidently, secure the best possible rates, and ultimately, drive away with a deal that makes sense for your budget.

Unlocking the Best Drives: A Comprehensive Guide to LAFCU Car Loan Rates

What Makes LAFCU Different? Understanding the Credit Union Advantage

Before we dive into the specifics of LAFCU car loan rates, it’s crucial to understand what LAFCU is and why choosing a credit union for your auto financing can be incredibly beneficial. LAFCU, like all credit unions, is a not-for-profit financial cooperative owned by its members. This fundamental difference sets it apart from traditional banks.

Unlike banks, which operate to generate profits for shareholders, credit unions return their earnings to members through lower interest rates on loans, higher yields on savings, and reduced fees. This member-centric approach often translates directly into more favorable terms for products like auto loans. When you choose LAFCU, you’re not just a customer; you’re a part-owner, and that relationship often comes with significant financial perks.

Demystifying LAFCU Car Loan Rates: The Core Factors

Understanding how LAFCU car loan rates are determined is the first step toward securing an optimal deal. Several key factors influence the interest rate you’ll be offered. By understanding these elements, you can take proactive steps to improve your eligibility for the most competitive rates.

Let’s break down the primary components that LAFCU, and indeed most lenders, consider. Each factor plays a vital role in assessing your creditworthiness and the overall risk associated with lending you money.

1. Your Credit Score: The Ultimate Predictor

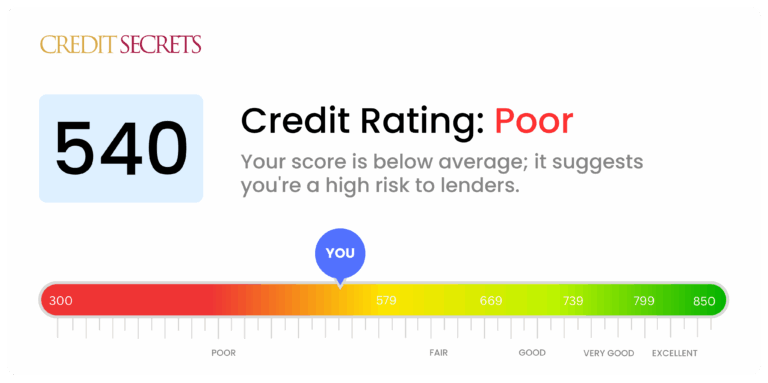

Your credit score is arguably the most significant factor in determining your LAFCU auto loan interest rate. This three-digit number, generated by credit bureaus, is a snapshot of your financial responsibility. A higher credit score indicates a lower risk to the lender, typically resulting in lower interest rates.

LAFCU, like other lenders, uses your credit score to gauge your likelihood of repaying the loan on time. Based on my experience, individuals with excellent credit (generally 720 and above) consistently qualify for the lowest advertised rates. If your score is lower, don’t despair; there are still options, but the rates might be slightly higher to reflect the increased risk.

2. The Loan Term: Short-Term Gains, Long-Term Savings

The loan term refers to the length of time you have to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72 months). While a longer loan term might offer lower monthly payments, it almost always results in paying more interest over the life of the loan. This is a common trade-off that borrowers often face.

Conversely, a shorter loan term usually comes with a lower interest rate, as the lender’s money is tied up for a shorter period. Pro tips from us: If your budget allows for higher monthly payments, opting for a shorter term can save you a significant amount in interest over time. LAFCU offers various terms, so it’s worth exploring the impact of each on your total cost.

3. Your Down Payment: Showing Your Commitment

A down payment is the initial amount of money you pay upfront for the vehicle. Making a substantial down payment reduces the amount you need to borrow, which in turn lowers the lender’s risk. This reduced risk often translates into more attractive LAFCU interest rates.

Beyond the rate, a larger down payment also builds immediate equity in your vehicle and can help you avoid being "upside down" on your loan (owing more than the car is worth). Aiming for at least 10-20% of the vehicle’s purchase price as a down payment is generally recommended to secure the most favorable terms and financial stability.

4. Vehicle Type and Age: New vs. Used

The type and age of the vehicle you intend to purchase also play a role in LAFCU car loan rates. New cars generally command slightly lower interest rates than used cars. This is primarily because new cars typically depreciate slower initially, have warranties, and present less risk of mechanical issues.

Used cars, while often more affordable upfront, can carry a slightly higher interest rate due to their age, mileage, and potential for unforeseen repairs. However, LAFCU offers competitive rates for both new and used vehicles, so it’s always worth getting a quote tailored to your specific choice.

5. Market Conditions: The Bigger Picture

Broader economic factors and the overall interest rate environment can influence LAFCU car loan rates. When the Federal Reserve adjusts its benchmark interest rates, it often has a ripple effect on consumer lending rates, including auto loans. While this factor is largely out of your control, it’s good to be aware that rates can fluctuate over time.

LAFCU aims to keep its rates competitive regardless of market shifts, leveraging its credit union model to pass savings onto its members. However, understanding the general economic landscape can help you decide if it’s an opportune time to finance a vehicle.

Types of LAFCU Car Loans: Finding Your Fit

LAFCU offers a range of auto loan products designed to meet diverse needs. Understanding the different types available can help you determine which option best suits your specific situation. Each loan type has distinct features tailored to various vehicle acquisition scenarios.

Whether you’re buying from a dealership, a private seller, or looking to improve your existing loan terms, LAFCU likely has a solution. Let’s explore the common categories of LAFCU auto loans.

1. New Car Loans

Designed for brand-new vehicles purchased from a dealership, LAFCU’s new car loans typically feature competitive rates and flexible terms. These loans often have the lowest interest rates due to the lower perceived risk associated with new vehicles.

LAFCU works with various dealerships, making the process seamless for members. You can often get pre-approved through LAFCU before stepping onto the lot, giving you significant leverage in negotiations.

2. Used Car Loans

If you’re in the market for a pre-owned vehicle, LAFCU offers robust used car loan options. These loans can apply to vehicles purchased from dealerships or even private sellers. While rates might be slightly higher than new car loans, LAFCU’s competitive edge as a credit union often means better deals than traditional banks.

It’s important to note that age and mileage limits may apply to used car financing. Always check LAFCU’s specific requirements for used vehicle loans to ensure your chosen car qualifies.

3. Auto Loan Refinancing

Perhaps you already have a car loan but are looking for better terms. Refinancing a car loan with LAFCU can be a smart financial move. If your credit score has improved since you first took out your loan, or if market rates have dropped, refinancing could significantly lower your interest rate and monthly payment.

Pro tips from us: Refinancing can also be beneficial if you want to shorten your loan term to pay off the car faster, or if you need to extend it to reduce your monthly burden. LAFCU makes the refinancing process straightforward, often saving members hundreds or even thousands of dollars over the life of their loan.

The LAFCU Car Loan Application Process: A Step-by-Step Guide

Securing a car loan with LAFCU is a relatively straightforward process, especially if you come prepared. Understanding each step can alleviate stress and ensure a smooth experience. Our guide will walk you through the essential stages, from becoming a member to driving off the lot.

Remember, preparation is key to a successful application and securing the best LAFCU car loan rates. Gathering your documents and understanding the requirements beforehand will save you time and effort.

Step 1: Become a LAFCU Member

Since LAFCU is a credit union, the first step is to become a member. Membership eligibility typically involves living, working, or worshipping in a specific geographical area, or being related to an existing member. LAFCU serves communities in Michigan, and their website provides clear guidelines on who can join.

Joining is usually a simple process, often requiring a small deposit into a savings account. Once you’re a member, you gain access to all of LAFCU’s financial products and services, including their competitive auto loans.

Step 2: Get Pre-Approved for Your Loan

Car loan pre-approval with LAFCU is one of the most powerful tools you have as a car buyer. Pre-approval means LAFCU has reviewed your financial information and determined how much they are willing to lend you, at what interest rate, before you even choose a specific car. This gives you immense bargaining power at the dealership.

With a pre-approval in hand, you walk into the dealership knowing your budget and your financing terms. This allows you to focus solely on negotiating the car’s price, rather than getting caught up in the financing details offered by the dealer. Common mistakes to avoid are letting the dealership control the financing discussion without having your own pre-approval.

Step 3: Prepare Your Documents

Whether you’re applying for pre-approval or the final loan, you’ll need a few key documents. Having these ready will expedite the LAFCU loan application process.

Typically, you’ll need:

- Proof of Identity: Valid government-issued ID (driver’s license, passport).

- Proof of Income: Recent pay stubs, tax returns, or bank statements.

- Proof of Residency: Utility bill or lease agreement.

- Vehicle Information (if applicable): Make, model, VIN, and purchase price.

Step 4: Submit Your Application

LAFCU offers convenient ways to apply for your car loan. You can typically apply online through their website, over the phone, or in person at one of their branches. The online application is often the quickest and most convenient method.

Fill out the application completely and accurately. Any missing or incorrect information could delay the approval process. If you have questions, LAFCU’s loan officers are usually very helpful and can guide you through the forms.

Step 5: Loan Decision and Closing

Once your application is submitted, LAFCU will review your information, check your credit, and provide a loan decision. If approved, you’ll receive the final terms, including your LAFCU interest rates, loan amount, and repayment schedule.

Upon acceptance, you’ll sign the necessary paperwork, and the funds will be disbursed. If you’re purchasing from a dealership, LAFCU can often coordinate directly with them to finalize the transaction.

Pro Tips for Securing the Best LAFCU Car Loan Rates

While LAFCU generally offers competitive rates, there are always strategies you can employ to ensure you get the absolute best deal possible. Based on my experience in financial advising, these tactics can make a significant difference in your overall loan cost.

Implementing these tips can not only save you money but also streamline your car buying experience. Let’s explore how to optimize your chances for the most favorable LAFCU car loan rates.

- Boost Your Credit Score: Before you even think about applying, check your credit report for errors and work on improving your score. Pay down existing debt, make all payments on time, and avoid opening new lines of credit. Even a few points can move you into a better rate tier. For more tips on improving your credit score, check out our detailed guide on .

- Save for a Larger Down Payment: As discussed, a larger down payment reduces the loan amount and signals financial stability to LAFCU, often leading to lower rates. Aim for at least 20% if possible.

- Choose a Shorter Loan Term: While it means higher monthly payments, a shorter loan term almost always comes with a lower interest rate, significantly reducing the total interest paid over the life of the loan.

- Get Pre-Approved: This cannot be stressed enough. Pre-approval from LAFCU gives you a firm offer, allowing you to negotiate the car price without dealer financing pressure. It also shows you are a serious buyer.

- Leverage LAFCU Membership Benefits: As a member, inquire about any special promotions or discounts on LAFCU auto loans. Credit unions often have loyalty programs or limited-time offers that can further reduce your rate.

- Don’t Forget About Co-Signers: If your credit score isn’t ideal, a co-signer with excellent credit can help you qualify for better LAFCU interest rates. Just ensure both parties understand the responsibilities involved.

Common Mistakes to Avoid When Applying for a Car Loan

Even experienced borrowers can make missteps during the car loan process. Avoiding these common pitfalls can save you money, time, and potential headaches. Common mistakes to avoid are those that can negatively impact your financial standing and the terms of your loan.

Being aware of these traps will empower you to make smarter decisions throughout your car buying journey.

- Not Checking Your Credit Report: Many people skip this crucial step. Always review your credit report for inaccuracies before applying. Errors can unfairly lower your score and lead to higher interest rates.

- Skipping Pre-Approval: As highlighted, not getting pre-approved leaves you vulnerable to dealer financing tactics that might not be in your best interest. It takes away your negotiation leverage.

- Focusing Only on Monthly Payments: While monthly payments are important, fixating solely on them can lead to longer loan terms and significantly more interest paid over time. Always consider the total cost of the loan.

- Ignoring the Total Cost of the Loan: This includes the principal, interest, and any fees. A low monthly payment can be deceptive if it’s stretched over 7 or 8 years, resulting in a much higher overall cost.

- Not Understanding All Fees: Be sure to ask LAFCU about any origination fees, application fees, or other charges associated with the loan. Transparency is key.

- Accepting the First Offer: Even with pre-approval, always compare LAFCU’s rates with other reputable lenders. While LAFCU is highly competitive, a quick comparison can confirm you’re getting the best deal.

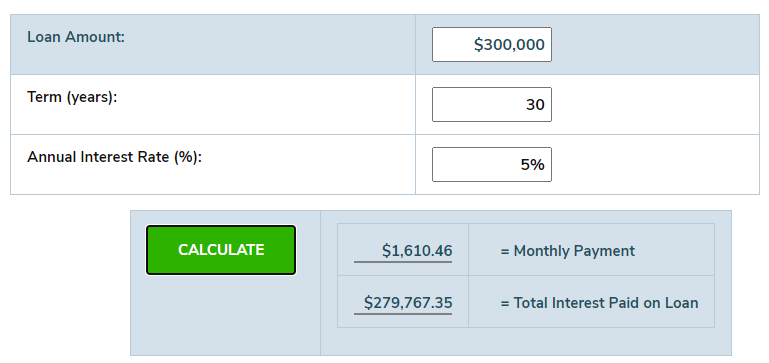

Using LAFCU Car Loan Calculators & Tools

LAFCU, like most modern financial institutions, provides online tools to help you plan your purchase. A LAFCU car loan calculator is an invaluable resource for estimating your potential monthly payments and understanding the impact of different loan terms and interest rates.

These calculators allow you to input various scenarios—such as different loan amounts, interest rates, and repayment periods—to see how they affect your budget. This practical step can help you set realistic expectations and refine your search for a vehicle that fits comfortably within your financial parameters. Utilizing these tools early in your process can prevent surprises later on.

Refinancing Your Car Loan with LAFCU: A Fresh Start

Even if you already have a car loan, it’s never too late to optimize your financing. Refinancing your car loan with LAFCU can be a smart financial move if your circumstances have changed or if you initially accepted less favorable terms. This process involves taking out a new loan to pay off your existing one, ideally at a lower interest rate or with more suitable terms.

When is refinancing a good idea?

- Improved Credit Score: If your credit has significantly improved since you got your original loan, you might qualify for a much lower interest rate.

- Lower Market Rates: General interest rates might have dropped since your initial loan, making refinancing attractive.

- Reduce Monthly Payments: Refinancing to a lower rate or extending the loan term can decrease your monthly outlay.

- Shorten Loan Term: If you want to pay off your car faster, you can refinance to a shorter term, often at a lower rate, and save on total interest.

The process for refinancing with LAFCU is similar to applying for a new loan. You’ll submit an application, provide necessary documents, and LAFCU will assess your eligibility for new, improved terms. If you’re unsure about the different types of car financing, our article on offers further insights.

Frequently Asked Questions (FAQs) about LAFCU Car Loans

To further assist you, here are answers to some common questions about LAFCU auto loans.

- Q: Do I need to be a LAFCU member to apply for a car loan?

- A: Yes, you must be a LAFCU member to take advantage of their auto loan offerings. Membership is usually straightforward and can be initiated at the time of your loan application.

- Q: How long does the LAFCU loan application process take?

- A: Often, pre-approval decisions can be made within a few hours or one business day, especially if you apply online and have all your documents ready. The final loan closing depends on various factors but is typically swift.

- Q: Can I get a LAFCU car loan with bad credit?

- A: While a good credit score helps secure the best rates, LAFCU, as a credit union, is often more flexible and willing to work with members across a broader credit spectrum than traditional banks. They may offer options or advice to improve your chances.

- Q: Does LAFCU finance private party car sales?

- A: Yes, LAFCU typically offers financing for vehicles purchased from private sellers, not just dealerships. You’ll need to provide vehicle information and ensure it meets their eligibility criteria.

- Q: What is the minimum loan amount for a LAFCU auto loan?

- A: Minimum loan amounts can vary, so it’s best to check directly with LAFCU or their website for current policies.

- Q: Can I apply for a LAFCU car loan entirely online?

- A: Yes, LAFCU provides a robust online application platform, allowing you to complete most, if not all, of the process digitally for your convenience.

For more general information on auto loans and responsible borrowing, you can visit the Consumer Financial Protection Bureau (CFPB) at https://www.consumerfinance.gov/.

Drive Away Confidently with LAFCU

Navigating the world of car loans can seem daunting, but with the right information, it becomes a clear path to your next vehicle. LAFCU offers a compelling option for auto financing, combining competitive LAFCU car loan rates with the personalized service and member-first philosophy of a credit union. By understanding the factors that influence your rate, preparing thoroughly, and leveraging the tips outlined in this guide, you can confidently secure a loan that fits your budget and lifestyle.

Don’t settle for less than the best. Explore what LAFCU has to offer and take the wheel of your next car with a smart, financially sound decision. Your dream car is within reach, and LAFCU is ready to help you get there.