Unlocking the Best Hapo Car Loan Rates: Your Ultimate Guide to Smart Vehicle Financing

Unlocking the Best Hapo Car Loan Rates: Your Ultimate Guide to Smart Vehicle Financing Carloan.Guidemechanic.com

Are you in the market for a new or used car? Perhaps you’re considering refinancing your existing auto loan to save money. When it comes to vehicle financing, securing the best possible interest rate can translate into significant savings over the life of your loan. For many in the Pacific Northwest, Hapo Credit Union emerges as a prominent and trusted option.

But what exactly are Hapo car loan rates, and how can you ensure you’re getting the most competitive offer? This comprehensive guide will demystify everything you need to know about Hapo’s auto loan offerings. We’ll dive deep into the factors influencing your rate, explore the application process, and share expert tips to help you drive away with the best financing deal.

Unlocking the Best Hapo Car Loan Rates: Your Ultimate Guide to Smart Vehicle Financing

Our goal is to equip you with the knowledge to make informed decisions, transforming what can often be a complex process into a clear, straightforward path. Let’s embark on this journey to smarter car financing with Hapo.

What Makes Hapo Credit Union Different for Car Loans?

Before we delve into the specifics of Hapo car loan rates, it’s crucial to understand the fundamental difference between a credit union like Hapo and a traditional bank. This distinction isn’t just semantic; it directly impacts the benefits you, as a member, can receive.

Credit unions are not-for-profit financial cooperatives owned by their members. Unlike banks, which primarily aim to generate profits for shareholders, credit unions focus on providing financial services and returns to their members. This member-centric philosophy often translates into more favorable loan rates, lower fees, and personalized service.

Hapo Credit Union, deeply rooted in its community, embodies this principle. Their commitment to members means they strive to offer competitive rates and flexible terms, making them a strong contender for your auto financing needs. Based on my experience in the financial sector, this foundational difference is often a key reason why credit union rates can be more attractive than those from larger, profit-driven institutions.

Understanding Hapo Car Loan Rates: The Core Factors

When you apply for an auto loan, Hapo—like any lender—will assess several key factors to determine your eligibility and the interest rate you’ll be offered. These factors are not arbitrary; they reflect the level of risk the lender perceives. Understanding them is your first step towards securing an optimal Hapo car loan rate.

Let’s break down the most influential elements:

Your Credit Score: The Primary Determinant

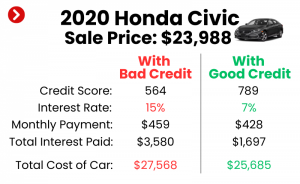

Your credit score is arguably the single most important factor influencing your car loan rate. This three-digit number provides a snapshot of your creditworthiness, indicating your history of managing debt responsibly. A higher credit score signals less risk to lenders.

Individuals with excellent credit scores (typically 760+) will consistently qualify for the lowest available Hapo car loan rates. These borrowers have demonstrated a consistent ability to pay their debts on time, making them highly desirable to lenders. They often receive premium offers with the most attractive terms.

Conversely, those with good (700-759), fair (650-699), or poor (below 650) credit scores will likely face higher interest rates. The increased rate compensates the lender for the perceived higher risk of default. It’s essential to know your credit score before applying, as it gives you a realistic expectation of the rates you might receive.

Loan Term: How Long You’ll Be Paying

The loan term refers to the length of time you have to repay your loan, typically expressed in months (e.g., 36, 48, 60, 72, or even 84 months). The chosen term has a direct impact on both your monthly payment and the total interest you’ll pay over the life of the loan.

Generally, shorter loan terms come with slightly lower interest rates. This is because the lender is exposed to risk for a shorter period. While a shorter term means higher monthly payments, it results in significantly less total interest paid, saving you money in the long run.

Longer loan terms, on the other hand, offer lower monthly payments, making a more expensive vehicle potentially more affordable on a monthly basis. However, the trade-off is often a slightly higher interest rate and a much greater total amount of interest paid over the extended period. It’s a balance between immediate affordability and long-term cost.

New vs. Used Vehicles: A General Rate Difference

The type of vehicle you intend to finance—whether it’s brand new or pre-owned—can also influence the interest rate Hapo offers. Typically, new car loans tend to have slightly lower interest rates than used car loans.

This difference stems from several factors. New cars are seen as less risky collateral because they haven’t depreciated as much, and their value is more predictable. They also often come with manufacturer warranties, reducing potential repair costs for the owner.

Used cars, while often more budget-friendly in their purchase price, generally carry a slightly higher risk for lenders. Their value can depreciate more rapidly, and their mechanical condition might be less predictable, especially for older models. Consequently, Hapo car loan rates for used vehicles might be a touch higher to account for this increased risk.

Vehicle Age and Mileage: Specifics for Used Car Rates

Delving deeper into used car financing, the age and mileage of the specific vehicle play a crucial role. An older vehicle with higher mileage is generally considered a higher risk than a newer used car with low mileage.

Lenders assess the potential for mechanical issues and the vehicle’s resale value. A car that is, for instance, 10 years old with 150,000 miles, will typically command a higher interest rate than a 3-year-old car with 30,000 miles. This is because the older, higher-mileage vehicle has a greater likelihood of needing costly repairs and a lower potential resale value, increasing the lender’s exposure.

Hapo, like other lenders, will factor these specifics into their rate determination for used vehicles. It’s not just "used" but how used the car is that matters.

Your Down Payment: Showing Your Commitment

Making a substantial down payment on your vehicle purchase can positively influence your Hapo car loan rate. A larger down payment reduces the amount you need to borrow, which in turn lowers the lender’s risk. When you have more equity in the vehicle from day one, you are less likely to default on the loan.

A significant down payment also demonstrates your financial commitment to the purchase. It signals to Hapo that you have the financial discipline to save and invest in your vehicle, making you a more attractive borrower. While not always mandatory, a down payment of 10-20% of the vehicle’s purchase price is often recommended to secure better rates and reduce your overall loan cost.

Membership History and Relationship: The Credit Union Advantage

One of the unique benefits of financing through a credit union like Hapo is the potential influence of your existing relationship. If you’ve been a long-standing member with other accounts (checking, savings, other loans) in good standing, this can sometimes work in your favor.

While not explicitly advertised as a rate-determining factor in the same way a credit score is, a strong, positive relationship with Hapo can build trust and rapport. This might subtly contribute to a more favorable rate offer or more flexible terms, especially in marginal cases. Pro tips from us: Building a strong financial relationship with your credit union can unlock benefits beyond just auto loans.

Current Market Conditions: Beyond Hapo’s Control

While Hapo strives to offer competitive rates, they operate within the broader economic landscape. General interest rate trends, largely influenced by the Federal Reserve’s monetary policy, impact all lenders. When the Federal Reserve raises its benchmark interest rate, borrowing costs across the board tend to increase.

Conversely, during periods of economic stimulus, rates might trend downwards. Hapo adjusts its loan offerings to remain competitive within these prevailing market conditions. For the most current economic indicators influencing interest rates, we often refer to resources like the Federal Reserve’s official website. Understanding these larger trends can help you decide if it’s a good time to finance or refinance.

Hapo Car Loan Options: Tailored to Your Needs

Hapo Credit Union offers a range of auto loan products designed to meet different member needs. Knowing these options can help you select the one that best aligns with your financial situation and vehicle purchasing plans.

New Car Loans: Driving Off the Lot with Confidence

Hapo’s new car loans are specifically designed for brand-new vehicles purchased from a dealership. These loans typically offer some of the lowest interest rates available, reflecting the lower risk associated with financing a new asset.

Terms can be quite flexible, often extending up to 84 months, though shorter terms are usually recommended for optimal savings. When considering a new car loan, Hapo will look at the vehicle’s MSRP, your credit profile, and your ability to make a down payment. They aim to make the process smooth, allowing you to focus on the excitement of your new purchase.

Used Car Loans: Smart Financing for Pre-Owned Vehicles

For those opting for a pre-owned vehicle, Hapo provides competitive used car loan options. As discussed, rates for used cars can be slightly higher than new car rates, and the terms might be more restrictive depending on the vehicle’s age and mileage.

Hapo often sets limits on the maximum age or mileage for vehicles they will finance. For example, a vehicle older than 10 years or with more than 120,000 miles might have different eligibility criteria or higher rates. It’s crucial to check these specifics with Hapo directly before you finalize your used car purchase.

Refinancing Your Existing Auto Loan with Hapo: Saving Money Today

Refinancing your current auto loan with Hapo can be a powerful financial strategy, particularly if your credit score has improved since you first took out your loan, or if current interest rates are lower than what you’re currently paying. Many members find significant savings through this process.

When you refinance, Hapo pays off your old loan, and you start a new loan with them, hopefully at a lower interest rate or with more favorable terms. This can lead to reduced monthly payments or a substantial decrease in the total interest paid over time. It’s a fantastic way to optimize your existing debt and free up cash flow.

The Pre-Approval Process: Your Secret Weapon

One of the most valuable tools in your car buying journey is getting pre-approved for a loan. Hapo offers a straightforward pre-approval process that can make a world of difference.

Pre-approval means Hapo has reviewed your financial information and determined the maximum loan amount you qualify for, along with an estimated interest rate. This empowers you by turning you into a cash buyer at the dealership. You’ll know your budget before you start shopping, and you can negotiate the vehicle price with confidence, separate from the financing discussion. This separation often leads to a better overall deal.

Navigating the Hapo Car Loan Application Process

Applying for a car loan might seem daunting, but Hapo strives to make it as user-friendly as possible. Understanding the steps and preparing beforehand can significantly streamline the experience.

Gathering Your Documents: Be Prepared

Before you even start the application, gather essential documents. This preparation can prevent delays. Common requirements include:

- Proof of Identity: Driver’s license or state ID.

- Proof of Income: Recent pay stubs (1-2 months), W-2s, or tax returns if self-employed.

- Proof of Residence: Utility bill or lease agreement.

- Vehicle Information: If you’ve already found a car, details like the VIN, make, model, and mileage.

- Current Loan Information: If refinancing, your current lender’s statement and payoff amount.

Having these readily available will make the application process much smoother and faster.

Online Application vs. In-Person: Choose Your Comfort

Hapo Credit Union typically offers multiple ways to apply for an auto loan. You can usually complete an application online from the comfort of your home, which is convenient and often quick. This is ideal if you prefer a digital experience and have all your documents scanned and ready.

Alternatively, you can visit a Hapo branch and apply in person. This allows you to speak directly with a loan officer, ask questions, and receive personalized guidance. Some individuals prefer this face-to-face interaction, especially if they have unique financial circumstances. Both methods aim to provide the same great service.

What Happens After You Apply?

Once you submit your application, Hapo will review your financial information, including your credit report. They will assess all the factors we discussed earlier – credit score, income, debt-to-income ratio, and the specifics of the vehicle.

You’ll typically receive a decision within a short period, sometimes even the same day for online applications. If approved, you’ll be presented with the loan terms, including your Hapo car loan rate, loan amount, and repayment schedule. If you have questions, this is the time to ask for clarification.

Common Mistakes to Avoid During Application

Based on my experience, people often make a few common mistakes that can hinder their loan application or lead to less favorable terms. Firstly, not checking your credit report beforehand is a big one. You might discover errors that could negatively impact your score.

Secondly, applying for too many loans at once can hurt your credit score with multiple hard inquiries. Focus on one or two strong contenders like Hapo. Lastly, underestimating your budget for the vehicle and associated costs (insurance, maintenance) can lead to financial strain down the road. Always consider the total cost of ownership, not just the monthly payment.

Maximizing Your Chances for the Best Hapo Car Loan Rates

Securing a low interest rate isn’t always about luck; it’s often about strategic preparation and smart financial habits. Here are our pro tips to help you get the most competitive Hapo car loan rates:

Improve Your Credit Score

This is paramount. If you’re not in a rush, take steps to boost your credit score before applying. Pay bills on time, reduce existing debt, and avoid opening new credit accounts. Even a small increase in your score can translate into significant savings on interest. For a deeper dive into improving your credit score, check out our comprehensive guide on .

Save for a Larger Down Payment

As mentioned, a substantial down payment reduces the amount you need to borrow and signals financial responsibility. Aim for at least 10-20% of the vehicle’s purchase price. This not only lowers your monthly payments but also makes you a more attractive borrower for the best rates.

Choose a Shorter Loan Term (If Affordable)

While lower monthly payments can be tempting, if your budget allows, opt for a shorter loan term. You’ll likely get a slightly lower interest rate, and you’ll pay far less in total interest over the life of the loan. Always calculate the total cost, not just the monthly payment.

Become a Hapo Member Early

If you’re considering Hapo for your auto loan, becoming a member well in advance can be beneficial. Building a relationship with the credit union, even if it’s just through a savings account, can demonstrate your commitment and potentially offer advantages down the line.

Shop Around and Compare Offers

Even if you’re set on Hapo, it’s always wise to compare their offer with one or two other reputable lenders. This comparison ensures you’re getting a truly competitive rate. Moreover, use Hapo’s pre-approval to your advantage when negotiating at the dealership. Knowing your financing options empowers you significantly.

Beyond the Rate: Other Hapo Car Loan Benefits

While the interest rate is a critical factor, it’s not the only benefit Hapo Credit Union offers with its auto loans. Their member-centric approach extends to several value-added services that can enhance your overall car ownership experience.

Excellent Member Service

Credit unions are renowned for their personalized and attentive member service, and Hapo is no exception. When you have questions about your loan, need assistance, or want to explore other financial products, you’ll often find a more direct and helpful interaction compared to larger institutions. This human touch can be invaluable.

Payment Protection Options

Life is unpredictable, and Hapo understands that. They often offer payment protection options, such as Debt Protection. This service can help cover your loan payments in the event of unforeseen circumstances like involuntary unemployment, disability, or even death, providing peace of mind. It’s a small added cost that can offer significant security.

GAP Insurance

Guaranteed Asset Protection (GAP) insurance is another valuable offering. If your car is totaled or stolen, your auto insurance typically pays out the actual cash value of the vehicle, which might be less than what you still owe on your loan due to depreciation. GAP insurance covers this difference, preventing you from being upside down on your loan. Hapo can often provide GAP insurance at a more competitive rate than dealerships.

Extended Warranties

Hapo may also offer options for extended warranties or vehicle service contracts. These can protect you from unexpected repair costs after your manufacturer’s warranty expires. While not directly part of the loan rate, these services are part of a holistic approach to vehicle ownership that Hapo supports, often at member-friendly prices.

Real-World Scenarios and Pro Tips

Let’s look at a couple of scenarios to illustrate how these factors play out and offer some practical advice.

Scenario 1: The First-Time Buyer with Fair Credit

Sarah, a recent college graduate, wants to buy her first used car. Her credit score is 680, considered fair. She has a stable job but limited savings for a large down payment. Hapo offers her a used car loan at 7.5% over 60 months.

- Pro Tip: Instead of immediately accepting, Sarah could aim to make even a small down payment (e.g., 5-10%). She could also consider a slightly older or less expensive used car to reduce the total loan amount. Over 6-12 months, if she diligently pays all her bills on time, her credit score could improve, making refinancing an option for a lower rate later.

Scenario 2: Refinancing to Save Money

Mark has an existing auto loan with a bank at 8.9% interest. His credit score has significantly improved from 650 to 740 since he bought the car two years ago. He approaches Hapo for a refinance.

- Pro Tip: Hapo reviews his improved credit and offers him a new loan at 5.5% over the remaining term. This simple move could save Mark hundreds, if not thousands, of dollars in interest over the next few years. Always check if refinancing is viable if your financial situation has improved or market rates have dropped.

Common mistakes to avoid are not fully understanding the loan terms and conditions. Always read the fine print, ask questions about any fees, and ensure you’re comfortable with the monthly payment and total cost. If you’re weighing your options between new and used vehicles, our article on offers valuable insights.

Hapo Car Loan Rates: A Smart Choice for Your Vehicle Financing

Navigating the world of car loans can feel overwhelming, but understanding the key factors that influence Hapo car loan rates empowers you to make smarter financial decisions. Hapo Credit Union, with its member-focused philosophy, competitive rates, and comprehensive range of services, stands out as an excellent choice for vehicle financing.

By focusing on improving your credit score, making a solid down payment, and understanding the various loan options, you can significantly enhance your chances of securing the best possible rate. Remember, a lower interest rate means more money stays in your pocket, not the lender’s.

Don’t just accept the first offer you receive. Take the time to prepare, understand your options, and leverage the benefits of a trusted financial partner like Hapo. Your dream car, financed intelligently, is within reach.

Conclusion

Securing a favorable auto loan rate is a cornerstone of smart vehicle ownership. We’ve explored the intricacies of Hapo car loan rates, from the fundamental impact of your credit score to the strategic advantages of pre-approval and membership. Hapo Credit Union offers a compelling package for those seeking competitive financing, coupled with a commitment to member service.

By diligently applying the strategies outlined in this guide – focusing on credit health, understanding loan terms, and utilizing Hapo’s diverse offerings – you are well-equipped to achieve a financing outcome that aligns with your financial goals. Take control of your car buying journey; explore Hapo’s auto loan options today and drive away with confidence.