Unlocking the Best Gesa Car Loan Rates: Your Ultimate Guide to Smart Auto Financing

Unlocking the Best Gesa Car Loan Rates: Your Ultimate Guide to Smart Auto Financing Carloan.Guidemechanic.com

Navigating the world of car loans can feel like a complex journey, but securing the right financing is crucial for driving away with confidence. If you’re considering a vehicle purchase in the Pacific Northwest, Gesa Credit Union likely stands out as a strong contender for your auto financing needs. With a reputation for member-focused service and competitive offerings, understanding Gesa car loan rates is your first step towards making an informed decision.

This comprehensive guide is designed to be your ultimate resource, breaking down everything you need to know about Gesa’s auto loan options. We’ll delve into how rates are determined, the application process, and expert strategies to ensure you secure the most favorable terms. Our goal is to empower you with the knowledge to not just get a loan, but to get the best loan for your financial situation.

Unlocking the Best Gesa Car Loan Rates: Your Ultimate Guide to Smart Auto Financing

What Makes Gesa Credit Union a Smart Choice for Auto Loans?

Gesa Credit Union isn’t just another financial institution; it’s a member-owned cooperative with deep roots in the communities it serves. This fundamental difference often translates into a more personalized experience and, potentially, more attractive financial products, including car loans. Unlike traditional banks, credit unions typically prioritize their members’ financial well-being over shareholder profits.

Based on my experience in the financial landscape, this cooperative model can lead to several advantages for borrowers. Gesa often reinvests its earnings back into the credit union, offering lower loan rates, higher savings rates, and reduced fees compared to many commercial banks. This commitment to its members’ financial health makes them a compelling option for anyone seeking a car loan. Their focus extends beyond just lending money; it’s about fostering financial stability within the community.

Understanding Gesa Car Loan Rates: The Core Factors at Play

When you apply for a car loan, the interest rate you’re offered isn’t a random number. It’s a carefully calculated figure influenced by several key factors. Understanding these elements is paramount to knowing what to expect and, more importantly, how to improve your standing for a better rate. Gesa, like other lenders, evaluates a range of criteria to assess your creditworthiness and the overall risk of the loan.

Let’s explore the primary determinants that will shape your Gesa car loan rate:

Your Credit Score: The Ultimate Predictor

Without a doubt, your credit score is the single most significant factor influencing your car loan rate. This three-digit number is a snapshot of your financial reliability, indicating how well you’ve managed debt in the past. Lenders use it to gauge the likelihood of you repaying your loan on time.

A higher credit score signals to Gesa that you are a low-risk borrower, making them more willing to offer you their most competitive interest rates. Conversely, a lower score suggests a higher risk, which typically results in a higher interest rate to compensate the lender for that increased risk. Pro tips from us: always check your credit score and report before applying for any significant loan. It allows you to identify and correct any errors, and gives you a clear picture of where you stand.

The Loan Term: How Long You’ll Be Paying

The loan term refers to the length of time you have to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72 months). This choice significantly impacts both your monthly payment and the total interest you’ll pay over the life of the loan. While longer terms offer lower monthly payments, they often come with a higher overall interest cost because the lender is taking on risk for a longer period.

Shorter loan terms, on the other hand, usually feature slightly lower interest rates but result in higher monthly payments. This is because the loan is repaid quicker, reducing the lender’s exposure to risk. When considering Gesa car loan rates, weigh the trade-off between affordable monthly payments and the total cost of the loan over time.

Your Down Payment: Showing Your Commitment

A down payment is the initial amount of money you pay upfront for the vehicle. Providing a substantial down payment reduces the amount you need to borrow, which can positively influence your interest rate. Lenders view a larger down payment as a sign of your financial commitment and reduces their risk.

Additionally, a larger down payment means you’re financing less, leading to lower monthly payments and less interest paid over the life of the loan. It also helps prevent you from being "upside down" on your loan, where you owe more than the car is worth. This financial prudence can directly translate into better Gesa car loan rates.

Vehicle Age and Type: New vs. Used

The type of vehicle you’re purchasing also plays a role in determining your interest rate. New cars generally qualify for lower interest rates compared to used cars. This is because new vehicles typically hold their value better initially, are less prone to mechanical issues, and are considered lower risk for the lender.

Used cars, while often more affordable upfront, can come with slightly higher interest rates due to their depreciation, potential for mechanical issues, and varied histories. However, Gesa offers competitive rates for both new and used vehicles, making it crucial to compare their specific offerings for each category. Ensure you’re transparent about the vehicle you intend to purchase during the application process.

Your Relationship with Gesa: Member Benefits

As a member-owned credit union, Gesa often rewards its existing members. If you’ve been a long-standing member with other accounts (like checking, savings, or other loans) in good standing, this relationship might work in your favor. Established members often have an advantage when it comes to securing the most competitive Gesa car loan rates.

This loyalty can be a significant factor in their decision-making process. Building a strong financial relationship with your credit union can unlock benefits that might not be available to new applicants. It’s always worth discussing your existing membership during your loan inquiry.

Types of Gesa Car Loans Available

Gesa Credit Union offers a variety of auto loan products designed to meet different needs, whether you’re buying a brand-new vehicle, a pre-owned gem, or looking to refinance an existing loan. Understanding these options is key to choosing the right path for your specific situation.

Here are the primary types of car loans you can typically find at Gesa:

- New Car Loans: These loans are for purchasing brand-new vehicles directly from a dealership. They often come with the most attractive interest rates and flexible terms due to the vehicle’s inherent value and warranty coverage. Gesa aims to make buying your dream new car an accessible reality.

- Used Car Loans: If you’re in the market for a pre-owned vehicle, Gesa provides competitive financing for used cars. While rates might be slightly higher than new car loans, they are still designed to be affordable. They assess the vehicle’s age, mileage, and condition to determine the loan terms.

- Refinancing Car Loans: Already have a car loan with another lender? Gesa offers refinancing options that could potentially lower your interest rate, reduce your monthly payments, or shorten your loan term. This is a fantastic opportunity to save money over the life of your loan, especially if your credit score has improved since you first financed your vehicle.

- Lease Buyout Loans: For those who are at the end of a car lease and love their vehicle, Gesa can provide financing to purchase the car outright. This allows you to own the vehicle you’ve been driving, often at a pre-determined residual value, and convert your monthly lease payments into equity.

Each of these loan types is tailored to specific scenarios, ensuring that you can find a suitable financing solution at Gesa Credit Union. It’s always best to discuss your individual needs with a loan officer to explore the best fit.

The Gesa Car Loan Application Process: A Step-by-Step Guide

Applying for a car loan doesn’t have to be intimidating. Gesa Credit Union strives to make the process as straightforward and transparent as possible for its members. By understanding the steps involved, you can approach your application with confidence and efficiency.

Here’s a breakdown of the typical Gesa car loan application journey:

Step 1: Gather Your Documents and Information

Preparation is key to a smooth application. Before you even begin, collect all the necessary paperwork. This usually includes:

- Personal Identification: Driver’s license, social security number, proof of address.

- Income Verification: Recent pay stubs, W-2 forms, tax returns (especially if self-employed).

- Employment Information: Employer’s name, address, and contact details.

- Vehicle Information (if known): Make, model, year, VIN, and purchase price.

Having these documents readily available will significantly speed up the application process.

Step 2: Consider Pre-Approval

One of the smartest moves you can make is getting pre-approved for a loan before you even step onto a dealership lot. Pre-approval means Gesa has reviewed your financial information and determined how much they are willing to lend you, along with an estimated interest rate. This gives you immense bargaining power as a cash buyer.

With a pre-approval in hand, you know your budget and can focus solely on negotiating the car’s price, rather than getting caught up in financing details at the dealership. Common mistakes to avoid are waiting until you’re at the dealership to think about financing, as this can put you under pressure to accept less favorable terms.

Step 3: Submit Your Application

Gesa offers several convenient ways to apply for a car loan:

- Online: Their website typically features an easy-to-use online application portal, allowing you to apply from the comfort of your home.

- In-Branch: Visiting a Gesa branch allows you to speak directly with a loan officer who can guide you through the process and answer any questions.

- By Phone: Some credit unions offer phone applications for added convenience.

Choose the method that best suits your comfort level. Be thorough and accurate with all information provided to avoid delays.

Step 4: Await Approval and Closing

Once your application is submitted, Gesa will review your financial information, run a credit check, and assess your overall eligibility. This process can range from a few hours to a few business days, depending on the complexity of your application and current volume.

If approved, you’ll receive a loan offer outlining the interest rate, term, and monthly payment. You’ll then proceed to the closing, where you sign the necessary loan documents, and the funds are disbursed. This can often happen directly with the dealership if you’re working with one, or directly to you for a private sale. For more detailed advice on improving your credit score, check out our guide on Boosting Your Credit Score for Better Loan Rates.

Maximizing Your Chances for the Best Gesa Car Loan Rates

While Gesa Credit Union aims to offer competitive rates, there are proactive steps you can take to position yourself for the absolute best terms. Securing a lower interest rate can save you hundreds, even thousands, of dollars over the life of your loan.

Here are expert strategies to help you maximize your potential for favorable Gesa car loan rates:

- Improve Your Credit Score: This is paramount. Pay all your bills on time, keep credit card balances low, and avoid opening too many new credit accounts before applying for a car loan. A higher score directly translates to lower rates. For more information on understanding and improving your credit, visit a trusted source like Experian’s Credit Education Hub for valuable insights and tools.

- Save for a Larger Down Payment: As discussed, a substantial down payment reduces the loan amount and signals financial responsibility to the lender. Aim for at least 10-20% of the vehicle’s purchase price if possible.

- Consider a Shorter Loan Term: While it means higher monthly payments, a shorter loan term often comes with a lower interest rate, saving you money in the long run. Evaluate your budget to see if you can comfortably afford a shorter term.

- Shop Around (Even with Gesa in Mind): While you’re focused on Gesa, it’s always wise to compare their offer with one or two other lenders. This ensures you’re getting a truly competitive rate and gives you leverage if you need to negotiate.

- Negotiate the Vehicle Price First: Separate the car purchase from the financing. Focus on getting the best possible price on the vehicle before discussing loan terms. This prevents the dealership from manipulating the numbers.

- Understand Your Budget: Before you even look at cars, know what you can truly afford for a monthly payment, including insurance, fuel, and maintenance. Don’t stretch your budget for a car that will put you in financial strain.

By implementing these strategies, you’ll demonstrate strong financial acumen, making you a highly attractive borrower for Gesa, and significantly increasing your chances of securing the best possible car loan rates.

Gesa’s Member Benefits and Financial Tools

Beyond competitive car loan rates, Gesa Credit Union provides a suite of member benefits and financial tools that can enhance your overall financial well-being, even after you’ve driven off the lot. These resources underscore their commitment to their members.

Gesa often offers:

- Financial Counseling: Access to financial experts who can help you budget, manage debt, and plan for future financial goals. This can be invaluable, especially if you’re navigating a large purchase like a car.

- Online Banking & Mobile App: Convenient access to your accounts, allowing you to monitor your loan, make payments, and manage other Gesa products from anywhere.

- Automatic Payment Options: Setting up automatic payments for your car loan ensures you never miss a payment, which is crucial for maintaining a good credit score and avoiding late fees.

- Insurance Services: Some credit unions, including Gesa, may offer car insurance services or partnerships, allowing you to bundle and potentially save.

- Other Loan Products: As a full-service financial institution, Gesa offers various other loans and credit lines that can complement your financial journey. If you’re exploring other financing options, read our comparison of Credit Unions vs. Banks: Where to Get Your Next Loan.

Leveraging these tools can make managing your car loan and your finances much easier, reinforcing the value of being a Gesa member.

Real-World Scenarios and Expert Insights on Gesa Car Loans

Let’s illustrate how different factors can impact Gesa car loan rates with a couple of real-world scenarios. Based on my years observing lending practices, these examples highlight the importance of your financial profile.

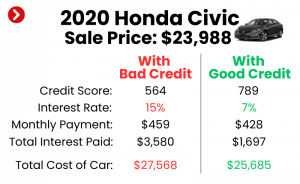

Consider Borrower A, who has an excellent credit score (760+), a stable job history, and offers a 20% down payment on a new car. Gesa is likely to offer them their lowest advertised rates, perhaps in the 4-6% range, depending on market conditions. Their monthly payment will be manageable, and the total interest paid over a 60-month term will be minimal.

Now, imagine Borrower B, with a fair credit score (620-670), a shorter employment history, and a desire for a zero-down payment. While Gesa may still approve their loan, the interest rate could be significantly higher, perhaps in the 8-12% range. This higher rate means a larger portion of their monthly payment goes towards interest, and the total cost of the car will be substantially more expensive over the loan term.

These scenarios clearly demonstrate that a strong financial standing directly translates to more affordable financing. Even a difference of a few percentage points on your interest rate can equate to thousands of dollars saved over the life of a car loan. It underscores why taking steps to improve your credit and save for a down payment is so vital.

Common Questions About Gesa Car Loans

To further equip you with knowledge, here are answers to some frequently asked questions about Gesa car loans:

How long does Gesa car loan approval typically take?

Approval times can vary. For online applications, you might receive a decision within minutes or a few business hours. In-branch applications, especially if all documents are ready, can also be quite swift, often within the same day. However, complex applications might take longer.

Can I apply for a Gesa car loan with a co-signer?

Yes, Gesa generally allows co-signers. If you have limited credit history or a lower credit score, a co-signer with excellent credit can significantly improve your chances of approval and help you secure a lower interest rate. Both your and your co-signer’s credit will be considered.

What if my credit isn’t perfect? Can I still get a Gesa car loan?

Gesa, as a credit union, is often more flexible than traditional banks. While a perfect credit score is ideal, they consider your overall financial picture, including your relationship with the credit union, income stability, and ability to repay. It’s always worth discussing your situation with a loan officer.

Are there any application fees for Gesa car loans?

Typically, Gesa does not charge application fees for car loans. However, always confirm this during your inquiry or application process. Be aware of potential fees during the closing process, although these are usually minimal and clearly disclosed.

Can I get a loan for a private party car purchase?

Yes, Gesa Credit Union often provides financing for vehicles purchased from private sellers, not just dealerships. The process might involve a bit more paperwork to verify the vehicle’s title and condition, but it’s a common and valuable option.

Drive Away Confidently with Gesa

Securing a car loan is a significant financial decision, and understanding all the moving parts is essential. By focusing on your credit health, making a strategic down payment, and choosing the right loan term, you’re well on your way to unlocking the best Gesa car loan rates. Gesa Credit Union stands as a strong partner in your journey, offering not just competitive financing but also a member-focused approach and valuable financial resources.

Don’t just get a car loan; get a smart car loan. Take the knowledge you’ve gained from this guide, prepare thoroughly, and confidently explore your options with Gesa. Your ideal vehicle, financed on favorable terms, is well within reach. Visit Gesa Credit Union’s official website or stop by a branch today to discuss your auto financing needs and take the next step towards driving your dream car.